Tax bills hit eight million Americans with penalties each year. The IRS charges one‑half of a percent per month for late payment, so a balance that starts at five thousand dollars can nearly double in nine years even without new tax added. About one‑third of penalty notices disappear once taxpayers learn how to ask the IRS to waive penalty charges and present clear proof. First Time Penalty Abatement grants relief in roughly 65 percent of accepted cases, saving filers an average of seven hundred dollars. Most requests reach a decision in six to twelve weeks. File Form 843 or call the IRS within 30 days of the notice so interest does not snowball.

Keep reading to match your situation with the right relief lane, draft a clean request, and see how Tax Hardship Center can back you up if the Service pushes back.

Understanding IRS Penalties and Relief Options

This section breaks down every common IRS penalty, shows how interest compounds, and outlines each path the Service offers to lift extra charges.

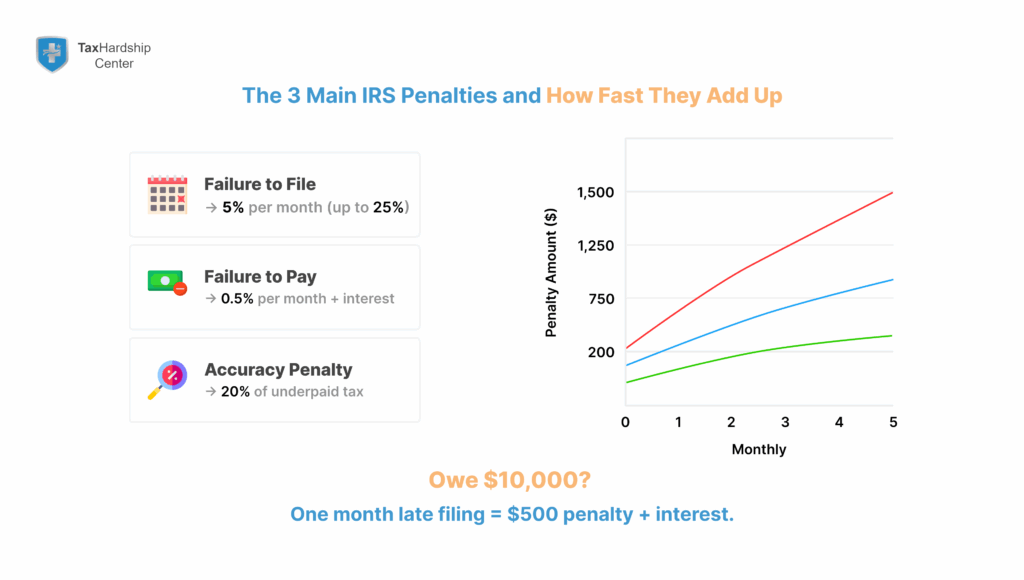

The IRS publishes roughly a hundred civil penalties, but three dominate individual notices: failure to file, failure to pay, and failure to deposit payroll taxes. Late filing costs five percent of tax due per month up to 25 percent. Late payment adds half a percent per month. Both stack interest that compounds daily at the federal short‑term rate plus three points. For a family owing ten thousand dollars, a single late filing month costs five hundred dollars plus interest; twelve months reaches the full ceiling of twenty‑five hundred dollars. Accuracy penalties land when numbers stray by at least ten percent. Each penalty carries a code on Notice CP or Letter 500 series. Study the code, because relief eligibility differs.

The IRS offers three primary waivers. First Time Penalty Abatement helps taxpayers who kept a clean record in the prior three years. Reasonable cause relief covers emergencies, disasters, and reliance on bad advice. Statutory exemption relief comes straight from law, often tied to federally declared disasters or combat‑zone service. All waivers require you to correct the original problem. That means file the missing return, pay or arrange payment of tax, and document everything. The IRS will not consider relief while compliance gaps remain.

A quick win lives in the First Time Penalty Abatement lane. Reasonable cause needs more evidence, but it covers more situations across unlimited tax years. Statutory waivers apply automatically once the IRS updates its systems, though the update sometimes lags. You can prompt faster action with a phone call.

Penalties That Qualify

- Failure to file

- Failure to pay

- Failure to deposit employment taxes

- Accuracy penalties under Section 6662

- Information return penalties for Form 1099 series

Penalties That Face Tough Review

- Trust fund recovery

- Civil fraud

- Erroneous refund penalties

The IRS assessed 37.3 million civil penalties last fiscal year and later removed 5.6 million after taxpayers asked. Those numbers prove that informed requests work. For deeper tactics, see our post on IRS penalty abatement strategies.

Partner With Tax Hardship Center Early

The sooner you consult a professional, the faster penalties disappear and interest stops ballooning. Our services at Tax Hardship Center include a rapid account transcript pull, a compliance check, and a tailored action plan within one business day. If First Time Penalty Abatement fits, our team files a same‑day request. When reasonable cause looks stronger, we gather evidence and draft a persuasive letter grounded in Penalty Abatement guidelines. For larger balances, we may pair abatement with an Offer in Compromise to resolve the underlying debt. Clients who follow our fast‑track roadmap save an average of four thousand dollars and close cases four weeks sooner than do‑it‑yourself filers.

