Millions of Americans file on time yet cannot pay the balance due. The IRS charges two separate penalties plus interest, and those add up fast. File the return anyway and pay something today because that lowers the monthly failure to pay hit. Set up a short-term payment plan online if you can clear the balance within 180 days. If your debt is large or your income fell, you may qualify for an installment agreement, an Offer in Compromise, or currently not collectible status.

Practical Steps You Can Take Today

Start with actions that stop the bleeding and keep you compliant. File the return or an accurate extension because the failure to file penalty runs at a higher rate than the failure to pay penalty. Pay any amount you can today because interest and penalties apply to the unpaid portion only. Open every IRS notice and respond by the stated date because missed deadlines close relief options. Create a simple budget for the next 90 days that covers rent or mortgage, food, utilities, and transportation before extra debt payments.

File first, then pay what you can

Filing signals cooperation and preserves access to plans. Send an e-filed return for speed, or mail certified with tracking if you cannot e-file. If documents are missing, request wage and income transcripts to complete the return correctly. Do not guess or file an incomplete return that creates further notices. If you already missed the filing date, file now because the penalty stops accruing for the months after you file. If returns are unfiled, get help fast through our Unfiled Tax Returns service.

Make an immediate partial payment

Use IRS Payments to post funds directly to your account. Even a small payment reduces the base that interest and penalties apply to each month. Label payments to the correct tax year and form so the IRS applies them properly. Keep the confirmation number and bank record with your tax file. If cash is tight, trim discretionary spending for 30 days to free a lump sum.

Prioritize essentials and protect your banking

Keep essential bills current so daily life stays stable while you solve the tax issue. Avoid bouncing checks and overdraft fees because those drag on progress. If you expect a levy risk, consider keeping only necessary funds in the account that receives income. Do not move money to hide it because that invites harsher enforcement. Communicate with creditors to pause or lower payments for a short window while you arrange an IRS plan.

Keep essential bills current so daily life stays stable while you solve the tax issue. Avoid bouncing checks and overdraft fees because those drag on progress. If you expect a levy risk, consider keeping only necessary funds in the account that receives income. Do not move money to hide it because that invites harsher enforcement. Communicate with creditors to pause or lower payments for a short window while you arrange an IRS plan.

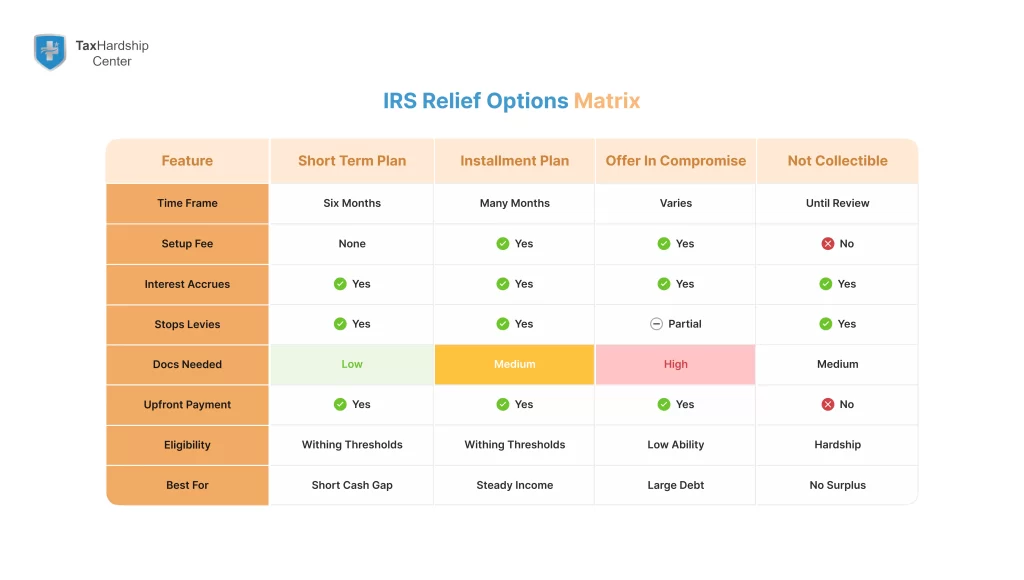

Payment Plans That Stop Penalties From Snowballing

You do not need to pay the full balance at once to get back on track. The IRS offers short-term and long-term plans with different fees and requirements. A short-term plan runs up to 180 days and usually has no setup fee. A long-term installment agreement spreads payments over many months and often works best when you owe several thousand dollars. Both options reduce collection pressure and help you avoid liens and levies when you make payments on time. Learn plan types and eligibility in our guide Understanding IRS Payment Plans and the IRS page on Payment plans and installment agreements.

