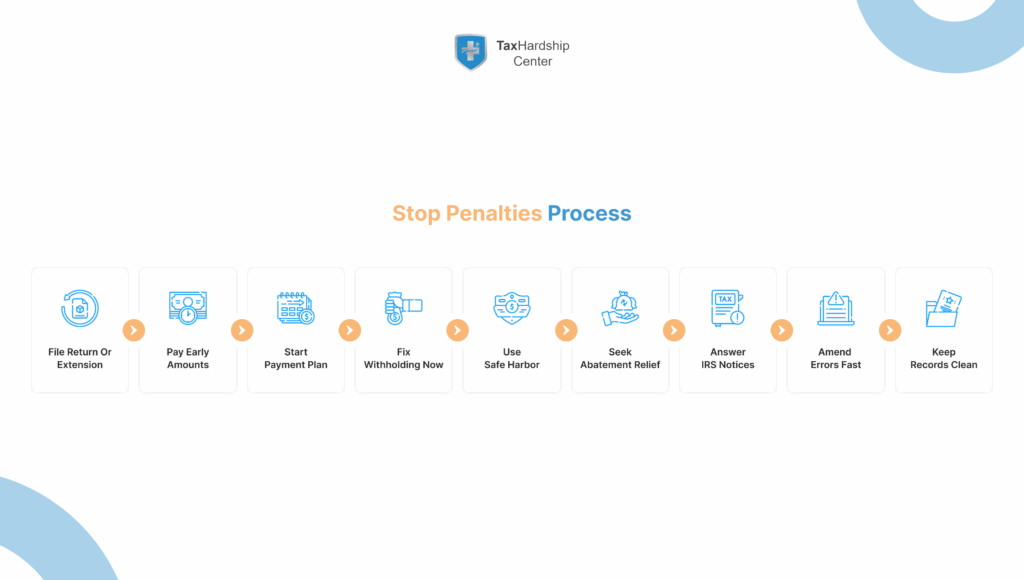

Clever taxpayers file on time, pay as much as possible, and keep interest from growing. First-time abatement can remove a penalty when you keep a clean filing record. Reasonable cause relief exists when life events show that you acted responsibly. An installment agreement keeps the IRS from adding new penalties while you pay over time. Strong withholding or quarterly estimates prevent underpayment charges later.

The IRS charges two main penalties: failure to file and failure to pay. Interest accrues daily on unpaid tax until you pay the full balance. You can avoid the failure-to-file penalty by filing on time even if you cannot pay in full. You can limit interest by paying as much as possible as early as possible.

What is the fastest way to avoid penalties right now?

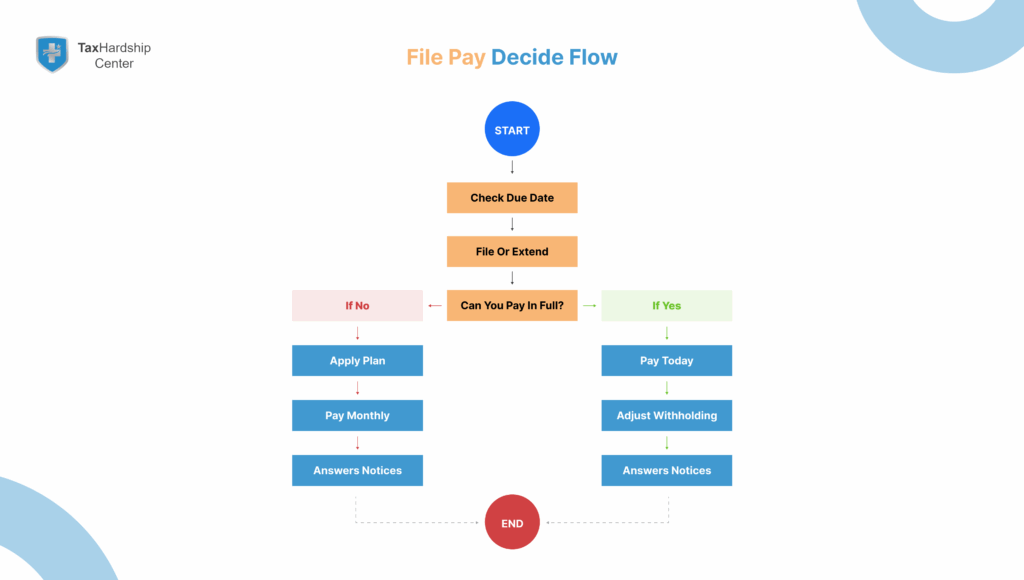

You stop the harshest penalty by filing your return or extension on or before the due date. You then pay as much as you can with the return or extension to reduce interest. If you cannot pay the rest, you apply for an online payment plan. You also check if you qualify for first-time abatement based on a clean three-year filing history. You keep future penalties away by fixing your withholding or estimated payments for the current year.

