Many taxpayers ask: “how can I reduce my taxes owed without drawing IRS heat?” The fastest wins hide in plain sight. Adjust taxable income, claim every legal credit, and time income so it lands in lighter brackets. Pair airtight records with proven strategies, and you will shrink the bill while staying on the IRS’s good side. The ideas below work whether you collect wages, run a side hustle, or manage a small portfolio.

Understand Your Tax Bracket and Income Shifting

Federal tax brackets work like shelves, not walls. Each layer of income fills brackets from the bottom up, so you often pay several rates on one paycheck. When you know the upper edge of your current bracket, you gain a clear map. Delay a year‑end commission, push a freelance invoice into January, or transfer dividend stocks to a spouse in a lower bracket. These moves shift dollars out of higher shelves and into lower ones.

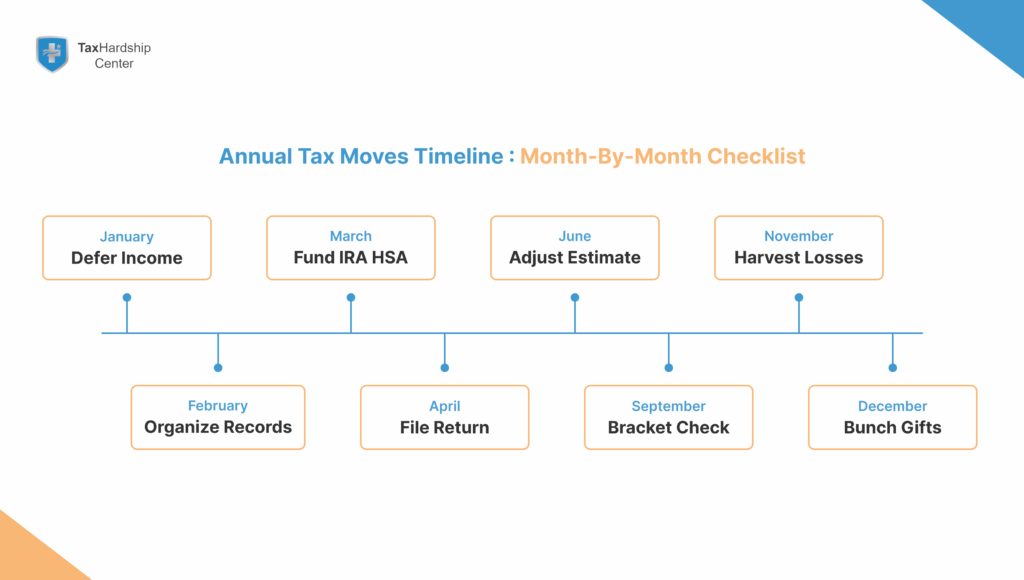

Run bracket projections in the fall. Add up wages, side gigs, capital gains, and retirement withdrawals. Subtract planned above‑the‑line deductions. You will see how far your last dollar reaches into the next bracket. If you sit two thousand dollars below the cutoff, delay income and avoid a four‑point jump. If you face a lighter income year, pull revenue forward and fill the empty lower brackets.

Couples filing jointly can hire a teen child in the family business, pay a fair wage, and move that pay into the child’s zero or ten‑percent bracket. The business deducts the wage, the child owes minimal tax, and the family saves as a unit. The child can even deposit earnings into a Roth IRA, planting decades of tax‑free growth.

