Introduction

Tax relief success is often discussed as a single outcome, yet every IRS program follows a distinct decision framework influenced by taxpayer data, financial reality, and the quality of representation. Many individuals explore tax relief options after receiving collection notices, only to encounter conflicting claims about approval rates and settlement possibilities. This creates uncertainty about what the IRS actually grants and which results are realistic. A clear explanation of the entities that shape IRS decisions helps distinguish credible pathways from unrealistic expectations.

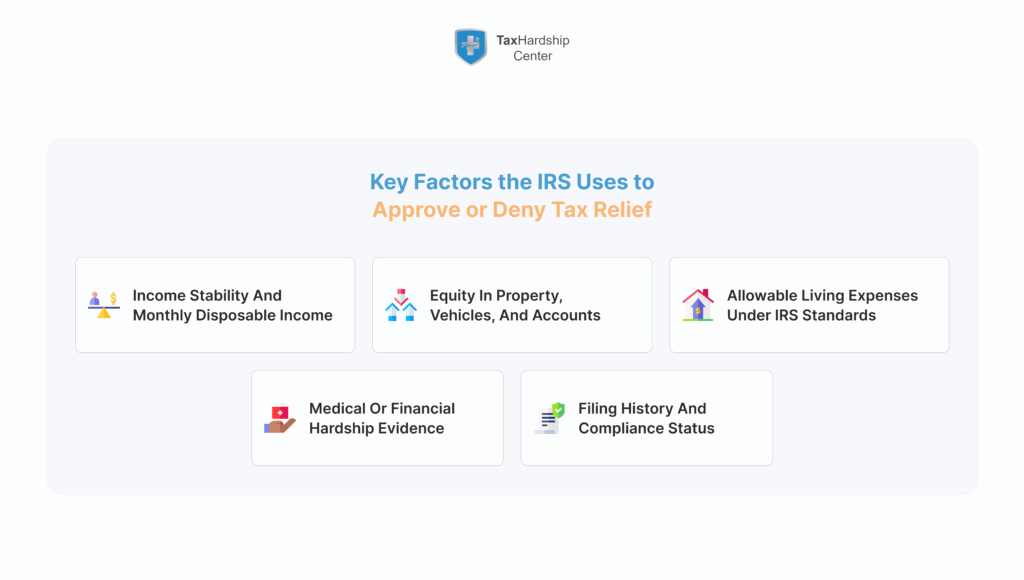

Tax relief programs operate within an interconnected structure defined by eligibility conditions, evaluation criteria, and documentation standards. The IRS does not approve requests based solely on subjective hardship declarations. Instead, approval depends on quantifiable variables such as allowable living expenses, net disposable income, asset equity, prior compliance, and the accuracy of supporting documents. These factors collectively determine the likelihood of success across programs like Offers in Compromise, penalty abatements, Currently Not Collectible status, and installment agreements.

The IRS also relies on predictable relationships between financial capacity and corrective options. When debt can be resolved through an affordable payment structure, relief programs offering reductions tend to be limited. When economic hardship is documented thoroughly and supported by verifiable evidence, approval probabilities increase. This pattern explains why many cases fail; the request does not align with the IRS’s data-driven decision rules.

Determining the probability of success becomes easier when examining the internal logic behind these programs. Each IRS decision evaluates whether the taxpayer can reasonably pay the debt within the remaining collection period. Every variable, from income stability to asset liquidity, contributes to this calculation. Relief becomes more likely when the numbers show limited repayment potential.

Tax relief firms interpret these variables to estimate potential results before submitting a request. Experienced representatives understand the IRS’s decision-making framework and prepare cases that align documented hardship with regulatory criteria. When a case aligns with these standards, success becomes far more predictable.

Understanding these relationships allows readers to form accurate expectations. Instead of viewing relief as a single outcome, it becomes clearer how each program operates, what the IRS looks for, and how taxpayer profiles influence approval rates. The following sections outline the core tax relief entities that consistently shape IRS results and explain how these forces interact within each program.

Key Takeaways

• IRS success depends on quantifiable financial variables, not generalized hardship claims.

• Each relief program operates on its own decision logic, resulting in different approval probabilities.

