Back taxes do not fix themselves. You can file back taxes online or by mail for previous years and stop penalties from piling up. You can still claim a tax refund for any year within the three year cutoff. You can request an IRS payment plan if you owe more than you can pay today. Filing your tax return protects Social Security benefits and keeps your tax records clean for mortgages, car loans, and business credit. Start with IRS transcripts, W 2s, and 1099s. Use tax software for simple returns and a tax professional for complex income, small business schedules, or multiple years.

Why you should file your past due return now

Filing past due tax returns buys peace of mind and saves real money. Every month you wait, failure to file and failure to pay penalties add to your tax debt and increase interest. You also risk losing refunds the day the three year window closes, which means the U.S. Treasury keeps your money forever. Lenders and landlords read your tax records when you apply for financing or leases, so current filings help you qualify on time. You also protect Social Security benefits because reporting self employment income adds quarters of coverage that count toward future payments.

Avoid interest and penalties

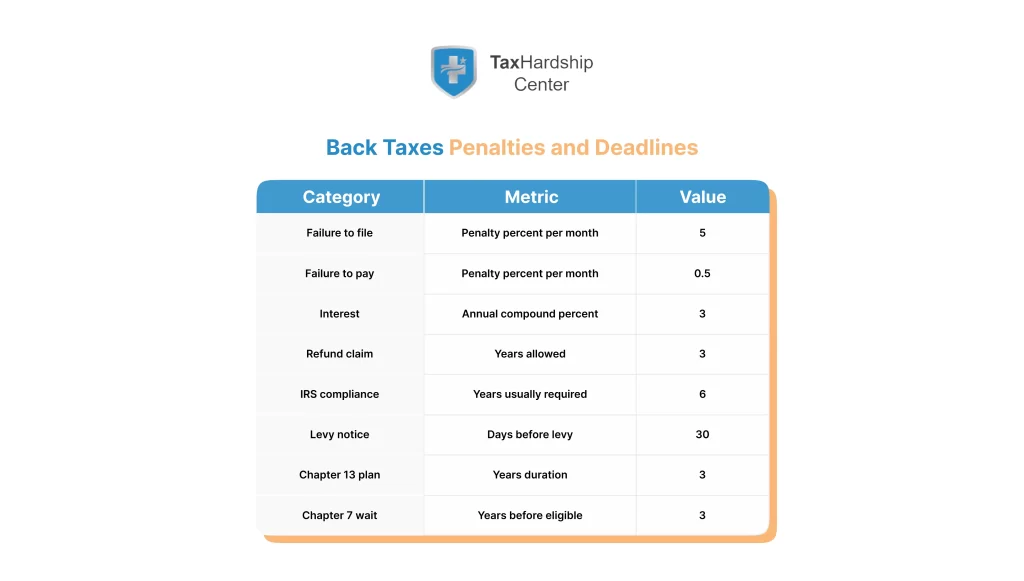

Penalties hit hard when you do not file taxes. The failure to file penalty grows each month based on your unpaid balance, and the failure to pay penalty stacks on top. Interest compounds on both the tax and the penalties until you resolve the bill. You cut these charges when you file tax returns and set a payment plan that fits your budget. You also keep penalties smaller by paying what you can with the return and by making additional payments online as cash allows.

Claim a refund before the three year cutoff

Refunds expire. The IRS pays refunds only if you file tax returns within three years of each original due date. If you miss that window, the refund vanishes and the law bars you from claiming it. Many people leave money on the table from withheld wages, refundable credits, and estimated payments. File taxes for those years and pull that cash back into your pocket. If you expect a refund and owe on other years, filing can also reduce your total balance and stop extra interest on that amount.

Protect your Social Security benefits and future income

Filing your tax return locks in earnings that flow to your Social Security record. Self employed workers pay individual income tax and self employment tax, which funds Social Security and Medicare and credits your account. You also avoid aggressive collection when you keep returns current because the IRS can levy Social Security benefits for unpaid taxes. Filing now keeps your future benefits intact and shields cash flow you need for rent, groceries, and fuel. You also present clean records when a new employer or lender requests proof of income.

