IRS forgiveness program application online ranks among the most searched tax relief questions right now. Most people qualify for a payment plan in minutes when they file all required returns and owe less than fifty thousand dollars. Many households that cannot afford full payment qualify for an Offer in Compromise when reasonable collection potential sits below the tax debt. You can apply online for installment agreements and start a settlement path after you gather income and expense proof. You learn what the IRS accepts, what each option costs, and how to apply the right way across this guide.

Do You Qualify for IRS Tax Forgiveness Right Now?

You want a straight answer before you apply, and this section delivers it. The IRS checks two things first, your filing compliance and your ability to pay. If you filed all required tax returns before the filing deadline and you cannot pay in full, you likely qualify for a payment plan or for hardship relief. People mistype it as a filling deadline, but the IRS calls it a filing deadline. If your income and allowable expenses leave little or no monthly ability to pay, or if you hold no equity the IRS can reach, you may qualify for an Offer in Compromise Program.

Quick check: can’t pay your tax liability in full?

Add your verified monthly income and subtract the IRS allowable living expenses for your household size and county. If the result shows little or no disposable income, the IRS often accepts a low monthly payment or a settlement under an OIC. If the number comes out strong, a short term or long term plan fits better. You avoid wasted effort when you pick the path that your numbers support.

File all required tax returns before you apply

The IRS will not approve relief if you leave returns unfiled. File every required return for individuals and any related business. Match wage and income items so transcripts and returns align. If you miss forms or leave out income, you risk a rejection or a hold on your application. You shorten processing time when you fix filings first.

Who should apply for IRS Fresh Start online

Online tools work best for individuals and wage earners who owe for recent years and have no complex business assets. If you owe less than fifty thousand dollars and can pay within a few years, the online payment agreement fits well. If you run a small business with employees or hold assets tied to Business Tax Liabilities, you may still apply online for some plans, but prepare full financials and supporting documents. People with older debts and liens can also use online steps to start, then complete any extra forms that the IRS requests.

Our Services at Tax Hardship Center

Our services at Tax Hardship Center cover every corner of IRS debt relief. We check your transcripts, confirm deadlines, and prepare a file that meets the IRS standards. We explain how options like installment agreements, the Offer in Compromise Program, or Currently Not Collectible status apply to your situation. We also guide clients on Tax Deposits and estimated payments so new balances do not pile onto old ones.

- Start with a free review at our Free Tax Consultation page.

- If a payment plan fits, we set up a streamlined Installment Agreement.

- For settlement, we prepare a complete Offer in Compromise package using the IRS Offer in Compromise Booklet.

- For liens, levies, or broader cases, we deliver IRS Tax Relief Services.

IRS Online Payment Plan: Apply in Minutes

You can set up a plan in one sitting when your debt and filing status meet the rules. The Online Payment Agreement tool asks for identity proof, then walks you through plan selection, payment details, and the monthly amount. The IRS calculates interest and penalties daily until you pay off the balance. You keep control by choosing direct debit or payroll deduction and by picking a draft date that matches your cash flow. If you miss a payment, you risk default, so build a number you can support every month.

Short-term payment plan up to 180 days

A short term plan helps when you can clear the balance in six months or less. You can request this plan without a setup fee if you pay by bank transfer, check, or money order. Interest and penalties continue until you pay in full. People use this option when a bonus, commission, or asset sale will land soon. You keep collection actions at bay while you finish the payoff.

Long-term installment agreement with direct debit

A long term plan spreads the balance across monthly payments. Most people choose direct debit because it costs less and keeps the plan in good standing. The IRS may ask you to choose the highest affordable payment that clears the debt within the maximum term. You can change the amount later if your situation shifts. Choose a date that falls a few days after payday to prevent overdrafts.

Setup fees, interest, and penalty basics

Setup fees vary by plan type and payment method. Direct debit plans cost less than plans you pay by invoice or card. Interest compounds daily on unpaid tax, and penalties apply for failure to pay until you clear the balance. You reduce total cost when you pay down principal faster or switch to direct debit. Read the fee chart during the application and pick the cheapest path that fits your budget.

Create your IRS Online Account and verify ID

You need an IRS Online Account to submit a plan. The system asks for a photo ID, a phone number, and in most cases a selfie with live identity verification. Prepare your last filed return, your current address, and your bank details. If verification fails online, you can prove identity by video call or in person. Finish the setup in one session to avoid timeouts and save your progress.