• Compliance history and documentation accuracy strongly influence IRS outcomes.

• Asset equity, income patterns, and allowable living expenses are core predictors of acceptance.

• Clear alignment between taxpayer data and IRS criteria produces a higher approval likelihood.

Core Tax Relief Entities That Determine IRS Success

IRS approval rates are controlled by a network of entities that interact with one another in predictable ways. Relief outcomes vary widely across programs because each program measures financial capacity and hardship using its own evaluation methods. Understanding these underlying elements helps clarify why certain taxpayers qualify for significant relief while others do not.

Several groups of entities consistently influence results:

• IRS relief programs, each with unique approval standards and evaluation steps

• Taxpayer financial variables, including income stability, expense thresholds, and asset values

• Representation quality and the structure of submitted documentation

• IRS procedural behavior, including backlog conditions and discretionary decision points

These factors interact to determine whether the IRS views a case as eligible, borderline, or unsuitable for relief. Each subsection below explores these entities in detail.

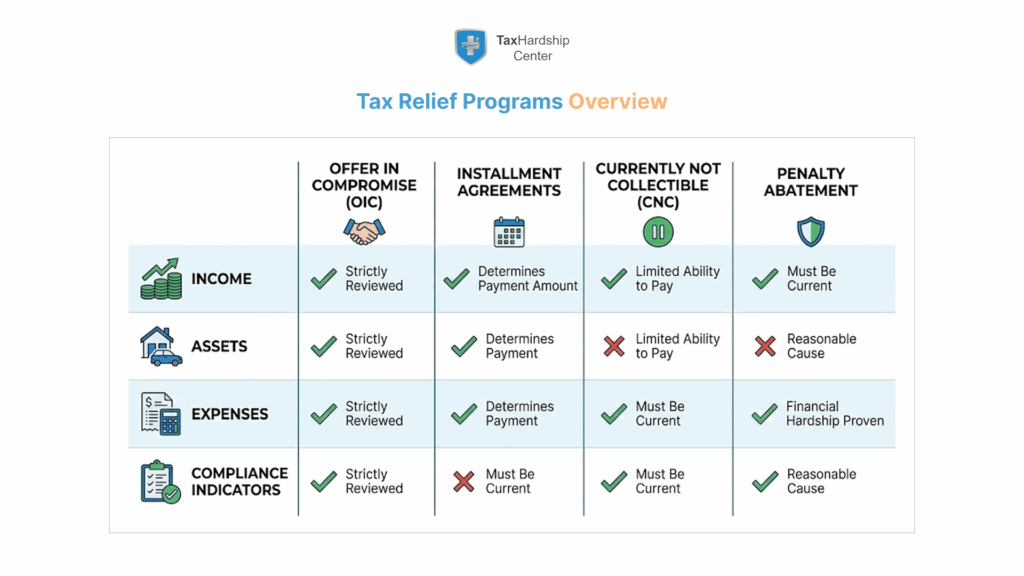

IRS Relief Programs as Distinct Entities with Separate Outcomes

Every IRS program serves a different purpose and applies its own qualification markers. For example, Offers in Compromise assess the difference between total debt and the calculated reasonable collection potential. Currently, Not Collectible status applies to short-term financial strain that prevents payment without causing economic hardship. Penalty abatement focuses on justification and historical compliance rather than ability to pay. Installment agreements evaluate whether the debt can be repaid within the remaining collection period.

These program structures create differing success rates because the IRS measures financial capacity differently in each setting. Relief is not granted based on preference; it is tied to the specific mechanism of the chosen program.

Taxpayer Financial Variables That Shape the IRS Decision

The IRS reviews financial information through a standardized lens that includes:

• Monthly income and stability

• Allowable living expenses using national and local standards

• Equity in vehicles, real estate, retirement accounts, or other property

• Outstanding debts, medical costs, and household obligations

• Historical filing and payment behavior

When these variables show limited repayment capacity, approval becomes more likely. When they suggest available funds or the capability to liquidate assets, rejection is common.

Documentation Quality, Representation Level, and Their Effect on Approval

Case outcomes often depend on how information is presented. Complete financial statements, bank records, medical documentation, and wage data must align with IRS thresholds. Experienced representatives reduce typical inconsistencies that delay or derail cases. High-quality submissions demonstrate credibility and reduce the need for follow-up requests.

