Introduction

Tax relief cost functions as a central decision point for individuals facing IRS debt, shaping expectations for how long a case might take, which services may be needed, and the kind of professional guidance required. Pricing varies significantly because each taxpayer profile includes specific attributes, such as the amount owed, the number of unfiled years, the presence of liens or levies, and the financial documentation required to verify hardship. These details determine the level of work a professional must perform, which creates distinct cost patterns across the tax relief industry.

Transparent pricing has become increasingly crucial as IRS enforcement actions intensify and as many individuals face uncertainty around what a credible service provider should charge. Cost clarity helps prevent confusion linked to misleading advertisements, unrealistic promises, and incomplete estimates that exclude core IRS compliance tasks. It also highlights the relationship between accurate documentation, IRS procedural steps, and the resources required to prepare and submit a viable relief request.

The role of the Tax Hardship Center within this landscape centers on a structured, case-based approach that clarifies what is included at each stage of the relief process. Instead of variable hourly billing or success-based fees prohibited in tax representation, the organization uses predictable pricing tied to the complexity and scope of work involved. This approach positions the service into the broader tax relief ecosystem while distinguishing it from high-risk providers known for vague estimates or inflated claims.

Modern IRS tax relief work also requires familiarity with financial standards, transcript data, debt aging, and the documentation patterns that determine eligibility for specific programs. These factors heavily influence professional labor time and the sequence of IRS interactions that follow. The cost of properly preparing IRS forms, reconstructing income records, managing back tax filings, and negotiating with the IRS reflects the complexity of these tasks. As a result, understanding the cost of tax relief involves not just a number but a detailed assessment of the case’s structure, evidence requirements, and regulatory boundaries.

This introductory framework sets the foundation for examining cost drivers, pricing models, IRS-linked variables, and the role of expertise in achieving a sustainable resolution path.

Key Takeaways

- Tax relief cost is shaped by IRS debt size, documentation availability, and the urgency created by active notices, liens, or levies.

- Professional pricing varies because each relief program requires distinct forms, financial analyses, and negotiation steps.

- Tax Hardship Center uses case-based pricing instead of hourly or contingent fees, aligning service fees with defined work scores.

- IRS transcripts, financial standards, and debt aging influence costs by determining procedural steps and evidence requirements.

- Transparency in cost protects individuals from misleading industry practices and supports predictable resolution planning.

Tax Relief Cost as a Core Entity in IRS Debt Resolution

Tax relief cost operates as an interconnected entity rather than a static figure. Cost levels reflect the attributes and conditions surrounding the taxpayer’s IRS status, the level of enforcement action already in motion, and the professional steps required to bring the account back into compliance. Because IRS debt cases follow standardized procedures but carry individualized variables, the cost entity should be understood through its relationships to documentation, eligibility criteria, IRS systems, and the nature of the relief program sought.

Several debt characteristics shape the pricing framework. The amount owed, the number of tax years involved, and the presence of unfiled returns directly influence the initial investigative workload. The type of income—whether W-2, 1099, or small business revenue—determines how much reconstruction or financial verification may be required. Each of these elements expands or contracts the time a practitioner must allocate to produce a compliant relief submission.

IRS enforcement status is another cost determinant. Cases involving CP503 or CP504 notices require immediate attention to prevent liens or levies, while active levies demand intensive communication with the IRS, making the professional workload more specialized. Resolution strategies also vary based on the Collection Statute Expiration Date, which adds complexity to cases approaching expiration because of the IRS’s review patterns and potential requests for updated financials.

Program-specific cost distinctions emerge because each relief option has its own procedural steps. Preparing an Offer in Compromise requires detailed financial analysis and asset verification, while establishing a simple Installment Agreement may involve fewer compliance actions. Cases requiring audit representation or penalty abatement often demand additional evidence gathering and structured documentation.

