You filed your return. You thought you were done. Then a letter showed up saying you owe more money.

That letter is a CP22A. And before you panic or toss it in a drawer, here is what it actually means and what you should do right now.

What Is a CP22A Notice?

A CP22A is a notice from the IRS telling you that changes were made to your Form 1040 and that you now owe a balance as a result.

These changes could come from information you submitted yourself, like an amended return, or from corrections the IRS made during processing. Either way, the result is the same: a new balance due that was not on your original return.

According to the IRS’s official CP22A notice page, this notice is not a bill for unpaid original taxes. It is specifically tied to a change that was applied to your account. That distinction matters when deciding how to respond.

Why Did You Get One?

There are a few common reasons a CP22A lands in your mailbox.

You filed an amended return. If you submitted a Form 1040-X to correct something on a prior return and that correction resulted in additional tax owed, the IRS sends a CP22A to confirm the new balance.

The IRS corrected your return. Sometimes the IRS identifies a math error, an incorrectly calculated credit, or a discrepancy between what you reported and what a third party (your employer, a bank, or a brokerage) reported. The correction gets applied, and you get the notice.

A tax relief agreement changed your balance. In some cases, if a previously approved resolution was modified or a payment was misapplied, you may see a CP22A reflecting the adjusted amount.

Whatever the reason, the notice will include the affected tax year, the amount now owed, and a due date. Read all three carefully before doing anything else.

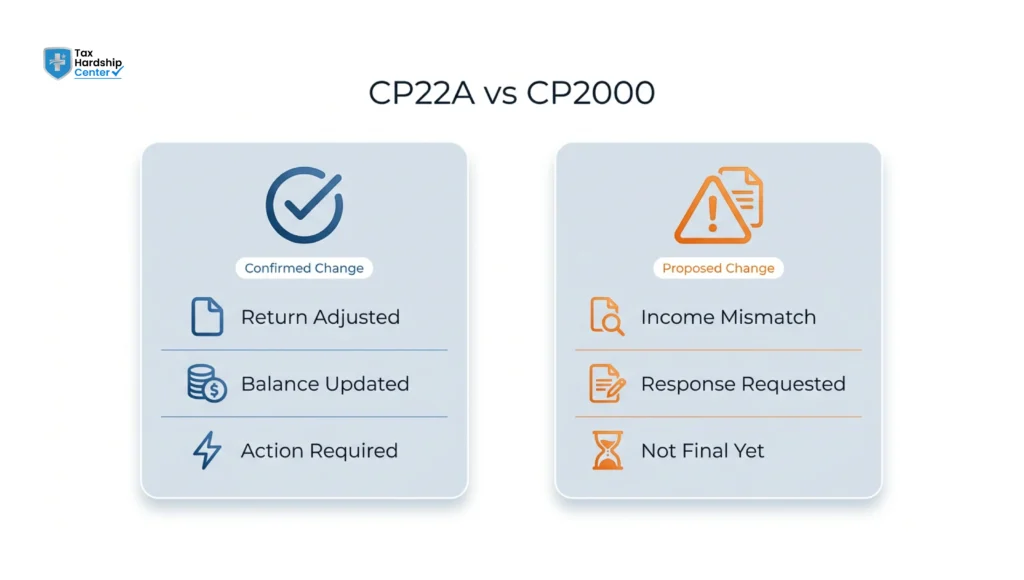

CP22A vs CP2000: Not the Same Thing

This one confuses a lot of people, and the confusion leads to wrong responses.

The CP2000 is a proposed notice. The IRS is saying: “We think your income was underreported. Here’s what we think you owe. Do you agree?” You have a chance to respond before anything is finalized.

The CP22A is a confirmation notice. The change has already been applied to your account. The balance shown is what the IRS says you owe right now, not a proposal.

That means the window for pushing back on a CP22A is narrower. It does not mean you cannot dispute it, but the process is different, and the timeline is tighter.

If you also received a CP2000 notice at some point before this, the CP22A may be the result of how that situation was resolved. Understanding the sequence matters.

How Much Time Do You Have?

The CP22A gives you 21 days to pay the balance shown before interest begins accruing on the unpaid amount.

