Property tax forgiveness programs help seniors cut annual bills, freeze assessed values, or defer payment until a home sells. Age thresholds usually start at 62, 65, or the state’s defined retirement age. Most programs require that the home is a primary residence and that total household income stays under a set limit. Many states also cap the home’s assessed value for eligibility and exclude large assets. You can often combine a senior exemption with a homestead exemption or a circuit breaker credit to reduce taxes even more.

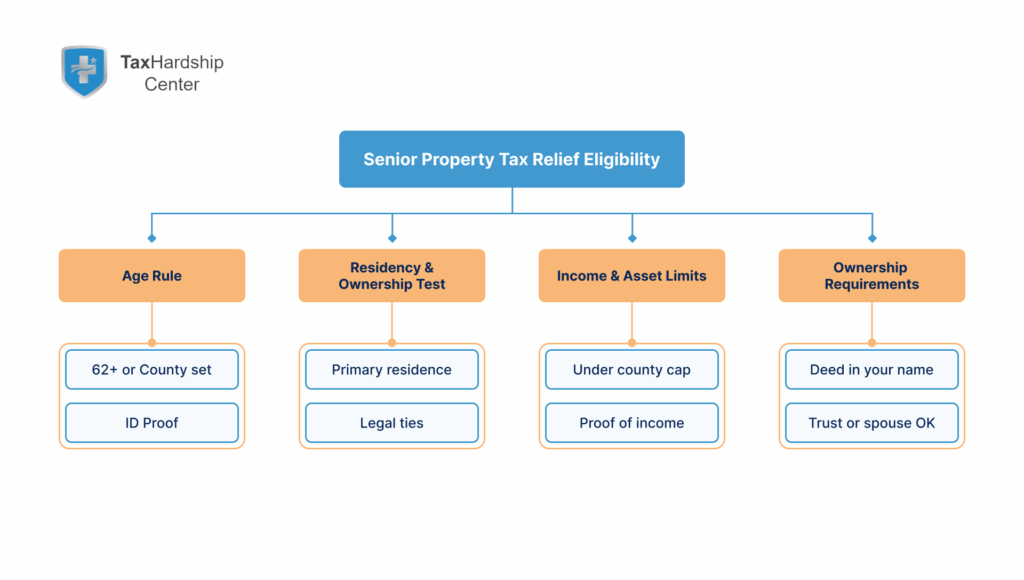

Eligibility Rules Seniors Should Check First

Start by confirming the baseline rules, since every state and county sets its own age, income, and residency criteria. Most senior programs require you to own and live in the home as your primary residence for a full year, keep your driver’s license or voter registration at that address, and meet an age threshold that ranges from 62 to 70 in some localities. Income limits often count all household earners, not just the senior, and can include Social Security, pensions, dividends, and IRA withdrawals depending on the jurisdiction. Programs also look at assessed value or total assets, which can disqualify homes that exceed a local cap even when income fits the limit. Read the fine print on renewals, since many exemptions need you to recertify each year, and missing that window can cause the full tax to return.

Age, Residency, and Ownership Tests

Most relief starts with age verification, which the assessor confirms with a government ID or birth certificate. Residency tests usually require that the home is your primary dwelling for most of the tax year, and short seasonal stays elsewhere can still qualify if you keep legal ties at the property. Ownership can be in one spouse’s name, in both names, or in a living trust, but you should confirm that your county recognizes your title format for exemptions. Surviving spouses often keep senior benefits if they remain in the home and meet income rules, though you may need to file a fresh application as the sole owner. If you split time between two states, only one property can receive a senior or homestead exemption in a given year.

Income and Asset Limits

Income caps vary widely, so review the definition used by your locality before applying. Some places use adjusted gross income, while others use total household resources, which can pull in non‑taxable Social Security and some veterans’ benefits. Asset tests can exclude retirement accounts up to a limit, but many programs count brokerage balances and cash savings. If you are close to the cap, gather documentation that shows medical expense deductions or long‑term care premiums, since those can reduce countable income in certain programs. Keep a worksheet that lists what is included and excluded, so you can respond quickly if the assessor asks for clarification.