Cost differences between providers often arise from divergent billing models. Some organizations charge by the hour, which can yield unpredictable totals, while others use multistage pricing that separates investigation, compliance, and negotiation work. Case-based models provide more stable estimates because each fee tier is aligned with defined tasks.

The industry’s trust challenges amplify the importance of transparent cost communication. Many individuals seeking tax relief have encountered unclear pricing or misleading service guarantees, which makes predictable structuring essential for informed decision-making. In this environment, comprehensive cost explanations help individuals evaluate not only price but the credibility of the work being performed.

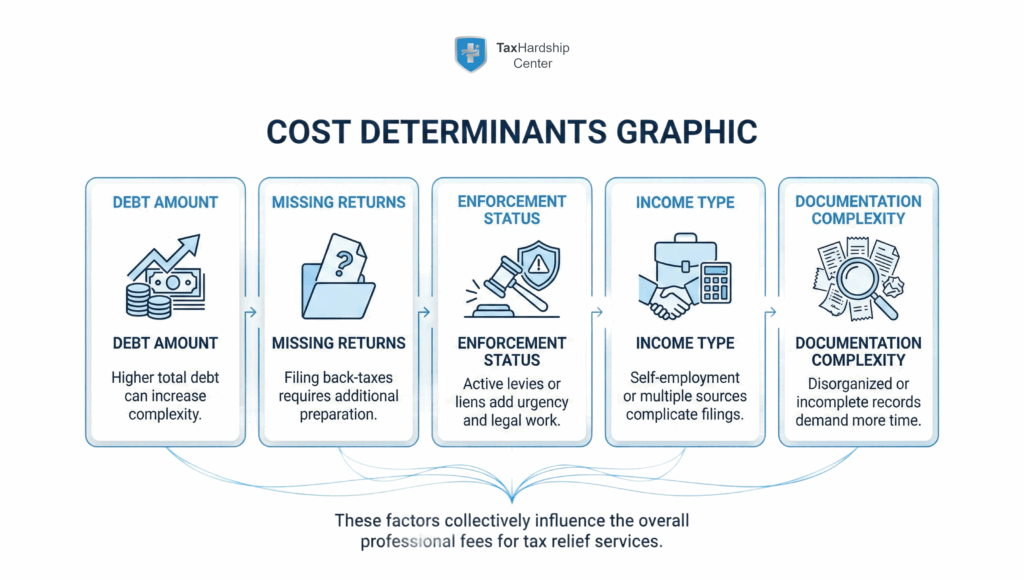