Online payment options including bank and credit card

You can pay by direct debit from a bank account, by debit card, or by credit card. Direct debit costs less and lowers the chance of a missed payment. Card payments add processor fees that increase your overall cost. If you choose a card, use it for short term timing only, then switch to direct debit once cash flow stabilizes. Confirm each payment posts to the correct year and balance.

Offer in Compromise: Settle Tax Debt for Less

The OIC program lets you settle for less than you owe when your reasonable collection potential comes in below the total debt. The IRS uses your monthly disposable income and your realizable equity to compute an offer amount. If your numbers support a low offer that reflects your true ability to pay, the IRS may accept it. You must stay current on all filings and estimated payments during review. You also must make required initial payments unless you qualify for the low income certification.

General offer in compromise (OIC) information

An OIC requires Form 656 and either Form 433 A OIC for individuals or 433 B OIC for businesses. Many taxpayers benefit from reading the official Offer in Compromise Booklet before starting. You propose a lump sum or a periodic payment offer. The IRS reviews bank statements, pay stubs, housing costs, transportation costs, health insurance, and asset equity. You raise acceptance odds when your documentation supports every number. You also state why the offer serves the best interest of both you and the government. Read our primer on IRS Form 656 for a clear checklist.

How do I know if an offer is right for me? Updated April 1, 2025

An offer makes sense when your monthly disposable income stays low after IRS standard expenses and when you hold little equity the IRS can reach. If you can afford a full pay plan within the statute of limitations, the IRS will likely reject a settlement. If you face a true hardship and cannot pay in full before the statute runs, an OIC often fits. Review your numbers with the pre qualifier tool and adjust for recent income changes before you apply.

Do I qualify for the Low-Income Certification?

You qualify when your adjusted gross income and household size fall at or below the threshold on the IRS low income chart. With certification, the IRS waives the application fee and the initial payment, and the agency suspends monthly payments while it reviews the offer. You still must send full financial disclosures and must stay current on any required estimated taxes. If your income rises during review, tell the IRS and update your forms.

When the application fee and initial payment are waived

Low income certification triggers the waiver. Some people who submit a periodic payment offer also qualify for a pause on required monthly payments during review. The waiver removes the upfront cost burden and helps people who face tight cash flow. Approval still depends on your ability to prove your hardship and your limited equity. Keep copies of every document and note conversation dates and case numbers.

What are the national and local standards used in an OIC?

The IRS uses national standards for food, clothing, and other items, and local standards for housing and transportation. These standards cap how much you can claim for basic living costs. You can claim higher actual costs in rare cases when you show necessary grounds, such as special medical needs. Most applicants get better results when they align expenses to the published standards and explain any variance. The standards also shape the disposable income the IRS uses in the offer math.

Where to find the current IRS expense standards

You can find the latest standards on the IRS website under Collection Financial Standards. The page lists national and local tables and explains how to apply them to your budget. Match your county and household size. Download a copy and keep it in your file because the numbers change each year. Use those tables when you build your 433 A OIC so your math lines up with the agency approach. Get a deeper walkthrough in our guide on the IRS Collection Process.

What happens if my offer isn’t calculated correctly or is too low?

If you miscalculate and propose too low, the IRS may return or reject the offer. A returned offer ends the process and does not carry appeal rights. A rejected offer allows an appeal within thirty days, and you can raise the amount or clarify your numbers. You avoid both outcomes by checking your math and backing every figure with documents. When in doubt, rebuild the calculation and verify each standard and asset entry.

Do I keep paying my installment agreement during OIC review?

If you already pay under an installment agreement, you continue those payments unless you qualify for low income certification and the periodic payment pause. Stopping without approval can cause default and add penalties. If your finances changed, ask the IRS to modify the plan while your offer sits in review. Keep your account current to show good faith and to reduce risk of enforced collection.

Will a tax lien be filed while my offer is pending?

The IRS may file a Notice of Federal Tax Lien to protect its interest while it reviews your case. A lien does not take money from your paycheck or bank account, but it records a claim on your property. You cannot sell or borrow against equity without addressing the lien. If the IRS accepts your offer and you complete the terms, you can seek lien release and withdrawal after the final payment clears.

Can the lien be removed or a levy be released?