Primary Residence and Homestead Status

A senior exemption almost always stacks on a homestead designation, and both should show on your tax bill once approved. Homestead status confirms that you treat the property as your permanent home, which often lowers the taxable value even before senior relief is applied. If you recently bought the home, file the homestead form first, then add the senior application so both flow into the next billing cycle. Check for portability or transfer rules if you downsize within the same county, since some places allow you to carry a portion of your saved value to the new home. Update your mailing address and title records after any move so you do not miss renewal notices.

Our services at Tax Hardship Center for seniors

You want clear, fast help that respects your budget. Our services at Tax Hardship Center match senior needs with practical relief options and clean paperwork. We set up Installment Agreements when you need predictable payments, pursue Penalty Abatement when fees inflate your bill, and use Currently Not Collectible status if cash flow cannot support any payment right now. When IRS or state issues overlap with property tax problems, we coordinate timelines so approvals do not conflict. Start with a short call to review documents and choose the next step that fits your income and home plan.

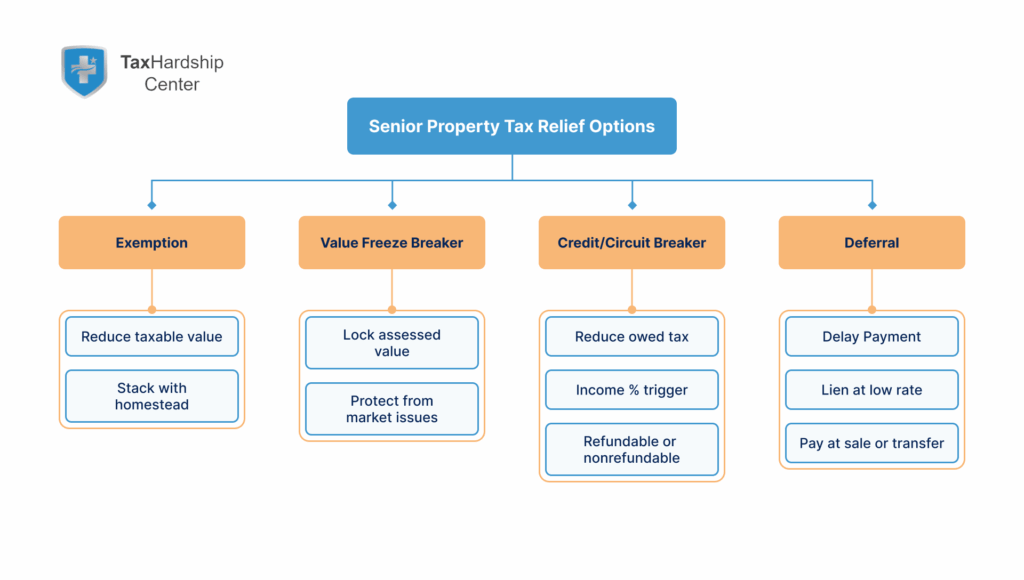

The Main Types of Property Tax Relief for Seniors

Senior property tax relief comes in several forms, and choosing the right mix can reduce bills now or defer them until later. Exemptions lower the taxable value of your home, credits reduce the actual tax owed, and freezes hold your assessed value steady even if neighborhood prices rise. Deferrals postpone payment and attach a lien that is settled when the property transfers, which can help cash flow for seniors on fixed incomes. Many states also offer circuit breaker programs that trigger extra relief when property taxes exceed a set share of income.

Senior Exemptions and Value Freezes

A senior exemption removes a fixed amount or percentage from the assessed value of your home, which lowers the tax calculation each year. Value freeze programs lock the assessment at a base year once you qualify, protecting you from future increases tied to market appreciation. Some localities let you combine an exemption with a freeze for larger savings, but you must keep your eligibility current. If your income rises above the cap, the freeze can lift in the next cycle, so plan for that change in your budget. Track renewal dates on your calendar, because missing a filing can reset your base year and reduce your long‑term benefit.

Credits and Circuit Breakers

Tax credits cut the amount you actually owe and can be refundable or nonrefundable depending on the program. Circuit breaker credits add protection when property taxes consume a high share of income, and the formula often scales relief as bills rise. These credits may require a state income tax filing even if you owe no income tax, so set a reminder to file the state form on time. Some programs allow renters over a certain age to claim a circuit breaker based on the share of rent that is treated as property tax. For federal deduction rules on real estate taxes and how they appear on your return, review IRS Publication 530 and the IRS guidance on homeowner tax benefits.