Do extensions remove penalties and interest?

Extensions give you more time to file, not more time to pay. If you owe after the original due date, the IRS charges a failure-to-pay penalty and interest. You still protect yourself by filing the extension to avoid the larger failure-to-file penalty. You also send a payment with your extension to cut interest and the failure-to-pay penalty. You then complete your return as soon as you can.

Can I remove a penalty after the IRS assesses it?

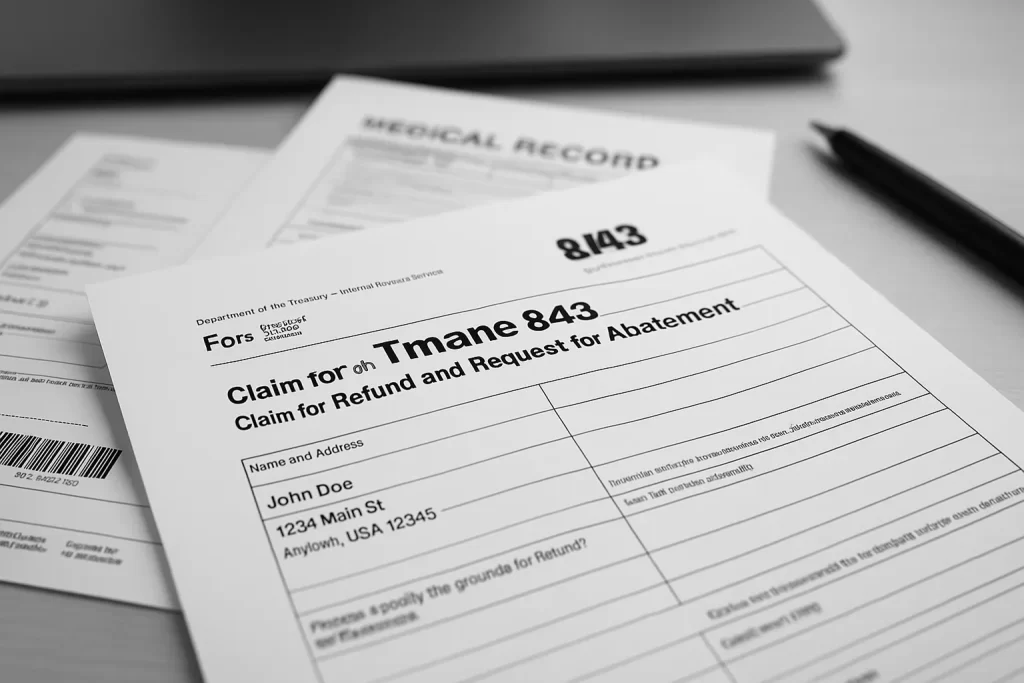

Yes, you can request penalty abatement in many cases. First-time abatement applies if you filed and paid on time for the prior three years and have no unaddressed penalties. Reasonable cause relief applies when events like serious illness, disasters, or records beyond your control made compliance impossible. You write a clear timeline, show documents, and explain how you fixed the issue going forward. The IRS reviews and may remove all or part of the penalty.

How do I keep interest from growing?

Interest stops growing only when you pay the tax and penalties in full. You reduce total interest by paying early and often. You apply extra funds to the principal balance rather than waiting for a final bill. You also avoid new penalties by keeping an active installment agreement when you cannot pay in full. Clean filing and fast responses to notices prevent compounding charges.

What is the safe harbor for estimated taxes?

Most people avoid underpayment penalties if they pay at least 90 percent of the current year tax or 100 percent of the prior year tax. If your adjusted gross income exceeded a high-income threshold last year, the prior-year safe harbor rises to 110 percent. You spread estimated payments across the four due dates to match your income flow. You review midyear and adjust when income changes. You aim to avoid a large bill at filing time.

What Counts as an IRS Penalty or Interest and Why It Hits Hard

This section explains every major charge the IRS can add to your balance and why quick action saves money. The failure-to-file penalty grows fast and tops the list of costly mistakes. The failure-to-pay penalty accrues monthly and adds up when you delay payment. Accuracy-related penalties apply when you understate tax by a large amount or show negligence. Interest compounds daily on tax and on many penalties, which makes small debts grow over time.