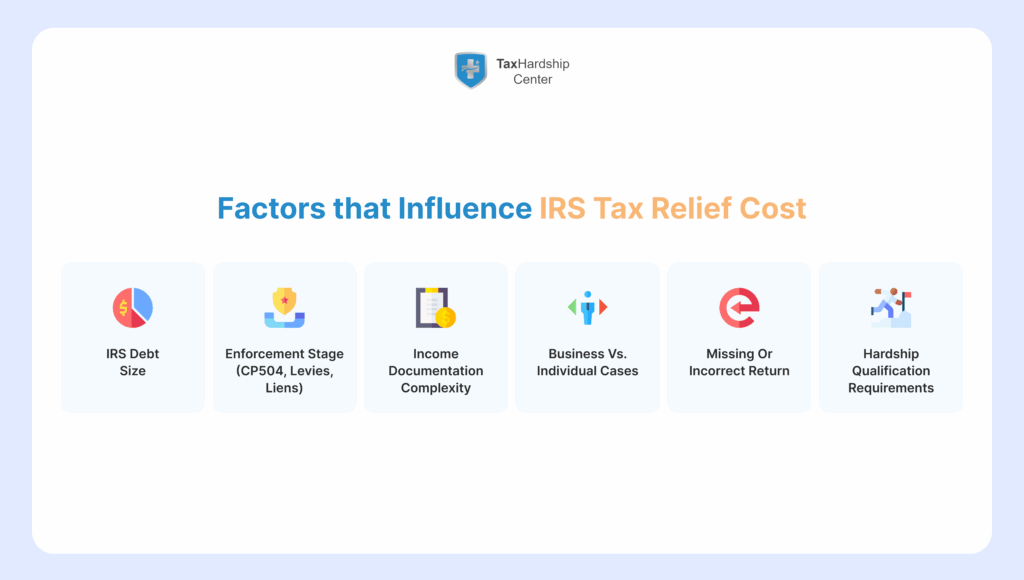

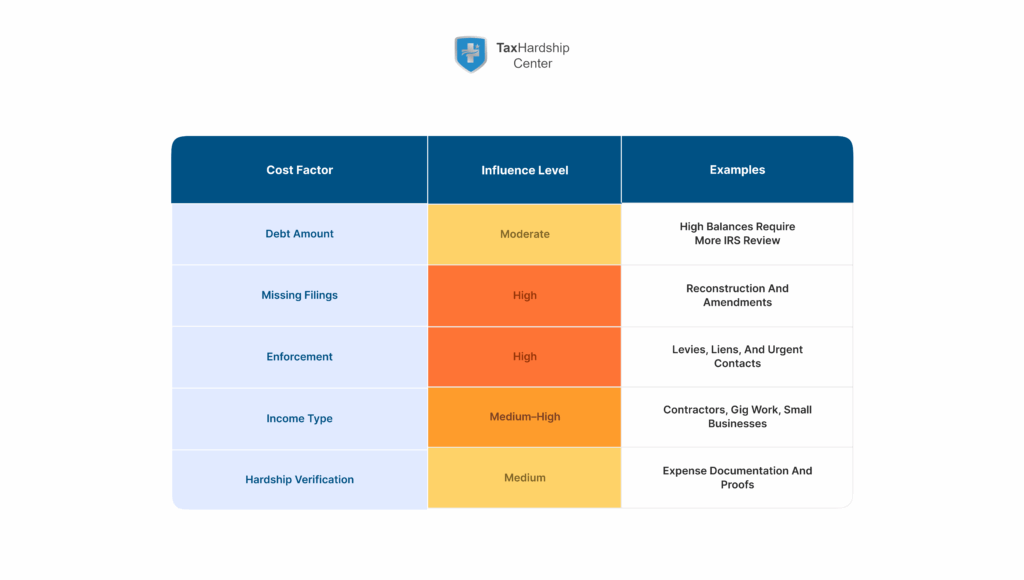

Factors that Determine the Cost of IRS Tax Relief Services

Several interconnected attributes influence professional pricing:

- IRS debt size

- Number of unfiled or incorrect returns

- Type of income and documentation complexity

- Active notices, liens, or levies

- Hardship qualification requirements

- Business ownership or multi-state obligations

A structured view of these factors appears in the table below:

| Attribute Category | Cost Influence | Reason for Impact |

| Debt amount | Moderate | Determines negotiation scope and filing requirements |

| Missing filings | High | Requires reconstruction and compliance work |

| Enforcement actions | High | Increases communication and evidence requirements |