Our services at Tax Hardship Center: file back taxes and set relief that fits

Our services at Tax Hardship Center focus on fast catch up filing and practical relief. We prepare each past due Form 1040 and line up the right fix for what you owe. If you need time, we request an Installment Agreement that matches your monthly budget. If your finances qualify, we evaluate an Offer in Compromise to settle for less. If cash flow cannot support payments, we pursue Currently Not Collectible status while you stabilize. For broader support, our IRS Tax Relief services cover liens, levies, and penalty relief with clear updates by phone and email.

What if you don’t file voluntarily

If you do not file back taxes, the IRS takes the wheel. Automated notices start, and penalties keep growing. The IRS may prepare a substitute for return based on income reports from employers, banks, and brokers, which often inflates your tax because it ignores deductions and credits. Enforcement actions follow if you ignore letters, and those actions can touch wages, bank accounts, and property. You also face headaches with state tax agencies because they share data with the IRS and may launch their own collection. Add one more risk to the list. To see how penalties stack up, read our breakdown of the IRS penalty for not filing taxes, then choose a filing path that stops extra charges.

Collection and enforcement actions the IRS may take

The IRS uses a set process once your account ages. It sends balance due notices, then escalates with liens and levies when you do not respond. A lien attaches to your property and can trip up home sales and business loans. A levy takes money from wages or bank accounts and can hit Social Security payments and vendor receipts. The IRS can also seize refunds from current year tax returns to pay older balances. You avoid most of this by filing, setting an installment agreement, and keeping up with your current year payments.

How IRS prepared substitute returns SFRs can hurt you

A substitute for return, often called an SFR, treats all income as taxable and gives you no say on deductions or tax credits. The IRS builds an SFR with W 2 and 1099 data and may miss basis, business expenses, or family credits that lower your individual income tax. That inflates your tax liability and triggers larger penalties and interest. You can replace an SFR by filing an original return for that year with supporting tax forms. Once the IRS processes your return, it adjusts the balance to the correct amount for your tax situation.

Impact on loans, credit, and business tax records

Banks and card issuers ask for recent tax returns when you apply for mortgages, business lines, or large credit limits. Late filing stalls approvals or forces you into higher rates. Vendors also review business tax records before they extend terms. Unfiled returns block SBA loan applications and state registrations for small business owners. Clean filings help you qualify for better credit and faster closings. Filing also supports clean bookkeeping and prevents mismatches between your financials and your tax returns.

How to file tax returns for previous years

You can file back taxes with a simple plan. Review the IRS filing past due returns page for official steps. Start by pulling every tax form that reports your income, withholding, or deductions. Build a year by year folder and match each W 2, 1099, and 1098 to the right tax year. Order IRS transcripts if you lack documents or moved since you last filed. Choose tax software or a tax professional based on the number of years and the complexity of your return. File each year on its own Form 1040 and include schedules that fit your business taxes or investments.

Gather tax forms, W 2s, 1099s, and IRS transcripts

You gather documents first to avoid errors that cause notices later. Ask prior employers for W 2 reprints and request 1099 copies from banks, brokers, and gig platforms. Pull 1098s for mortgage interest and student loans, and collect child care, property tax, and education records if you plan to claim tax credits. Create an IRS online account and download wage and income transcripts to cross check missing forms. A complete set helps you file tax returns that match IRS records, which speeds processing and reduces letters.

Use IRS Form 1040 for each past year

You file an original individual income tax return for each past year using that year’s Form 1040. You include the right schedules for items like Schedule C for sole proprietors, Schedule E for rentals, and Schedule D for capital gains. You also include child tax credit and education credit forms if they apply to your tax situation. You attach W 2s to the front if you mail the return and include documentation the instructions require. You sign and date each return and keep copies with your worksheets.

Filing electronically vs. mailing past due returns

You can e file some prior year tax returns through modern tax software, which speeds acknowledgment and reduces math mistakes. Many software products support the last few tax years, and some allow state filings for matching years. If your year falls outside the software window, you print and mail to the IRS service center listed in the instructions for that year. Use certified mail for a clear paper trail. If you claim a refund close to the three year deadline, you file as soon as possible to preserve your refund.