How the IRS Accepts or Rejects Requests Based on Predictable Criteria

Numerical and procedural markers guide approval:

- Verification of filing compliance

- Review of financial disclosures and bank statements

- Comparison of expenses to IRS standards

- Assessment of asset liquidation potential

- Determination of reasonable collection potential

- Decision based on program guidelines

These steps create a predictable sequence that determines success. When financial data fits the program’s intended purpose, IRS acceptance becomes more likely.

IRS Success Rates by Tax Relief Program

IRS success rates vary sharply across tax relief programs because each category evaluates financial capacity and hardship under different criteria. Approval does not depend solely on the level of distress presented by a taxpayer. Instead, success arises when the requested form of relief matches the numerical thresholds the IRS uses to determine what can reasonably be collected before the statute of limitations on collections expires. As a result, each relief program reflects its own approval patterns.

Offer in Compromise requests are among the most scrutinized program types. The IRS evaluates these cases using reasonable collection potential calculations that factor in income, equity in assets, and allowable expenses. Approval becomes likely only when the numbers show that full repayment is not feasible. Many cases fail because the taxpayer’s disposable income or asset equity exceeds the threshold predicted by the IRS formula. Rejection often occurs when bank statements reveal unreported funds, when expenses surpass allowable standards, or when the documentation does not match financial disclosures.

Penalty abatement produces a very different success pattern. The IRS weighs reasonable cause, compliance history, and documented evidence of an event that disrupted the taxpayer’s ability to stay current. Cases that demonstrate medical emergencies, natural disasters, or other unexpected disruptions tend to show higher approval odds. First-time penalty abatement relies on a taxpayer’s compliance record for the three prior years, which often results in higher acceptance rates for individuals who have historically filed on time.

Currently, Not Collectible status follows a hardship-centered approach. Approval is common when verified income fails to meet the IRS’s living-cost standards. The IRS reviews bank statements, wage data, and household expenses to confirm that any payment would not compromise basic living needs. Approval rates tend to rise among individuals with limited income, high medical expenses, or unstable employment.

Installment agreements constitute the broadest category of relief because they focus on the taxpayer’s ability to repay over time. Success does not signify debt reduction; instead, it means establishing a formal payment arrangement. The IRS grants streamlined agreements when the taxpayer’s debt, income, and payment history match internal guidelines. Partial-payment installment agreements undergo more thorough analysis and depend on limited repayment capacity throughout the remaining collection window.

Innocent spouse relief displays a narrower form of success because the IRS requires strong evidence showing a lack of knowledge or participation in the understatement or nonpayment of tax. Approval increases when financial control within the household, documented separation, or relevant hardship can be demonstrated.

These outcome patterns show that tax relief success depends on the alignment between the program’s structure and the taxpayer’s financial reality. Each program’s approval probability reflects a different method of evaluating capacity, hardship, and compliance, resulting in distinct success rates.

How Taxpayer Profiles Influence Tax Relief Success

Taxpayer profiles play a central role in determining eligibility for tax relief outcomes, as the IRS evaluates each case using numerical indicators that reflect the actual repayment potential. Income levels, expense structures, debt characteristics, and compliance records interact in predictable ways. These elements form the foundation of IRS risk assessment and influence whether a case is accepted or rejected.

Income is a core predictor. Stable wages, consistent business revenue, or predictable retirement income often reduce the likelihood of relief through debt reductions, unless allowable expenses offset the income. Low or fluctuating income increases the probability of hardship-based outcomes, primarily when supported by recent pay stubs, profit-and-loss statements, or unemployment records.

Allowable living expenses represent another decisive component. The IRS uses national and local standards to determine reasonable costs for food, housing, transportation, and other essentials. When a household’s actual expenses exceed these standards, the IRS often recalculates the figures downward unless documented necessity can be demonstrated. A profile showing expenses above IRS standards faces reduced approval odds unless exceptional circumstances apply.