Yes, the IRS can release a levy when you enter a payment plan, qualify for hardship status, or when the levy causes immediate economic hardship. The IRS can also withdraw a filed lien after you set up a direct debit installment agreement and make a few successful payments. You support these requests with forms and proof of compliance. Timely action and clear documentation speed relief.

Edge cases: seasonal income, shared assets, and side gigs

Seasonal earners often show uneven cash flow, so document slow months so monthly disposable income reflects reality. If you share assets, the IRS typically considers only your share, but you must show the ownership split. Side gig income needs full tracking for deposits and expenses. If Bankruptcy Proceedings come up, talk to a professional first, because discharge rules vary by year and by type of tax.

Fresh Start Program Options at a Glance

You have more than one path to relief, and this section lays them out side by side. Fresh Start covers streamlined installment agreements, Offers in Compromise, penalty relief, and lien withdrawal rules tied to direct debit plans. Currently Not Collectible status gives a timeout when you face a true hardship. Bankruptcy Proceedings also interact with these programs, and while bankruptcy discharges some tax debts, others survive and need a plan. Pick the option that clears the debt at the lowest total cost without risking default. For more background on forgiveness versus settlement, see our explainer on IRS Debt Forgiveness vs. Offer in Compromise.

Installment agreements and online payment plans

Installment agreements fit taxpayers who can afford a steady monthly payment. Streamlined terms apply at certain balance thresholds when you qualify, and the IRS may skip a full financial review. Direct debit lowers setup fees and reduces default risk. You can apply online for most individual plans and receive a quick decision. Keep a buffer in your bank account to cover the draft every month. Learn how streamlined terms work in our article on the IRS Streamlined Installment Agreement.

Offer in Compromise for tax debt forgiveness

An OIC aims to match what the IRS can collect within the statute to a one time settlement or a short series of payments. You need tight documentation and a budget that follows the standards. When your numbers support a low offer, the program can save you thousands. You must stay compliant for five years after acceptance. Any default during that time can bring the full debt back.

Currently Not Collectible status for financial hardship

CNC status stops active collection when you cannot pay anything after basic living costs. The IRS reviews your 433 F or 433 A, compares expenses to standards, and then places your account in hardship status if you qualify. Interest and penalties continue to accrue. The IRS can review your case later if your income changes. CNC protects your paycheck and bank account while you stabilize.

Penalty abatement for first-time or reasonable cause

First time penalty abatement can remove the failure to file or failure to pay penalty in one qualifying year if you met a clean history standard. Reasonable cause abatement applies when events outside your control led to late filing or payment. You must support the request with dates, details, and documents. People often combine abatement with a payment plan or an OIC to cut total cost. Ask for abatement as soon as you qualify. For tactics and scripts, read our post on IRS penalty abatement strategies.

Tax lien withdrawal after direct debit installment agreement

If the IRS filed a lien and you enter a direct debit plan, you can request lien withdrawal after you make a few successful payments and meet the criteria. Withdrawal removes the public notice and improves access to credit. You must keep the plan in good standing and file all future returns on time. File the withdrawal request form and attach proof of direct debits and compliance.

Step-by-Step: Apply for IRS Fresh Start Online

You can start from your laptop or phone and finish the core steps in one day. The IRS tools guide you through identity proof, eligibility checks, and plan setup. An OIC still requires forms by mail, but you can pre qualify online and assemble everything before you send the package. Follow this sequence to reduce errors and speed a decision. Keep a folder with copies of every screen and submission.

Gather income, expenses, and past-due tax returns

Pull your last three months of bank statements and pay stubs. Add proof of rent or mortgage, utilities, insurance, vehicle payments, and medical costs. Download IRS transcripts to confirm income and withholding reported to the agency. File any missing returns before you start an application. Accurate documents prevent delays and keep your math tight.

Use the Online Payment Agreement application

Open the Online Payment Agreement and log in with your IRS Online Account. Enter your balance, choose short term or long term, and pick a draft date. The tool shows the monthly amount based on your choice and the remaining statute of limitations. If the tool rejects your first choice, lower the term or raise the amount until the system accepts a plan you can support. Submit and save the confirmation. You can also review official details on the IRS site for the Online Payment Agreement.