Failure to file versus failure to pay

The failure-to-file penalty is bigger and reaches a high cap when months pass without a return. Filing on time prevents this charge even if you cannot pay. The failure-to-pay penalty is smaller but continues to accrue until you clear the debt. You lower both exposures by filing and paying something by the due date. You then set a plan to handle the rest.

Accuracy and information return penalties

Large understatements or negligence can trigger an accuracy-related penalty. Missing or late information returns can also draw separate penalties, especially for businesses that file many forms. You reduce risk by keeping documentation and matching forms like W-2s and 1099s to your return. You amend quickly when you find an error. You use checklists to avoid repeated mistakes.

How interest works on IRS balances

Interest accrues daily on unpaid tax, and it also applies to many penalties once the IRS assesses them. The rate changes quarterly and can rise when market rates rise. You pay less interest when you pay earlier in the year and when you make extra payments. You also cut interest by stopping new penalties that would become part of the balance. A payment plan helps you control the account while you finish paying.

File on Time Every Year and Stop the Failure-to-File Penalty Before It Starts

This section shows how timely filing protects you from the largest penalty, even when cash feels tight. You file your return or a valid extension by the April deadline, and you mark state deadlines separately. You keep digital reminders and a checklist for tax documents. You e-file to timestamp your submission, and you keep the acceptance notice. You do not wait for the perfect return when time runs short because filing something on time saves real money.

Practical steps to hit the filing deadline

Create a document list in January and request missing forms by early March. Gather prior-year returns, W-2s, 1099s, and forms that support credits and deductions. Use trusted software or a preparer and start a draft return early. Submit the return or extension with a payment before the deadline. Save confirmations and set a follow-up date to finish any remaining items.

Why an extension still helps

An approved extension avoids the failure-to-file penalty, which costs far more than the failure-to-pay penalty. You also gain time to receive corrected forms and to fix complex issues. You include a payment with the extension to cut interest and the smaller penalty. You then complete the return long before the extended deadline. You document every step so you can show good faith if the IRS asks.

Pay as Much as You Can by the Due Date and Shrink Interest From Day One

This section covers smart payment tactics that cut total cost even when you cannot pay in full. You send any amount with your return or extension. You prioritize IRS debts over lower-rate obligations when interest rates rise. You consider short-term budgeting moves to free cash for your tax bill. You avoid high-fee credit products and compare rates before using credit cards. You always confirm that payments apply to the correct tax year and form.

Make targeted payments during the year

Use IRS Direct Pay or the Electronic Federal Tax Payment System to make periodic payments. Apply windfalls like bonuses or refunds from amended returns. Break large balances into weekly or biweekly amounts to keep momentum. Track balances and interest so you can see progress. Keep records of every transaction in case you later seek abatement. For structured options that fit your cash flow, review IRS payment relief options.

Avoid costly payment mistakes

Do not skip a payment while waiting for a notice. Do not mix business and personal tax payments. Do not ignore small residual balances after a return correction. Do not assume the IRS will apply payments the way you intend. Do not forget to adjust withholding to prevent the same problem next year.

Our Services at Tax Hardship Center: Fast Relief Without Missteps

This section explains how we step in when timelines are tight and interest is climbing. At Tax Hardship Center, we help you choose and set up the right installment agreement and make sure payments post to the correct year. Our advisors prepare complete files for penalty abatement so you do not leave relief on the table. When settlement makes sense, our team evaluates and submits an Offer in Compromise. If your finances qualify, we can position you for Currently Not Collectible status to pause collections while you stabilize.

Use an IRS Payment Plan to Halt New Penalties and Keep Your Account in Good Standing

This section explains how installment agreements protect you while you pay over time. A payment plan reduces or stops certain penalties once the agreement starts and remains current. You avoid enforced collection as long as you make payments and file on time going forward. You choose between short-term and long-term plans based on the total balance. You apply online when eligible to speed approval through the Online Payment Agreement.

Set up the right plan for your situation

Short-term payment plans cover balances you can clear within 180 days. Long-term plans use direct debit and work well for larger debts. You propose a payment that fits your budget and leaves room for current-year taxes. You keep all future returns and payments current while on the plan. You consider revising the plan if your income changes. For deeper guidance, read our blog on understanding IRS payment plans.

Keep the agreement in good standing

Make automatic payments to avoid missed due dates. File all returns on time during the agreement. Contact the IRS immediately if a payment fails. Increase payments when you can to reduce interest. Document hardships if you need a temporary adjustment.

