Introduction

Tax relief functions as a structured pathway for resolving federal tax debt when financial strain or IRS enforcement pressure prevents timely payment. The concept covers a wide range of actions the IRS may take, from adjusting penalties to settling qualified debts. The process depends on an interconnected set of entities: IRS collections procedures, taxpayer financial conditions, compliance history, documented hardship, and the specific relief programs available under federal guidelines.

IRS systems are designed to assess both willingness and ability to pay. When filings are overdue, balances remain unpaid, or income and expenses fall into a pattern signaling hardship, the IRS escalates collection actions. These steps, such as notices, liens, or wage garnishments, reveal the agency’s assessment of risk and collectability. Each IRS reaction reflects a predicate that indicates the taxpayer’s position in the collection life cycle.

Financial hardship also plays a central role. If household income fails to cover essential living costs under the IRS National Standards, or if circumstances such as medical events or employment changes disrupt financial stability, these indicators often point toward potential eligibility for relief. Programs such as installment agreements, penalty reduction, settlement options, and temporary collection suspension rely heavily on documentation that accurately depicts financial constraints and asset equity.

The concept of tax relief becomes especially relevant when taxpayers confront signals suggesting that standard payment expectations no longer align with real financial conditions. These signals do not appear in isolation. They connect directly to IRS evaluation methods, enforcement patterns, and the specific pathway a case may follow through collections, appeals, or structured programs. Services offered by organizations like Tax Hardship Center are often valuable at these turning points, especially when IRS communication, documentation requirements, or financial calculations become complex.

A clear understanding of how tax relief operates, why IRS actions escalate, and what circumstances often lead to eligibility for relief helps clarify when specialized assistance may be beneficial.

Key Takeaways

- IRS tax relief refers to structured programs that reduce, restructure, or temporarily suspend federal tax obligations.

- IRS notices, balance escalation, and enforcement actions reveal the agency’s internal assessment of collectability.

- Financial hardship indicators, such as rising expenses or income loss, often serve as early signals of eligibility for relief.

- Asset equity, disposable income, and filing compliance influence the outcome of IRS relief evaluations.

- Professional representation may be valuable when documentation becomes complex or enforcement becomes more stringent.

Core Concepts Behind Tax Relief and IRS Financial Hardship Resolution

Definition of Tax Relief as an IRS Entity Action

Tax relief refers to actions the IRS may take to adjust, reduce, settle, or temporarily pause federal tax balances under specific conditions. These actions depend on financial analysis, compliance status, and the IRS determination of reasonable collection potential. Tax relief does not function as a single program but rather a collection of pathways tailored to different financial situations.

Typical forms of relief include structured payment plans, settlements for less than the full balance, temporary collection suspensions, and penalty reductions. Each option corresponds to a distinct IRS evaluation process that examines assets, income, expenses, and long-term repayment capacity. Penalties and interest may continue to accrue in specific programs, and settlement options require strict financial substantiation.

IRS Role in Determining Eligibility

The IRS evaluates tax relief eligibility through a standardized financial review. This review examines:

- Income and its consistency across recent periods

- National Standard allowances for food, housing, transportation, and out-of-pocket costs

- Bank account balances and immediate cash flow

- Vehicle equity, home equity, and retirement account accessibility

- Monthly disposable income and projected repayment ability

These elements combine into a model that helps determine whether a taxpayer qualifies for long-term payment restructuring, temporary suspension of collection activity, or settlement through an Offer in Compromise. The IRS also considers compliance factors. Missing tax returns, inaccurate reporting, or significant gaps in documentation can slow or block relief approval.

Common Triggers Leading to the Need for Tax Relief

The need for relief typically arises when tax balances exceed the taxpayer’s ability to make timely payments. Certain conditions signal that relief may be appropriate:

- Accumulating back taxes as penalties and interest increases the total balance

- IRS notices intensifying from initial reminders to levy warnings

- Ongoing financial strain that prevents payment of current and past-due taxes

- Long-term income instability or unexpected hardship events

- Difficulty meeting basic living costs under IRS National Standards

A clear understanding of these developments helps identify when intervention becomes necessary and which program may align with the taxpayer’s financial profile.