Short-term payment plan basics

Choose a short-term plan when you can clear the balance within six months. You can request it online for many balances or by calling the number on your notice. Interest and the failure to pay penalty still accrue until you finish paying, but you avoid new collection actions while you remain on track. Set calendar reminders for your own payment dates so you never miss one. If your situation changes, switch to a long-term plan before you fall behind.

Long-term installment agreements

Apply for a streamlined installment agreement if you owe within the current thresholds and can pay within the standard term. Automatic bank debit reduces missed payments and helps avoid default. If you cannot qualify for streamlined terms, you may need to provide a financial statement and documents to support income and expenses. Keep the payment realistic because default restarts aggressive collections. Review the plan each year in case you can increase payments and end interest sooner. When you are ready, our Installment Agreement service handles the setup from end to end.

Fees, interest, and how to lower costs

The IRS charges a setup fee for some long-term plans and reduced fees for direct debit. Interest compounds daily on the unpaid balance, and the failure to pay penalty adds monthly costs. Making a larger initial payment cuts the debt that interest hits. Filing all missing returns prevents plan denial or default. If you receive a refund in a later year, the IRS will apply it to your debt rather than sending a check. For basics straight from the source, see IRS Topic 202: Tax payment options.

The IRS charges a setup fee for some long-term plans and reduced fees for direct debit. Interest compounds daily on the unpaid balance, and the failure to pay penalty adds monthly costs. Making a larger initial payment cuts the debt that interest hits. Filing all missing returns prevents plan denial or default. If you receive a refund in a later year, the IRS will apply it to your debt rather than sending a check.

When You Owe More Than You Can Ever Pay

|

Some taxpayers cannot pay the full amount within any reasonable timeline. The IRS offers an Offer in Compromise for cases where the amount you can pay is less than the total debt. The agency also considers special factors such as age, health, and earning potential. An offer requires complete financial disclosure and a nonrefundable application fee and initial payment. When prepared correctly, an accepted offer settles the debt for less than owed and ends collection activity after you meet all terms. Start by reviewing our Offer in Compromise service.

How an Offer in Compromise works

You must meet filing and payment requirements before the IRS will consider an offer. You submit a detailed financial package and propose an amount based on your ability to pay. The IRS reviews your assets, income, expenses, and equity to calculate reasonable collection potential. During review, interest and penalties continue, but active levies often pause. If accepted, you must stay current on all filings and payments for five years, or the IRS can reinstate the debt. For forms and online access, use the IRS Online Payment Agreement portal when applicable.

When an offer makes sense

Use an offer when your income cannot support payments even over a long term. Significant medical issues, fixed income, or business collapse often point toward this route. If you own substantial equity or high-value assets, the IRS will expect you to use that value before settling for less. Run the numbers with care because a weak offer wastes time and money. If your finances improve soon, an installment agreement may beat an offer.

Common offer mistakes to avoid

Do not submit incomplete forms or numbers that do not match your documents. Avoid guessing at asset values or leaving out bank accounts because the IRS will verify them. Do not stop filing current returns while your offer sits in review. Keep copies of everything you send and note delivery dates. If the IRS rejects the offer, consider an appeal if you believe the calculation missed facts.

Do not submit incomplete forms or numbers that do not match your documents. Avoid guessing at asset values or leaving out bank accounts because the IRS will verify them. Do not stop filing current returns while your offer sits in review. Keep copies of everything you send and note delivery dates. If the IRS rejects the offer, consider an appeal if you believe the calculation missed facts.

Pause Collections While You Stabilize Cash Flow

When you cannot pay anything beyond basic living costs, you can request currently not collectible status. The IRS will review your financials and pause active collection while you meet essential expenses. Interest still accrues, and the IRS may file a notice of federal tax lien to protect its claim. This status gives breathing room while you recover income or restructure your budget. You must file returns on time during this period. Read our primer on Currently Not Collectible status to see if you qualify.

How currently not collectible status works

You submit a financial statement with income, expenses, and assets. The IRS compares your numbers to national and local standards for necessary costs. If you qualify, the IRS stops levies and garnishments while you remain in hardship. The agency will review your case periodically to see if your ability to pay has changed. If your income rises, you may move into an installment agreement.

Keep records and stay compliant

Track pay stubs, rent or mortgage statements, utility bills, medical costs, and child care expenses. Update the IRS when major changes occur so you do not lose status unexpectedly. File every return on time to avoid default. Save a small emergency fund if possible so you can handle surprises without missing filings. If the IRS requests new documents, send them by the deadline to protect your pause.