Asset structure strongly affects success rates. Home equity, vehicle value, retirement accounts, and other assets influence the IRS view of repayment potential. Taxpayers with significant equity typically face lower approval rates for settlement-based programs because liquidation or borrowing appears feasible. Profiles with limited or no liquid assets align more closely with programs like Currently Not Collectible or Offer in Compromise.

Compliance history functions as a gatekeeping factor. The IRS rarely grants significant relief to taxpayers with unfiled returns, inconsistent payment behavior, or unresolved errors in prior filings. Profiles showing consistent compliance face fewer procedural hurdles and typically experience higher approval rates.

Debt size and age also contribute to IRS decisions. Larger debts with limited remaining collection periods may prompt the IRS to consider settlement options. Smaller debts with long collection timelines often lead to installment agreements rather than reduction programs.

Below is a structured view of how profile characteristics affect outcomes:

| Profile Component | Typical IRS Interpretation | Effect on Success |

| Low income with essential expenses | Limited repayment capacity | Higher relief approval |

| High income and low expenses | Strong payment potential | Lower settlement approval |

| High asset equity | Liquidity available | Frequent rejections |

| Consistent filing record | Lower compliance risk | Greater acceptance |

| Short time left on the collection statute | Limited recovery time | More settlement consideration |

These interactions show that approval patterns stem from the alignment of taxpayer characteristics with IRS standards. Profiles that demonstrate verifiable hardship and limited repayment capacity consistently show higher success probabilities.

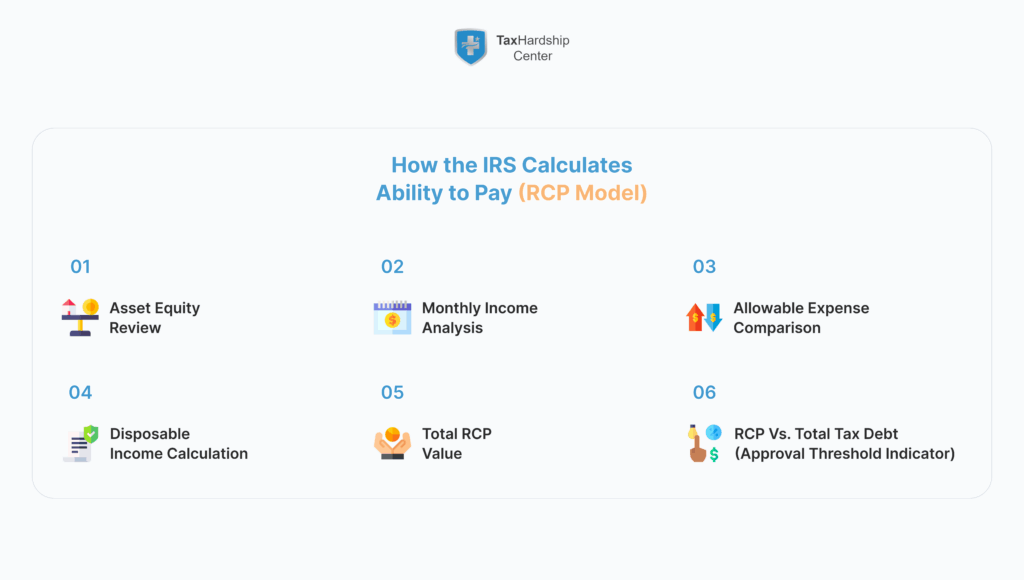

How IRS Evaluates Ability to Pay Using Reasonable Collection Potential

Reasonable collection potential (RCP) operates as one of the foundational metrics the IRS uses when considering relief requests, especially settlement programs. This calculation reflects the amount the IRS can reasonably expect to collect before the statute of limitations expires. RCP shapes decisions for Offers in Compromise and influences the level of scrutiny applied to payment plans, hardship claims, and collection pauses.

RCP begins with an asset evaluation. The IRS reviews tangible and intangible holdings, including real estate, vehicles, bank accounts, investments, and retirement funds. Each category is assigned a realizable value based on equity calculations and liquidation assumptions. When asset equity exceeds tax debt, settlement-based programs are usually rejected because the IRS views liquidation or borrowing as feasible.

Next, the IRS analyzes income. Monthly earnings, business revenue, pensions, and other income sources are reviewed through historical patterns. Fluctuations in business income, seasonal work cycles, or recent job loss may reduce income projections, while stable wage employment often increases expected capacity.