Key Signs Tax Relief May Be Needed Based on IRS Behavior and Taxpayer Circumstances

IRS Letters and Notices Signaling Escalating Enforcement

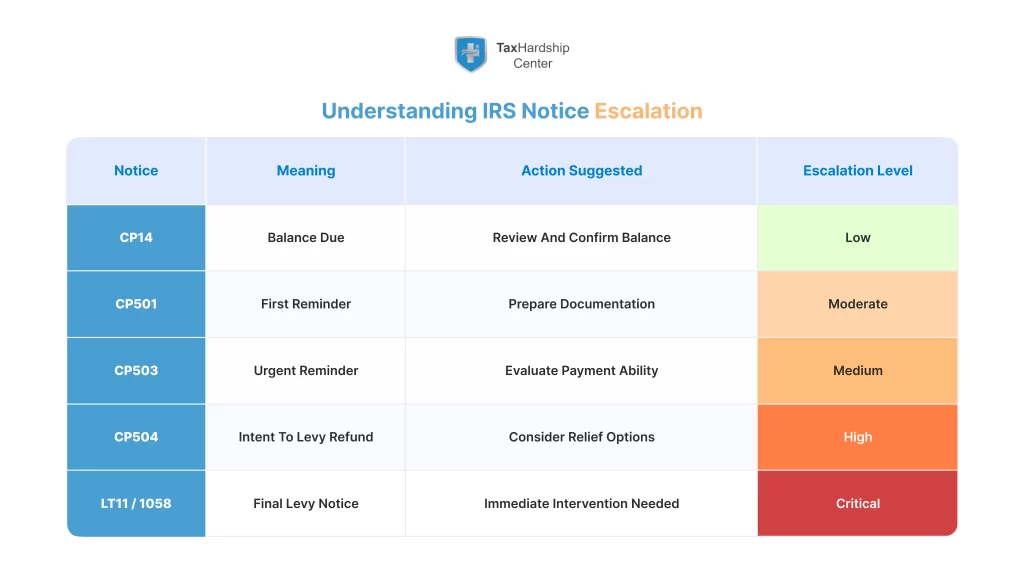

IRS notices form a sequential pattern that reveals how the collections system interprets a taxpayer’s level of risk and responsiveness. The earliest notices, such as CP14, indicate that a balance has been assessed and remains unpaid. As reminders progress to CP501 and CP503, the IRS signals increasing urgency. These notices show that the account remains unresolved and that the agency expects immediate attention.

The transition to CP504 marks a pivotal shift. CP504 warns of the intent to levy state refunds and indicates that enforcement actions may proceed if no response is received. LT11 or Letter 1058 represents an even more serious stage. These letters notify taxpayers of the IRS’s legal right to levy wages, bank accounts, or other property. They also outline appeal rights under the Collections Due Process framework.

This escalation reflects the IRS’s move from standard communication to active enforcement. The sequence shows how the IRS evaluates collectability, compliance, and responsiveness. When notices reach advanced stages, tax relief often becomes necessary to halt or prevent levies, reduce the balance, or establish a manageable payment structure.

Structured Notice Progression Table:

| IRS Notice | Meaning | Implication for Relief Need |

| CP14 | Initial balance due reminder | Early indication of unresolved tax liability |

| CP501 | First reminder after no response | IRS signaling persistent delinquency |

| CP503 | Urgent reminder | Greater risk of enforcement activity |

| CP504 | Intent to levy state refund | Strong indicator that relief or action is required |

| LT11 / Letter 1058 | Final levy notice with appeal rights | Immediate need for structured tax relief intervention |

