Catching up on three years of unfiled tax returns works best when you start fast and follow a clear sequence. You do not need to pay every Dollar on day one to file three clean tax returns. You can claim Income Tax Refunds that still fall within the three year window and you can set a payment plan for any taxes owed. The IRS can create a substitute return if you do nothing, which skips credits and inflates your Tax Liability. File accurate returns, match IRS transcripts, and use a plan that protects your cash. You improve Accuracy, preserve Max Refund amounts, and stop new IRS notices.

File past due tax returns now to stop penalties and claim refund credits

Filing now cuts failure to file penalties and slows new charges that grow every month. Each day you wait adds interest on unpaid taxes and raises the risk of a Tax lien, levy, or wage garnishment. You protect Social Security benefits and refund offsets when you file and pay or set a plan. You also control your filing status, dependents, deductions, and tax credit claims instead of the IRS doing it on your Behalf.

Start with a simple goal. Put three signed tax returns on file that match what the IRS sees on wage and income reports. You claim Refund Money only after you file the correct year. You also position yourself for penalty relief later because compliance matters for Eligibility. When you file, direct deposit Tax Refund Funds to a Savings Account for faster access and better control of Transactions. For a deeper primer, read our plain English guide to filing back taxes online.

What this means for credits, lenders, and your budget

Refunds and refundable credits such as Earned Income Credit and the additional Child Tax Credit require a timely filed return. Mortgage Lenders often ask for the last two or three filed returns during loan underwriting. File now so your Website banking portal shows cleared direct deposits and you can verify Availability of funds. Clean filings help with business Financing, rental applications, and professional licensing. You lower your Liability when your filings include all eligible deductions and credits for Maximum Savings Guaranteed in practice, not as a sales slogan.

Set up an installment agreement if you can’t pay the full tax debt

Many taxpayers file first and pay over time. An installment agreement lets you pay in set amounts while you keep current on future filings. You choose a short term plan if you can finish within months or a long term plan if you need a smaller monthly payment. You keep collection at bay when you pay on time and file new returns on time. Interest continues, but the failure to pay penalty rate can drop in a direct debit plan. For options and comparisons, see our understanding IRS payment plans explainer.

Short term payment plan and budgeting moves

Pick a short term payment plan if you can pay within about 180 days. No setup fee applies to most short term plans. Move funds from a Savings Account or apply a future refund to the balance. Use a simple Calculation to confirm you can cover living costs and the new payment. If cash stays tight, consider a lower long term payment instead of missing a due date.

Long term and partial pay installment agreements

A long term installment agreement spreads payments across many months. You can apply online and set automatic debits from a bank account. If your budget cannot ever cover the full Tax Liability before the collection statute ends, ask for a partial pay installment agreement. List your income, necessary expenses, and household size. The IRS looks at Eligibility Criteria and may approve a reduced payment that still fits your cash flow.

Currently not collectible status and smart timing

If you cannot afford any payment, request currently not collectible status. The IRS reviews your Documentation and may pause active collection when your budget shows no room for payments. Use this breathing room to rebuild savings, fix Bookkeeping, and update withholding so the next year does not add new debt. When income improves, switch to a small payment and keep the plan in good standing.

Our services at Tax Hardship Center: fast filings and payment plan setup

Our services at Tax Hardship Center make a three year catch up doable without guesswork. We prepare each year on the correct forms, match IRS transcripts, and set direct deposit so your Max Refund lands in your Savings Account. When taxes are owed, we help you apply for an installment agreement that fits your budget and stops most collection actions. If you qualify for a settlement, we prepare the paperwork for an Offer in Compromise to reduce Liability. If a levy or paycheck issue already started, our wage garnishment team works to lift it while we file your missing returns.