Allowable expenses form the third component. The IRS applies standardized limits to essential categories. Taxpayers whose expenses fall within or below these standards are assessed more favorably for hardship outcomes. Expenses above standards are adjusted downward unless a documented necessity can be shown. Medical costs, dependent care, and specific business expenses may qualify for additional consideration.

The IRS constructs RCP using the following structure:

- Determine equity in assets after subtracting encumbrances.

- Calculate monthly income minus allowable living expenses.

- Multiply the resulting monthly disposable income by a program-specific number of months.

- Add the disposable-income projection to asset equity to form the total RCP.

- Compare the figure to the total tax liability.

When RCP exceeds the tax debt, relief programs aimed at reducing liability face significant hurdles. When RCP falls below the debt or approaches zero, settlement-based relief becomes more plausible.

RCP also affects installment agreements. Taxpayers with moderate disposable income but limited assets may be placed in partial payment installment agreements, while those with higher disposable income are directed into full-payment arrangements.

Documentation heavily influences each step. Bank statements reveal cash flow, while wage records and financial statements verify earnings. Expense claims must match receipts or invoices to satisfy the IRS.

RCP acts as a predictive indicator of tax relief success because it quantifies the ability to pay in a standardized format. Cases supported by clear evidence and financial patterns aligned with hardship frameworks tend to achieve stronger outcomes across programs.

Patterns Observed in IRS Decision Behavior

IRS decision behavior follows recognizable patterns influenced by economic conditions, internal workload, risk assessment protocols, and the timing of tax debt within the collection period. While each case receives an individualized review, observable trends appear in approval data over time. These patterns help clarify why relief becomes more achievable in specific scenarios and more restrictive in others.

Economic downturns often correspond with elevated acceptance rates for hardship-based programs. During periods of widespread unemployment, reduced small-business revenue, or sharp increases in essential living costs, IRS reviewers tend to observe a higher volume of cases that legitimately fall within hardship categories. When financial statements confirm decreases in income or increases in unavoidable expenses, approvals for Currently Not Collectible status and certain penalty abatements tend to rise. These patterns reflect the IRS preference for realistic collection assessments rather than aggressive pursuit of uncollectible debts.

Backlog conditions also influence procedural behavior. High case volume may lead to extended timelines, but it can also increase the likelihood of decisions that prioritize efficient resolution. This is particularly noticeable in installment agreements, where straightforward cases receive faster approval when documentation is complete. Cases involving complex asset structures or inconsistencies may experience longer delays, reinforcing the importance of clean, accurate submissions.

Cases approaching the Collection Statute Expiration Date (CSED) display another pattern. When the remaining collection window narrows, the IRS evaluates whether full recovery is plausible. If the taxpayer’s income and assets cannot support repayment within the limited timeframe, settlement programs may become more viable. This does not guarantee approval, but the combination of limited time and limited ability to pay often strengthens the argument for compromise outcomes.

Documented medical hardship consistently correlates with higher approval rates for both CNC status and penalty relief. Medical records showing chronic conditions, permanent disability, or recent major medical expenses signal unavoidable financial strain. When expense patterns align with IRS hardship criteria, decisions tend to favor the taxpayer.

Red flags frequently trigger faster rejection. These include undisclosed bank accounts, unexplained cash deposits, expenses significantly above IRS standards without supporting documentation, or inconsistent income claims between pay stubs and tax returns. Patterns of noncompliance in prior years may also negatively shape outcomes. IRS reviewers use these markers to assess risk, reliability, and overall credibility of the request.

These observable trends demonstrate that a blend of financial logic, timeline constraints, documentation clarity, and the broader economic environment shapes IRS behavior. Understanding these patterns helps clarify when relief efforts align with the IRS’s decision-making structure and when they face substantial resistance.

Claims Commonly Made by Tax Relief Firms vs. Outcomes Achievable in Reality

Marketing messages from tax relief firms often present simplified promises that do not match the structure of actual IRS relief programs. These claims can create unrealistic expectations by conflating different program outcomes or presenting rare results as everyday experiences. Distinguishing promotional language from the IRS’s documented processes helps clarify what success truly means.

