If an IRS CP504B notice just landed on your desk, stop. Do not ignore it. Do not put it in a pile. This one is different.

The CP504B is not a gentle reminder. It is a Notice of Intent to Seize or Levy on Your Property, specifically issued to businesses. The IRS is telling you, in writing, that they are preparing to take action against your business assets unless you respond.

Here is what you actually need to know and what to do about it.

What Is a CP504B Notice?

The CP504B is an IRS notice sent specifically to businesses. It means you have an unpaid federal tax balance and the IRS has reached the point where they are authorized to seize your business property to collect it.

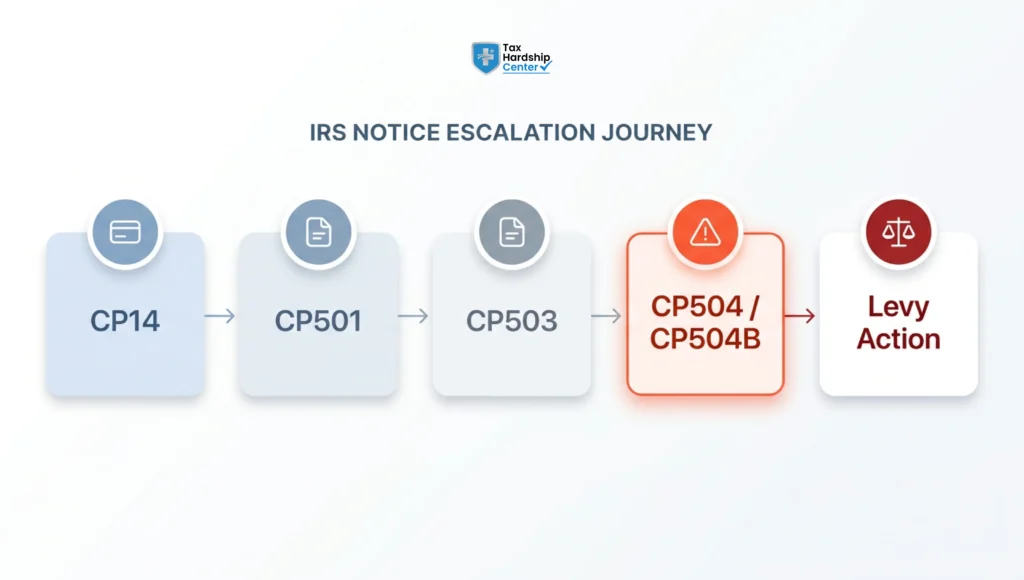

According to the IRS’s official CP504B notice page, this notice is sent after prior balance-due notices went unanswered. By the time CP504B arrives, the IRS has typically already sent:

- A CP14 (initial balance due)

- A CP501 (first reminder)

- A CP503 (second reminder)

- A CP504 or equivalent (final warning before CP504B)

So no, CP504B is not your first warning. It just might be your last chance before things get complicated fast.