State e-file and tax extension deadlines for past returns

State e-file rules vary, but most states accept prior year returns only for a limited window. If e-file closes for your year, print and mail the state return with required copies of your federal Form 1040. Watch state tax extension deadlines, because a late state filing can trigger separate penalties even if you fix federal filings. File the state and federal returns for each year at the same time to keep records aligned. Save certified mail receipts for both agencies.

Exemptions, credits, and deductions in older years

Older tax years may allow personal exemptions and different standard deduction amounts. Review instructions for each year so you claim exemptions and child credits where they still apply. Compare itemized deductions to the standard deduction before you choose. Keep support for medical costs, mortgage interest, and property tax if you itemize. Clean worksheets help you answer IRS questions fast.

Disclosures and transactions: document everything

Back filings work best when you track every key transaction and disclosure. Keep ledgers for business expenses, mileage logs, sales data, and copies of 1099 and W-2 forms. Add a brief statement if you estimate numbers because of missing records. Disclose foreign accounts and digital asset sales when required. Organized disclosures reduce audit risk and speed processing.

Crypto investments and hobby income in previous years

Report crypto investments as property and track each sale with date, basis, and proceeds. Use exchange statements and a simple spreadsheet when you rebuild old transactions. Treat hobby income as other income without business deductions, and move to Schedule C only when the activity rises to a trade or business. Keep wallet addresses, transaction IDs, and exchange reports in your file. Accurate reporting prevents penalties and keeps future notices off your inbox.

Help filing your past due return

You decide who handles your back taxes based on risk and time. Tax software and online tax tools work well for simple wage income and no business schedules. A tax professional adds value when you own a business, claim complex deductions, or juggle multiple unfiled years. You also benefit from professional help when you receive IRS notices, face a levy, or want to request penalty relief. The right partner guides your filing and your relief options so you clean up the past and stay current.

When tax software and online tax tools can assist

Online tax software gives you step by step prompts that cover W 2 wages, interest, dividends, and basic credits. The programs also import some 1099s and calculate the child tax credit and the earned income credit when you qualify. Many platforms include a tax calculator that shows your projected refund or balance due as you enter data. You can often file taxes online for the last few years and pay any taxes owed by bank account, debit card, or credit card. Software works best when your return fits inside the interview and you do not need strategic advice.

When to seek help from a tax professional

Hire a tax professional when you own a small business, receive K 1s, sell investments, or face self employment taxes across multiple years. A pro reconstructs records, finds missing deductions, and defends your positions if the IRS asks questions. Enrolled agents, CPAs, and tax attorneys also handle calls with the IRS so you avoid missteps. Read customer reviews and ask about past cases that match your profile. Choose someone who will map a plan across all years and who will help you set up payment plans and estimated taxes.

How Tax Hardship Center supports your filing and relief

Tax Hardship Center builds a simple path from unfiled returns to a clean slate. Our tax professionals pull IRS transcripts, reconstruct income, and prepare each Form 1040 with care. We review your tax deductions and tax credits line by line, then propose the best relief for what remains. We handle installment agreement requests, penalty abatement, and if you qualify we prepare an offer in compromise. Start with a quick case review at Tax Hardship Center and see how our team turns past due returns into filed returns that close the loop.

Autofill, desktop products, and mobile filing tips

Modern tax software offers autofill for basic data and imports some 1099s. Desktop products work well for multi year work because you can save local copies and reinstall if needed. Mobile apps help with quick W-2 scans, but review every screen on a larger display before you submit. Complete any installation or activation steps early so updates download before you start. Always save PDFs and the e-file acceptance email for each year.

Expert preparer availability and referrals

Back taxes often need an expert preparer who handles controversy work. Ask about availability during peak season and request referrals from clients with similar facts. Verify professional licenses and years of experience with back filings and payment plans. Confirm who speaks to the IRS on your behalf and who answers email when notices arrive. A clear service scope keeps work on schedule and prevents costly complications.

How many years back can you file back taxes?

You can file back taxes for any year, but the IRS usually wants six years to consider your account current. You must file within three years of the original due date to claim a tax refund, so act fast if you stand inside that window. If you owe taxes, filing older years still helps because it stops the failure to file penalty and lowers risk of enforcement. Special cases may require more than six years when income looks unreported or when fraud enters the picture. A tax professional helps you judge the right span for your situation.