Some firms promote the idea that most taxpayers qualify for broad settlement reductions through the Offer in Compromise program. In practice, the IRS relies on RCP calculations that restrict eligibility to individuals with verifiable financial limitations. High income, steady wages, or significant assets frequently disqualify applicants. Settlement approval is not driven by persuasive negotiation but by the numerical alignment between debt and capacity.

Certain firms frame “success” in ways that do not reflect meaningful relief. For example, receiving acknowledgement that a case has been opened or securing a short-term pause in collections may be labeled as substantial progress. While these steps have procedural value, they do not change the underlying liability. In other cases, firms may highlight payment plan approvals as evidence of special negotiation skills, even though many installment agreements follow preset IRS guidelines.

Another area of misrepresentation involves penalty abatement. Some firms imply that penalties can be removed in most cases, regardless of the filing history or cause. Actual approval depends heavily on prior compliance and documented evidence demonstrating reasonable cause, such as natural disasters, serious illness, or unavoidable circumstances. Without these elements, penalties typically remain in place.

Comparison between marketing claims and actual IRS outcomes can be summarized in the table below:

| Marketing Claim | IRS Reality | Typical Outcome |

| “Most taxpayers qualify for large settlements” | RCP restricts eligibility | Limited to verified hardship cases |

| “Negotiation can eliminate penalties easily” | Requires documented reasonable cause | Moderate approval for those with evidence |

| “Installment plans are special deals” | Based on strict eligibility rules | Common approval but not a unique concession |

| “Case acceptance equals success” | Acceptance only begins review | No guarantee of relief |

Reputable firms avoid overselling outcomes and instead focus on aligning taxpayer data with IRS criteria. Organizations that emphasize compliance restoration, precise documentation, and realistic expectations tend to produce more reliable results. Firms such as Tax Hardship Center use structured evaluations to determine whether a taxpayer’s financial profile meets the requirements for each program. This reduces the likelihood of submitting cases with minimal approval potential.

Understanding the distinction between promotional language and IRS decision-making processes helps taxpayers identify credible relief options and avoid unrealistic promises.

Representation Quality and Its Impact on IRS Success

Representation quality plays a significant role in IRS relief outcomes because it determines how effectively financial data is organized, documented, and presented. IRS reviewers rely on clear, consistent information. Submissions that demonstrate accuracy and transparency tend to move through the process more smoothly, while disorganized filings often lead to delays, additional information requests, or denials.

Different types of representatives contribute varying strengths. Enrolled Agents specialize in federal tax matters and handle the majority of IRS negotiation work for individuals. Their familiarity with procedural rules and submission formats helps prevent errors that undermine relief requests. Attorneys provide support in cases involving legal disputes, complex liabilities, or confidential matters. CPAs offer strong insight into income verification and financial structure, but may be less involved in negotiation unless they specialize in tax resolution.

Representation affects the RCP process directly. Experienced professionals understand how to document asset values correctly, present necessary expense justifications, and clarify financial inconsistencies before the IRS identifies them as red flags. This reduces the likelihood of misinterpretation and supports a more accurate assessment of economic hardship.

Documentation quality influences IRS perception of credibility. Incomplete forms, inconsistent bank statement entries, or unexplained transfers frequently raise concerns about financial transparency. Skilled representatives compile records that align cleanly with disclosures, reducing the risk of rejection due to avoidable discrepancies.

Key elements influenced by representation quality include:

• Accuracy of income reporting

• Proper classification of allowable expenses

• Correct valuation of assets

• Explanation of unusual financial activity

• Timeliness of responses to IRS requests

• Consistency between statements, returns, and supporting evidence

Representation also plays a predictive role in success rates. Cases prepared by experienced practitioners tend to produce fewer errors, which reduces the likelihood of procedural rejection before the IRS evaluates eligibility. When representatives anticipate potential challenges, they prepare additional evidence to support hardship claims and preempt IRS objections.

Organizations such as Tax Hardship Center use structured processes to review financial information and align it with IRS criteria. This includes detailed intake evaluations, analysis of income and expense ratios, and preparation of documentation that satisfies IRS formatting expectations. These steps ensure that each case is supported by coherent financial data and presented in accordance with IRS guidelines.