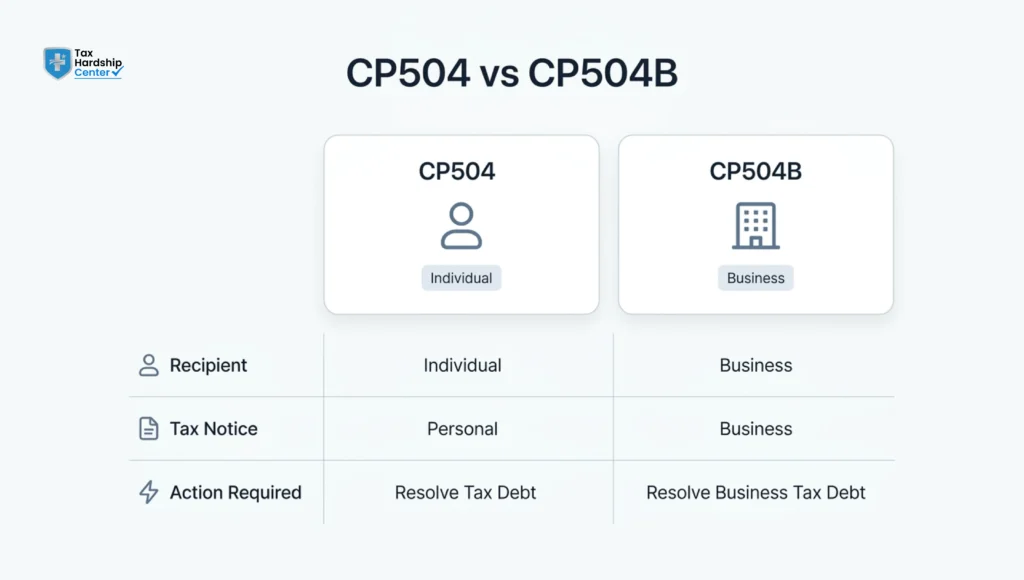

How Is CP504B Different From a Regular CP504?

This is a question people ask constantly, and it matters.

The CP504 is typically issued to individual taxpayers. The CP504B is issued to businesses. Same urgency, but the exposure is different. When you own a business, the IRS can reach your:

- Business bank accounts

- Accounts receivable

- Business assets and equipment

- State tax refunds owed to your business

Your business’s ability to operate, pay vendors, and run payroll can all be affected by what comes after a CP504B if it goes unaddressed.

If you have previously dealt with IRS notices around installment agreements or payment plans, know that the window for resolving this at the payment plan stage is still open when CP504B arrives. But it will not stay open long.

What the IRS Can Actually Seize

This is the part most people do not read carefully enough.

The IRS defines “property or rights to property” broadly. For businesses, that includes:

- Funds in your business checking or savings accounts

- Money owed to you by clients (they can instruct your clients to pay the IRS instead)

- Business equipment, vehicles, and physical assets

- Any state tax refund your business is owed

One thing the CP504B cannot do on its own: seize your wages or personal bank account. That requires a different notice process. But if the business is yours personally, and the IRS determines personal liability exists (especially in cases involving trust fund penalties or payroll tax debt), the situation can escalate to personal exposure quickly.

How Much Time Do You Have?

The CP504B gives you 30 days to respond before the IRS can move to enforce the levy.

Thirty days sounds like time. It is not.

Here is what needs to happen inside that window:

- Confirm the amount the IRS says you owe

- Identify if the balance is correct or if there is an error worth disputing

- Evaluate your resolution options (full payment, installment agreement, Offer in Compromise, Currently Not Collectible status)

- Make contact with the IRS or have a representative do so on your behalf

The IRS operates on its own timeline and getting a hold of the right person can take time. If you are doing this alone, thirty days evaporates quickly.

What Happens If You Ignore It

Straightforward answer: the IRS moves forward with the levy.

After 30 days with no response, the IRS can legally begin seizing your property. They do not need to go to court. They do not need your permission. And they do not have to give you additional warnings before taking funds from your business bank accounts.

Additionally, a federal tax lien may already be on file. Ignoring a CP504B does not make the lien go away. It typically makes it worse.

A tax lien affects your business credit, your ability to get bonding or financing, and how vendors and partners may perceive your business. Addressing it while you still have options is almost always better than waiting until enforcement starts.

For context on how IRS collection escalates after this stage, this IRS collection process overview explains the enforcement steps in plain language.

Your Response Options

Receiving CP504B does not mean you are out of options. Here is a realistic breakdown:

Pay in full. If you can, this closes the matter. You can pay online at IRS Direct Pay or by other accepted methods listed on your notice.

Set up an installment agreement. If full payment is not possible, an installment agreement lets you pay the balance over time. IRS Form 9465 is the standard request form. Businesses may have different qualifying criteria than individual taxpayers.

Request Currently Not Collectible (CNC) status. If your business genuinely cannot pay without shutting down operations, CNC status pauses IRS collection while you stabilize. It does not eliminate the debt, but it buys time.

Submit an Offer in Compromise. If you qualify, an Offer in Compromise allows you to settle for less than you owe. Most businesses do not qualify unless financial hardship is clearly documentable, but it is worth evaluating.