At Tax Hardship Center, we help you resolve back taxes with tailored strategies for individuals and small businesses. If you run payroll or owe employment taxes, our payroll tax relief service addresses Business Taxes and trust fund exposure while you get current on filings. For broader cases, our national IRS tax relief program pairs Bookkeeping and Accounting review with filing support for Maximum Savings. You get clear options, Audit Support level documentation, and a plan that balances speed and Savings.

Match IRS wage and income reports before you file returns

The IRS already holds copies of your W 2, 1099, and 1098 forms. Pull wage and income transcripts for each unfiled year before you prepare any tax return. Match every item to your records so you avoid mismatch letters. Confirm withholding, retirement distributions, mortgage interest, and health insurance forms such as 1095 A. This step improves Accuracy and lowers the chance of extra notices. Use the IRS Get Transcript tool to download what the IRS sees.

Use transcripts to fill gaps and confirm withholding

Transcripts list wages, interest, dividends, brokerage sales, retirement payouts, and more. They also show withholding totals and some state tax data. Use that data to reconcile income and payments across your tax returns and to protect your Max Refund. If a payer made an error, ask for a corrected form and keep proof. Clean matching keeps your account quiet after you file.

Refunds expire for unfiled returns after three years

Refunds do not sit forever. You have three years from the original due date to claim a refund on an unfiled return. The same timing applies to many refundable credits. If you miss the window, the IRS keeps the money and you cannot revive it with an appeal. File the refund year first and include direct deposit info for speed. The IRS explains this policy on its page about filing past due tax returns.

How to check if a refund still exists

Review withholding and estimated payments for each year. If those payments exceed tax, you likely qualify for a refund. Check the calendar for the three year mark from the original due date. If the deadline approaches, file that year now and track the refund status online on the IRS Website once processing starts.

Do I need to file all three unfiled returns right now?

File all required returns as fast as you can, but stage the work to hit the right deadlines. Start with the year that still offers a refund or the year that reduces penalties the most. Meet any date in an IRS notice first to avoid a levy. You can submit all three returns together if you finish them at the same time. Many filers send the refund year first and the balance due years a few days later.

Why staging helps cash flow and focus

Staging lets you use a refund from one year to lower a balance on another. It also spreads document hunting and review. Use a simple spreadsheet or Accounting software to track what remains for each year. Update the list as you receive missing forms and finish each return.

How the IRS treats unfiled taxes and substitute returns (SFRs)

If you do not file, the IRS can prepare a substitute return based only on third party forms. An SFR usually assumes single filing status, no dependents, and no credits. That choice inflates your Tax Liability and can trigger liens and levies. File your own return to replace the SFR and to claim the right status, dependents, and credits. For context on notices and enforcement actions, review our IRS collection process overview.

Replace SFRs fast and protect credits

An SFR can block refunds and raise your balance. File your own return even if collection already started. The IRS will process your return and adjust the account. You keep far more control over outcomes when your return sits on file instead of an SFR.

When criminal charges apply versus civil penalties and interest

Most late filers face civil penalties and interest, not criminal cases. Criminal risk rises when someone willfully hides income or files false returns. If your facts involve fake documents or repeated lies, you should get professional help before you file. If life events caused the delay, file now, pay what you can, and request penalty relief. The IRS wants accurate returns and current compliance.

Real world signals that raise the stakes

Badges of fraud include fake IDs, false Social Security numbers, and staged Documentation. Honest mistakes, missing forms, and cash flow issues usually resolve through filings and agreements. Respond to every notice and keep a log of calls and letters.