| Income type | Moderate to high | Affects the level of documentation needed |

| Business complexity | High | Involves multi-layered records and forms |

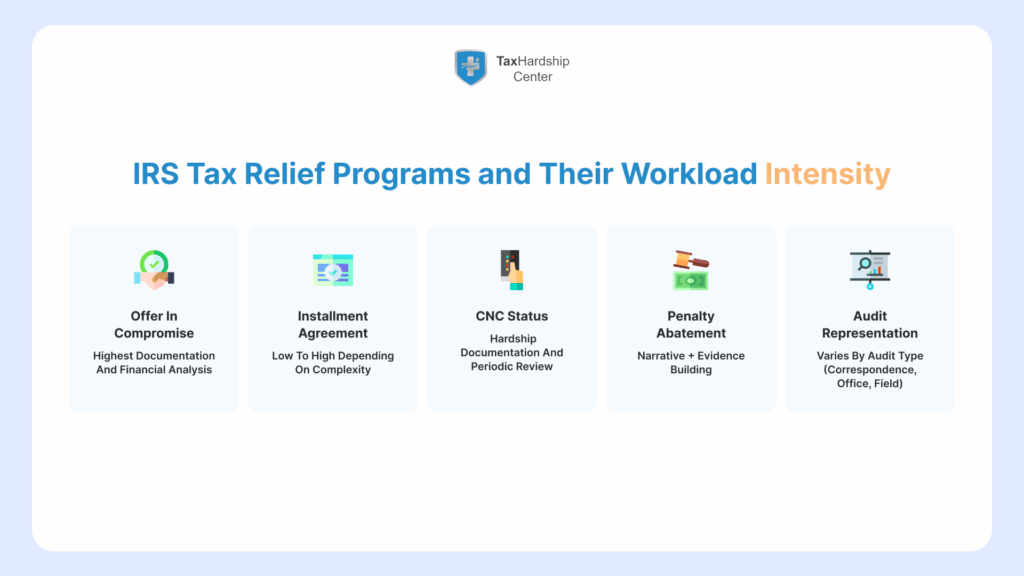

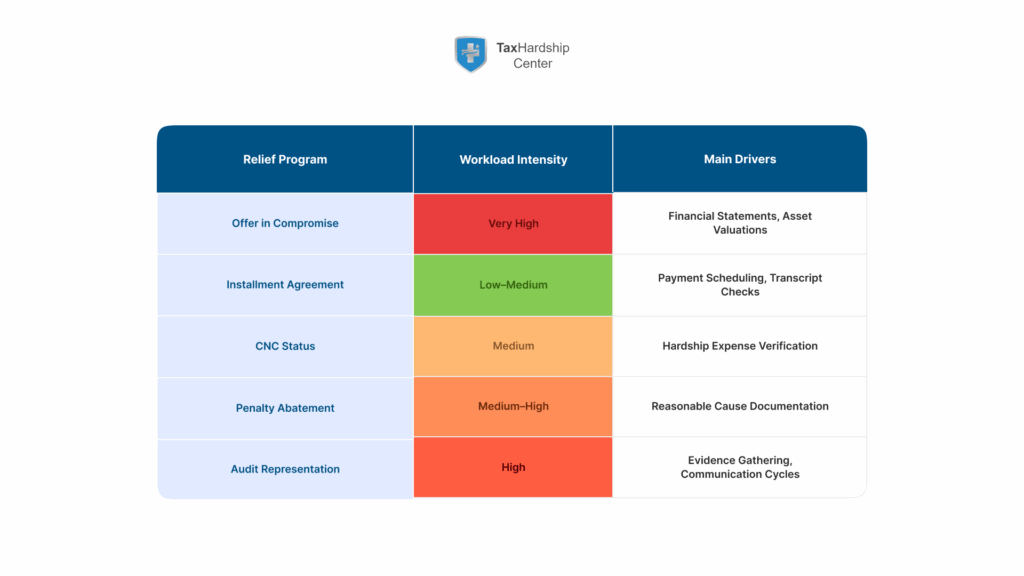

How Tax Relief Costs Vary by Relief Program

Different IRS programs require different work inputs:

- An Offer in Compromise requires asset reviews, income verification, and detailed financial forms.

- Installment Agreements range from simple payment scheduling to more complex negotiations involving transcript corrections.

- Currently Not Collectible cases require precise hardship documentation aligned with IRS financial standards.

- Penalty Abatement depends heavily on historical filings, reasonable cause evidence, and multi-year analysis.

Each program’s cost reflects these requirements rather than a generic price range.

Reasons Tax Relief Cost Estimates Differ Across Providers

Variations in cost arise from:

- Billing approach: hourly fees, program-based tiers, or case-based flat pricing.

- Differences in service scope, such as whether back tax filings are included.

