A CP504 notice is the IRS raising the stakes. It usually shows up after earlier balance-due letters did not get resolved, and it is designed to push your case closer to enforcement.

If you respond the right way now, you can often prevent the situation from becoming a wage or bank levy issue. The goal is simple: get the IRS out of “enforcement mode” and into an approved resolution, as fast as possible.

What CP504 Means And Why It’s Serious

CP504 is the IRS’s Notice of Intent to Levy under Internal Revenue Code section 6331(d). The IRS says you received it because they have not received payment of your unpaid balance.

The IRS also states that if you do not pay the amount due immediately, it can levy your income and bank accounts, and seize your property or rights to property, including your state income tax refund.

Two details matter here:

- CP504 is described by the IRS as your final reminder that they intend to levy and that they will begin searching for other assets to levy.

- The IRS also notes it can file a Notice of Federal Tax Lien if it has not already done so.

CP504 may also include passport-related language. The IRS explains that seriously delinquent tax debt can trigger certification to the State Department under the FAST Act passport rules.

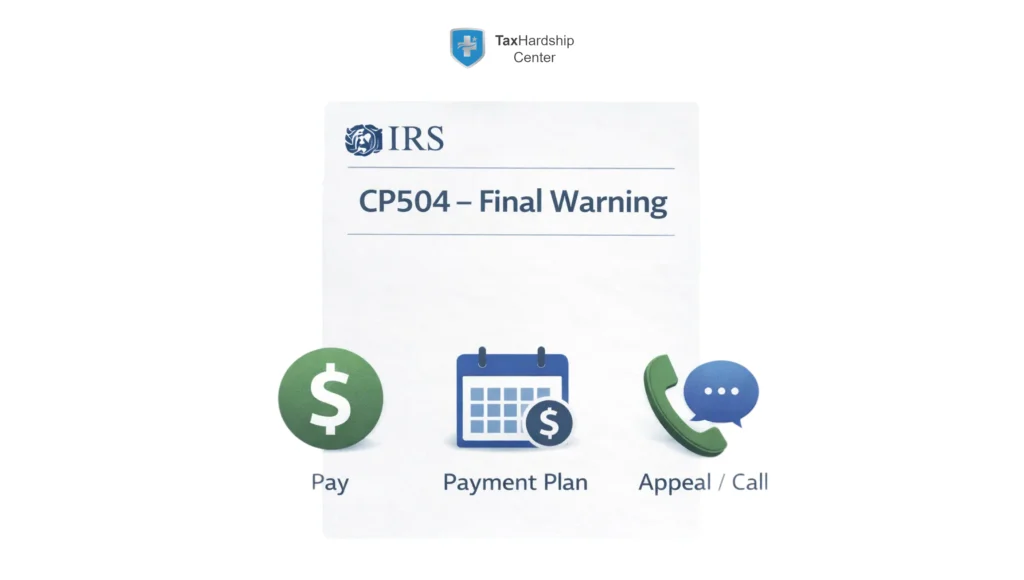

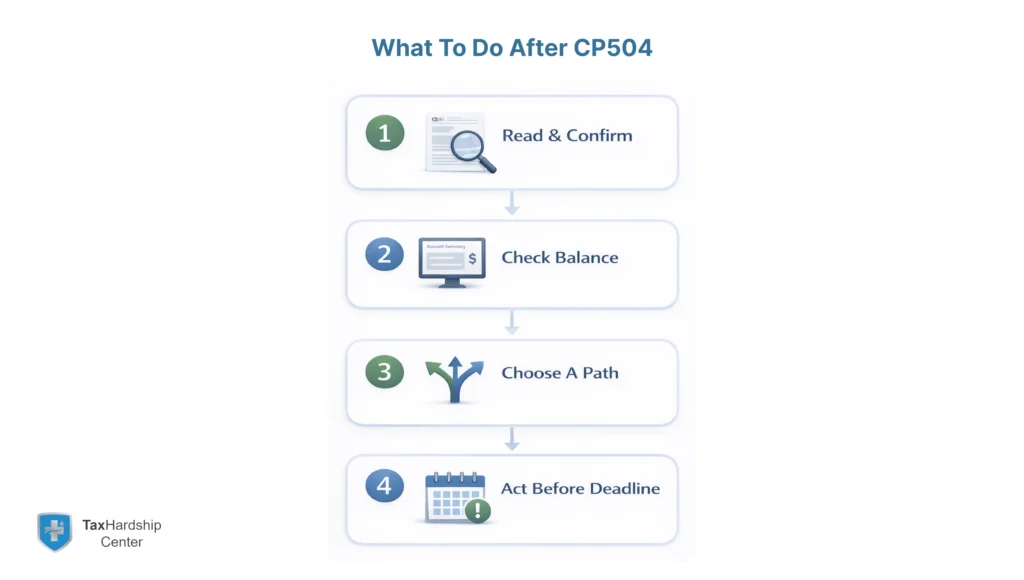

Immediate Actions To Prevent Enforcement

First Hour: Stop Guessing And Get The Facts

- Read the notice top to bottom, and highlight the tax year(s), balance, and any deadline printed on it.

- If you already paid or set up an installment agreement, do not assume the IRS updated your account. The IRS specifically says you should still call to make sure your account reflects payment or an arrangement.

- Log in to your IRS account to confirm the balance and payment history if you can.

