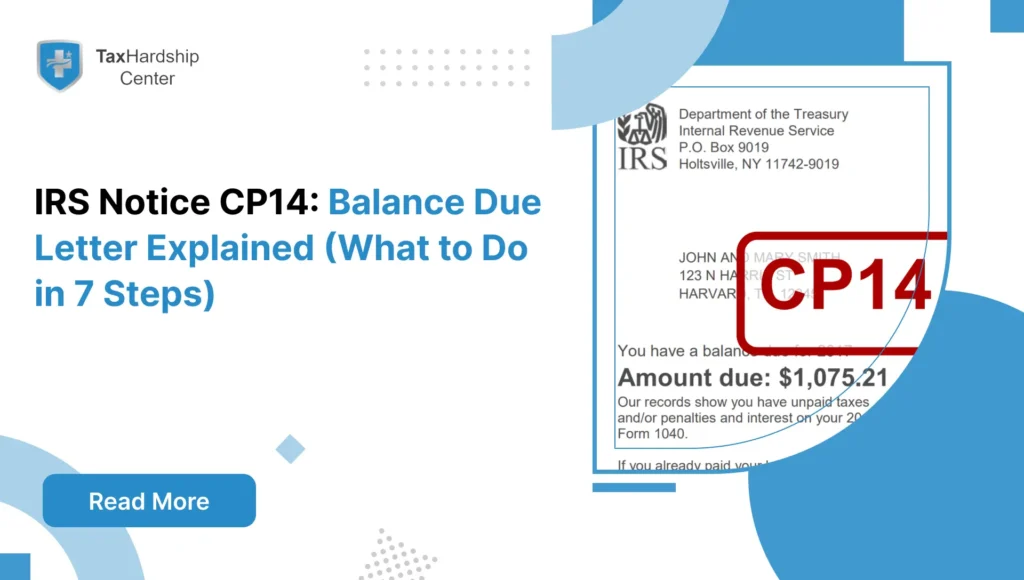

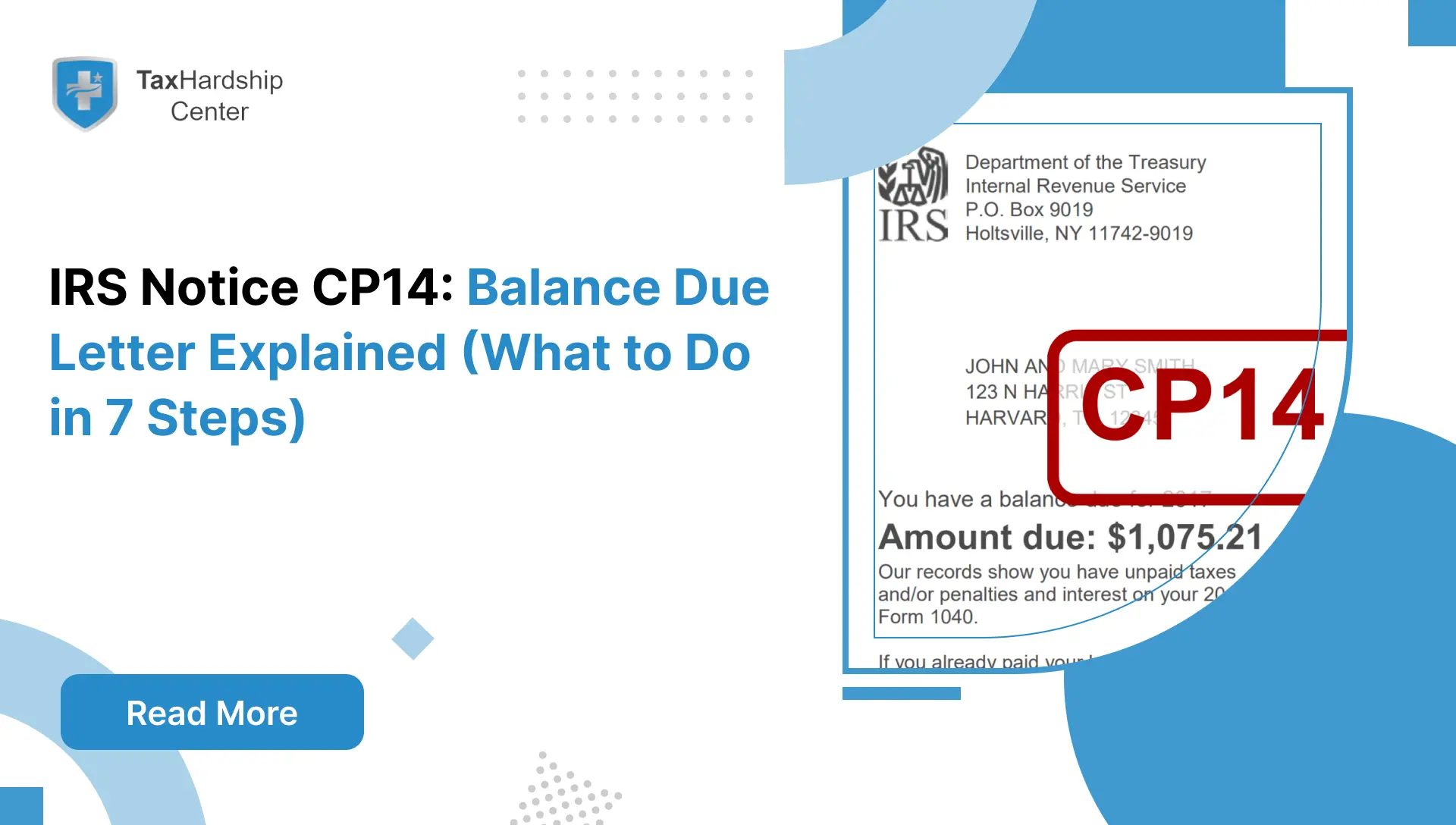

Opening a CP14 notice can feel like the IRS just dropped a surprise bill on your kitchen table.

Sometimes it really is a balance you still owe. Other times, it is a timing issue, like a payment that has not posted yet. Either way, CP14 is not a letter to ignore, because interest and penalties can continue to accrue, and the IRS can escalate collection activity if the balance is not resolved.

What Is An IRS Notice CP14