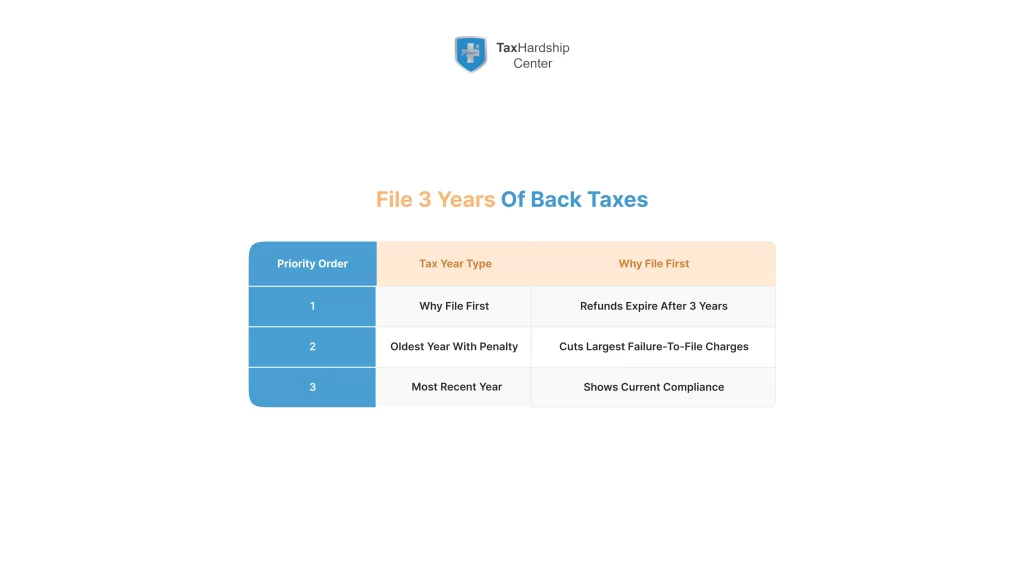

Which tax years to prioritize first when filing taxes late

Start with any year that still allows a refund. Then file the oldest year that carries the largest failure to file penalty. Next, file the most recent year to show current compliance. If a notice sets a firm date for a specific year, file that year first. This order protects expiring refunds, cuts cumulative penalties, and shows good faith.

A simple priority matrix

Create a matrix with columns for refund, expected balance, notice deadlines, and collection risk. Rank the years and follow the order. This system adds clarity, keeps your plan on track, and supports Maximum Savings.

How late can you file and how to confirm missed deadlines

Three clocks matter. You have three years to claim a refund on an unfiled return. The IRS has three years to assess more tax for most filed returns, longer if large underreporting occurs. The IRS has up to ten years to collect an assessed tax balance. Confirm missed deadlines by reviewing original due dates, extensions, and your account transcripts.

Use transcripts and notices to verify your timeline

Order account transcripts for each year. Look for posted returns, assessments, and SFR entries. Compare those entries to your records. If a refund deadline nears, file that year first. If the collection statute on an old balance nears its end, still file new years on time to avoid fresh issues.

Immediate steps if you haven’t filed taxes in 3 years

Set a one week plan to gather records. Pull wage and income transcripts, W 2s, 1099s, and 1098s. List any missing forms and request replacements. Confirm your filing status and dependents for each year. Decide whether you will use a Tax Filing Service, Desktop Software, or a Bookkeeping Service with tax prep.

Keep momentum and cut new notices

Respond to any IRS letter before the date on the notice. You can call and ask for a short hold while you finish your returns. Keep notes from each call and mail certified copies when you send paper returns. Save scans of everything for future reference.

Gathering necessary documents and paperwork

Accurate returns start with complete Documentation. Build a checklist for each year that covers W 2s, 1099 NEC, 1099 MISC, 1099 INT, 1099 DIV, 1099 R, 1098, and 1095 A. Add brokerage statements, K 1s, and state forms. Pull bank statements and receipts if you claim itemized deductions or run a business.

W 2s, 1099s, 1098s, and other tax forms you will need

W 2s report wages and withholding. 1099 NEC reports Self Employment Income. 1099 MISC covers rents, royalties, and other income. 1099 INT and 1099 DIV cover interest and dividends. 1099 R reports retirement distributions. 1098 reports mortgage interest. 1095 A connects to the Premium Tax Credit. If you lack copies, the IRS lists transcript types and how to order them.