Qualify for Penalty Relief and Ask for Abatement the Right Way

This section shows how to remove penalties you already owe. First-time abatement works when you have a clean record for the prior three years. Reasonable cause relief applies when events outside your control prevented compliance. Statutory exceptions and IRS errors also allow relief. You gather proof and explain the timeline clearly to improve your chances. See the IRS page on penalty relief and learn how our penalty abatement service builds a strong request.

First-time abatement steps

Confirm you filed and paid on time for the prior three years. Make sure you filed the current return or a valid extension. Pay or arrange to pay the underlying tax. Call the IRS or write a letter requesting first-time abatement and cite your record. Keep notes of the call and copies of letters for your files. For strategy tips, review our guide to reducing IRS penalties.

Reasonable cause relief that works

Explain what happened, when it happened, and how it prevented filing or payment. Provide documents like hospital records, insurance claims, or statements from third parties. Show that you acted responsibly before and after the event. Describe steps you took to prevent a repeat. Keep the tone factual and concise. The IRS outlines reasonable cause standards and First Time Abate on its administrative penalty relief page.

Manage Withholding and Estimated Taxes to Avoid Underpayment Penalties

This section covers safe harbors and midyear adjustments that stop penalties before they start. You review your paystub withholding with Form W-4 after life changes like marriage, a new job, or side income. You compute quarterly estimates if you make nonwage income from a business, investments, or rentals. You use the 90 percent current-year or 100 percent prior-year safe harbor to avoid penalties. High earners aim for 110 percent of the prior-year tax when required. You adjust midyear to keep on track when income shifts. See IRS Topic 306 on the underpayment of estimated tax for details.

Build a simple estimate routine

Mark the four estimate dates on your calendar and use a worksheet each quarter. Track income and deductions so you can update totals quickly. Pay more in quarters with higher income to match cash flow. Revisit your plan each time you land a new client or sell an asset. Keep confirmations from EFTPS for your records.

Fix withholding problems fast

If you underwithheld early in the year, ask your employer to increase withholding for the next pay periods. Withholding counts as paid evenly across the year, which can help avoid penalties. Use a special withholding bump late in the year if needed. Combine that with an extra estimated payment for cushion. Confirm changes appear on your next paystub.

Use Extensions Wisely and Understand What They Cover and What They Do Not

This section clarifies how extensions help and where they do not. An extension gives more time to file but not more time to pay. You still send a good-faith payment with the extension to reduce charges. You collect late-arriving forms and finish an accurate return. You fix complex issues like basis tracking or K-1 questions without rushing. You wrap up long before the extended deadline to avoid last-minute surprises.

How to estimate your extension payment

Start with last year’s tax and adjust for known changes. Add income from new jobs, side work, or sales. Subtract higher withholding or estimated payments already made. Consider safe harbor rules to avoid penalties. Send the best estimate you can rather than waiting for perfect information.

Common extension myths

An extension does not hide a balance due. An extension does not stop interest. An extension does not excuse missing forms forever. An extension does not apply to state returns unless the state says so. An extension does not replace the need to organize your records.

Respond to IRS Notices Quickly and Fix Issues Before Costs Snowball

This section helps you act fast when the IRS sends a letter. You open the notice, read the code, and note the response date. You compare the IRS numbers with your records. You call if the notice invites a call, or you mail a response with copies of documents. You keep a log of dates and contacts for your file.

Disputes and adjustments that stop extra charges

If the IRS misapplied a payment, you ask for a correction. If a third party sent a late or wrong form, you provide proof. If identity theft caused a mismatch, you follow the IRS identity verification process. If you agree with the change, you pay or set a plan right away. You do not wait and let small balances turn into larger debts.

When You Cannot Pay in Full, Compare Options Like Offer in Compromise and Currently Not Collectible

This section outlines hardship options that can pause or reduce what you owe. An Offer in Compromise can settle for less than the full amount when you meet strict financial criteria. Currently Not Collectible status pauses active collection when you cannot pay basic living expenses. Partial pay installment agreements combine a plan with a balance that expires at the collection statute date. You review each option against your budget and assets. You use accurate financial disclosure to support your choice. Learn more about our Offer in Compromise service and Currently Not Collectible help.

How to choose the right hardship path

List income, expenses, assets, and debts with current documentation. Test affordability with a realistic monthly budget. Consider how long the IRS has left to collect. Compare the cost and time of each program. Pick the path that gives stability and compliance going forward.

Special Rules for Business Owners and Payroll Taxes That Demand Extra Care

This section alerts employers to strict payroll tax rules and steep penalties. Trust fund taxes from employee withholding carry personal liability for responsible persons. Deposit schedules and form deadlines require a calendar that you follow. Missing deposits can trigger immediate penalties and interest. Accurate worker classification prevents payroll tax surprises. Clean bookkeeping helps you spot issues before they grow.

