|Caring for a spouse, living on fixed income, or dealing with health issues can push taxes to the back burner. Seniors ask the same core questions: Can the IRS forgive penalties and interest, can Social Security be garnished, and which form gets me relief the fastest. You can qualify for penalty relief or even a settlement if you show a solid history, a valid reason, or a true inability to pay. The IRS rarely forgives the tax, but it can remove penalties, reduce balances through an Offer in Compromise, or pause collections. Know your income, assets, and medical costs before you choose a path.

Eligibility and Quick Answers for Seniors

This section explains who qualifies for relief, how age matters, and which options work best when you live on retirement income.

Seniors qualify for the same IRS relief programs as everyone else, but age often strengthens your case when fixed income and medical costs limit ability to pay. The IRS looks at your filing history, your reason for falling behind, and your current financials. Penalties can get removed through First-Time Abatement or Reasonable Cause. Balances can get reduced through an Offer in Compromise if your income and assets cannot cover the tax in a reasonable time. Collections can pause under Currently Not Collectible when basic living costs leave no room for payments.

Fast answers

- Can the IRS take Social Security: The IRS can levy up to 15% of certain benefits, but not Supplemental Security Income.

- Can the IRS forgive interest: Interest almost never gets removed unless the IRS caused an unreasonable delay.

- Does age alone qualify you: No, but age-related health limits and fixed income can support Reasonable Cause, OIC, or CNC.

- Will a payment plan stop penalties: It stops new failure-to-pay penalties from growing as fast and stops most collection actions.

Tax Hardship Center: Senior-focused help when relief cannot wait

This section explains how our team pairs senior needs with the right IRS program and gets the paperwork right the first time.

Our services at Tax Hardship Center start with a transcript review and a budget that respects retirement costs. We set up Installment Agreements that fit fixed income, pursue Penalty Abatement when a clean record or valid reason applies, and prepare Offers in Compromise when income and assets fall short. If you have unfiled years, we help you catch up fast through our Unfiled Tax Returns service so relief can move forward. At Tax Hardship Center, we help you protect Social Security and pensions while we resolve the debt with the simplest path that works.

First-Time Penalty Abatement (FTA): When a Clean Record Helps

This section shows how a solid past filing record can remove penalties for one tax period.

First-Time Abatement removes failure-to-file and failure-to-pay penalties for one year if you kept a clean compliance record. You need no penalties in the prior three years and you must have filed all required returns or filed an extension for the year in question. FTA works best for a single slip caused by a move, surgery, caregiver duties, or a one-off oversight. Interest on penalties drops when the penalty goes away, which lowers the total balance. See the IRS rules on penalty relief and consider professional help for a targeted request or use our Penalty Abatement service.

When FTA makes sense

- You filed on time for the prior three years.

- You have one late year with otherwise clean history.

- You can pay or set a plan once penalties come off.

- You want a quick, low-paperwork fix.

Reasonable Cause Penalty Relief: Prove Why You Fell Behind

This section explains how to show facts and documents that justify penalty removal beyond FTA.

Reasonable Cause relief fits seniors who missed deadlines due to death in the family, serious illness, natural disaster, or reliance on incorrect professional advice. The IRS wants a timeline that shows when the issue started, what you did to comply, and how you fixed it once you could. Support your claim with hospital records, prescriptions, obituaries, insurance claims, or letters from caregivers. Write a short statement that connects your facts to the missed filing or payment date. For background, review the IRS page on penalty relief and, if needed, ask us to draft a request through our Penalty Abatement service.

What to include in your statement

- Dates, names, and plain facts that show what happened.

- Proof of hospitalization or medical orders that limited your actions.

- Evidence of mail disruptions or disaster claims.

- Steps you took to file or pay as soon as you could.

Installment Agreements: Spread Payments Without Breaking Retirement

This section covers payment plans that stop most collections while you clear the debt over time.

An installment agreement lets you pay monthly and keep the IRS from levying most assets while you stay current. Seniors often use a streamlined plan when balances fall under set thresholds and returns are filed. Pick a payment that survives after housing, utilities, food, insurance, and medical costs. Direct debit plans reduce default risk and can lower setup fees in some cases. Read the IRS guide to payment plans and compare options with our Installment Agreement service. For more detail, see our blog on the Streamlined Installment Agreement.

Types of payment plans

- Short-term payment plan when you can pay within 180 days.