A CP14 is the IRS’s first and most common balance-due notice. It tells you the IRS believes you have unpaid tax, shows the amount (including penalties and interest), and requests payment within a short window.

The IRS also maintains a CP14 explainer page that summarizes the basics: read the notice carefully, pay by the due date, set up a payment plan if you cannot pay in full, and contact them if you disagree.

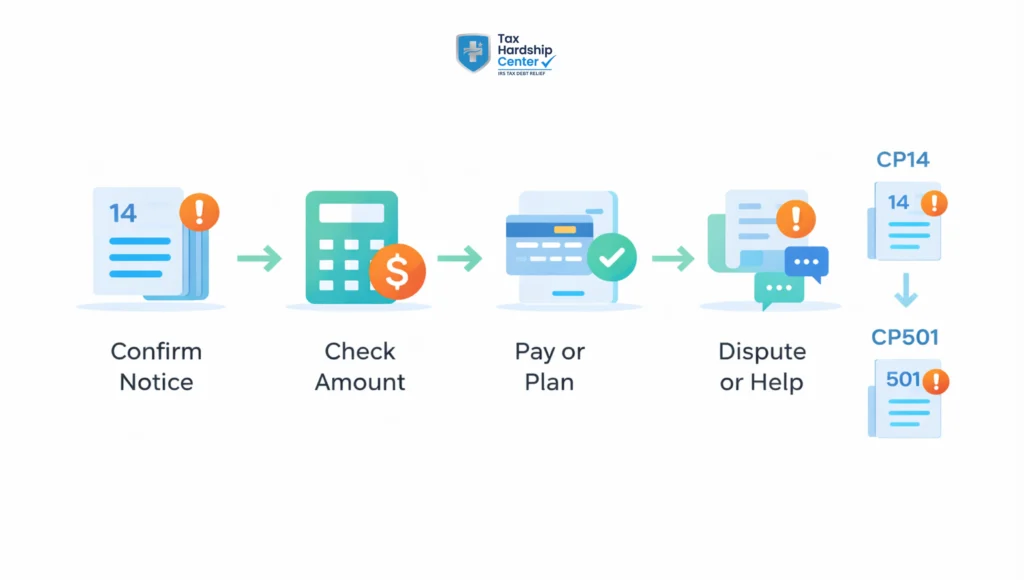

CP14 Vs CP501: What’s The Difference

This is one of the most common points of confusion.

