Getting a final levy notice can feel like the IRS is already at your bank account.

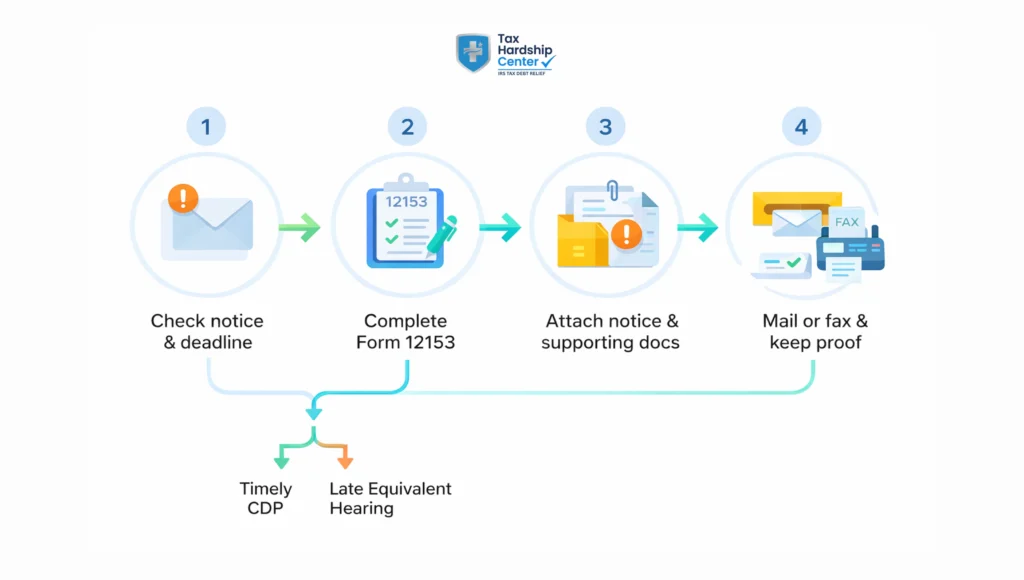

In many cases, you still have one powerful move left: requesting a Collection Due Process hearing. Filing Form 12153 on time can pause levy action in most situations and put your case in front of the IRS Independent Office of Appeals, where you can propose a payment plan, hardship status, or other resolution.

What Is Form 12153, and When Do You Need It

Form 12153 is the IRS form used to request a Collection Due Process (CDP) hearing, or an Equivalent Hearing, with the IRS Independent Office of Appeals when you receive a CDP notice under IRC 6320 (lien) or 6330 (levy).

You typically use it when you receive notices such as:

- Final Notice, Notice of Intent to Levy, and Notice of Your Right to a Hearing (often LT11 or Letter 1058).

- Notice of Federal Tax Lien Filing and Your Right to a Hearing.

If you are holding an LT11 or Letter 1058 right now, these internal guides can help you understand what the IRS is warning about and how fast the timeline moves.

CDP Hearing Vs Equivalent Hearing

Collection Due Process Hearing

A timely CDP request generally stops levy action in most cases while Appeals reviews your case, and it suspends the 10-year collection period while the CDP process runs.

It also preserves your right to go to court to challenge the Appeals’ determination, if you disagree with the outcome.

Equivalent Hearing

If you miss the timely CDP deadline, you can request an Equivalent Hearing by checking the box on the form. An Equivalent Hearing is similar, but it does not stop levy action, does not suspend the 10-year collection period, and does not give you Tax Court review rights.

Form 12153 explains the late-filing windows as:

- Lien notice: one year plus five business days from the lien filing date

- Levy notice: one year from the date of the CDP levy notice

One More Important Reality

Even if you request a CDP levy hearing, it does not prevent the IRS from filing a Notice of Federal Tax Lien.

Before You Start: Documents To Gather

Before you fill anything out, gather these items first. It will make your request cleaner and faster.

- Your CDP notice, such as LT11, Letter 1058, or the lien filing notice

- Your most recent proof of income (pay stubs, profit and loss for business owners)

- Bank statements and a basic list of monthly expenses

- Proof of payments already made, if you believe the IRS balance is wrong

- If you want a collection alternative, start assembling financial statement materials (Form 433-A for individuals, Form 433-B for businesses)

How To Fill Form 12153 Step By Step

This section follows the numbered lines on the form so you can complete it without guessing.

Line 1: Basis For Hearing Request

Check the box that matches what you received:

- Filed Notice of Federal Tax Lien

- Notice of Proposed or Actual Levy

If you received both types, the form allows you to check both boxes.

Line 2: Equivalent Hearing Box

Only check this if you might be late and still want Appeals to review the situation as an Equivalent Hearing.

If you are still within the deadline, you can leave it unchecked.

Lines 3 Through 6: Taxpayer Information

Fill in:

- Name and taxpayer identification number

- Current address

- Best phone number and best time to call

If this is a joint matter, complete Taxpayer 2’s information as well.

Line 7: Tax Information From Your Notice

This is where people waste time.

The form says you do not have to complete Line 7 if you include a copy of the notice you are appealing.

Best practice is to do both if you have room: attach the notice and fill in the basics (type of tax, form number, tax periods) so nothing gets misrouted.

Line 8: Reason You Are Requesting A Hearing

This is the most important section.

The form warns that your request will not be honored if you do not provide a reason for the dispute.