First 48 Hours: Choose One Of Three Paths

Path 1: Pay In Full (If You Truly Can)

Paying in full is the fastest way to end enforcement risk. The IRS instructs taxpayers to pay the amount owed immediately.

Path 2: Set Up A Payment Plan (Most Common Best Move)

If you cannot pay in full, move straight to a payment plan, because it is the most direct way to show cooperation and stabilize the account. The IRS tells you to make a payment plan if you cannot pay the full amount.

Path 3: Call If You Disagree

If you believe the notice is wrong, or you have already fixed it, the IRS says to call the toll-free number on your notice.

First Week: Reduce Risk Even Further

- Make a partial payment if possible. Even a partial payment can reduce ongoing additions and show good-faith movement while you finalize a plan.

- Get compliant. If you have unfiled returns, that can block approvals for many resolution options, including some payment plans.

- Keep documentation. Save screenshots, confirmations, and certified mail receipts if you send anything by mail.

How To Set Up An IRS Payment Plan From CP504

For many taxpayers, the fastest option is the IRS Online Payment Agreement system, which allows you to apply online and receive immediate approval decisions in many cases.

Step By Step: Online Payment Agreement

- Create or sign in to your IRS Online Account.

- Go to the IRS Online Payment Agreement application.

- Choose your plan type and monthly payment amount.

- If you choose direct debit, have your routing and account numbers ready.

- Submit and save your confirmation.

Which Plan Type Fits CP504 Situations

The IRS outlines common online eligibility guidelines:

- Short-term plan, you owe less than $100,000 in combined tax, penalties, and interest, and can pay within 180 days.

- Long-term plan, you owe $50,000 or less in combined tax, penalties, and interest, and have filed all required returns.

If you cannot apply online, the IRS also allows payment plan requests by submitting Form 9465 in many situations.

How To Appeal A CP504 (CAP)

CP504 is one of the notices where the IRS says you may request an appeal under the Collection Appeals Program (CAP) before collection action takes place, by following the instructions on your notice.

What CAP Is (Plain English)

CAP is a faster administrative appeal option for certain collection actions, but it is not the same as a Collection Due Process hearing. One key limitation is that you generally cannot go to court if you disagree with a CAP decision.

How To Request CAP

A common CAP workflow is:

- Ask for a conference with the IRS employee’s manager if you disagree with the collection decision.

- If unresolved, submit Form 9423 (Collection Appeals Request) to the address on the notice, within the timeframe shown.

CAP Vs CDP: Why This Matters

The CP504 sample notice itself explains that CAP is different from the Collection Due Process program.

In many cases, the stronger CDP hearing rights are tied to later “final notice” letters like LT11 or Letter 1058, not CP504, unless you have already received that separate notice.

What Happens If You Ignore CP504

The IRS states that if you do not pay or make payment arrangements, it can file a Notice of Federal Tax Lien.

The IRS also states it can seize your state tax refund and, if a balance remains, may later send a notice that gives you the right to a hearing before Appeals, then move forward with levying other property or rights to property.

This is why CP504 is a “do not delay” moment, it is often the last stage where simple actions, like a fast online payment plan, can prevent bigger enforcement steps.

When To Call A Professional

CP504 can still be handled directly in many cases, but professional IRS representation often makes sense when:

- You have multiple years involved, unfiled returns, or a large balance that will require financial documentation.

- You are close to deadlines and cannot risk a rejected plan or missed appeal window.

- You are worried about wage garnishment, a bank levy, or a lien filing and need fast intervention.

FAQs

Is CP504 A Final Notice Before A Levy

The IRS describes CP504 as your Notice of Intent to Levy and your final reminder that it intends to levy wages, bank accounts, or your state tax refund, and that it will begin searching for other assets to levy.

How Long Do I Have To Respond To CP504

Your notice shows the specific response deadline. The CP504 sample notice states that if the IRS does not receive payment arrangements or the amount due within 30 days from the date of the notice, it may levy property or rights to property.

Can I Set Up A Payment Plan After Receiving CP504

Yes. The IRS instructs taxpayers to set up a payment plan if they cannot pay the full amount owed, and it points them to the Online Payment Agreement tool as a quick option.

Can I Appeal A CP504 Notice

The IRS says you may request an appeal under the Collection Appeals Program (CAP) before collection action takes place by following the instructions on your notice.

Does CP504 Mean A Tax Lien Has Been Filed

Not always, but the IRS states it can file a Notice of Federal Tax Lien if it has not already done so.

Conclusion

A CP504 notice is a clear signal that your tax account is moving toward enforcement. The best outcomes usually come from doing the basics quickly, confirming the balance, picking a resolution path, and getting an approved arrangement in place before the IRS escalates to liens or levies.

Key Takeaways:

- CP504 is the IRS Notice of Intent to Levy, and it can involve wages, bank accounts, and your state tax refund.

- If you can pay in full, do it. If not, set up a payment plan immediately using the IRS Online Payment Agreement tool when eligible.

- If you disagree or you have already paid or arranged a plan, call the number on the notice and confirm your account status.

- If you need to challenge the collection action at this stage, CP504 points to the Collection Appeals Program (CAP), which is different from CDP.

- If your case is complex or you are worried about levy or lien escalation, professional IRS representation can help you move faster and avoid costly missteps.