- The level of expertise among enrolled agents, CPAs, or attorneys.

- Transparency in outlining the required IRS steps and documentation

- Additional charges linked to reinstatement, amendments, or appeals.

These distinctions influence predictability, trustworthiness, and user expectations within the tax relief market.

Tax Hardship Center (THC) Pricing Model and Service Structure

Tax Hardship Center organizes its pricing through a case-based framework that aligns each fee with the specific workload required for IRS debt resolution. This structure avoids the unpredictability of hourly billing and the prohibited contingency arrangements sometimes advertised in the tax debt marketplace. The model is built around the depth of financial analysis, the scope of compliance tasks, and the type of representation needed. Each case begins with a review of IRS transcripts and historical filings, which establishes the baseline for determining which relief pathways are viable and which documents must be reconstructed.

Service tiers clarify what work is performed at each step. The investigation includes retrieving and analyzing IRS transcripts, reconstructing the filing history, and identifying potential penalties affecting the balance. THC then conducts a compliance review to evaluate missing returns, filing inaccuracies, income documentation gaps, and any inconsistencies that could prevent the IRS from accepting a relief request. This stage helps determine the case’s complexity band and the corresponding cost bracket.

The representation tier includes direct communication with the IRS, preparation of financial disclosure forms, negotiation of relief programs, and submission of supporting documentation. This level of work requires familiarity with IRS financial standards and often involves multiple rounds of verification or clarification. Businesses, individuals with mixed income sources, and taxpayers with multi-year issues typically fall into higher-complexity categories due to the additional documentation required.

Transparent pricing practices play a central role in THC’s approach. The organization avoids hidden charges and clearly distinguishes between compliance tasks, negotiation work, and post-resolution support. Program-specific fees reflect the intensity of labor required rather than a blanket rate that obscures actual case demands. This clarity stands in contrast with relief mills that advertise exceptionally low entry fees but later add charges for essential procedures like filing back returns or submitting IRS forms.

Accreditation and public reviews reinforce trust in these pricing practices. THC’s professional staff includes enrolled agents, who are authorized to represent taxpayers before the IRS. Documentation standards, communication protocols, and process transparency help distinguish the service from providers that rely on high-pressure sales strategies. The presence of consistent positive reviews and industry-recognized credibility signals further supports the organization’s integrity within the tax relief ecosystem.

The resulting pricing model balances predictability with case-specific tailoring. It allows individuals facing IRS debt to understand the scope of work being performed, the procedural steps required for relief, and the labor intensity involved in managing long-term communication with the IRS.

Stage-Based Breakdown of Tax Relief Cost

The cost of professional tax relief services reflects a sequence of stages, each carrying unique documentation requirements and time commitments. These stages shape the total workload and explain why pricing differs significantly from case to case. Understanding the progression from investigation to resolution clarifies how each tier contributes to the overall cost structure.

The initial case evaluation involves pulling IRS transcripts, reviewing notices, and determining the accuracy of prior filings. Transcript analysis identifies the debt’s composition, including principal, penalties, and interest. It also reveals whether the IRS has issued enforcement notices or flagged irregularities. This stage may appear simple, but it often uncovers years of unfiled returns or income that must be reconstructed, creating a meaningful cost driver.

The compliance stage focuses on correcting and updating past filings. Cases involving missing returns, estimated tax gaps, or incorrect income entries require reconstruction using bank statements, payroll records, and third-party forms. The level of effort intensifies when multiple income streams are involved or when business records lack structure. Compliance work also includes amending prior filings, which adds documentation and verification steps.

Negotiation and representation form the core of professional tax relief. This stage involves preparing IRS forms such as 433-A, 433-F, or 656, depending on the relief option. Financial disclosures must align with IRS standards for expenses and assets, requiring detailed verification of living costs, bank activity, and ownership records. Multiple negotiations may occur during this period, especially when the IRS requests clarification or updated statements. Active levies, liens, or garnishments increase the intensity of communication and, therefore, influence costs.