- Streamlined plan for balances under set limits with simple approval.

- Partial-pay plan when your budget supports only a smaller monthly amount.

- Direct debit plan to avoid missed payments and mail delays.

Offer in Compromise (OIC): Settle for Less Than You Owe

This section outlines when a settlement works and how the IRS values income and assets for seniors.

An Offer in Compromise can settle your tax for less when you cannot pay the full amount before the collection statute ends. The IRS measures what it could collect from your monthly disposable income and from assets like savings, home equity, vehicles, and nonretirement investments. Seniors on fixed income with high medical costs often show low disposable income, which helps. Retirement accounts count as assets, but early withdrawal penalties and taxes reduce their value in the analysis. Learn the IRS rules for an Offer in Compromise and review our service page for Offers in Compromise. For deeper context, read our blog on OIC eligibility.

OIC success tips

- List all medical premiums, copays, prescriptions, and caregiving costs.

- Document pension, Social Security, and retirement account distributions.

- Include proof of housing, utilities, and insurance costs.

- Do not offer more than your reasonable collection potential.

Currently Not Collectible (CNC): Pause Collections When Income Falls Short

This section explains how to qualify for a pause in collections when basic expenses leave no room to pay.

Currently Not Collectible status stops active collection while your finances do not support payments. You will complete a financial statement that shows income and necessary living costs. The IRS may file a Notice of Federal Tax Lien, but active levies should stop once CNC begins. The IRS can review your case later to see if income improved. Seniors use CNC during recovery from surgery, after a spouse passes, or when rent and prescriptions consume most income. To understand CNC in plain terms, read our guide to IRS hardship.

How to strengthen a CNC request

- Use current bank statements to prove income and spending.

- Include lease, utility, and insurance bills.

- Show medical invoices and pharmacy printouts.

- Update the IRS if income drops again.

Social Security, Pensions, and IRS Collections: What Seniors Must Know

This section clarifies how the IRS treats government benefits and retirement income during collections.

The IRS can levy up to 15% of certain Social Security benefits through the Federal Payment Levy Program, but it cannot levy Supplemental Security Income. Private pensions and annuities can face levy after due process notices, while qualified retirement accounts require special steps. Required minimum distributions still count as income, which affects OIC and CNC math. Medicare premiums, Medigap plans, and long-term care costs can reduce disposable income when verified. Keep benefits letters and 1099s ready for any relief request.

For levy rules and payment options, see the IRS pages on getting help with tax debt and payment plans.

Quick guardrails

- SSI stays off limits to IRS levies.

- Social Security retirement benefits can face up to a 15% levy.

- RMDs count as income in ability-to-pay reviews.

- Verified medical and insurance costs can reduce the amount you must pay.