First Time Penalty Abatement Explained

This section guides you through the requirements, timing, and tactics for a fast First Time Penalty Abatement, the easiest relief for clean taxpayers.

First Time Penalty Abatement, often called FTA, wipes a single tax year or quarter of late filing, late payment, or failure to deposit penalties. You qualify by meeting three tests. First, you filed all returns, even returns with zero tax. Second, you paid or arranged full payment of the tax due on the year you want waived. An installment agreement counts as payment for this test. Third, you stayed penalty‑free for the three tax years before the year in question. The IRS checks these tests in seconds through its master file.

Call the number on your notice, state that you request First Time Penalty Abatement, and ask the agent to run an “FTA screen.” The system returns an immediate yes or no. If yes, you will hear the amount credited and the remaining balance. Write the agent’s name and badge number, then ask for a faxed confirmation. If the agent says no because of an unfiled return, resolve the filing and call again.

Written requests work when you prefer paper trails or have multiple years to address. Draft one letter per year and attach Form 843. The IRS will apply the same tests but may take up to twelve weeks to answer. Use certified mail to lock in the request date.

When to Use FTA

- Your compliance record is spotless for three years

- Penalties exist only for late payment or filing

- You can pay the tax within 30 days

Common FTA Pitfalls

An open audit disqualifies the request. An installment agreement in default also derails relief. Solve those issues first. Many taxpayers lose FTA by calling before they file the missing return, so remember: file, then ask.

Tax Hardship Center explains FTA in more depth on our Form 941 penalty guide, which details mistakes payroll filers make and how to fix them.

Reasonable Cause: Build a Strong Case

Learn how to frame facts, gather proof, and persuade the IRS that life events, not neglect, caused the late filing.

Reasonable cause centers on what a prudent person would do under the same circumstances. The IRS agent looks for an event out of your control that ties directly to the failure and shows you acted as soon as the barrier lifted. Serious illness, death in the immediate family, natural disaster, fire, or unavoidable absence rank high. Reliance on incorrect written advice from a tax professional also qualifies. A torn rotator cuff that kept you in surgery on April 15 could support reasonable cause. A busy schedule does not.

Build a tight timeline. Start when the event struck. Note each attempt to comply, each call to the IRS, and each stride toward resolution. Next, collect documents. Hospital discharge papers, insurance claims, police reports, or FAA incident logs all play. Attach only the pages that prove dates and facts. More does not equal better. The goal is clarity.

Structuring Your Narrative

- Event description

- Immediate impact on tax duties

- Steps you took to comply once able

- Current compliance status

Documentation Essentials

- Medical records with dates

- Ownership documents showing lost records replaced

- Letters from tax professionals admitting fault

- Witness affidavits for events without formal paper

When weather disasters strike, the IRS often issues automatic penalty relief. Check the official notice at IRS penalty relief for 2020 and 2021 returns to see if your state receives automatic protection.

Preparing Your Penalty Abatement Request Letter

A superior letter shortens review time and lifts approval odds. This section walks through every element and includes stylistic tips.

Start with the taxpayer information block. Use uppercase for your name and address to ensure scanning software reads it. List the tax year, form, notice number, and penalty amount. In the first paragraph state the request and cite either First Time Penalty Abatement or reasonable cause. Keep sentences under twenty words for clarity.

Next, lay out a numbered timeline. Each point starts with a date, continues with the action, and ends with the result. Example: “March 10, 2025: Tornado destroyed home office, including tax records. Filed insurance claim same day.” This format shows effort.

Add a paragraph that references law. Quote Internal Revenue Manual 20.1.1 and show how your facts fit. Conclude with a statement of ordinary business care: “Throughout the period I exercised ordinary care by maintaining bookkeeping software, engaging a CPA, and remitting quarterly estimated tax.” Sign in blue ink and add a phone number.

Attachments Index

- FEMA claim 12345

- Hospital discharge summary

- CPA engagement letter

- Proof of tax paid on April 30, 2025

Mailing and Follow Up

Send to the address on the notice by certified mail with return receipt. The IRS date‑stamps receipt within three days of delivery. Check the tracking number and save the green card. Call the IRS at day 30 to confirm the letter reached the queue.

Filing Form 843 for Penalty Relief

Form 843 turns your narrative into an official request. This section breaks down every line you must fill.

Lines 1 through 3 ask for taxpayer name, address, and identification. Use the same address on your tax return. Check the box for penalty or addition to tax on Line 4. On Line 5a mark the code for failure to file or pay. On Line 5b enter the year. The critical detail lands on Line 7. Write a short reason such as “First Time Penalty Abatement per IRM 20.1.1” or “Reasonable cause due to Hurricane Ida disaster DR‑4611‑LA.” Attach a full explanation letter.