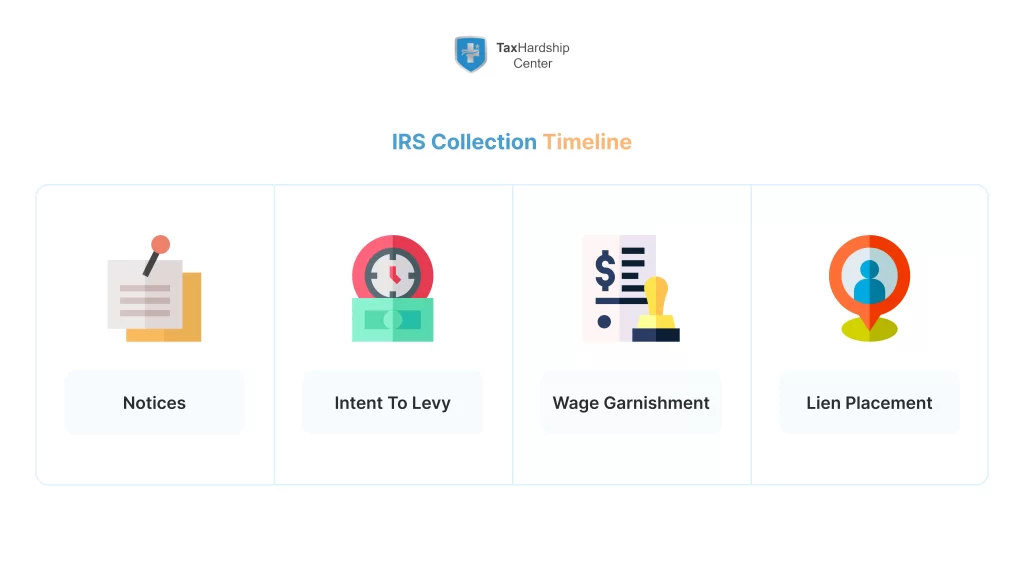

Wage Garnishment, Bank Levies, and Property Liens

Enforcement actions occur when IRS systems determine that prior notices have not produced payment or communication. Wage garnishment reduces disposable income by directing a portion of earnings to the IRS. This step signals that the agency has already completed a series of warnings and decided that forced collection is necessary.

Bank levies remove funds directly from financial accounts. This action can disrupt essential expenses and create immediate financial strain. Property liens function differently. A lien does not seize property but secures the government’s interest in assets. Liens may hinder access to credit, property sales, and refinancing. Lingering liens typically indicate a long-standing balance that has progressed beyond routine notice cycles.

Each enforcement action increases the likelihood that structured tax relief is needed. Programs such as installment agreements, Offers in Compromise, or Currently Not Collectible status can reduce or pause these actions, but eligibility depends on timely financial documentation and compliance.

Inability to Pay Current Taxes or Past-Due Balances

Financial strain is a primary indicator that tax relief may be appropriate. The IRS evaluates income relative to essential living costs. If monthly household expenses fall within or below the National Standards yet still leave insufficient funds to cover tax obligations, the situation often fits the framework for relief.

In addition, rising interest and penalties may push a manageable balance into an unmanageable one. Taxpayers who cannot realistically reduce the balance within a reasonable period, or who struggle to remain current on new taxes while addressing old ones, frequently qualify for structured programs.

Changes in Life Circumstances Affecting Tax Payment Ability

Certain events significantly alter financial stability and influence relief eligibility:

- Job loss or reduction in working hours

- Medical conditions requiring substantial out-of-pocket expenses

- Natural disasters impacting income or property

- Changes in household size or dependent care costs

- Marital transitions that alter filing status or financial obligations

The IRS considers documented life changes when assessing reasonable collection potential. Sudden financial disruptions may qualify for a temporary suspension of collection, reduced settlement terms, or a structured payment plan.

Compliance Issues and Unfiled Tax Returns

Unfiled returns prevent the IRS from calculating an accurate balance and can delay or block access to relief programs. Missing filings may trigger substitute returns prepared by the IRS, which often reflect higher tax liabilities due to a lack of deductions or credits. Consistent filing lapses also suggest noncompliance, which decreases the likelihood of approval for settlement or hardship status.

Filing all required returns typically becomes a prerequisite for program consideration. Once compliance is restored, relief pathways such as installment agreements or Offers in Compromise become accessible.