IRS timeline: claim refunds within three years, but file up to six

The refund clock runs for three years. You file within that time to claim your money, including withholding and refundable credits. The IRS often requests the last six years of returns to resolve a nonfiler case and to restore good standing. You can file older years as well, but refunds on those years do not pay out after the deadline. Filing those older years still reduces risk and shows good faith if you need a payment plan or penalty relief. Use transcripts and bank records to rebuild those years so your numbers match reported income. For background on time limits, review our explainer on the IRS statute of limitations.

Special cases: beyond six years or suspected fraud situations

The IRS can ask for more than six years when the facts call for it. If your income jumps without matching filings, or if badges of fraud appear, an examiner may push the lookback further. Criminal cases remain rare, yet you should not ignore that risk when facts look bad. File complete and accurate returns and document every position. A tax attorney or enrolled agent with controversy experience adds a buffer and protects your rights during reviews.

Reconstructing missing income with IRS transcripts

When documents go missing, transcripts fill the gaps. Wage and income transcripts list W 2 and 1099 forms that payers filed to the IRS. You can also use bank statements, merchant records, mileage logs, and point of sale reports to rebuild business taxes on Schedule C. A pro can craft reasonable estimates when exact records do not exist and can attach statements that explain methods. Clean reconstruction shows good faith and reduces questions during processing.

Entities and C corp differences for back filings

Your entity type controls which forms you file for each year. Sole proprietors use Schedule C with Form 1040, while an S corporation files Form 1120-S and a C corp files Form 1120. Late corporate returns can trigger separate penalties from individual returns and can affect shareholder basis. Match each entity return to the right year and state filing. Coordinate owner K-1s so totals flow cleanly to individual income tax returns.

What happens if I don’t file back taxes?

The bill grows, and options shrink. Penalties and interest add weight every month until you file and pay. The IRS files liens that block credit and levies wages and bank accounts that you need for daily life. State agencies copy the file and start their own collection for state income tax. You also risk identity issues when mismatched income sits in limbo and triggers notices that you never see because the IRS mails them to old addresses.

Growing tax liability from penalties and interest

Failure to file penalties run higher than failure to pay penalties, so you save the most by filing even if you cannot pay today. Interest compounds daily on taxes owed and on added penalties. When you stack several years, the growth accelerates and eats future income. Filing now caps the penalty clock for each year and lets you set an installment agreement that fits your budget. You also protect current refunds from offset by clearing old balances faster.

Wage garnishments, bank levies, liens, and more

The IRS collects with liens and levies once notices go unanswered. A wage garnishment takes a slice of each paycheck and keeps going until you resolve the balance. A bank levy grabs money in your account on the day it hits and can repeat if the account refills. A federal tax lien clouds title to a home or car and spooks lenders and buyers. You avoid most of this by filing, requesting a payment plan, or proving hardship through currently not collectible status when cash flow falls short. Use our Complete Wage Garnishment Guide to understand how orders work and how fast you can stop them.

Long term effects on individual income, credit, and small business

Unfiled returns cause long term damage. Landlords, lenders, and investors treat missing filings as a red flag. You may pay higher rates or lose deals you want for a home or a vehicle. Small business owners face suspended licenses and blocked contracts when agencies require proof of current filings. Clean returns protect your individual income, your credit profile, and your business tax records so you can speak to banks and vendors with confidence.

Influence of the One Big Beautiful Bill new tax law on back taxes

New tax laws shift deductions, credits, and reporting rules that affect how you file back taxes and how you plan future returns. Changes to energy credits, the standard deduction, and itemized deduction limits may change your results when you file prior years within allowed windows. Reporting rules for marketplace payments and digital platforms also adjust who receives 1099s and how you reconcile side income. You should review official IRS updates for any new law that affects your open years. A tax professional tracks these shifts and helps you time filings to capture legal benefits and avoid surprises.

Deduction changes: SALT cap, energy credits, income reporting

The state and local tax SALT cap limits itemized deductions for many filers and still matters for high tax states. Energy efficient home credits and clean vehicle credits shift often and require careful reading of eligibility and timing rules. Income reporting for gig work and online sales continues to evolve, which places more 1099s in your mailbox and more lines on your return. These rules can change the best path for previous years if you still stand within filing windows. Document your claims and keep purchase records and certification letters for any credit you claim.