Records for deductions, credits, and dependents

Track childcare, tuition, student loan interest, charitable gifts, and medical costs. Keep birth certificates and Social Security cards for dependents. For a Rental Property, keep ledgers for Rental Income and expenses such as repairs, property taxes, and mortgage interest. Keep mileage logs and receipts if you run a business.

Where to request transcripts, returns, and copies

Use Get Transcript online to pull wage and income transcripts and account transcripts. If you cannot verify identity online, file Form 4506 T for transcripts by mail. Use Form 4506 to order a full copy of a prior return when a lender or a court requires it. Transcripts cover most needs for filing back tax returns.

What you need to file your back tax returns

You must use the correct forms for each year. Prior year 1040 forms and schedules change from year to year. Prior year instructions show different standard deduction amounts and credit rules. Use prior year tax software or hire a tax professional who prepares each year on the right forms. This protects Accuracy and reduces math error notices.

E file versus mail for older filings and amended returns

You can e file some prior year returns if the IRS still supports e file for those years. Older years require paper filing by mail. Amended returns with Form 1040 X allow e file for many recent years. If you mail a return, use certified mail and keep the receipt. Attach W 2 and 1099 copies and include any required schedules.

How do I file 3 years of taxes step by step

Treat each year as its own project. Open the correct prior year software and start a new return. Enter every income item from your transcripts and documents. Choose the right filing status and dependents for that year. Claim credits such as the Earned Income Credit and the Child Tax Credit when you qualify. Review the summary, verify withholding and estimated payments, and file.

Self employment, rentals, and special incomes

Report Self Employment Income on the Schedule C Tax Form. Keep clean ledgers in QuickBooks or another Accounting tool so your numbers tie to bank Transactions. For a Rental Property, report Rental Income and expenses on Schedule E. Include Unemployment Income from Form 1099 G when it applies. Clean records help you reach Maximum Savings without audit headaches.

Prepare, review, and submit each year correctly

Run a final error check in the software. Confirm bank account and routing numbers for direct deposit or debit. Print a copy for your files even when you e file. If you mail a return, include a check or money order only if it fits your budget. Write the year and your Social Security number on the check and keep a scan.

Payment options if you can’t pay taxes owed

You have choices after you file. Pick a short term plan if you can clear the balance within months. Pick a long term installment agreement if you need a smaller, steady payment. If your budget cannot handle any payment, request currently not collectible status. If the numbers show you cannot pay in full before the collection statute ends, ask for a partial pay installment agreement. To compare structures, read our IRS repayment program overview.

How interest and penalties change once a plan starts

Interest continues until you pay in full. The failure to pay penalty rate can shrink in a direct debit plan. Filing all returns stops the failure to file penalty on those periods. Keep current with new tax filings and estimates to avoid plan default. If you prefer to apply directly, the IRS hosts an online payment agreement application.

Paying with credit, loans, or other Financing

You can pay by card, but processing fees add cost. A credit union loan can beat card rates if you need Financing. Weigh all costs against the IRS plan. Do not drain retirement accounts to pay unless you understand taxes and penalties on withdrawals.

Penalty relief when you file taxes late

You can request penalty relief when you show a clean history or a valid reason. First time penalty abatement can remove certain penalties for one year if you stayed compliant for the three prior years. Reasonable cause relief applies when events outside your control prevented timely filing or payment. Interest usually remains, but you still save real money when penalties drop. Learn tactics in our post on penalty abatement strategies.

First time penalty abatement and reasonable cause

Check your compliance over the last three years. If you meet that standard, request first time penalty abatement by phone or in writing. If not, prepare a reasonable cause statement with facts, dates, and actions you took to fix the problem. Medical events, disasters, theft, or reliance on wrong professional advice can support relief. Keep documents that prove your claims.