Types of IRS Tax Relief Programs and the Conditions for Each

Offer in Compromise (Debt Settlement)

An Offer in Compromise allows the IRS to settle a tax debt for less than the total balance when repayment would create financial hardship or when collection is unlikely within the statutory period. Approval depends on the IRS calculation of reasonable collection potential, which examines equity in assets, bank account balances, monthly disposable income, and projected ability to pay over time.

The IRS uses a structured financial model to determine whether an offer aligns with the agency’s expectations. If assets show minimal equity and household income barely meets necessary living costs under National Standards, the IRS may view a reduced settlement as appropriate. Complexities arise when property equity exists but is not easily accessible, requiring additional documentation. Medical hardships, unstable earnings, or recent life disruptions can also influence the assessment.

Key Components Evaluated in an Offer in Compromise

- Quick-sale value of real estate or vehicles

- Retirement account accessibility and penalties

- Bank account averages based on 1–3 months of statements

- Monthly disposable income is calculated after allowable expenses

- Future income projections based on employment patterns

When financial documentation demonstrates low collection potential, the IRS may accept a settlement proposal. Rejection often occurs when expenses exceed allowable limits, when income remains steady enough to support payments, or when asset equity contradicts hardship claims.

Installment Agreements (Structured Payments)

Installment agreements offer a structured way to pay tax debt over time. The IRS examines the balance owed, the taxpayer’s income patterns, and remaining collection statute timeframes. Several types exist:

Categories of Installment Agreements

- Regular installment agreements for balances requiring full-payment plans

- Streamlined agreements that allow approval without extensive financial documentation

- Partial-payment agreements that reduce monthly obligations when income is limited

These agreements depend on consistent monthly payments and ongoing compliance with filing obligations. If disposable income supports a predictable payment schedule, the IRS often views this route as the most suitable approach.

Currently Not Collectible Status (Temporary Hardship)

Currently Not Collectible status provides temporary relief when financial conditions prevent any payment. The IRS suspends collection actions after verifying that income does not exceed necessary living expenses. During this period, levies stop and wages cannot be garnished, although penalties and interest may continue to accrue.

This status often applies when households face medical burdens, job loss, or long-term instability. It is not permanent and requires periodic IRS reviews.

Penalty Abatement

Penalty abatement reduces or eliminates penalties for late filing, late payment, or failure to deposit. The IRS may consider a first-time abatement for taxpayers with clean histories. In contrast, reasonable cause abatement requires evidence of circumstances such as medical emergencies, disasters, or significant disruptions that prevented compliance. Supporting documentation plays a central role in the approval process.

IRS Fresh Start Program

The IRS Fresh Start initiative expands access to settlement and payment options. It adjusts thresholds for streamlined installment agreements, makes lien withdrawal more accessible in certain conditions, and simplifies eligibility for settlement pathways. This framework supports taxpayers with moderate but manageable financial constraints.

