You opened your mail and found a letter from the IRS saying your return was changed and that you now owe money.

Not the kind of letter anyone wants. But it is not the end of the world either.

A CP21A notice is something many taxpayers receive, and most resolve it without drama. The key is to understand exactly what it means and respond appropriately before the balance grows.

Here is everything you need to know.

What Is a CP21A Notice?

A CP21A is a notice from the IRS confirming that changes were made to your Form 1040 and that those changes resulted in a balance you now owe.

This is the opposite of a CP21B. Where a CP21B tells you a refund is coming, a CP21A tells you that the math moved against you. A correction was made, and you now owe more than your original return showed.

The balance on a CP21A is not a proposal. It is the IRS telling you the change has already been applied and the amount is due.

According to the IRS’s official CP21A notice page, the notice also includes details about interest charged on the unpaid balance from the return’s original due date.

Why Did You Get One?

There are several reasons the IRS sends a CP21A.

You filed an amended return. If you submitted a Form 1040-X to correct something on a prior-year return and that correction resulted in additional tax owed, the CP21A is the IRS’s confirmation of the new balance.

The IRS corrected your return. Sometimes the IRS catches a discrepancy during processing. A credit that was calculated incorrectly, a deduction that was adjusted, or a mismatch with information reported by a third party can all trigger a change. If the correction increases what you owe, you get a CP21A.

A previously approved agreement changed your account. In some cases, changes to a payment plan or a prior resolution can result in a CP21A reflecting the adjusted balance.

Whatever the source, the notice will spell out the tax year affected, what changed, and the amount now owed. Read those three things first.

What Is Actually Inside the Notice

The CP21A includes several distinct sections, and it helps to know what each one is telling you.

Billing summary. This shows the updated balance due, including the original tax, any interest charged, and any penalties applied. These are listed separately so you can see exactly how the total was calculated.

Payment coupon. A detachable section at the bottom for mailing a check or money order. The notice number and tax year are printed on it. If you pay by mail, use this.

Payment options. The notice outlines how you can pay, including online through IRS Direct Pay, by phone, or by mail. It also references the option to set up a payment plan if you cannot pay the full amount immediately.

Interest and penalty detail. The IRS charges interest on unpaid balances from the original due date of the return, not from the date of the notice. This means interest may already be higher than you expect, especially if the tax year affected was a few years ago.

What the IRS says to do. This section outlines your response options and the deadline. Pay attention to the date shown. That is your window.

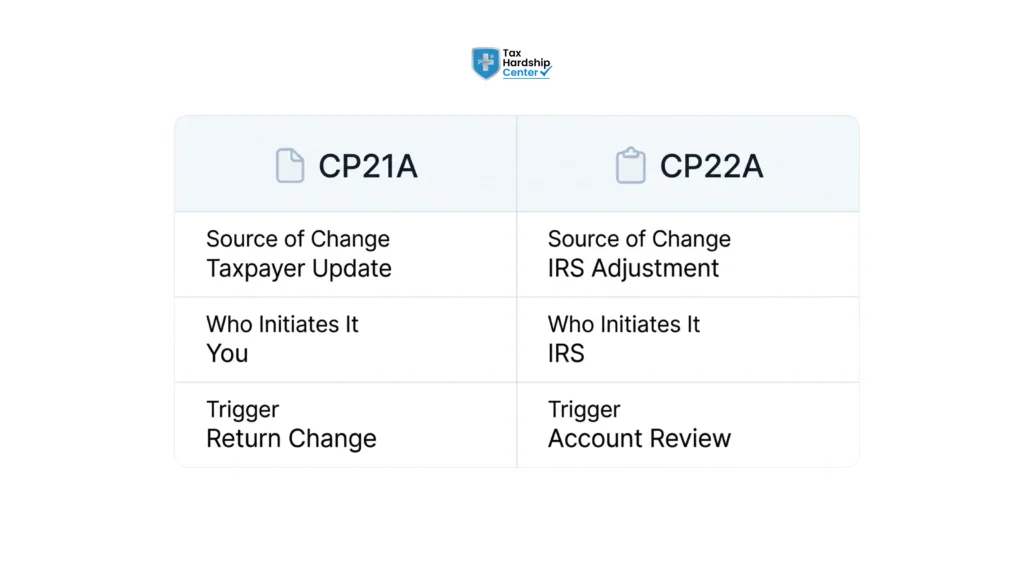

CP21A vs CP22A: What Is the Difference?

This is a question that comes up constantly, and the distinction matters.

Both notices tell you that a change was made, and you now owe money. The difference is in what triggered the change.