Check eligibility with the OIC pre-qualifier tool

Use the pre qualifier to test your offer before you fill out the full forms. Enter income, expenses, and basic asset values. The tool gives a rough estimate of an acceptable offer or tells you that a plan fits better. Adjust inputs to reflect accurate standards and current pay. If the estimate shows a workable offer, move forward with a complete 656 package. For context on plan fees and thresholds, see the IRS page on payment plans and installment agreements.

Submit required forms and supporting documents

If you pursue an OIC, complete Form 656, 433 A OIC or 433 B OIC, and include copies of your documents. Include the application fee and initial payment unless you qualify for the low income waiver. Mail the packet with tracking and keep your receipt. If you submit a payment plan online, upload any requested proof promptly through your IRS account. Keep Tax Deposits and estimated payments current during review to avoid default.

Track your application and respond to IRS notices

Watch your mail and your IRS Online Account for updates. Respond to every notice by the stated date. If the IRS asks for more proof, send clean copies with clear labels. If you move, update your address so letters do not miss you. Keep a log of calls, names, and case numbers.

What If You Can’t Pay Anything Today?

Some people face cash flow so tight that even a small payment hurts essentials. The IRS allows a pause when you show hardship. You can request a short delay in collection or seek CNC status with a full financial statement. You can also ask for penalty relief that lowers the balance and makes a small plan possible later. Protect groceries, housing, and basic medical care first.

Ask the IRS to delay collection temporarily

Call the number on your notice and explain your situation. The IRS may delay collection for a few weeks or months while you gather documents or recover from a short term setback. A delay does not stop interest or penalties. It does prevent immediate levies while you prepare a formal plan. Use the time to pull records and build a long term solution.

Show financial hardship with a Collection Information Statement

Submit Form 433 F or 433 A with accurate income and expense details. Attach proof for every line. The IRS compares your numbers to standards and decides whether to approve hardship status. Clear labeling helps the reviewer find what they need fast. Keep copies of everything you submit.

Protect essential expenses under IRS standards

The standards protect basic costs like housing, utilities, food, and transportation within set limits. Claim every allowed category and do not leave money on the table. If you must claim more than the standard, explain the reason and include proof. Essential childcare or medical costs often qualify. The more precise your package, the smoother the review.

How the IRS Collection Process Works

You win when you understand the timeline and act before heavy tools hit. The collection clock starts after the IRS assesses the tax and sends a bill. If you ignore notices, the agency can file a lien and then levy wages or bank accounts. Each notice signals a step and gives you a chance to act. A plan or an offer stops levies, and compliance keeps them away.

Timeline from tax bill to lien and levy

First comes the initial bill. Then reminder notices follow with rising urgency. After that, the IRS can file a Notice of Federal Tax Lien and, if you still take no action, can issue a Final Notice of Intent to Levy. The levy can hit paychecks, bank accounts, or certain government payments. You keep control when you respond early.

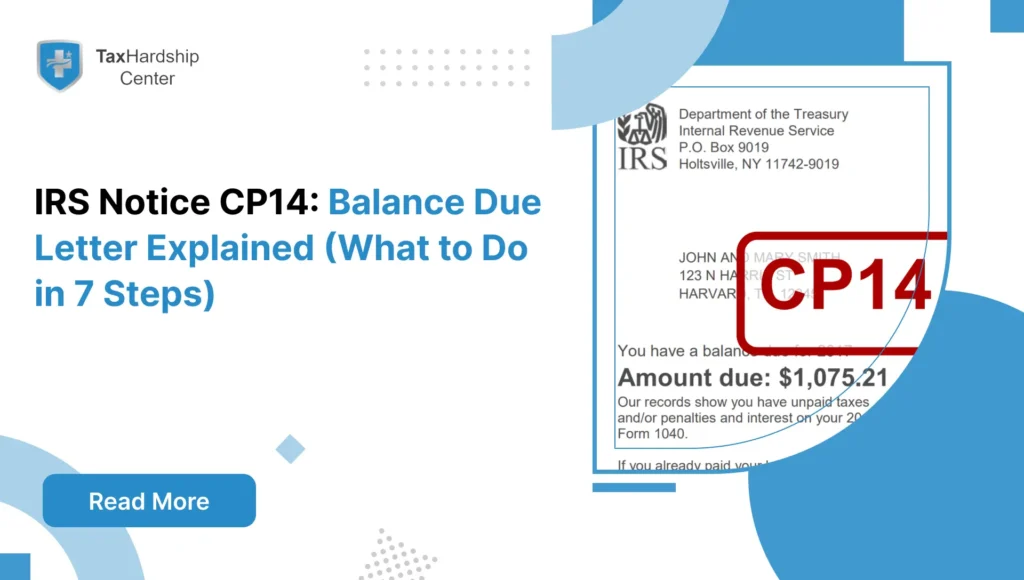

Notices you’ll receive and what each one means

Common letters include CP14 for the first bill, CP501 and CP503 as reminders, and CP504 warning of intent to levy certain property. The LT11 or Letter 1058 signals a final intent to levy and your right to a hearing. Read each letter, note the response date, and take action. Missing a deadline limits your options.