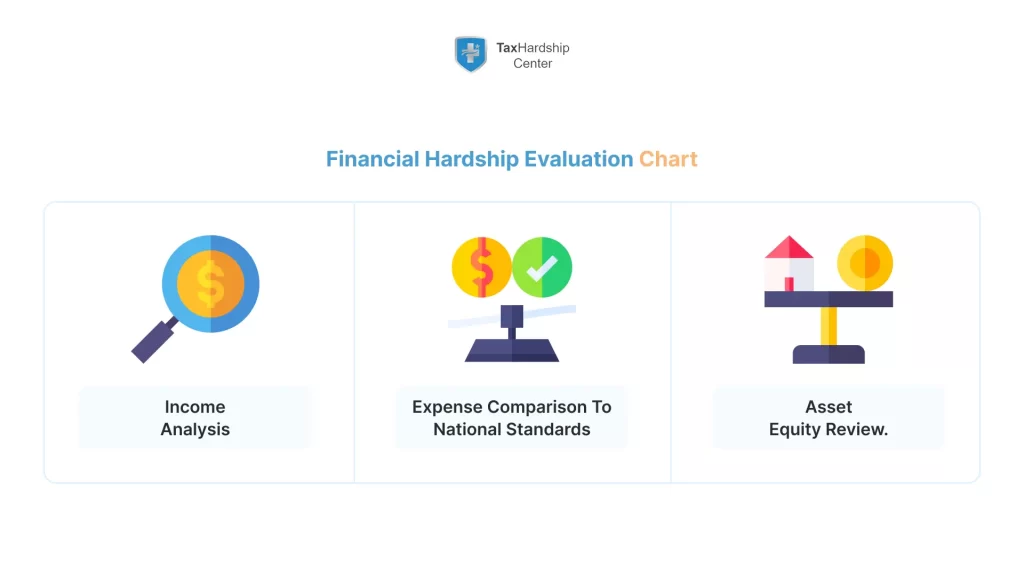

How IRS Evaluates Taxpayer Hardship and Relief Requests

The IRS Financial Analysis Framework

The IRS uses a standardized financial model to evaluate relief requests. This analytical structure compares actual household expenses with national and local standards that reflect typical living costs nationwide. These standards influence how the IRS interprets affordability and help determine whether a taxpayer qualifies for settlement, payment restructuring, or temporary hardship status.

Key factors include:

- Total household income and consistency of earnings

- Out-of-pocket medical costs within allowable limits

- Housing and utility expenses relative to local standards

- Vehicle operation and ownership costs

- Bank balances and cash flow

- Equity in property, vehicles, or liquid assets

The IRS uses these inputs to calculate disposable income. If disposable income remains negative or minimal, hardship-based relief becomes more likely.

How IRS Considers Risk, Compliance, and Collection Probability

Relief evaluations extend beyond financial numbers. The IRS considers several behavioral indicators:

- Filing consistency across previous years

- Accuracy of income reporting

- Recent attempt to resolve obligations

- Response patterns to IRS notices

These factors help the agency determine whether a structured arrangement or settlement is feasible. The IRS also considers future collection probability, which evaluates long-term earning potential, employment stability, and available assets.

When the IRS Rejects Relief Requests and Why

Rejection occurs when financial submissions fail to align with IRS expectations. Frequent reasons include:

- Inflated or unallowable expenses exceeding National Standards

- Omitted income sources

- Asset valuations that do not reflect market reality

- Lack of documentation supporting medical or financial hardship

- Missing tax returns or inconsistent filing histories

In such cases, the IRS may propose alternative arrangements, request additional documentation, or maintain collection actions until compliance conditions are met.

How to Get Tax Relief Through Proper Documentation and IRS Communication

Required Forms and Evidence for Hardship or Settlement

Effective tax relief requests require documentation that accurately reflects financial hardship. The IRS typically uses forms such as Form 433-A for wage earners and Form 433-F for general financial disclosure. Offers in Compromise require Form 656 alongside detailed financial attachments.

Common documentation includes:

- Pay stubs and income summaries

- Bank statements reflecting average balances

- Mortgage and rent records

- Vehicle loan statements

- Utility bills

- Medical invoices

- Retirement account statements

- Proof of extraordinary expenses

The IRS evaluates these records to confirm accuracy and to assess whether financial constraints justify relief.

Common Filing and Documentation Errors

Mistakes often delay relief or trigger rejection. Typical errors include:

- Underreporting income due to inconsistent documentation

- Overstating expenses beyond allowable limits

- Failure to list assets or provide accurate equity information

- Missing signatures or incomplete forms

- Submitting outdated or missing tax returns

Correcting these issues usually requires resubmission with full supporting evidence.

Role of Professional Representation in Obtaining Tax Relief

When Assistance from IRS-Authorized Practitioners Becomes Beneficial

Professional representation often becomes important once IRS notices escalate or when complex financial details shape the outcome of a tax relief request. IRS-authorized practitioners, such as enrolled agents or tax attorneys, understand procedural requirements and the specific documentation standards that influence IRS decision-making. Their involvement is most beneficial when cases include multiple years of unfiled returns, substantial balances, or asset valuation challenges that impact eligibility for settlement or hardship status.