Deferrals for Cash‑Flow Relief

Deferral programs allow qualifying seniors to postpone paying property taxes until they move, sell, or pass the property to heirs. The county places a lien and charges interest at a set rate, which is usually below credit card or personal loan rates. Deferrals help seniors who want to stay in their homes but need current cash flow for health care, repairs, or daily expenses. Heirs should understand how the lien works, since the balance must be cleared from sale proceeds or estate funds at transfer. Review the interest rate and annual limits each year to decide whether a deferral still fits your financial plan.

How to Apply and Get Approved

A clean application shortens processing time and reduces the risk of denial. Start at your county assessor or treasurer website and download the senior exemption, credit, or deferral forms, then read the checklist for each. Gather proof of age, proof of ownership, a recent tax bill, and income documents such as SSA‑1099, 1099‑R, and state income tax returns. If your income changed midyear due to retirement or medical costs, attach a brief statement with dates and amounts so the reviewer sees the full picture. Submit before the filing deadline, request a stamped copy or submission receipt, and record your confirmation number in your notes. For background on settlement options if federal tax debt affects your budget, see our explainer on Offer in Compromise eligibility.

Documents Most Offices Ask For

Expect to provide a government ID, a deed or property tax statement, and a utility bill or voter registration card to prove residency. Income documents can include Social Security statements, pension forms, IRA distribution records, and bank interest forms. Some offices ask for a life estate agreement, trust certificate, or marriage certificate if ownership or survivor rights are involved. If you are applying for a deferral, include mortgage statements and insurance proof so the county confirms lien priority and coverage. Keep digital scans of everything in a labeled folder by year to make renewals fast.

Filing Windows and Renewal Cycles

Counties set strict filing windows, often between January and April, and late applications may push benefits to the next tax year. Renewal rules vary, but many exemptions require an annual affidavit to confirm that age, residency, and income still qualify. If your income fluctuates, watch the threshold each year and plan distributions to remain eligible where possible. When you move or transfer title, file update forms quickly so your benefits do not lapse due to record mismatches. Call the assessor if your approval letter does not arrive on schedule, and keep notes of each contact.

How Relief Affects Mortgages, Escrow, and Budgets

Tax relief changes the flow of money through your mortgage escrow and your monthly cash plan. If your lender escrows property taxes, approval can lower the escrow target, which may reduce your monthly payment after the next analysis cycle. You might receive an escrow refund for the surplus created by your new exemption or credit, but lenders often wait until the annual review to adjust. If you use a deferral, your mortgage contract may require lender consent because a county lien will attach to the property. Update your annual budget to reflect lower taxes and set aside part of the savings for maintenance, insurance, and emergency repairs. If IRS balances also affect cash flow, compare an Installment Agreement with a short‑term plan, and read our guide to IRS payment plans.

Communicating With Your Lender and Insurer

Send your approval letter to the mortgage servicer and ask when the escrow analysis will reflect your new bill. Confirm that your insurer has current coverage limits and that your property tax relief does not affect replacement cost calculations. If you receive an escrow surplus check, consider applying it to principal or building a home reserve fund. Seniors without escrow should calendar the revised due dates and amounts to prevent missed payments. Keep every statement that shows the new billed tax so you can reconcile lender math during the next analysis.

Common Mistakes and How to Avoid Them

Small errors can delay approval or reduce the size of your benefit. Applicants often forget to sign every page that requires a signature, omit a required schedule, or leave out a proof of residency. Some seniors over‑report income by including non‑counted items or under‑report it by missing retirement distributions, which leads to questions or denials. Others assume one‑time approval lasts forever and skip the renewal, which causes the full tax to return until relief is reinstated. Prevent these issues by using the county checklist, reviewing every line, and keeping a master packet for renewals. If penalty notices appear while you sort local relief, request Penalty Abatement to stop extra charges while you correct filings.