The resolution and post-resolution stage includes implementing installment agreements, monitoring IRS correspondence, and analyzing the Collection Statute Expiration Date for future implications. Continued IRS requests for documentation or financial updates may arise, particularly in cases involving hardship status or business operations. Some resolutions require periodic check-ins to ensure compliance with payment plans or filing obligations, which can add to the long-term workload.

The table below summarizes key cost influences at each stage:

| Stage | Core Tasks | Cost Drivers |

| Evaluation | Transcript review, notice analysis | Number of years, enforcement status |

| Compliance | Return filing, amendments | Document gaps, business income |

| Negotiation | IRS forms, financial analysis | Hardship evaluation, asset verification |

| Resolution | Monitoring, communication | Long-term compliance requirements |

This multi-stage structure explains the layered nature of tax relief costs and the need for precise pricing tied to defined tasks.

Cost of Specific IRS Tax Relief Programs

Each IRS relief program carries its own procedural requirements and documentation demands, creating distinct pricing patterns across the industry. The nature of the program determines the level of financial analysis required, the IRS forms required, and the negotiation steps involved. Because taxpayers vary widely in income structure, debt composition, and compliance history, program-specific costs reflect a blend of IRS criteria and individual case attributes.

An Offer in Compromise is one of the most labor-intensive relief programs. It requires a detailed review of income, assets, expenses, and financial obligations. The IRS expects a full valuation of bank accounts, vehicles, real property, and potential future income. Preparing Form 656 and supporting documentation involves multiple layers of verification, often requiring clarification during review. Cases involving business ownership or shared household income increase the workload because the IRS examines all sources contributing to the financial picture.

Installment Agreements range from straightforward agreements requiring minimal documentation to complex cases that involve manual reviews by the IRS. Simple agreements typically require proof of income and updated transcripts. More complicated cases may involve restructuring payment terms, correcting transcript errors, or addressing historical compliance before the IRS accepts the proposal. These differences explain the range of labor commitment and cost between cases that appear similar on the surface.

Currently Not Collectible status requires evidence that paying the IRS would create financial hardship. The IRS compares income and expenses against standardized financial thresholds, making accurate documentation essential. Many cases require reconstructing household expenses and verifying recurring payments. Because the IRS periodically reviews CNC status, preparing for potential follow-up inquiries becomes part of the extended workload.

Penalty Abatement hinges on the ability to demonstrate reasonable cause. Evidence may include medical history, natural disasters, or financial disruptions that prevented timely filing or payment. Cases often require multi-year documentation, and the strength of the narrative influences the IRS evaluation. The cost structure reflects the need to align documentation with IRS expectations and prepare persuasive explanations.

Audit representation also contributes to significant cost variability. Correspondence audits generally involve limited exchanges of letters, while office or field audits demand extensive preparation, document collection, and communication. Business audits often require a detailed examination of expense categories, deductions, and revenue reporting practices.

The diversity of IRS programs and their procedural differences create distinct cost patterns tied not to generic industry averages but to the real-world labor required for successful navigation.

How IRS Actions Influence Tax Relief Pricing

IRS enforcement activity directly affects tax relief pricing because each action triggers specific procedural requirements, documentation demands, and communication steps. These actions define how urgently a case must be handled, how much negotiation labor will be required, and which forms or appeals may need to be prepared. As enforcement escalates and professional workload intensifies, two taxpayers with the same debt amount may face very different cost structures.

IRS notices are among the most significant cost drivers. Early notices, such as CP14 or CP501, signal the existence of a balance but do not necessarily involve enforcement action. Later notices, including CP503 and CP504, indicate that the file is moving toward levy or lien readiness. A case that reaches CP504 status often requires immediate intervention, repeated communication with the IRS, and documentation to demonstrate hardship or eligibility for negotiation. This increases the time and resources professionals allocate, raising the overall cost of representation.