How retroactive rule changes may affect refunds or liability

Lawmakers sometimes make changes that apply to the prior year or even earlier, which can alter refunds or tax owed. You may benefit from a higher credit or a new deduction that applies to a year you still can amend. You may also lose an expected benefit if caps or thresholds move. A pro will review your open years and flag any change that justifies an amended return or a different filing sequence. That strategy can turn a balance due into a smaller bill or a refund.

Planning strategies for current filings and previous years

You can pick the order you file when several years sit open. File refund years first to put cash in your account, then file balance due years and set a single installment agreement. Make current year estimated payments on time so the IRS sees forward progress. Update your withholdings with your employer to bring this year in line. Keep organized records so you move faster if you need an offer in compromise or penalty relief later.

Mortgage lenders and underwriting standards care about filed returns

Mortgage lenders and underwriters ask for two years of filed returns and recent transcripts. Missing years can pause approvals or lead to weaker terms. Filed returns show stable income for loan repayment and reduce risk flags in underwriting standards. Keep copies of acceptance emails and transcript printouts in your loan file. Clean paperwork speeds closings and preserves your rate lock.

Avoid the worst: tips to file taxes late with confidence

You can file late taxes with a calm plan and a few tools. Use IRS calculators and free preparation tools if your return stays simple, and upgrade to a pro when you add business tax schedules or several years. Request an installment agreement online when your budget cannot carry the full balance. Ask for penalty abatement if a first time lapse or a documented hardship caused the delay. Keep current year filings clean so you show good faith while you resolve older balances.

Use tax forms, calculators, and IRS preparation tools

Start with Form 1040 instructions and the IRS Interactive Tax Assistant to confirm credits and filing status. Use the IRS Tax Withholding Estimator and the online tax calculator inside your software to preview your result. The IRS Free File program can help if your income falls within limits, and Volunteer Income Tax Assistance VITA helps many taxpayers at no cost. Gather your forms and use these tools to complete accurate returns that fit rules for each year. The right tools cut errors and speed processing.

Set up payment plans or installment agreements

If you owe, you can request an online payment plan and pick a monthly amount that works. Short term plans cover smaller balances that you can clear in a few months. Long term installment agreements stretch payments across several years so you keep room for rent, food, and fuel. You can pay by direct debit from your bank account, by payroll deduction, or through online payments by card or bank transfer. A clean plan stops levies and gives you a clear finish line. For a deeper look at plan types and costs, see our guide to IRS payment plans, and when you are ready, apply through the IRS Online Payment Agreement application.

Explore penalty abatements, offers in compromise, or NOL relief

Penalty relief can reduce costs when you show reasonable cause or when you qualify for first time abatement. An offer in compromise can settle a tax debt for less than the full amount when your assets and income cannot cover the balance. Net operating losses NOLs can offset income in open years when business income swings, which can lower tax and unlock refunds. A tax professional can judge which path fits your profile and prepare the forms with supporting records. Smart relief turns a heavy bill into a manageable plan.

Use the IRS website and Online Account

The IRS website gives you the fastest path to clean up back taxes and manage your tax liability in one place. Create an IRS Online Account to view balances, set a payment plan, and pull transcripts for each tax year. The site also links to Free File partners during filing season and to Direct Pay so you can send payments from a bank account without fees. A current online account helps you spot notices early and confirm that the IRS received your tax return. You move faster when you keep every document and confirmation together in one secure portal.

Set up your IRS Online Account for transcripts and payments

Open an IRS Online Account and complete identity verification. Once inside, download wage and income transcripts to rebuild missing W 2 and 1099 forms for previous years. Review your account balance by tax year and use the payment plan tool to request an installment agreement that fits your budget. You can also update your address so future letters reach the right place. Save PDF copies of every transcript and screen so your records match what the IRS sees on its website.