A CP21A results from a change that was requested or initiated on your behalf. That usually means an amended return you filed or a correction resulting from a prior agreement or communication with the IRS.

A CP22A results from a change the IRS made on its own during processing, often due to a discrepancy between your return and information from an employer, bank, or other third party.

In practice, both notices mean the same thing: a balance is owed, and a response is needed. But knowing which one you have helps you trace where the change came from and whether it is worth disputing.

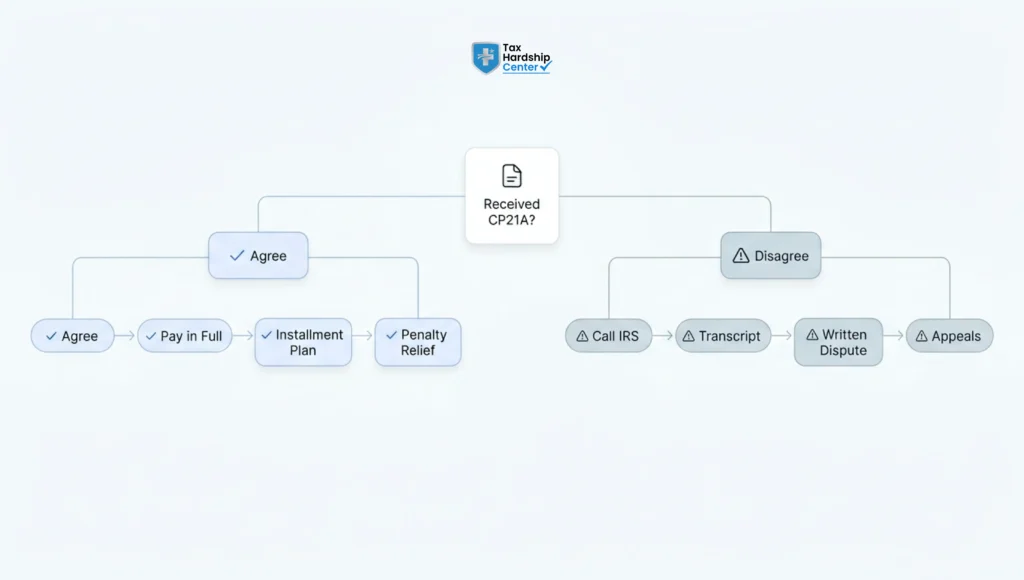

What to Do If You Agree With the Changes

If the CP21A makes sense to you, whether because you filed an amended return or because the IRS correction is clearly accurate, here is how to move forward.

Pay in full. The fastest way to stop interest from growing. You can pay online through IRS Direct Pay using a bank account at no cost. You can also pay by phone or use the payment coupon in the notice to mail a check.

Set up an installment agreement. If paying the full amount right now is not possible, a payment plan lets you pay the balance in monthly installments. The IRS offers both short-term plans (paid within 180 days) and long-term plans. Understanding your IRS payment plan options before you call the IRS helps you choose the right one for your situation.

Request penalty abatement. If penalties have been added to your balance and this is your first time facing this situation, you may qualify for first-time penalty abatement. This does not eliminate the underlying tax, but it can meaningfully reduce the total you owe.

What to Do If You Disagree

Getting a CP21A for a change you did not initiate, or one that does not look right, is frustrating. But you do have options.

Call the number on the notice. Start there. Have your original return, the notice, and any relevant documents in front of you. Ask the IRS agent specifically what change was made, what triggered it, and what documentation they used.

Request your account transcript. This shows everything that has been applied to your account for that tax year. It is the clearest way to see exactly what happened and in what order. You can request it through the IRS Get Transcript service.

Submit a written response. If the issue cannot be resolved by phone, put your dispute in writing. Include copies of any supporting documents. Send it to the address on the notice and keep a copy for yourself.

File a corrected amended return. If the CP21A relates to an amendment you previously filed and you believe it was applied incorrectly, a new 1040-X may be necessary. This is worth doing with professional help to avoid causing further confusion with your account.

Escalate to the IRS Office of Appeals. If the IRS does not accept your explanation, you have the right to request an independent review. The Office of Appeals is separate from the team that made the original change.

What Happens If You Ignore a CP21A

Short answer: the balance grows, and more notices follow.

Interest compounds daily on the unpaid amount. Penalties can be added on top. And if the balance remains unpaid long enough, the IRS will move through the standard escalation sequence: CP501, CP503, CP504, and eventually enforcement action, including tax liens and levies.

A tax lien can affect your credit and your ability to sell property or get financing. A levy can be taken from your bank account or wages. Neither of those outcomes is inevitable from a CP21A, but both become more likely the longer the notice sits unaddressed.