Stop levies with a payment plan, OIC, or hardship status

You can halt levy actions by entering an installment agreement, by submitting a processable OIC, or by proving hardship for CNC status. The IRS pauses levies when you hold an active plan in good standing or while it reviews a timely OIC. If a levy already hit, you can seek release by showing the levy creates an immediate hardship or by setting a qualifying plan. Move fast and document everything.

Updates and Changes in IRS Tax Forgiveness for 2024 and 2025

Rules and forms change, and you save time when you use current versions. The IRS updates expense standards each year and may adjust application fees. Online tools also receive upgrades that improve identity verification and status tracking. On April 1, 2025, guidance affirmed the focus on accurate expense standards and complete financials for OIC review. Always download fresh forms before you submit.

Form updates, fee changes, and expense standard revisions

Check the latest 656 and 433 A OIC or 433 B OIC before you fill them out. Fee amounts can change, and low income thresholds can shift with inflation. National and local standards update on a regular cycle. Plan numbers with the new tables to avoid a mismatch. New forms often include clearer instructions that reduce errors.

What these updates mean for online applications

Online Payment Agreement flows continue to streamline plan setup for qualifying taxpayers. Identity verification grows stronger to prevent fraud, so set aside time to complete it in one go. Updated standards may raise or lower disposable income on paper, which can change an OIC outcome. Rerun your numbers with the new standards before you send anything.

Know Your Tax Debt Solutions and Payment Options

You choose faster and better when you compare options by cost, speed, and risk. This section stacks payment plans, OIC, CNC, and penalty abatement side by side. Short term plans cost the least in fees and interest, but they require rapid cash. Long term plans spread the hit. OIC saves the most when you qualify, yet it demands deep documentation and strict compliance. CNC protects essentials when income cannot cover even a small payment.

Compare payment plans, OIC, CNC, and penalty abatement

Payment plans keep levies off your back and fit many taxpayers. OIC suits people with low disposable income and minimal equity. CNC helps households in crisis who need breathing room. Penalty abatement cuts balances when you meet history or reasonable cause rules. Many people blend options over time to reach the best outcome. For more angles, read our guide to Understanding IRS Payment Plans.

When to choose short-term vs long-term plans

Pick short term when you can clear the balance within six months. Pick long term when you need a lower monthly number and steady cash flow. If you expect a raise or a new job, you can start long term and increase later. If your income will drop, consider an OIC or hardship. Always build a plan that you can sustain.

Direct debit vs card payments: costs and benefits

Direct debit costs less and lowers default risk. Card payments add fees and increase total cost, but they can help with timing in a pinch. Bank drafts post reliably after payday. If you use a card, switch to debit after the first month to save money. Confirm each payment posts to the right year.

Common Filing Roadblocks and How to Avoid Them

You hit delays when paperwork falls short or math goes off. You can avoid most issues with a checklist and a review before you submit. Complete every return, match transcripts, and follow the expense standards. Keep copies of every document you send. If the IRS asks for more proof, respond on time with clean copies.

Missing tax returns or income records

Unfiled returns stop approval in its tracks. Pull wage and income transcripts to find missing W2s or 1099s. File accurate returns and attach any statements the IRS needs. If you cannot find a document, request a copy from the payer or use transcripts to recreate the entry. Keep a checklist and tick off each year. Start with our resource on Unfiled Tax Returns.

Estimate errors in disposable income or equity

Bad math kills offers and stalls plans. Rebuild your budget with the current standards and check every number twice. Verify asset values with statements and market sources. Do not inflate expenses above standards without proof. If the numbers change, update the IRS promptly.

Ignoring IRS notices during the application process

Silence invites levies. Open every letter and act before the deadline. Use your IRS Online Account to check balances and messages. If a notice confuses you, call and ask for a clear explanation. Keep a log of calls with dates and names.