Plan the exit

Use this window to rebuild income, reduce other debts, and right-size expenses. Explore side income or a higher-paying role if your schedule allows. When cash flow improves, request a plan that fits the new budget. Clearing the tax debt restores credit access and removes stress from future filings. A clear plan keeps you from sliding back into collections.

Use this window to rebuild income, reduce other debts, and right-size expenses. Explore side income or a higher-paying role if your schedule allows. When cash flow improves, request a plan that fits the new budget. Clearing the tax debt restores credit access and removes stress from future filings. A clear plan keeps you from sliding back into collections.

Avoid Bigger Trouble: Filing, Notices, and Deadlines

Compliance buys options and prevents harsher enforcement. File missing returns because the IRS will not approve most relief when returns remain open. Read every notice and mark action dates on your calendar. Request penalty relief when you qualify and keep proof that supports the request. If the IRS threatens a levy, respond within the window to protect appeal rights.

Penalties and how to reduce them

The failure to file penalty accrues at a higher monthly rate than the failure to pay penalty. Filing stops the failure to file penalty from growing. You can request first-time penalty abatement if you filed and paid on time for the prior three years. Reasonable cause relief may apply when serious events prevented compliance. A strong request cites dates, facts, and documents. For hands-on support, see our Penalty Abatement service.

Tax liens and levies

A notice of federal tax lien secures the government’s interest in your property. It can affect credit and the ability to sell or refinance assets. A levy takes wages or bank funds to pay the debt. Active payment plans, offers under review, and currently not collectible status can prevent or pause levies. Prompt action keeps more control in your hands. Learn the time frames in our blog on how long the IRS can collect back taxes.

Appeal rights and reviews

You can request an appeal when you disagree with a collection action. The Collection Due Process hearing window is short, so watch dates closely. Appeals consider whether the IRS followed procedure and whether your plan fits your finances. Keep your documents organized so you can present a clear case. If you miss the main window, other appeal routes may remain.

You can request an appeal when you disagree with a collection action. The Collection Due Process hearing window is short, so watch dates closely. Appeals consider whether the IRS followed procedure and whether your plan fits your finances. Keep your documents organized so you can present a clear case. If you miss the main window, other appeal routes may remain.

Documents, Proof, and How to Work With the IRS

Strong documentation smooths every request and speeds results. Build a simple folder system that holds identification, income, expenses, assets, and debts. Label each file by year and topic so you can find items fast when the IRS asks. Keep digital copies with secure backups for safety. A complete package lowers back-and-forth and reduces errors.

What to gather before you apply

Collect pay stubs, profit and loss statements, bank statements, mortgage or lease records, vehicle notes, insurance bills, medical bills, and child or dependent care costs. Include statements for retirement accounts and life insurance with cash value. List all debts with balances and payments. Note any special circumstances that affect your budget. Accurate data leads to realistic plans. For financial forms, review our explainer on IRS Form 433-F.

Best ways to contact the IRS

Use your notice for the correct phone number and hours. Call early in the day and expect hold time. Be polite, concise, and prepared with your Social Security number, notice, and a summary of your proposal. After the call, write a one-paragraph note that lists what you agreed to and the name or ID of the agent. Send follow-up documents by tracked mail or secure upload if offered.

When to get professional help

Seek help if you have multiple years unfiled, large balances, or complex business income. A professional can prepare returns, build a budget, and match the right relief to your situation. They can also handle calls and deadlines while you focus on work and family. If you already tried once and hit a wall, a guided second attempt often succeeds. Choose a firm with clear fees and experience in IRS collections.

Seek help if you have multiple years unfiled, large balances, or complex business income. A professional can prepare returns, build a budget, and match the right relief to your situation. They can also handle calls and deadlines while you focus on work and family. If you already tried once and hit a wall, a guided second attempt often succeeds. Choose a firm with clear fees and experience in IRS collections.

Special Cases for Small Businesses and the Self-Employed

Business taxes bring extra rules and faster enforcement. Payroll tax debt draws quick attention because it involves employee withholdings. Sales tax and excise tax also trigger strict procedures. Self-employed taxpayers must manage estimated taxes to avoid new balances. Plan for these cases with tighter cash controls and better forecasting.

Payroll taxes and trust fund recovery

If your business missed payroll deposits, address that first. The IRS can assess the trust fund recovery penalty on responsible individuals. Set a realistic plan and make all new deposits on time going forward. Keep payroll current while you resolve the past debt. Consider a professional payroll service if prior errors caused the problem.