The IRS is not rushing to collect. But they are not waiting indefinitely either.

When a CP21A Is More Complicated Than It Looks

Most CP21A notices are straightforward. You owe a balance; you pay it or set up a plan, done.

But sometimes a CP21A surfaces something bigger.

If the notice references a tax year where you also have unfiled returns, the CP21A balance may be just one piece of what the IRS has noted on your account. Resolving the notice without addressing the bigger picture can create additional problems.

If the balance on the notice is much larger than expected, it may involve penalties and interest that have been building for a while. In those cases, penalty abatement and an installment agreement together can be more effective than paying the listed balance alone.

And if you have received multiple IRS notices across different tax years, a single CP21A is unlikely to close the full issue. That is worth knowing before you call the IRS to resolve one notice and discover there are others.

How Tax Hardship Center Helps With CP21A and Related IRS Balances

When a CP21A lands with a balance you were not expecting, the instinct is to either pay it immediately or avoid it. Neither response is always right. Tax Hardship Center works through the notice with you to ensure the balance is accurate, the response is correct, and the resolution fits your financial situation.

For taxpayers who agree with the changes but cannot pay in full, the firm sets up installment agreements that reflect actual cash flow, not just the IRS minimum. For those who believe the change is wrong, the team handles the dispute process directly, including account transcript requests, written responses, and IRS calls.

If the CP21A is connected to a larger IRS issue, whether that is back taxes, unfiled returns, or prior notices that went unresolved, the Tax Hardship Center addresses the full picture through its tax debt resolution services. Get a free case review to find out exactly what you are dealing with before the interest compounds further.

FAQs

What is notice CP21A?

CP21A is an IRS notice confirming that a change was made to your Form 1040, and you now owe a balance as a result. The change has already been applied to your account, and interest begins accruing from the return’s original due date.

What is the difference between CP21A and CP22A?

A CP21A results from a change that was initiated on your behalf, such as an amended return you filed. A CP22A results from a change the IRS made on its own during processing, often due to a discrepancy with third-party information. Both mean a balance is owed, but the source of the change is different.

Will a CP21A lead to collections?

Not immediately. But if the balance goes unpaid, the IRS will send escalating notices and may eventually take enforcement action, including tax liens and levies. Responding within the timeframe of the notice prevents that sequence from starting.

Do I need to amend my return after a CP21A?

Not usually. The CP21A confirms a change that has already been processed. Filing another amended return in response could further complicate your account. If you believe the change is incorrect, dispute it through the IRS rather than filing a new amendment without guidance.

What happens if I cannot pay the full balance on a CP21A?

You can request an installment agreement to pay over time. Both short-term and long-term options are available. Interest continues to accrue during the plan, but it stops the account from escalating to enforcement while you pay.

How long do I have to respond to a CP21A?

The notice will include a specific date. In most cases, you have 21 days before additional interest and penalties begin compounding more significantly. For disputes, acting within 60 days of the notice date gives you the strongest position.

What if I did not initiate any change but still received a CP21A?

Call the IRS using the number on the notice and ask specifically what change was made and what triggered it. If the change was made based on third-party information the IRS received, reviewing your account transcript will show exactly what was applied. If you suspect someone else made changes to your return, report it as potential identity theft.

Conclusion

A CP21A indicates that a change was made to your return and that you owe the difference. It is not a catastrophe. But it does need a response.

Check that the balance is right. Understand where the change came from. Then pay it, plan it, or dispute it, depending on what the notice actually reflects.

The worst thing you can do is nothing. The IRS will keep the clock running regardless of whether you open the letter.

Key Takeaways

- CP21A confirms a change was already applied to your Form 1040 that resulted in a balance owed

- Interest accrues from the original due date of the return, not from when you receive the notice

- Common causes include amended returns you filed and IRS processing corrections

- CP21A differs from CP22A in the source of the change, though both result in a balance due

- You can pay in full, set up an installment agreement, or request penalty abatement if eligible

- Disputing a CP21A requires calling the IRS, reviewing your transcript, and potentially submitting a written response

- Ignoring a CP21A triggers escalating notices and eventually enforcement action including liens and levies

- A CP21A connected to broader unresolved IRS issues should be addressed as part of the full picture

- Acting within the timeframe on the notice gives you the most options at the lowest total cost

- A professional representative can handle the dispute or payment plan process more efficiently than navigating it alone

Not sure whether your CP21A balance is right or how to respond? Get a free case review with Tax Hardship Center and get a straight answer before the interest clock runs further.