Use the IRS website Free File and Direct Pay options

If your income qualifies, the IRS Free File program connects you to trusted software so you can file taxes online at no cost. You can also use Fillable Forms for simple cases when you know the lines you need. When you owe, use Direct Pay on the IRS website to send money from a checking or savings account and reduce interest charges. You can also schedule future payments so your plan runs on time. Always confirm the payment confirmation screen and keep the receipt with your return copy.

Watch for email confirmations and phishing risks

Most IRS communication arrives by mail, not email, so treat surprise emails as suspicious. Your tax software may email filing and payment confirmations, and those messages help you track status. Do not click links in emails that claim you owe tax or that ask for gift card payments. When in doubt, go to the IRS website directly and sign in to your account to verify. Keep a simple folder for email receipts from your software so you can prove filing dates and payment amounts.

Privacy controls, data sharing disclosures, and opt-out choices

Review privacy settings in your IRS Online Account and in any software you use to file back taxes. Read disclosures about data sharing, marketing, and bank products so you understand how companies use your information. Use opt-out links to limit marketing email and data transfers that you do not want. Confirm your address and zip code to ensure letters arrive on time. Keep a simple log of what you consented to and when you changed settings.

Protect your savings account during IRS collection

Your checking and savings account sit in the path of IRS levies when a balance ages, so you protect that cash by filing and setting a plan early. A filed return and a live installment agreement usually stop bank levies before they hit. If a levy arrives, you still have options to request a release based on hardship or to shift to a direct debit plan. You also gain time by showing proof of rent, food, medical costs, and other necessary expenses. The goal is to keep basic living money safe while you resolve the tax debt.

How levies reach checking and savings accounts

The IRS sends a notice and demand for payment, then issues a final notice of intent to levy if you do not respond. After the waiting period, the agency can serve a bank levy that freezes the money in your accounts that day. The bank holds funds and then sends them to the IRS unless you resolve the issue. A levy can sweep both checking and savings accounts, and it can repeat if new deposits arrive later. Filing returns and requesting a payment plan before that point usually prevents the levy.

Ways to release a bank levy fast

Call the IRS as soon as you learn about a levy and request a release when you show hardship or a pending installment agreement. Provide bank statements, pay stubs, and a simple budget that proves you cannot meet basic needs without the funds. Ask your tax professional to fax the agreement or proof of filing while you stay on the line. If you receive Social Security or veterans benefits, confirm protections that apply. Move to direct debit installments so the IRS stops further levy action.

Keep a hardship budget and direct debit plan

List fixed costs like rent, utilities, insurance, and required loan payments. Track food, fuel, and medical costs for at least three months. Use that budget to set an installment agreement that keeps enough cash in your savings account for emergencies. Automate a direct debit payment from a bank account on a date that matches your paycheck cycle. Review the plan each quarter and increase payments when income improves so interest falls quicker.

Bankruptcy and back taxes

Bankruptcy can reset finances, but it does not erase every tax liability. Some older income taxes can receive a discharge when you meet strict timing and filing rules. Recent taxes, trust fund taxes, and fraud penalties usually survive. A bankruptcy filing also pauses IRS collection during the case, which can help you protect wages and bank accounts while you regroup. Coordinate with a bankruptcy attorney and a tax professional before you file so you pick the right chapter and timing.

When Chapter 7 can discharge income tax liability

Chapter 7 may wipe out eligible income tax debts when you filed the returns on time or at least two years before the case, the taxes come from a return due at least three years ago, and the IRS assessed the tax at least 240 days before the filing. You must also show no fraud and no willful evasion. If you meet those rules, the court can discharge that tax liability and free up income for current obligations. You still need to stay current on new filings to avoid fresh balances.

When Chapter 13 helps with payment plans and liens

Chapter 13 creates a court approved payment plan that lasts three to five years. Priority taxes and recent years usually require full payment inside the plan, while older unsecured taxes may receive partial payment. The automatic stay pauses levies and wage garnishments while the plan runs. A filed plan can also manage tax liens by paying the value of the secured claim over time. Chapter 13 works well when you need structure and time to clear several years at once.

Taxes that bankruptcy does not discharge

Bankruptcy does not erase payroll trust fund taxes, recent income taxes, or taxes tied to fraud. It also does not remove most tax liens from property you owned before the case. Penalties on nondischargeable taxes may also survive. You still gain relief from collection during the case and a cleaner path after discharge. Speak with a qualified attorney to confirm how the rules apply to your facts and to choose the best route for long term relief.