Maximize Above the Line Deductions

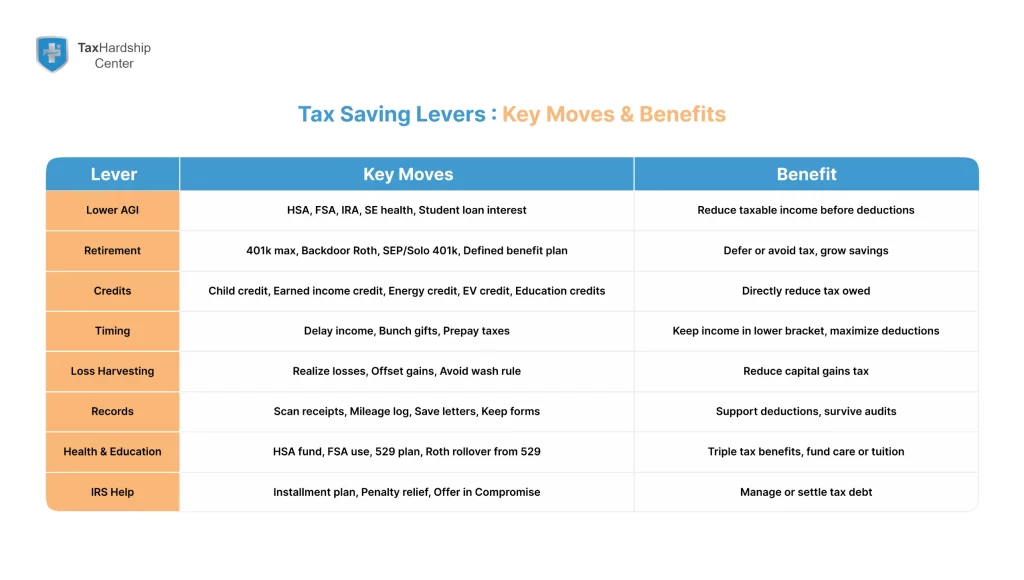

Above‑the‑line deductions slash adjusted gross income before it meets the standard or itemized deduction. HSAs, traditional IRA contributions, self‑employed health insurance, student loan interest, and educator expenses headline the list.

A Health Savings Account lets a family with a high‑deductible plan stash more than eight thousand dollars in 2025. The contribution is deductible, growth compounds tax deferred, and withdrawals for qualified care exit tax free. Publication 969 spells out the current limits and rules. (irs.gov) If your employer funnels dollars by payroll deduction you dodge FICA tax as well.

Self‑employed professionals can open a solo 401k. Combine elective deferrals with a profit‑sharing contribution and bank as much as sixty‑three thousand dollars. Add the deduction for half of self‑employment tax and your AGI drops fast. By lowering AGI you may qualify for Tax Hardship Center’s Installment Agreement assistance should cash flow tighten later.

Leverage Tax Credits to Offset Liability

Credits beat deductions because they reduce tax dollar for dollar. The child tax credit cuts up to two thousand dollars per qualifying child, while the earned income tax credit refunds much more for moderate earners. The IRS lists income limits and rules for the EITC on its official page. (irs.gov) Parents can layer the American Opportunity and Lifetime Learning credits during college years.

Homeowners enjoy a thirty‑percent residential clean‑energy credit on solar panels and heat pumps. Drivers who switch to a qualifying electric vehicle earn up to seventy‑five hundred dollars back. If a balance remains, Tax Hardship Center’s Offer in Compromise service can negotiate a settlement while you stay current on future returns.

To protect your lien position, review our blog on steps to handle an IRS tax lien. It walks through payoff timing so credits are not lost to enforced collection.

Optimize Retirement Contributions

Retirement accounts provide a current deduction plus future growth. Workers under fifty can defer up to twenty thousand dollars into a 401k in 2025, with a six‑thousand‑five‑hundred‑dollar catch‑up for those fifty and older. Traditional IRA contributions add seven thousand more.

High earners who lose the IRA deduction can still execute a backdoor Roth. Contribute after‑tax dollars to a non‑deductible IRA, then convert. The move locks in tax‑free growth and guards against future rate hikes without raising today’s bracket.

Self‑employed taxpayers should explore a SEP IRA or solo 401k. Up to twenty‑five percent of net earnings can hide from the IRS until retirement, often when your bracket runs lower. A defined‑benefit plan can push limits even higher for professionals with steady profits.

Use Tax Advantaged Accounts for Health and Education

Medical bills and tuition dent any budget. HSAs offer the only triple‑tax advantage in the code. Contributions escape income tax, growth defers, and withdrawals for qualified care leave the account tax free. Treat an HSA like a stealth retirement account by investing unused balances.