Pick the closest checkbox, then add a short explanation in plain language. Common examples:

- I Am Not Liable For The Tax The IRS Is Trying To Collect

Use this carefully. The form notes you can generally dispute the amount only if you did not receive a deficiency notice or did not otherwise have a prior opportunity for Appeals or a court to consider your dispute. - I Have Made Payments That Were Not Applied

If you paid and the IRS did not credit it correctly, list the payment date, amount, and method, and attach proof. - Financial Hardship Or Collection Alternative

If you cannot pay in full, check the hardship or collection alternative boxes and be ready to back it up with financials. - Notice Of Federal Tax Lien Withdrawal

If you are challenging a lien filing and requesting withdrawal, select it and explain why you believe it qualifies, then be prepared to provide the documentation Appeals needs.

If you need more space, the form allows you to include additional pages.

Line 9: Proposed Collection Alternative

If you are asking for a solution, select it here:

The form strongly suggests submitting a financial statement (Form 433-A or 433-B) with your request unless you meet a financial statement exception.

The IRS CDP FAQs also emphasize that if you want collection alternatives considered, Appeals will need a financial statement, and including it upfront can reduce processing time.

Line 10: Signatures And Representatives

Sign and date the form. If you are filing jointly, both taxpayers sign.

If a representative signs for you, the form says to include an executed Form 2848 unless it is already on file.

What To Attach to Form 12153

Use this checklist as your “do not forget” list.

Form 12153 Submission Checklist

| Attachments | When You Need Them |

| Copy of your CDP notice | Always, it helps route your request correctly |

| Form 433-A and or Form 433-B | If your issue is “payments not applied.” |

| Proof of payments made | If your issue is “payments not applied” |

| Proof of income and expenses | If you are claiming hardship or proposing a monthly payment |

| Supporting documents for special claims | Bankruptcy discharge info, innocent spouse request (Form 8857), lien resolution documents |

If you are proposing an Offer in Compromise or installment agreement as your alternative, remember that appeals may require you to be current on required filings and provide financial information to qualify.

Where To Fax Or Mail Form 12153

This is where many people lose time or miss the deadline.

Form 12153 instructs you to send it to the address for requesting a hearing shown on your CDP notice, not the payment address. It also tells you to include a copy of the notice to ensure proper handling.

If you are not sure of the correct address, or you want to fax your hearing request, the form says to call the phone number on the CDP notice.

Practical mailing tips that protect you:

- Use certified mail and keep the receipt

- Keep a complete copy of what you sent

- Keep proof of the date you sent it; the form explicitly tells you to do this

What Happens After You File

If your request is timely, the form explains that it will prohibit levy action in most cases and suspend the 10-year collection period until the Appeals determination becomes final.

Publication 594 states that during a CDP hearing, the IRS is generally prohibited from levying on the property at issue, and the 10-year collection period is suspended during CDP.

Your conference with Appeals may be by phone, correspondence, or in person if you qualify.

Common Mistakes That Delay Or Deny Your Request

- Sending Form 12153 to the payment address instead of the hearing request address on the notice

- Leaving Line 8 too vague, the form says the request will not be honored without a reason

- Asking for a payment plan or hardship, but not including financial statements (433-A and or 433-B)

- Trying to dispute the underlying tax amount when you already had a prior opportunity, Appeals can only consider liability in limited circumstances

- Missing the deadline, then not checking the Equivalent Hearing box, or not filing within the one-year window

FAQs

What Is Form 12153 Used For?

It is used to request a Collection Due Process or Equivalent Hearing with the IRS Independent Office of Appeals after you receive a CDP notice related to a lien or levy.

How Long Do I Have To File Form 12153?

Publication 594 explains that for proposed levies, the date is generally 30 days from the date of the letter, and your notice will show the deadline you must meet for a timely CDP request.

Where Do I Mail Or Fax Form 12153?

Mail it to the address for requesting a hearing shown on your CDP notice, not the payment address. If you want to fax, call the number on your notice or 1-800-829-1040 to confirm the correct fax number.

What Should I Write In The “Reason” Section?

Choose the most accurate checkbox and explain your issue clearly. The IRS requires a stated reason, and your request will not be honored if you provide no reason.

Do I Need To Attach Financial Forms?

If you want a collection alternative, such as an installment agreement, Offer in Compromise, or hardship status, Appeals will typically need a financial statement, and the IRS recommends including Form 433-A and/or 433-B as needed.

Does Filing Form 12153 Stop A Levy?

A timely request generally prohibits levy action in most cases while the CDP process runs, but it does not prevent the IRS from filing a Notice of Federal Tax Lien.

Conclusion

Form 12153 is not just paperwork; it is your best chance to slow things down and present a workable solution before enforced collection gets worse. If you file on time, explain your issues clearly, and attach the correct financial documents, you give Appeals what they need to review your situation and consider alternatives such as a payment plan, hardship status, or settlement.

Key Takeaways:

- File Form 12153 to request a CDP hearing after a lien or levy CDP notice, and include a copy of the notice.

- Send it to the hearing request address on the notice, not the payment address, and keep proof of when you sent it.

- A timely CDP request generally pauses levy action and suspends the 10-year collection period while the case is reviewed.

- If you want collection alternatives, include Form 433-A and/or 433-B, along with supporting documents, up front to reduce delays.

- If you miss the timely deadline, you may still request an Equivalent Hearing, but you lose levy protection and Tax Court review.