Active levies or liens further complicate matters. A bank levy requires rapid coordination to verify account activity, document hardship, and request release. A wage garnishment demands coordination with the employer and the IRS, along with supporting financial disclosures. The professional steps involved include preparing the appropriate forms, confirming compliance status, and, when necessary, contesting outdated or incorrect IRS records. Each of these tasks increases labor requirements, thereby affecting pricing.

The Collection Statute Expiration Date also influences professional strategy and workload. When a case approaches expiration, the IRS may intensify review and request updated financial documentation. Cases near expiration require careful monitoring of compliance and timing, as specific taxpayer actions can unintentionally extend the statute. Professionals must analyze transcripts, calculate the statute timeline, and determine whether a relief option could lengthen or shorten exposure to enforcement.

IRS Fresh Start thresholds create additional distinctions. Debt levels above certain limits trigger manual reviews or additional financial disclosure. Cases below the thresholds may qualify for streamlined installment agreements, reducing the amount of documentation required. Professionals analyze transcript data and financials to determine whether adjustments or corrections can place the taxpayer into a more favorable category.

The table below summarizes the relationship between IRS actions and pricing:

| IRS Action | Cost Influence | Reason |

| Early notices | Low | Limited compliance issues |

| CP503/CP504 notices | Medium to high | Active enforcement risk |

| Liens/levies | High | Immediate action and documentation |

| Approaching CSED | Medium | Increased IRS scrutiny |

| Fresh Start thresholds | Variable | Documentation requirements differ |

These mechanisms demonstrate how IRS behavior shapes cost trajectories by dictating which procedural steps must be taken and how quickly they must be completed.

Taxpayer Profiles and Their Typical Cost Categories

Taxpayer profiles are a significant determinant of tax relief costs because each profile has distinct documentation patterns, income structures, and compliance histories. These variables influence the amount of professional labor required to prepare IRS forms, reconstruct filings, and negotiate acceptable resolutions. Categorizing these profiles clarifies why similar debt amounts may produce different cost outcomes.

Wage earners with W-2 income often fall into lower complexity categories. Their verification procedures rely primarily on standard payroll records and IRS wage transcripts, making reconstruction of income relatively straightforward. Missing filings in these cases usually require fewer supporting documents. As a result, service costs tend to remain closer to baseline ranges associated with compliance and negotiation tasks.

Independent contractors or gig economy workers exhibit greater variability. Income sources are often fragmented across different platforms or clients, each producing its own documentation requirements. Professionals must usually reconcile bank deposits, 1099 forms, and expense logs. These reconstruction tasks increase time commitments, especially when the IRS questions the accuracy of prior return entries. This profile typically aligns with mid-range cost brackets due to elevated documentation demands.

Small business owners introduce additional layers of complexity. Business returns, payroll records, expense categories, and potential misclassification of deductions complicate compliance analysis. Professionals reviewing these cases must often correct bookkeeping gaps, prepare multiple forms, and address questions that arise during IRS review. Multi-entity structures or mixed personal-business expenses significantly increase labor intensity, placing these cases in higher cost tiers.

Retirees or individuals living on fixed incomes create a different pattern of complexity. Verifying pension income, Social Security benefits, and limited assets may seem straightforward, but hardship qualification often depends on demonstrating that essential expenses exceed available income. This requires detailed documentation of medical costs, housing, and other necessary living expenses. Cases involving hardship evaluation often require meticulous alignment with IRS financial standards.

The table below summarizes typical profile-based cost patterns:

| Taxpayer Profile | Documentation Complexity | Common Cost Category |

| W-2 wage earners | Low | Lower range |

| Independent contractors | Medium | Mid-range |

| Small business owners | High | Upper range |

| Retirees/fixed income | Medium | Mid-range (varies with hardship) |

These distinctions illustrate how the cost entity interacts with taxpayer structure, compliance history, and financial documentation requirements

Comparing Tax Hardship Center Pricing to Typical Industry Ranges

Tax Hardship Center’s pricing structure differs from broader industry models by emphasizing case-based clarity and eliminating fees that obscure the actual cost of comprehensive representation. Many providers use entry-level pricing that appears low at first glance but excludes essential components such as back tax filings, IRS transcripts, or follow-up documentation requests. This fragmented structure can lead to inflated final costs once core tasks are added.