Fixing errors on late filings

Mistakes happen under pressure. You can amend a filed return with Form 1040 X. Use it to fix filing status, add a dependent, correct direct deposit info, or claim a missed credit. If the change produces an extra refund, file before the refund statute expires. If the change increases tax, submit payment or fold it into your installment plan.

Prevent repeat errors next year

Create a yearly tax folder, set reminders for key dates, and update W 4 withholding or estimated taxes. Keep clean Bookkeeping and reconcile accounts monthly. Consider a Bookkeeping Service if you need help with ledgers, payroll, and sales tax.

Special cases when you file taxes late

Some situations need extra steps. If you run a business, track Business Taxes with accurate Accounting so your return ties to books. Self employed filers must calculate self employment tax and may need to pay quarterly estimates. If you sat in bankruptcy for part of a year, check with your attorney before you file. Identity theft can block e file, so you may need an Identity Protection PIN. Military service in a combat zone and federally declared disasters can extend deadlines for filing and payment. State income tax rules can differ from federal rules, including refund timelines.

Desktop tools and workpapers that help

You can prepare returns with Desktop Software or an online platform. Some filers prefer QuickBooks Desktop for Desktop Projects, job costing, and clean year end reports. Others prefer QuickBooks Online and a cloud backup. Use what keeps your ledgers accurate. Export clean trial balances and workpapers for your tax pro.

What happens if you don’t file taxes

Nonfilers face escalating actions. The IRS can send CP letters, file an SFR, assess tax, and add penalties and interest. If you still do not file, the IRS can file liens, send levies to your bank account, or garnish wages. Large unresolved balances can trigger passport restrictions. You avoid these outcomes when you file and choose a payment path that you can keep. For garnishment math and thresholds, review our wage garnishment calculation guide.

Why the IRS files an SFR and why to replace it

The IRS files an SFR to secure an assessment based on what it sees from payers. That return assumes no credits and often overstates tax. You can fix the account by filing your own return that claims the right status, dependents, and credits. This reduces the assessed balance and can remove a lien or stop a levy request.

Work with a tax professional or use tax software

Tax software can handle many three year catch up cases. You can use a Tax Filing Service if you prefer help with forms and math. A tax professional adds value when you face missing records, SFRs, self employed activity, rentals, or audit risk. Ask about experience with unfiled returns, transcript analysis, and IRS payment plans. Get pricing in writing and review scope, timelines, and support.

What to expect from software and services

Software tiers such as Deluxe often include features like import, error checks, and Audit Support. Some brands advertise a Refund Guarantee, Audit Support Guarantee, or Audit Defense. Read the fine print. These offers do not replace clean records and accurate filings. No provider can Guarantee Business Returns or promise Tax Savings Guaranteed or Maximum Savings Guaranteed for every case. You raise the odds of a Max Refund when you keep solid records and follow the rules.

Bookkeeping and Accounting support that pays off

Clean ledgers drive clean filings. Use QuickBooks, spreadsheets, or another ledger to track income and expenses. Reconcile bank and credit card accounts so your Transactions tie to statements. If you need help, hire a Bookkeeping Service for monthly cleanup. Accurate books support lower risk and better results if the IRS questions a return.

Checklist: File three years of back taxes without setbacks

Use this checklist to keep your plan on track. Work year by year so you do not miss a form or a credit. Keep copies of everything and track each mailing or e file receipt. Mark dates for follow up on refunds, transcripts, and notices. Update your withholding so you do not repeat the cycle next year.

Documents, forms, and deadlines

- Gather W 2s, 1099s, 1098s, brokerage statements, and 1095 A if you used Marketplace coverage.

- Pull wage and income transcripts and account transcripts for all three years.

- Confirm filing status and dependents for each year.

- Download prior year 1040 forms and instructions or open prior year tax software.

- Check refund deadlines and file refund years first.

Filing steps and follow up

- Prepare each year separately on the correct forms, including Schedule C for Self Employment Income and Schedule E for rentals.

- Review withholding, estimated payments, and tax credits before you file.