Controls that keep payroll compliant

Use automated payroll systems that schedule deposits on time. Reconcile payroll reports to general ledger monthly. Review notices from the IRS and state agencies the day they arrive. Assign backups for payroll duties during vacations or illness. Keep a year-end checklist for W-2s, 1099s, and information returns.

Keep Clean Records and Amend Returns Fast When You Spot a Mistake

This section focuses on documentation that supports penalty relief and smooth corrections. Organized records let you answer IRS questions in minutes. Clear logs help you request abatement with confidence. Amended returns fix errors before the IRS contacts you. Quick action shows good faith and can reduce penalties. A tidy file saves time for everyone involved.

A simple record system that works

Store digital copies of all returns, forms, and receipts in a secure cloud folder. Keep a running spreadsheet of estimated payments and withholding changes. Save IRS confirmations and notice response letters together. Add notes with dates and names after any IRS call. Review your folder each quarter to stay current.

How Tax Hardship Center Helps You Prevent and Resolve Penalties

This section explains how expert guidance saves money and stress during the tax year. Tax Hardship Center reviews your filing history, notices, and cash flow to map the fastest fix. The team sets up the right installment agreement, requests penalty abatement, and prepares Offer in Compromise or Currently Not Collectible filings when needed. Advisors help you adjust withholding and estimates so you avoid new issues. Clear timelines and weekly check-ins keep your case moving. You leave with a plan that protects the next year as well.

What to expect when you engage us

You start with a short discovery call to review your goals and deadlines. We collect transcripts and documents with your consent. We present options with pros and cons and a step-by-step plan. We handle filings and calls while you focus on work and family. We set reminders so you stay compliant after resolution. For more context, see our blog on IRS back tax relief options.

In summary, how to avoid penalties and interest in simple steps

This section gives you a concise wrap-up and a checklist you can act on today.

- File your return or a valid extension by the due date to avoid the largest penalty.

- Send a good-faith payment with the return or extension to cut interest.

- Keep e-file confirmations and document your steps.

- Send a good-faith payment with the return or extension to cut interest.

- Pay as much as possible early and use a payment plan to stay protected.

- Automate payments and increase amounts when you can.

- Track interest so you can see results.

- Automate payments and increase amounts when you can.

- Seek penalty relief when you qualify.

- Use first-time abatement with a clean history.

- Build a reasonable cause case with dates and documents.

- Use first-time abatement with a clean history.

- Fix current-year withholding and estimates.

- Aim for the 90 percent current-year or 100 percent prior-year safe harbor.

- High earners target 110 percent of prior-year tax when required.

- Aim for the 90 percent current-year or 100 percent prior-year safe harbor.

- Respond to IRS notices immediately and keep records organized.

- Correct errors, confirm payments, and log every contact.

- Amend returns quickly when you find mistakes.

- Correct errors, confirm payments, and log every contact.

These steps cut costs now and prevent future problems. You can handle many tasks on your own with a clear plan. If you need guidance, Tax Hardship Center stands ready to help. A brief call can turn a stressful balance into a manageable path forward.

FAQs

How do I avoid the failure-to-file penalty if I am missing a form?

File the return by the deadline using the best information you have and include an extension if you need more time. You then file an amended return when the missing form arrives. Filing on time protects you from the largest penalty. You keep proof that you requested the form from the issuer. You also track any amended changes so you can pay quickly.

Can I get penalties removed if I had a serious illness?

Yes, reasonable cause relief may apply when illness, disaster, or similar events prevented compliance. You provide dates, medical records, and a statement explaining the impact. You show that you acted responsibly before and after the event. You outline steps you took to prevent a repeat. The IRS reviews and may abate all or part of the penalty.

Does an installment agreement stop interest?

No, interest continues until you pay in full, but a payment plan can reduce or stop certain penalties and keeps your account compliant. You still save money by paying sooner and paying extra when possible. You avoid enforced collection while you stay current. You combine the plan with better withholding. You review the plan each year.

What if my income varies through the year?

Use the annualized installment method for estimated taxes so payments match your income timing. Increase withholding in high-income months to smooth totals. Revisit estimates each quarter and after big income events. Keep a log to support your calculations. Aim to meet a safe harbor so you avoid penalties even with variable income.

Is first-time abatement a one-time benefit?

Yes, it generally applies once per tax type when you meet the criteria. You need a clean three-year history and compliance for the current year. You can still seek reasonable cause relief for other years when facts support it. Keep records to show your good compliance track. Use the experience to improve your process going forward.