Flexible Spending Accounts also lower taxable pay, though funds expire if unused past the grace period. Parents shave income with 529 plans. Many states grant a state tax deduction for contributions, and federal law allows tax‑free withdrawals for qualified education costs. The plan now permits a limited Roth IRA rollover after fifteen years, giving savers another tax‑free bucket.

Strategically Harvest Capital Losses

Market swings hurt, but losses can help lower taxes. Sell a position below cost, lock the loss, and use it to erase gains on winners. If losses exceed gains you can apply up to three thousand dollars against ordinary income each year and carry the balance forward.

The wash‑sale rule blocks you from buying the same security within thirty days. Swap a large‑cap index fund for a similar but not identical fund or rotate among tech stocks to keep exposure without losing the deduction. For deeper guidance check our blog on choosing the right IRS payment plan so gains and losses align with cash‑flow needs.

Charitable investors can donate appreciated stock, avoid capital gains, and still harvest losses elsewhere. Combined with timing moves in the next section, you can zero out tax on investment income even in a volatile year.

Time Income and Expenses Like a Pro

Small timing moves produce big savings. Pay property taxes, January mortgage interest, and lump charitable gifts in December when your bracket runs high. Use a donor‑advised fund to bunch two years of gifts into one deduction while spreading support to charities later.

On the income side delay what you can. Ask a client to mail the check on January second or hold a capital‑gain sale until the new year. Deferring income may keep you under phaseouts for valuable credits. If you expect a low‑income year, reverse the tactic by accelerating revenue and waiting on deductions.

Business owners who still owe after timing moves often turn to our Penalty Abatement service to wipe late fees before they grow.

Keep Clean Records and Proof

Audit fear should never stop you from claiming deductions. Scan each receipt and store digital copies in date‑stamped folders. Reconcile statements monthly. For mileage, use a GPS app that exports spreadsheets; estimates fail IRS scrutiny.

Save written acknowledgments for charitable gifts over two hundred fifty dollars and payroll stubs that show retirement and HSA contributions. Solid proof turns an audit into routine correspondence and supports filings should you later apply for Tax Hardship Center’s Tax Debt Forgiveness program.

When the IRS Comes Calling, Get Help from Tax Hardship Center

A certified letter rattles any taxpayer. Open the notice, note the deadline, and read the code. Most letters request clarification or payment within thirty days. Call early in the morning to cut hold time and write the agent’s badge number.

If you agree with the balance but cannot pay, arrange an installment plan through our Installment Agreement assistance. If the balance looks inflated, pursue an Offer in Compromise. If penalties drive the total, start with Penalty Abatement before interest multiplies the damage.

At Tax Hardship Center, we help you choose the right path and handle the paperwork so you avoid liens, levies, and sleepless nights.

In summary…

In summary, smart planning, airtight records, and timely action can shave thousands from your tax bill. Follow the playbook below:

- Map your marginal bracket and shift income when rates change.

- Max out above‑the‑line deductions and stack eligible credits.

- Fund retirement and HSA accounts early.

- Harvest losses and bunch expenses to match income swings.

- Keep bulletproof documentation for every claim.

- Lean on Tax Hardship Center for payment plans, penalty relief, or settlement options when the IRS presses hard.

Start with the highest‑impact tactic on the list, automate records, and review your plan each fall. If you hit a roadblock, call our team for a free consultation and keep more of what you earn.

FAQs

Q. How can I reduce my taxes owed if I am self‑employed?

A. Increase your SEP IRA or solo 401k contribution, deduct health insurance premiums, and track every legitimate business expense such as home office, mileage, and software.

Q. Does itemizing still make sense after the higher standard deduction?

A. Itemizing matters when your combined mortgage interest, state and local taxes, charitable gifts, and medical bills exceed the standard deduction, or when itemizing hooks credits limited by AGI.

Q. What is the income limit for the child tax credit in 2025?

A. The full $2,000 credit phases out at $200,000 for single filers and $400,000 for joint filers.

Q. Can capital loss carryovers expire?

A. No. Unused net capital losses roll forward indefinitely until you use them against future gains or ordinary income.

Q. Will contributing to a Roth IRA reduce my current tax bill?

A. A Roth IRA