Industry pricing often follows three patterns: hourly billing, tiered service packages, and low-entry/high-add-on models. Hourly billing introduces unpredictability because the taxpayer cannot anticipate how many hours will be needed to complete compliance or negotiation tasks. Tiered packages offer predefined scopes but may exclude specialized work needed for complex income structures or active enforcement. Low-entry models frequently advertise minimal initial fees while deferring significant charges until after the individual has committed, complicating informed decision-making.

Tax Hardship Center prices its services through transparent, case-based assessments that map directly to the required scope of work. This structure accounts for IRS transcript analysis, compliance evaluation, documentation reconstruction, and negotiation steps. By defining these elements upfront, the model avoids unexpected add-ons commonly seen in the relief marketplace. The approach also reflects the level of professional expertise involved, including enrolled agents authorized to represent individuals before the IRS.

Public trust indicators align with THC’s model compared with industry averages. Many relief mills hold inconsistent reputations, short track records, or a history of complaints tied to misleading guarantees or incomplete service packages. THC’s communication protocols, accreditation, and documented reliability contrast with those of organizations that base pricing on aggressive sales strategies rather than procedural accuracy.

Cost comparison also involves understanding what is included in the quoted range. THC’s case-based structure typically incorporates core compliance tasks that other providers bill separately. Because compliance work underpins all negotiation attempts, integrating it into upfront pricing often yields more predictable final costs.

The table below reflects typical distinctions:

| Provider Model | Pricing Predictability | Common Issues |

| Hourly billing | Low | Uncertain final cost |

| Tiered packages | Medium | Exclusions not disclosed upfront |

| Low-entry models | Low | Significant add-on fees |

| THC case-based model | High | Defined scope tied to actual workload |

These contrasts highlight how transparent pricing aligned with clear service definitions positions THC as a more reliable option within the tax relief sector.

Conclusion

Transparent tax relief pricing depends on an accurate understanding of IRS procedures, case complexity, and the documentation required to support a viable resolution. The distinctions between income types, taxpayer profiles, enforcement stages, and relief programs explain why costs vary across the industry. Predictable pricing structures, such as those used by Tax Hardship Center, provide clarity by linking fees directly to defined professional tasks, including transcript review, compliance updates, financial disclosure preparation, and negotiation steps. This structured approach reduces uncertainty and aligns the service with the genuine workload required to manage IRS interactions effectively. Within a marketplace that often relies on vague estimates or narrowly framed promotional offers, pricing transparency remains a critical indicator of credibility and service quality.

Frequently Asked Questions

1. What defines the cost range for IRS tax relief services?

Tax relief pricing reflects debt size, enforcement level, missing filings, income structure, and the amount of documentation required to support negotiations or compliance corrections.

2. Why do Offer in Compromise cases cost more than other relief programs?

Offer in Compromise submissions require detailed financial analysis, asset verification, and extensive disclosure, increasing the labor commitment compared to other programs.

3. How do IRS notices affect professional tax relief costs?

Later-stage notices or active enforcement actions require rapid intervention, more frequent communication, and additional documentation, raising the workload and total cost.

4. Which taxpayer profiles typically fall into higher cost categories?

Small business owners and independent contractors often incur higher costs due to complex income verification, multi-source documentation, and multi-year filing reconstruction.

5. Does case-based pricing reduce unexpected tax relief charges?

Case-based pricing clarifies what tasks are included, reducing the risk of unpredictable add-on fees often associated with hourly billing or low-entry pricing models.