- E file supported years and mail older years by certified mail with attachments.

- Set up an installment agreement if you cannot pay in full and choose autopay from a Savings Account.

- Track refund status, save receipts, and store all filed tax returns and Documentation securely.

How Tax Hardship Center helps you file three years

At Tax Hardship Center, we help you file three years of unfiled tax returns with a calm, documented process. We analyze transcripts, verify Eligibility, and prepare each year for Accuracy so your filings support a Max Refund or the lowest lawful Liability. For balances, we set a right sized installment agreement, evaluate Offer in Compromise potential, and move fast to resolve an IRS tax levy or garnishment. If you own a company, we address payroll taxes while we complete personal filings, so Mortgage Lenders and agencies receive complete, timely returns.

You receive clear takeaways, phone and email updates, and a single point of contact. We prepare appeal letters, organize Documentation for Audit Support, and keep you current on new filings so penalties stop. Our plan respects your budget, protects Savings Account balances, and aims for durable savings rather than quick fixes.

In summary…

A clear plan turns three years of unfiled returns into a fix you can finish. File the refund year first, match transcripts, and choose a payment plan that fits your budget. Replace any SFRs with accurate returns and request penalty relief when you qualify. Keep ledgers clean so next year takes less work and yields better results.

- File now to stop new penalties and protect refund credits

- Filing ends the failure to file penalty and starts resolution.

- Refunds on unfiled returns expire after three years.

- Filing ends the failure to file penalty and starts resolution.

- Confirm what the IRS sees before you file

- Pull wage and income transcripts for each year and match every item.

- Fix mismatches before you file to avoid extra notices.

- Pull wage and income transcripts for each year and match every item.

- Choose a payment option that fits your budget

- Short term plan, long term plan, partial pay, or currently not collectible.

- Interest continues, but penalties can drop in a plan.

- Short term plan, long term plan, partial pay, or currently not collectible.

- Use penalty relief where you qualify

- First time penalty abatement or reasonable cause relief can save money.

- Keep dated records to support your request.

- First time penalty abatement or reasonable cause relief can save money.

- Keep records and prevent repeats

- Reconcile accounts monthly and update withholding or estimates.

- Use software or a Bookkeeping Service so your numbers stay accurate.

- Reconcile accounts monthly and update withholding or estimates.

These Takeaways keep you focused and productive. You can do this on your own with solid tools or with help from a pro who files unfiled returns every day. If you want a calmer road, Tax Hardship Center can prepare each year, pursue relief, and set a payment plan that matches your cash flow.

FAQs

How do I file 3 years of taxes at once without errors?

Prepare each year on its own set of forms in prior year tax software. Pull wage and income transcripts and match every W 2 and 1099 to avoid notices. Confirm filing status and dependents for each year and review credits like the Earned Income Credit and Child Tax Credit. Run an error check and print a copy for your records. E file supported years and mail the others by certified mail.

Can I still claim a refund for an old tax year?

Yes if you file within three years of that year’s original due date. Refundable credits follow the same window. If you miss it, the refund expires. File refund years first and include direct deposit details. Move any refund to a Savings Account to protect it for bills or for a payment plan.

What if I can’t pay the taxes owed right now?

File anyway. Then pick a payment plan that fits your budget. Choose a short term plan if you can clear the balance soon. Choose a long term installment agreement or request currently not collectible status if money stays tight. Ask for penalty relief such as first time penalty abatement or reasonable cause to cut costs.

Will unfiled taxes affect my Social Security benefits?

Unpaid federal taxes can lead to offsets that reduce certain federal payments. File and set a plan to limit future collection actions. If you already receive notices about offsets, move fast. File missing returns, set a plan, and keep new filings current to protect benefits.

Can I face criminal charges for not filing tax returns?

Most late filers do not face criminal charges. The IRS reserves criminal cases for willful evasion and fraud. If you worry about exposure, speak with a qualified tax professional before you file.