Estimated taxes for sole proprietors and gig workers

Set aside a set percentage of each payment into a separate tax savings account. Make quarterly estimated payments to avoid new penalties. Track mileage, home office, and other deductible costs so your taxable income reflects real profit. Review your rates each quarter and adjust if income changes. Use simple software or a spreadsheet to forecast the next payment.

When a business should consider an offer or CNC

If revenue fell and debt exceeds realistic profit, an Offer in Compromise may fit. If you cannot pay anything after essential business and household costs, currently not collectible can pause collections. Keep business and personal records separate to simplify reviews. Close inactive entities that create confusion. Tight operations help you qualify and stay compliant after relief. For small-business tactics, see our guide to negotiating tax debts.

If revenue fell and debt exceeds realistic profit, an Offer in Compromise may fit. If you cannot pay anything after essential business and household costs, currently not collectible can pause collections. Keep business and personal records separate to simplify reviews. Close inactive entities that create confusion. Tight operations help you qualify and stay compliant after relief.

Talk to Tax Hardship Center Before You Decide

At Tax Hardship Center, we help you compare all options and pick the lowest-cost path over time. We review your income, expenses, and assets, then match you with a plan that the IRS will accept. If a payment plan works, we implement it with direct debit so you stay on track. If settlement or hardship fits better, we build the file and handle every deadline. Explore our full IRS Payment Relief Options and Services pages to see how we work.

In summary…

This section distills the article into simple, direct takeaways you can act on today.

- Act now

- File the return or extension to stop the bigger penalty.

- Pay something today to reduce interest and the failure to pay penalty.

- File the return or extension to stop the bigger penalty.

- Pick the right plan

- Short-term plan if you can pay within 180 days.

- Long-term installment agreement for larger balances with steady income.

- Short-term plan if you can pay within 180 days.

- Consider hardship options

- Offer in Compromise when you cannot ever pay the full amount.

- Currently not collectible when you cannot pay anything after essentials.

- Offer in Compromise when you cannot ever pay the full amount.

- Protect your rights

- Open every notice and respond by the stated date.

- Request penalty relief when you qualify and keep proof.

- Open every notice and respond by the stated date.

- Stay organized

- Gather income, expense, asset, and debt records before you apply.

- Keep all future filings current to avoid default.

- Gather income, expense, asset, and debt records before you apply.

A clear plan, prompt filing, and honest numbers give you control. Solve the tax debt step by step, and keep cash flow stable while you do it.

How Tax Hardship Center Can Help Right Now

Our services at Tax Hardship Center focus on speed, accuracy, and realistic budgeting. We set up Installment Agreements that fit your monthly cash flow so you avoid default. When full payment is not possible, we prepare and submit Offers in Compromise with complete financial packages that match IRS standards. If hardship leaves no room to pay, we secure Currently Not Collectible status to pause collections. We also pursue Penalty Abatement when your record and facts support it.

FAQs

What happens if I file but cannot pay the IRS right now

The IRS still charges interest and the failure to pay penalty, but filing stops the larger failure to file penalty. Filing also keeps relief options open. You can set up a short-term or long-term plan to avoid enforced collection. Pay any amount you can today to cut costs. Keep filing on time in future years while you pay down the balance.

Can the IRS take my paycheck or bank funds if I owe

Yes, the IRS can levy wages or bank accounts after it sends required notices. You can often stop a levy by setting up a qualifying plan or by entering currently not collectible status. Respond quickly to levy warnings to preserve appeal rights. Keep records of your income and expenses so you can propose a realistic resolution. If a levy hits, contact the IRS immediately to request release once you set a plan.

Do payment plans remove penalties and interest

Plans do not remove interest and penalties already assessed. They prevent harsher actions while you pay. You can request first-time penalty abatement if you met prior compliance, and you can request reasonable cause relief for serious events. Larger initial payments reduce interest going forward. Staying current on new filings prevents new penalties.

How does an Offer in Compromise affect my credit

The IRS does not report to consumer credit bureaus. If the IRS filed a notice of federal tax lien, public records may affect lending decisions. An accepted offer resolves the debt once you meet terms, which lenders often view as positive compared to active collections. Keep copies of the acceptance letter for your records. Maintain compliance for five years after acceptance to avoid reinstatement.

Should I borrow from a 401(k) or use a credit card to pay taxes

Tapping retirement can trigger taxes and penalties that increase your overall cost. High-interest credit cards can create a worse problem than the IRS debt. Compare the IRS plan costs to loan or card rates before you borrow. Often a direct debit installment agreement costs less and carries fewer risks. Get advice before moving retirement funds.