After Approval: Staying Compliant to Keep Your Relief

Relief only sticks when you follow the rules after approval. You must file on time, pay on time, and keep estimated taxes current if you owe quarterly. If you accepted an OIC, you must stay clean for five years after acceptance. If you hold an installment agreement, you must make every payment and file every new return on time. Compliance keeps liens moving toward withdrawal and protects your result.

File future tax returns on time every year

Set calendar reminders for April filing and for quarterly estimates if you are self employed. Use e file to speed up processing and reduce errors. Keep copies of returns and confirmations. Late filings can default a plan or void an accepted offer. Build a simple checklist and follow it every year. For more help, see our post on how long the IRS can collect back taxes.

Make all payments by the due date

Automate where you can. Direct debit and payroll deduction reduce missed payments. If cash runs tight, call before the due date to adjust the plan. Do not skip without notice. One missed payment can trigger default and bring back collection actions.

How to request lien withdrawal after compliance

If you set up a direct debit plan and made a series of successful payments, file the lien withdrawal request. Include proof of debits, current filing compliance, and plan status. Withdrawal removes the public notice and improves credit access. Keep a copy of the approval for your records. Our Complete Wage Garnishment Guide explains how liens and levies differ and when each one falls away.

At Tax Hardship Center, we help you submit a clean application that gets traction

You avoid false starts when a professional packages your case with the right forms and evidence. We match your budget to national and local standards, confirm any Business Tax Liabilities, and prepare you for questions about assets and income swings. We also advise when Bankruptcy Proceedings help or when a Fresh Start option delivers a better outcome.

- Explore our detailed page on IRS Repayment Programs if a payment plan seems likely.

- Compare plan types in our guide to Understanding IRS Payment Plans.

- Learn about OIC payments and timelines in Offer in Compromise payments.

- If back returns block approval, use our checklist to File Back Taxes.

- For a quick path to a decision, start a Free Tax Consultation.

In summary…

You can apply online for payment plans in minutes and start an OIC case with the right prep. File all returns, gather proof, and match the IRS standards. Pick the option your numbers support and keep every promise you make.

- Payment plans fit most taxpayers who can afford a monthly amount.

- Direct debit costs less and lowers default risk.

- Short term plans finish in six months, long term plans stretch the balance.

- Direct debit costs less and lowers default risk.

- OIC works when disposable income and equity sit below the debt.

- Use the pre qualifier and follow current standards.

- Low income certification can waive fees and pause payments during review.

- Use the pre qualifier and follow current standards.

- CNC protects households who cannot pay anything today.

- Interest and penalties continue, but levies stop.

- The IRS can review later if income rises.

- Interest and penalties continue, but levies stop.

- Penalty abatement lowers the balance when you meet criteria.

- Ask early and send proof.

- Combine abatement with a plan for best results.

- Ask early and send proof.

Stay compliant after approval. File and pay on time. Request lien withdrawal when you meet the rules. Tax relief only sticks when you keep the basics tight.

FAQs

Do you qualify for IRS tax debt forgiveness?

You may qualify for settlement under an OIC when your reasonable collection potential sits below the total debt. Monthly disposable income and realizable equity drive the math. If you cannot pay in full within the statute of limitations, an offer may fit. If you can afford a plan, the IRS will likely direct you there.

Can I apply for an OIC online or only by mail?

You use the online pre qualifier to test your case, but you submit the full OIC by mail with Form 656 and Form 433 A OIC or 433 B OIC. You can upload some follow up items through your IRS Online Account after an offer unit assigns your case. Keep tracking numbers and copies of every page.

Do I need to keep paying an existing installment agreement?

Keep paying unless you qualify for low income certification that pauses periodic offer payments. If the payment amount no longer fits, ask for a modification while your offer sits in review. Do not stop paying without approval.

Will a lien be filed, and can a levy be released?

The IRS may file a lien to protect its claim during review. It can release a levy when you enter a payment plan, qualify for hardship, or show immediate hardship from the levy. You can request lien withdrawal after you set a direct debit plan and make a run of successful payments.

How fast does the IRS accept or reject an online payment plan?

Many plans receive approval immediately or within a few days when you qualify under streamlined rules. Complex cases may take longer and may require more proof. You speed decisions by verifying identity, filing all returns, and choosing direct debit.