Filing Time Limits

You must file within three years after the return due date or two years after you paid the penalty. Treasury Regulation 301.6402‑3 sets those windows.

Where to Send

Individuals mail Form 843 to the same service center that processes the original return. Businesses send to the Ogden, Utah center. Verify the address on Form 843 instructions before mailing.

Electronic Filing Option

Large payroll processors and some tax software now allow Form 843 through the Modernized e‑File channel. Check with your provider because the IRS plans to expand the pilot.

Calling the IRS: What to Say

A live call can erase penalties in minutes when you follow a tight script. This section provides that script.

Start with identity verification: name, address, last four of Social Security, filing status, and prior year refund amount if requested. State: “I am calling to request First Time Penalty Abatement on my 2024 Form 1040 late payment penalty.” Pause for the agent to run the FTA tool. If you seek reasonable cause, say: “I have documentation of a house fire that prevented timely filing. May I fax it to you now?” Most agents provide a secure fax number or open an e‑fax inbox.

If the agent approves, ask for the amount waived, the remaining balance, and the date interest will adjust. Request confirmation by secure message or fax. If denied, ask for the denial reason, and request a supervisor review. Note every detail because you may need it for a written appeal.

Best Times to Call

- Tuesday through Thursday right after 8 a.m. local time

- Last week of the month, when call volume dips

- Avoid the day after a holiday when hold times triple

Check your transcript the next Friday to see if code 290 posted with zero amount. If not, plan a written follow‑up.

Tracking Your Request and Next Steps

Know how to read your transcript and what to do if the answer takes longer than promised.

Create an IRS Online Account and download the Account Transcript for the tax year. The transcript lists each transaction by date and code. Code 290 with zero amount indicates the penalty disappeared. Code 294 marks partial abatement. A denied request shows code 350 “Penalty Reversal Denied.” If the transcript remains unchanged after twelve weeks, call the IRS with your certified mail receipt handy and ask for the status.

Interest on the underlying tax continues, so pay the balance or start an installment agreement even while you wait. Interest stops only when the tax balance reaches zero. The IRS charges an interest rate that resets quarterly. Paying faster always saves money. When payment in full feels impossible, ask about our negotiate with the IRS program to set realistic terms.

Appeal Rights

File Form 9423 within 30 days of a denial to reach the Office of Appeals. Attach a copy of your original letter and cite additional evidence. Appeals officers work independently and often approve relief when the field office skipped guidelines.

Reapplication Strategy

You may submit a fresh Form 843 if new facts emerge, such as a disaster declaration issued after the first request. Highlight the new information in the cover letter.

How Tax Hardship Center Helps

At Tax Hardship Center, we help you erase penalties and settle tax debts without guesswork. A dedicated enrolled agent pulls transcripts and runs a compliance check within 24 hours. We map the fastest relief route, whether it is First Time Penalty Abatement, reasonable cause, or a statutory waiver under a disaster declaration. Our in‑house writers craft letters that mirror the language in Internal Revenue Manual 20.1.1 and Treasury Regulation 301.6402‑2.

Our tax debt forgiveness guide explains how these penalty removals sync with an overall debt‑settlement strategy. For balances that stretch budgets, we can roll abatement into an Offer in Compromise to finish the job. Clients save four thousand dollars on average and see cases close in under three months. We charge a transparent flat fee—no percentages.

Added Value

- Same‑day case analysis

- Direct line for client calls

- Written guarantee of response time

- Money‑back promise if we cannot submit a request

In summary…

Here is the fast track to lighter IRS pressure.

- Clean up filings before you speak with the Service

- Check your record for First Time Penalty Abatement eligibility

- Build a clear timeline and attach hard proof for reasonable cause

- Use Form 843 and a concise letter to formalize the request

- Call the IRS to speed review and document each conversation

- Watch your transcript weekly and appeal quickly if denied

Act early, stay organized, and lean on experts when the dollar signs grow. The IRS follows published rules. Show you meet those rules and penalties fall away.

FAQs

What is the fastest way to ask the IRS to waive a penalty?

A phone request for First Time Penalty Abatement removes eligible late filing or payment penalties during the call when your history qualifies.

Does the IRS remove interest along with penalties?

The IRS removes interest tied to the penalty amount once the penalty disappears. Interest on the tax itself stays until you pay the balance.

How long does penalty abatement take through Form 843?

Most written requests post a decision within six to twelve weeks, though disaster periods and peak filing months may push the timeline.

Can I ask for penalty relief twice?

You may request reasonable cause relief as many times as events warrant. First Time Penalty Abatement applies once every four years.

Will asking for penalty abatement flag my return for audit?

No. Penalty abatement runs through the Account Management function. The process does not increase examination risk.

Need personal guidance on how to ask the IRS to waive penalty charges? Contact Tax Hardship Center today for a free transcript review and a clear action plan.