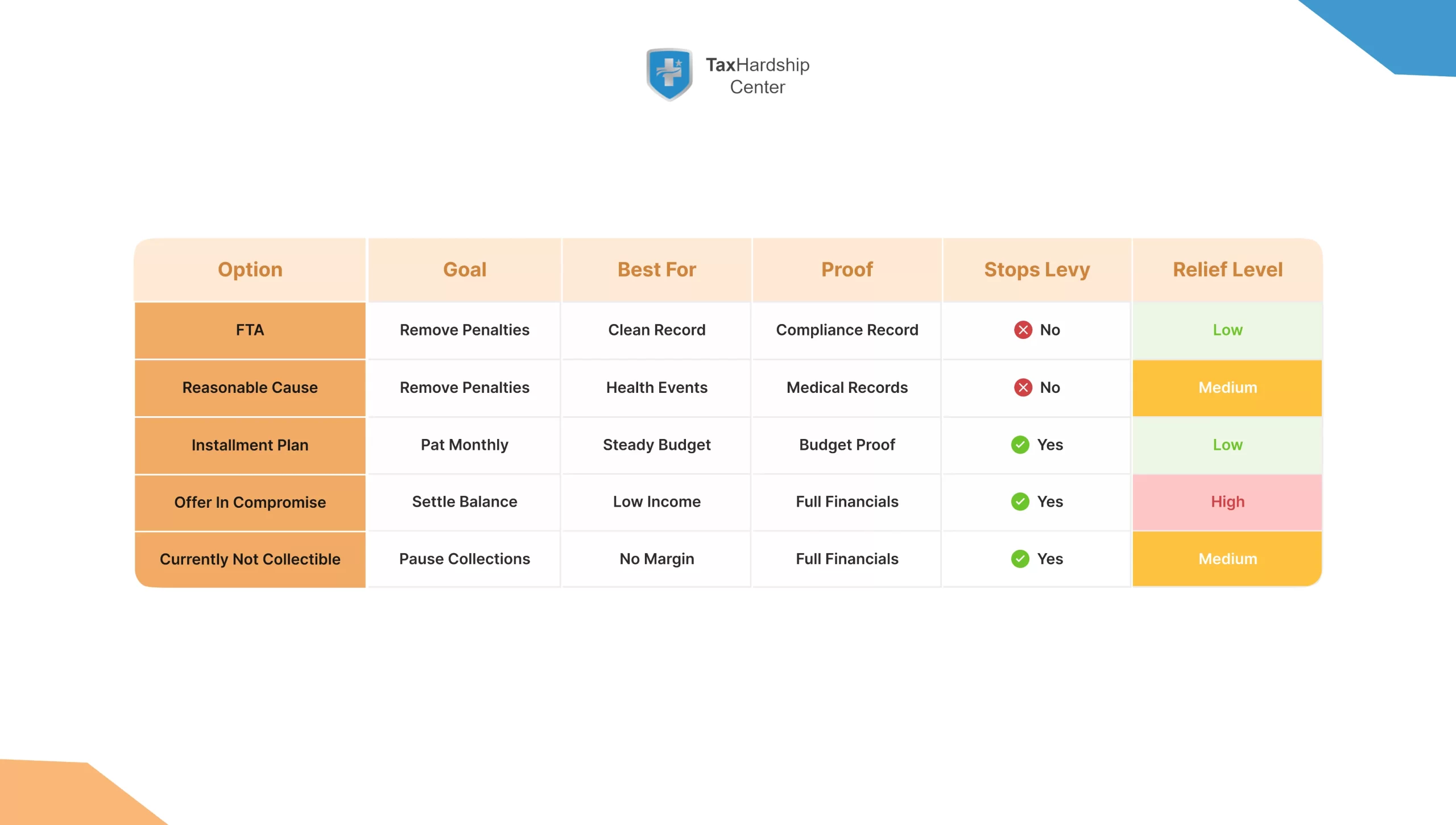

Picking the Right Path: Simple Decision Rules for Seniors

This section gives a clear way to match your situation to the best relief option.

Use these rules to choose fast. Pick First-Time Abatement if you have one late year and three clean years before it. Choose Reasonable Cause if health events or disasters explain the miss and you can prove it. Select an installment agreement if you can make a steady payment without cutting essentials. Consider an OIC if your income and assets cannot cover the tax before collection time runs out. Ask for CNC if basic expenses eat your budget and payment plans still fail.

One-page chooser

- Clean record and one slip: Try FTA.

- Documented hardship or disaster: Try Reasonable Cause.

- Stable budget with room to pay: Pick an installment plan.

- Low income and few assets: Explore OIC.

- No margin after essentials: Request CNC.