Dispute the balance. If you believe the IRS amount is incorrect, your first step is to respond in writing with supporting documentation. Do not let the 30-day window pass while you are gathering records.

Request a Collection Due Process (CDP) hearing. If a levy has been filed or is about to be executed, you have the right to request a CDP hearing using Form 12153. This can pause the levy action while you present your case.

Why Tax Hardship Center Is the Right Call for CP504B Cases

Business owners who receive a CP504B are not in the same position as someone who owes $5,000 in personal income tax. The stakes are different. The timelines are tighter. And choosing the wrong path can affect your employees, your vendors, and your ability to keep operating.

Tax Hardship Center works specifically with business owners dealing with IRS enforcement. Whether the issue is unpaid payroll taxes, business income tax debt, or a lien affecting your operations, the firm maps out a path to resolution that accounts for your cash flow, obligations, and timeline. Not a generic script. Your situation.

The services most relevant to a CP504B scenario include IRS levy relief, installment agreement setup, Offer in Compromise evaluation, and business tax debt resolution. Every case starts with a free consultation where you get a direct, honest read on your options before committing to anything.

If you are looking at a CP504B right now, do not wait out the 30 days trying to figure it out alone. Get a free case review with Tax Hardship Center and know where you stand.

FAQs

What is IRS notice CP504B?

CP504B is a Notice of Intent to Seize or Levy Your Property, issued specifically to businesses with unpaid federal tax balances. It means the IRS is prepared to take enforcement action unless you respond within 30 days.

How serious is a CP504B?

Very serious. It is one of the last notices the IRS sends before it moves to seize business property. Unlike earlier notices, CP504B carries real enforcement authority.

Is CP504 the final notice from the IRS?

CP504B is among the final warning notices, but it is not always the absolute last. After CP504B, the IRS can proceed to levy without additional advance notice in many cases. Do not treat it as another reminder.

What can the IRS seize after a CP504B?

For businesses, the IRS can seize funds in business bank accounts, accounts receivable (by redirecting your clients to pay them instead), business equipment, vehicles, and any state tax refunds owed to the business.

How do I respond to CP504B?

Your options include full payment, setting up an installment agreement, applying for an Offer in Compromise, requesting Currently Not Collectible status, or disputing the balance if you believe it is incorrect. A professional representative can help you choose the right path.

How do I pay IRS notice CP504B online?

You can pay online using IRS Direct Pay at irs.gov/payments. You will need your notice number and the tax period shown on the CP504B. Payment by check or money order using the payment voucher on the notice is also accepted.

What happens if I ignore a CP504B?

The IRS proceeds with a levy after the 30-day window closes. This means they can legally access your business bank accounts and redirect funds to satisfy the debt without any further notice.

Conclusion

A CP504B is serious. It is also something a lot of business owners go through when they respond quickly and make smart decisions about their options.

The IRS is not trying to put you out of business. They want to collect what they are owed. That means there are legitimate resolution paths available, from payment plans to levy releases to CNC status, and they work when you use them in time.

Act within the 30-day window. Know your options. And if you are not sure which path fits your situation, talk to someone who has seen it before.

Key Takeaways

- CP504B is a Notice of Intent to Seize or Levy, issued specifically to businesses with unpaid federal tax debt

- It comes after multiple earlier notices and signals that the IRS is ready to enforce collection

- You have 30 days from the notice date to respond before levy action can begin

- The IRS can seize business bank accounts, accounts receivable, equipment, and state refunds

- Ignoring CP504B does not make a tax lien go away; it typically makes it worse

- Response options include full payment, installment agreements, CNC status, Offer in Compromise, or a CDP hearing

- IRS Direct Pay at irs.gov is the fastest online payment option

- Not everyone qualifies for an Offer in Compromise; an honest evaluation is critical before pursuing this path

- A federal tax lien on file can impact your business credit and financing before the levy even executes

- Acting within the 30-day window dramatically improves your available options

Ready to understand your exact situation? Get a free case review with Tax Hardship Center and know your next step before the 30 days run out.