Penalties may also apply if the balance remains unpaid. The IRS charges interest on unpaid tax from the due date of the original return, and late payment penalties can add up faster than most people expect.

If you need time to figure out your options, that is fine. But do not let the 21 days pass without at least making contact or setting up a resolution. Silence is interpreted as inaction, and inaction leads to the next level of notices, which escalate toward levy and collection action.

What Happens If You Ignore It

Short answer: more notices, more interest, and eventually enforcement.

The CP22A is not the last word the IRS will send. Ignore it, and you will likely receive a CP501, then a CP503, then a CP504. Each one carries more urgency and more financial consequences.

Interest compounds daily on unpaid balances. Penalties stack. And if the balance grows large enough, the IRS can file a tax lien against you, which affects your credit and your ability to buy property or secure financing.

None of this happens overnight. But it all starts with not responding to a notice like this one.

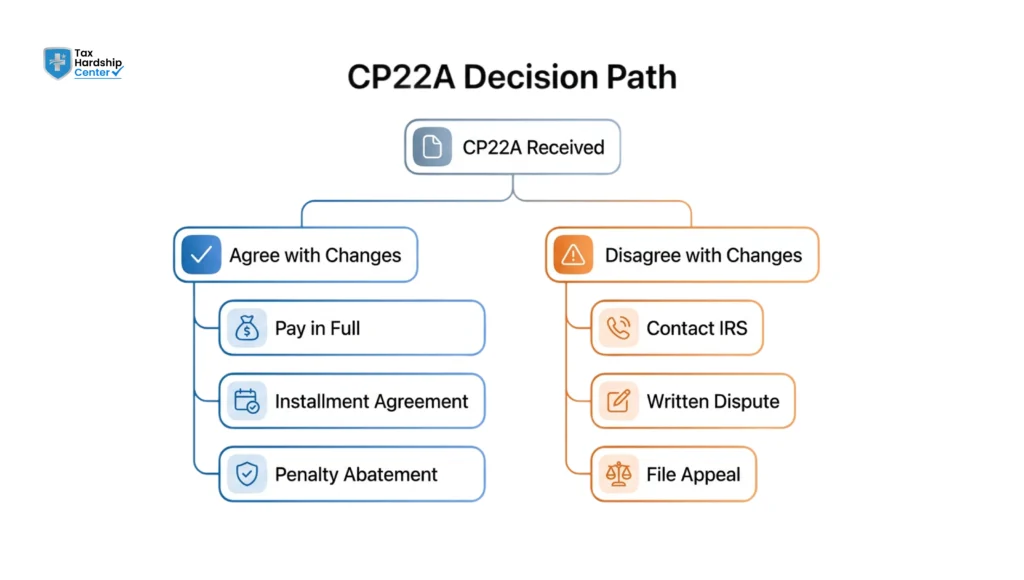

Your Options When You Agree With the Changes

If the CP22A reflects a change you already knew about, or one you now understand and accept, here is how to move forward.

Pay in full. The fastest way to close the matter. You can pay online at IRS Direct Pay using your bank account, or by check using the payment voucher included with the notice.

Set up an installment agreement. If you cannot pay the full amount right now, you can request a payment plan.IRS Form 9465 is the standard way to apply. Short-term plans (paid within 180 days) and long-term plans (with monthly installments) are both available, depending on your balance and financial situation.

Request penalty abatement. If this is your first time facing a balance due, or if circumstances made timely payment genuinely impossible, you may qualify for a first-time penalty abatement. This does not remove the tax owed, but it can reduce the penalties added on top.

Your Options When You Disagree

If you believe the change on your CP22A is wrong, you have the right to dispute it. But you need to act within the timeframe shown on the notice.

Here is what the dispute process looks like:

Call the number on the notice. Start by calling the IRS directly. Have your notice, your original return, and any supporting documents ready. Explain specifically why you believe the change is incorrect.

Submit a written response. If the issue requires documentation, send a written explanation along with copies of the relevant records. Do not send originals.