When to Appeal or Reapply

File an appeal if the assessor denies your application for a reason that you can fix with added documents or a clearer explanation. If your denial stems from income that exceeded the cap, watch for midyear rule updates or apply again after your income falls, such as the year after a large one‑time distribution. Consider a valuation appeal if the assessed value looks high compared with similar homes, since a lower value can help with both homestead and senior relief math. When you inherit a home from a spouse, reapply under survivor provisions that preserve senior status where allowed. Track deadlines for both benefit appeals and valuation appeals, since they often run on different calendars.

How Tax Hardship Center Supports Seniors

Property tax rules change often, and many offices use different forms for exemptions, credits, and deferrals. Our team helps you confirm eligibility, prepare accurate applications, and organize documents that examiners expect to see. We also review mortgage escrow impacts and help you set a budget that reflects lower tax bills. If a denial arrives, we show you how to appeal and build a clear case with the right evidence. Reach out for a quick review of your situation, so you can use every senior relief program you qualify for. If IRS debt also presses your budget, we can pair relief with an Offer in Compromise or IRS tax relief plan so you can protect the home and the income that supports it.

Work with Tax Hardship Center to maximize relief

At Tax Hardship Center, we help you turn rules into real savings by coordinating county forms with federal relief so cash keeps flowing. We build clean applications, prep income worksheets, and time filings so you keep homestead, senior exemptions, and freezes active. When you need breathing room, we set up Installment Agreements, pursue Offer in Compromise settlements, and file Currently Not Collectible requests when income cannot support payments. We also protect paychecks and bank accounts if collections start by addressing wage garnishment. Call us to align your property tax relief with a plan that fits your retirement budget.

In summary…

A short recap helps you act with confidence and avoid missed savings. Use the points below to review the key steps and decide which path fits your home and income.

- Confirm eligibility first

- Check age threshold, residency, and ownership format.

- Compare program income definitions with your documents.

- Check age threshold, residency, and ownership format.

- Pick the right relief mix

- Combine homestead with senior exemptions or freezes when allowed.

- Use credits or circuit breakers if taxes consume a high share of income.

- Combine homestead with senior exemptions or freezes when allowed.

- Apply with a complete packet

- Include ID, ownership, residency, and all income proofs.

- Track deadlines and keep digital copies for renewals.

- Include ID, ownership, residency, and all income proofs.

- Plan the cash flow

- Send approvals to your lender and review escrow changes.

- Build a reserve with part of the tax savings for home needs.

- Send approvals to your lender and review escrow changes.

- Avoid common pitfalls

- Do not skip the annual affidavit if your county requires one.

- Reapply or appeal quickly if your situation changes.

- Do not skip the annual affidavit if your county requires one.

Use these steps to reduce your bill now, protect future years with a freeze, or improve cash flow through a deferral. With steady paperwork and good timing, most seniors can lower property taxes and stay in the homes they love.

FAQs

What age qualifies a homeowner for senior property tax relief? Many programs start at 62 or 65, though some localities set different thresholds. Always check your county assessor rules and state guidelines before you apply. Age proof is usually a driver’s license, passport, or birth certificate. Surviving spouses can often keep the benefit with proper paperwork.

Can I get both a homestead and a senior exemption? Yes, in most places a senior exemption stacks on top of a homestead exemption, which reduces taxable value before senior relief applies. File both forms so they appear on the next bill. Check whether you must refile each year. Keep approval letters for your records.

How do income limits work for seniors on Social Security? Some programs count Social Security as income, while others do not, and a few count only a portion. Read the definition used by your locality so you can document what is included and excluded. If your income sits near the cap, track deductible medical costs that can lower countable income. Keep year‑end SSA‑1099 forms in your application folder.

What is the difference between an exemption and a deferral? An exemption or credit lowers today’s bill, while a deferral postpones payment and adds a lien that is paid later. Deferrals help seniors who need cash flow more than immediate savings. Review the interest rate and the effect on heirs before choosing a deferral. Some seniors use both by deferring the reduced bill after an exemption.

Will relief lower my mortgage payment? If you escrow taxes, your lender may reduce the monthly payment after the next analysis cycle. An approval can also produce a one‑time escrow refund if the account becomes overfunded. Ask your servicer for the schedule and keep your approval letter on file. Update your budget to reflect the new total cost of owning your home.