CP14 is typically the first “balance due and demand for payment” notice.

CP501 is usually a reminder notice sent after the IRS did not receive your payment or a response to the previous notice requesting payment. In other words, CP501 often follows CP14 if the account remains unresolved.

Quick Comparison Table

| Notice | What It Usually Means | What It Signals |

| CP14 | First balance-due notice and demand for payment | The IRS believes you still owe for that tax year |

| CP501 | Reminder notice after a prior balance-due notice | You have not paid or responded yet |

If you want to understand where CP14 fits in the broader collections sequence, the Tax Hardship Center also covers the IRS collections notice timeline and escalation path.

What CP14 Means For Penalties And Interest

Once a balance is due, two things typically happen while it remains unpaid.

Interest Accrues

Interest generally accrues on unpaid tax from the due date until the balance is paid in full, and the rate can change quarterly. The IRS explains that underpayment interest is compounded daily.

The Failure-To-Pay Penalty May Apply

If you do not pay by the due date listed on the notice, the IRS states the failure-to-pay penalty is generally 0.5% of the unpaid tax per month or partial month, and it can be reduced to 0.25% per month during an approved installment agreement.

This is why acting early matters. Even if you cannot pay in full, moving into a formal plan can slow the monthly penalty rate.

What To Do In 7 Steps

Use these steps in order. They are designed to help you avoid the two biggest mistakes people make with CP14: paying twice or ignoring it until the IRS escalates.

Step 1: Confirm The Notice Is Real And For The Right Tax Year

Start by checking the notice number (CP14) and the tax year involved. The IRS notes you can look up notices by number, and the CP or LTR number is typically on the notice itself.

If anything feels off, do not use contact information from a random email or text. Use the IRS guidance on notices and your official online account to confirm what is happening.

Step 2: Read The Amount Breakdown, Not Just The Total

CP14 generally shows tax due plus penalties and interest.

Write down these three items for your records:

- Tax year

- Total balance due

- Payment due date

Step 3: Check whether you have already paid or the IRS Has Not Posted Your Payment Yet

This matters more than most people realize.

In June 2024, the IRS acknowledged some taxpayers received CP14 notices showing a balance due even though they paid with their return, because the notice may have been triggered before the payment posted or because the payment needed additional handling. The IRS said those who paid in full and on time should not respond immediately while the IRS researches the issue, and any penalties and interest would be automatically adjusted when payments are applied correctly.

Practical checklist:

- Look for proof of payment (bank confirmation, canceled check, payment receipt).

- Create or sign in to your IRS online account to monitor whether the payment posts.

Step 4: If You Owe The Balance, Decide Whether You Can Pay In Full

If the balance is correct and you can pay it, paying sooner reduces ongoing interest and penalties.

The IRS lists multiple ways to pay, including paying through your online account.

Step 5: If You Cannot Pay In Full, Choose A Payment Path Immediately

The IRS is clear that if you cannot pay the full amount, you should still pay as much as you can and set up arrangements for the rest.

Two common paths:

- Apply for a payment plan online through the IRS Online Payment Agreement system.

- Review IRS payment plan and installment agreement options to match your balance and situation.

Step 6: If You Disagree With The Balance, Respond The Right Way

If you disagree, do not ignore the notice.

THC recommends calling the IRS number on the notice and having your paperwork ready (proof of payment, amended return, canceled checks, supporting documents).