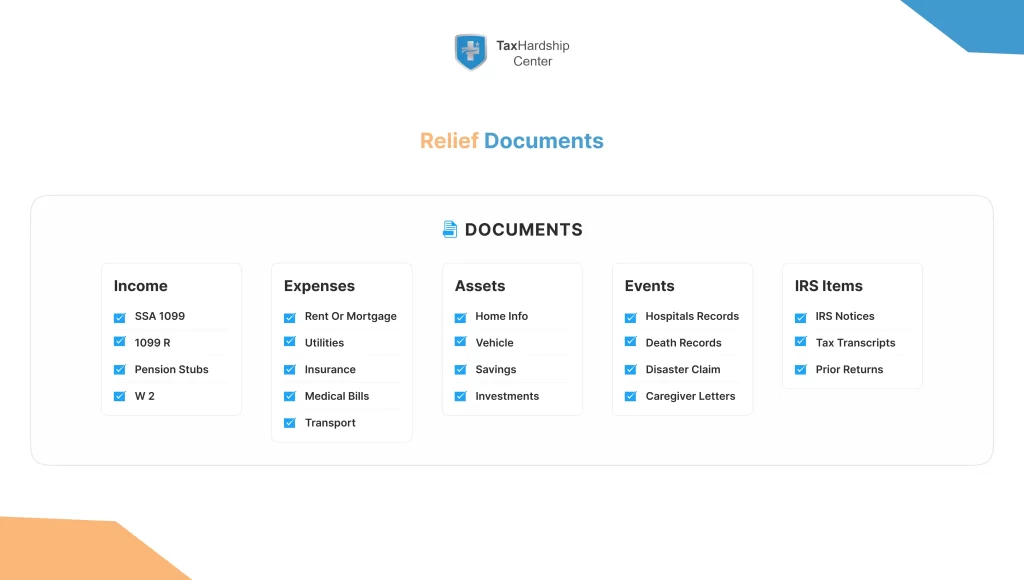

Documents to Gather Before You Apply

This section lists what to collect so the IRS can verify your story and numbers.

Pull the paperwork first to avoid delays. Gather the last three months of bank statements, current benefits letters, and medical bills. Add a lease or mortgage statement, utility bills, insurance premiums, and property tax statements. Include proof of income such as Social Security 1099s, pension 1099-Rs, and any W-2s or 1099-NECs. Keep copies of prior IRS notices and any disaster or hospital records that support penalty relief. If years are missing, use our Unfiled Tax Returns service so relief options like OIC or payment plans do not stall.

Organization checklist

- Income: SSA-1099, 1099-R, pension stubs, any part-time W-2s.

- Expenses: rent or mortgage, utilities, insurance, medical, and transportation.

- Assets: home info, vehicles, savings, and nonretirement investments.

- Events: hospital records, death certificates, disaster claims, or letters from caregivers.

How Tax Hardship Center Supports Seniors

This section describes how our team helps you pick the right path, prepare forms, and deal with the IRS.

At Tax Hardship Center, we review your IRS transcripts, confirm balances and deadlines, and map a relief plan that fits your budget. We prepare FTA or Reasonable Cause requests with the right documents and a tight statement. We build installment plans that survive real retirement costs and adjust them if income changes. We assemble Offer in Compromise packets with a realistic number that reflects your true ability to pay. We request CNC when expenses leave no room so collections pause while you recover. To get started, request a free consultation or go straight to our Offer in Compromise and Installment Agreement service pages.

In summary, here are the key takeaways

This section recaps the main points so you can act with confidence and avoid missteps.

- Who qualifies

- Seniors qualify for the same relief programs, but fixed income and medical costs can strengthen the case.

- Clean history supports First-Time Abatement for one year of penalties.

- Seniors qualify for the same relief programs, but fixed income and medical costs can strengthen the case.

- Your main options

- Reasonable Cause removes penalties when you prove why you missed deadlines.

- Installment agreements keep collections at bay while you pay monthly.

- Offers in Compromise settle for less when income and assets fall short.

- Currently Not Collectible pauses collections when basic costs consume income.

- Reasonable Cause removes penalties when you prove why you missed deadlines.

- How to choose

- One late year with a clean record: FTA.

- Documented hardship: Reasonable Cause.

- Budget room to pay: Installment plan.

- Low income and limited assets: OIC.

- No margin after essentials: CNC.

- One late year with a clean record: FTA.

- What to prepare

- Bank statements, benefits letters, medical bills, housing and utility costs, and IRS notices.

- Bank statements, benefits letters, medical bills, housing and utility costs, and IRS notices.

Move quickly, keep records, and match your situation to the option that protects your fixed income. A focused plan reduces stress and saves money.

FAQs

This section answers common questions seniors ask about tax forgiveness and collections.

Does the IRS offer special forgiveness just for seniors?

No. Seniors use the same programs as everyone else, but fixed income and health costs can strengthen OIC, CNC, or Reasonable Cause cases.

Can the IRS take my Social Security check?

The IRS can levy up to 15% of certain Social Security benefits, but it cannot levy SSI. A payment plan, CNC, or OIC can stop or prevent a levy.

Will the IRS remove interest on my tax debt?

Interest rarely gets removed unless the IRS caused an unreasonable delay. Penalty relief still cuts total interest because penalty interest drops when the penalty goes away.

Is an Offer in Compromise realistic if I own a home?

Yes, but equity counts. The IRS looks at quick-sale value minus any loans, and then compares that value to your income and expenses.

How long does relief take?

FTA can take days to weeks. Reasonable Cause can take weeks to a few months. OICs and CNC reviews often take several months, so send complete documents early.