Request an amended return review. If the change came from a 1040-X you filed, and you believe the IRS applied it incorrectly, you may need to walk through the amendment with an IRS agent or have a representative do so on your behalf.

File a formal appeal. If the IRS does not agree with your position after the initial contact, you can escalate to the IRS Office of Appeals. This is a separate, independent process within the IRS where your case is reviewed by someone who was not involved in the original decision.

For a complex dispute, working with a professional representative is usually faster and more effective than navigating it alone. The IRS responds differently when a licensed representative is on the case.

Why Taxpayers Trust the Tax Hardship Center for CP22A Resolution

When a CP22A lands with a balance you were not expecting, the first reaction is usually confusion, followed quickly by stress. Tax Hardship Center handles exactly this situation every day for taxpayers who are unsure whether to pay, dispute, or negotiate.

The firm specializes in IRS notice resolution, which means reviewing the notice, tracing the change back to its source, and advising on the fastest and most cost-effective path forward. If the balance is correct and payment is not immediately possible, Tax Hardship Center sets up installment agreements that match your actual cash flow, not just the minimum the IRS prefers. If the balance is wrong, the team handles the dispute process, including written responses, IRS calls, and appeals if needed.

For taxpayers whose CP22A is part of a larger unresolved IRS situation, whether there are unfiled returns, prior balances, or earlier notices that went unanswered, the tax debt resolution process at Tax Hardship Center addresses the full picture. One issue rarely exists in isolation. Get a free case review and find out exactly where you stand before the interest clock runs any further.

FAQs

What does CP22A mean?

CP22A is an IRS notice confirming that a change was made to your Form 1040 and that you now owe a balance as a result. The change may come from an amended return you filed or a correction the IRS applied during processing.

Is CP22A the same as CP2000?

No. A CP2000 is a proposed notice that asks you to confirm or dispute an income discrepancy before any changes are made. A CP22A confirms a change that has already been applied to your account. The CP22A means the balance is already official.

Can I pay CP22A online?

Yes. You can pay the balance shown on a CP22A at IRS Direct Pay using your bank account, at no fee. The payment option is also listed on the notice itself, along with the payment voucher for check or money order.

How do I dispute a CP22A?

Call the number on the notice with your documentation ready. If the issue requires more than a phone call, submit a written response with supporting records. If the IRS does not accept your explanation, you can escalate to the IRS Office of Appeals.

What happens if I cannot pay the full amount on a CP22A?

You can request an installment agreement to pay over time. Short-term plans allow up to 180 days; long-term plans set up monthly payments. Interest continues to accrue on the unpaid balance during the plan, but it prevents the account from escalating to enforcement.

What if I had never received earlier notices before the CP22A?

This happens. Notices sometimes go to an old address or get lost. The IRS is not required to prove you received every prior communication before sending a CP22A. Contact the IRS to explain the situation and request a review of the account history.

How long do I have to respond to a CP22A?

The notice gives you 21 days to pay before interest begins. For disputes, the window is typically 60 days from the date of notice. Acting sooner always gives you more options than waiting until the deadline.

Conclusion

A CP22A is not the end of the world. It is a notice that a change was made to your return and a balance is now due. That balance can be paid, disputed, or resolved through a plan, depending on your situation.

What it cannot be is ignored. The sooner you respond, the more options you have and the less it ends up costing you.

Key Takeaways

- CP22A confirms a change already made to your Form 1040, with a balance now owed

- It is not the same as a CP2000, which is a proposal you can respond to before anything is finalized

- Common causes include an amended return, an IRS processing correction, or a third-party income discrepancy

- You have 21 days to pay before interest begins accruing on the balance

- Ignoring a CP22A leads to escalating notices and eventually IRS enforcement action

- You can pay in full, set up an installment agreement, or request penalty abatement if eligible

- Disputes must be initiated within the timeframe shown on the notice

- Written responses to the IRS should include copies of supporting documents, never originals

- A licensed representative can handle the dispute or negotiation process on your behalf

- Acting within the 21-day window gives you the most options at the lowest total cost

Not sure whether to pay, dispute, or negotiate? Get a free case review with Tax Hardship Center and get a straight answer before the interest compounds further.