If you have already paid and the payment has not been posted, TAS suggests monitoring your online account and responding within the timeline on the notice if the payment is not applied in time.

Step 7: Watch For CP14 Variants That Change The Instructions

Not every “CP14-looking” letter works the same way.

Two common variants:

- CP14C: The IRS says the payment due date is on the CP14C cover sheet, not the CP14 notice itself.

- CP14IA: issued when you owe money and have recently received correspondence about your payment plan.

If your letter is CP14C or CP14IA, follow the instructions for that specific notice type.

Payment Options: If You Cannot Pay in Full

If a CP14 balance is correct but paying it all at once would strain your budget, the goal is to get into a structured option before the IRS escalates the case.

Option 1: Online Payment Plan

The IRS online payment agreement application is the fastest route for many taxpayers, and the IRS explains that you typically need an IRS Online Account to apply.

Option 2: Installment Agreement Alternatives And Strategy

On the IRS side, installment agreements are part of the IRS payment plan system, with different plan types and setup fees depending on how you apply and how you pay.

On the Tax Hardship Center side, you can review what installment agreements look like and how they work in practice, especially if the balance is large or multiple years are involved.

Option 3: Hardship Options If Paying Anything Is Not Realistic

If paying the IRS would prevent you from meeting basic living expenses, you may need a hardship-based approach, not just a longer payment plan.

Option 4: Settlement Path When Full Payment Is Not Possible

An Offer in Compromise is a formal settlement program for qualifying taxpayers who cannot pay the full balance. Tax Hardship Center’s OIC resources explain the concept and the mechanics of application.

When To Get Professional Help

You can often handle CP14 yourself when it is a simple, single-year balance you can pay or place into an online plan.

Consider getting help when:

- You have multiple years involved, missing filings, or the balance seems incorrect.

- You already paid, but the IRS isn’t applying the payment, and deadlines are approaching.

- The amount is large enough that picking the wrong solution could trigger collection pressure, liens, or levies later.

FAQs

What Is A CP14 Notice From The IRS?

A CP14 is the IRS’s first balance-due notice and demand for payment. It states the amount due (including penalties and interest) and requests payment within a short timeframe.

What Should I Do First When I Receive A CP14 Notice?

Read the notice carefully, confirm the tax year and amount, and check whether you have already paid. The IRS and TAS both emphasize not ignoring the notice and paying or arranging payment if the balance is correct.

CP14 Vs CP501: Are They The Same?

No. CP14 is usually the first balance-due notice. CP501 is a reminder sent after the IRS did not receive your payment or response to a previous notice.

What If I Received A CP14, but I Already Paid?

The IRS has acknowledged that some taxpayers received CP14 notices even though they paid, due to timing or processing issues with payment posting. Verify your payment, monitor your IRS online account, and follow the instructions in the notice if the payment does not post on time.

How Long Do I Have To Respond To A CP14?

TAS notes CP14 requests payment within 21 days, and also explains that if the balance due is not fully paid within 60 days, the IRS can proceed with collection activity. Your specific notice dates still control, so use the deadline printed on your letter.

What Are My Payment Options If I Cannot Pay In Full?

The IRS provides payment plans and installment agreements, including the option to apply online through the payment agreement application.

Conclusion

A CP14 notice is the IRS’s first signal that your account shows a balance due. The fastest way to reduce stress is to confirm whether the balance is correct, then choose the right path: pay in full, set up a payment plan, or dispute the notice with documentation if it is wrong. If you have already paid, do not pay twice. Monitor your online account and respond within the required timeframe if the payment does not post.

Key Takeaways:

- CP14 is typically the first IRS balance-due notice and demand for payment.

- CP501 usually comes after CP14 as a reminder when the IRS has not received payment or a response.

- Interest compounds daily, and rates can change quarterly, so delays can increase the total cost.

- If you cannot pay in full, a formal payment plan can help, and an approved plan can reduce the monthly failure-to-pay penalty rate.

- If you have already paid, verify payment before paying again. The IRS has acknowledged that CP14 notices can sometimes go out before payments post, and corrections may be automatic once payments are applied.