Practitioners assist in organizing financial disclosures, ensuring that income and expense calculations align with National Standards, and preparing responses to IRS inquiries. Their role becomes critical during situations involving wage garnishment, pending levies, lien disputes, or disagreements over settlement offers. By managing communication and presenting a cohesive financial narrative, these professionals help reduce errors that can lead to rejection or further enforcement.

Cases involving medical hardships, variable income, dissolved businesses, payroll tax liabilities, or prior compliance complications often require detailed financial explanations. Experienced representatives analyze how each factor affects collection potential, then structure submissions that align with IRS expectations while accurately portraying financial strain.

How Tax Hardship Center Supports IRS Tax Relief Cases

Tax Hardship Center assists taxpayers by evaluating their financial conditions, identifying viable relief options, and preparing documentation that accurately reflects hardship or settlement eligibility. The organization reviews income consistency, asset equity, allowable expenses, and prior compliance patterns before recommending an appropriate strategy.

Its specialists handle communications with the IRS, including requests for additional information and responses to notices. They prepare detailed financial analyses for installment agreements, Offers in Compromise, Currently Not Collectible status, and penalty abatement requests. For cases involving advanced enforcement, such as wage garnishment or bank levies, the organization seeks temporary relief while determining a long-term resolution.

By aligning financial disclosures with IRS standards and presenting organized documentation, Tax Hardship Center helps ensure that relief requests meet procedural requirements and reflect the taxpayer’s actual financial condition.

Questions Frequently Asked About How to Get Tax Relief

What factors influence the IRS decision on tax relief eligibility?

Eligibility depends on several interconnected factors, including household income, allowable expenses, asset equity, filing status, and accuracy of submitted documentation. The IRS evaluates whether a taxpayer can reasonably satisfy the balance within the remaining statute period. Consistent filing and reliable income reporting also influence the agency’s assessment of risk and future collectability.

How IRS verify financial hardship details?

Verification is conducted by reviewing bank statements, pay stubs, utility bills, mortgage records, and medical invoices. The IRS compares these documents with National Standards to determine the credibility of hardship claims. Any discrepancies, such as expenses exceeding permitted limits or missing records, may prompt further inquiry.

What happens if IRS notices are ignored?

Ignoring notices typically results in enforcement. Early reminders escalate to formal levy warnings, then to wage garnishment, bank levies, and property liens. Advanced enforcement can significantly disrupt financial stability, making structured relief or professional representation essential for regaining control.

Can tax relief be approved for medical or emergencies?

Medical conditions or emergency events often strengthen hardship claims when supported by evidence. High medical expenses, temporary loss of income, or long-term treatments may justify suspending collection or reducing settlement terms. The IRS requires documentation such as medical invoices, hospital records, and proof of income changes to evaluate the situation.

How tax relief interact with tax liens or levies?

Tax relief programs can pause or reduce enforcement depending on eligibility. Installment agreements may limit new enforcement activity, while settlement proposals often require the IRS to delay specific actions during evaluation. Currently Not Collectible status stops levies altogether, though liens may remain as security. Lien withdrawal may be possible after entering qualifying payment arrangements.

Conclusion

Tax relief provides a structured way for the IRS to resolve tax debt when financial strain or enforcement pressure make payment unrealistic. Each step in the process reflects how the IRS evaluates income, expenses, asset equity, compliance history, and the likelihood of collecting the balance. As notices progress from simple reminders to levy warnings, these signals indicate when a case is moving toward enforcement and when tax relief becomes necessary.

Financial hardship remains the core factor. Situations involving medical costs, reduced income, or essential living expenses that exceed household resources often match the criteria for settlement or temporary suspension of collection. The IRS relies on documented evidence and national standards to confirm whether these circumstances justify relief.

Programs such as installment agreements, Offers in Compromise, Currently Not Collectible status, and penalty abatement each address different financial profiles. Their success depends on accurate documentation and consistent filing behavior. When details become complex or enforcement has already begun, professional assistance can help clarify eligibility and guide communication with the IRS.

Recognizing early warning signs, understanding IRS expectations, and preparing detailed financial records provide a clear path toward resolving tax debt. When economic pressure and IRS actions converge, tax relief offers a structured route toward stability and long-term resolution.