Refund request and tax refund time frames

You request a refund by filing original returns or amended returns for each year. The tax refund time frames depend on filing method and workload, but e-file with direct deposit usually posts faster than mail. The three year statute controls whether the IRS can pay your refund at all, so check dates before you file. Track status with the IRS refund tool and save every email confirmation from your software. If the window already closed, apply any excess payments to other years you still owe.

Banking services to deposit funds and plan loan repayment

Pick direct deposit for refunds to a checking or savings account you control. Some providers offer refund advance products, but read the disclosures and fees before you accept. A refund processing service fee may apply if you choose to pay prep fees from your refund. Verify that any provider holds a money transmission license in your state when it handles your funds. If you owe tax, schedule automatic payments so the plan fits with rent, utilities, and loan repayment.

At Tax Hardship Center, we help you finish the job

At Tax Hardship Center, we help you close out unfiled years and protect your budget for the road ahead. We design one plan that covers filing, payments, and any relief you deserve. You can choose a Repayment Program with direct debit timing that fits payday, or reset an Installment Agreement if your income changed. If you run a small business, our Bookkeeping services keep records clean so next year files on time. When facts support it, we build and file a full Offer in Compromise package with supporting transcripts and budgets.

In summary…

A short plan and steady steps fix back taxes and protect your money and benefits. You gather forms, file each year, secure a payment plan, and keep current so penalties stop. You pick software or a professional based on complexity and time. You also watch new tax law changes so you capture credits and avoid errors.

- File now to cut penalties and interest

- Failure to file costs more than failure to pay

- Filing stops the largest penalty and starts the clock on relief

- Failure to file costs more than failure to pay

- Claim refunds within three years

- File refund years first so cash funds the cleanup

- Missing the window transfers your money to the Treasury

- File refund years first so cash funds the cleanup

- Protect benefits and credit

- Reporting income preserves Social Security credits

- Current filings improve loan approvals and business terms

- Reporting income preserves Social Security credits

- Choose the right help

- Use software for simple returns and few years

- Hire a pro for small business, rentals, or many years

- Use software for simple returns and few years

- Set payment plans and request relief

- Installment agreements fit real budgets

- Penalty abatement and offers in compromise reduce totals

- Installment agreements fit real budgets

A clear filing sequence and the right relief tools bring you back to good standing. If you want a guided path end to end, connect with Tax Hardship Center for a quick case review.

FAQs

Can I file back taxes online for previous years?

You can e file some prior year returns through modern tax software, usually for the last few years the platform supports. If your year falls outside that range, you print and mail to the IRS. You still gather the same tax forms and attach W 2s when you mail. E filing gives you faster acknowledgment and fewer math errors. Mailing works fine when you use certified mail and follow the instructions for the right address.

How many years back will the IRS require me to file?

The IRS often requests six years to bring a nonfiler current. You can file more years if needed, but the agency usually considers six years enough to close a case. If fraud or large unreported income appears, an examiner may ask for more. Filing complete and accurate returns reduces that risk. A pro can assess your facts and build a plan the IRS will accept.

What if I cannot pay my taxes when I file?

You should still file to stop the failure to file penalty. Then you request an online payment plan and pick a monthly payment that fits your budget. You can also apply for penalty relief or currently not collectible status when hardship exists. Paying what you can upfront reduces interest and penalties. Clean filings and a good faith payment plan prevent most levies.

Do unfiled returns affect Social Security benefits?

Yes. Self employed income affects Social Security credits, and filing ensures that income reaches your record. The IRS can also levy part of Social Security payments for past due federal tax. Filing and arranging a plan protects benefits and shows progress. Keep current year payments on track to avoid new issues. Save proof of filings in case agencies request documentation.

When should I hire a tax professional instead of using software?

Hire a pro when you own a small business, receive K 1s, hold rentals, or face several unfiled years. A professional reconstructs records, claims legal deductions, and handles IRS notices. You also gain help with installment agreements, penalty relief, and offers in compromise. Read customer reviews and confirm they handle back taxes often. The right team saves time and reduces total cost.