Representation quality reinforces the relationship between financial evidence and IRS decision-making. When economic data is organized effectively and supported by comprehensive documentation, relief outcomes become more predictable, and the likelihood of approval across multiple programs increases.

When Tax Relief Success Is Impossible: IRS Conditions That Block Approval

Certain financial and compliance conditions create significant barriers to approval of tax relief because the IRS bases its decisions on verifiable capacity, documented hardship, and historical behavior. When a case does not align with the structural logic of relief programs, approval becomes virtually unattainable. These conditions reflect the IRS’s responsibility to protect federal revenue while applying relief only to individuals who cannot genuinely repay.

High disposable income remains one of the most common barriers. When monthly earnings exceed allowable living expenses by a substantial margin, the IRS calculates the disposable income available to satisfy the liability. In these situations, installment agreements often become the default option. Settlement-based programs such as Offers in Compromise fail because the IRS views consistent disposable income as evidence that repayment is feasible.

Another major obstacle arises when asset equity exceeds tax debt. Equity in real estate, vehicles, investment accounts, and retirement funds signals repayment potential through liquidation or borrowing. Even if the taxpayer prefers not to liquidate, the IRS uses asset value as a measurable indicator of financial capacity. Relief requests that contradict these valuations are typically rejected. In some cases, taxpayers with substantial real estate equity may qualify for installment agreements, but settlement-based programs rarely succeed.

Noncompliance also blocks approval. Missing returns, unfiled years, late filings, and inconsistent tax reporting undermine credibility and prevent the IRS from evaluating full liability. The IRS requires all tax years to be filed before considering relief. Cases developed without full compliance stall until filing obligations are met. Long-term noncompliance also signals risk, intensifying scrutiny of financial claims and reducing the likelihood of favorable outcomes.

Cases involving luxury spending, unexplained cash flow, or significant discretionary expenses face further challenges. IRS reviewers compare living costs to national and local standards. Expenditures that exceed these limits without documentation of necessity undermine claims of hardship. Patterns of discretionary spending on nonessential items during periods of alleged hardship often lead to denial.

The presence of recent asset transfers or attempts to shield resources through informal arrangements also reduces approval potential. Transfers to relatives, undervalued sales, or sudden withdrawals raise credibility concerns and may prompt the IRS to request additional records or result in a direct rejection. These patterns suggest an ability to pay or an attempt to avoid collection.

Below is a structured overview of conditions that frequently block relief:

• High disposable income under IRS standards

• Significant home or vehicle equity

• Unfiled returns or inconsistent compliance

• Large discretionary expenses unsupported by documentation

• Asset transfers that reduce visible equity

• Bank records showing unexplained deposits or withdrawals

Approval becomes impossible when the financial data conflicts with the IRS’s evaluation structure. Relief programs rely on clear demonstration of hardship and limited repayment capability, and cases that contradict these indicators rarely progress.

THC’s Role in Structuring Cases for Higher Success Probability

The Tax Hardship Center applies structured case-preparation processes that align taxpayer information with IRS decision frameworks. This alignment increases the likelihood of achieving relief outcomes that meet program standards. The approach centers on reviewing financial data, identifying eligibility markers, and organizing documentation to reflect the IRS guidelines that shape approval decisions.

Case development begins with a review of income, assets, and expenses. Analysts examine wage records, business earnings, and household financial activity to determine whether the taxpayer’s profile fits the characteristics the IRS considers indicative of hardship. Evidence such as medical bills, employment interruptions, dependent care needs, or significant shifts in income is evaluated to determine its relevance to IRS criteria.

THC reviews allowable expenses using national and local standards. When expenses exceed these thresholds, the team identifies areas requiring documentation or clarification. Cases involving unusual costs, such as long-term medical treatment or care for dependents with disabilities, require detailed evidence to justify deviations from standard expense limits. Properly structuring these records helps ensure the IRS recognizes their validity.

Asset analysis forms another core component. THC examines home equity, vehicle value, retirement accounts, and other property to determine whether asset equity aligns with settlement opportunities or points toward payment arrangements. When assets create approval barriers, representatives identify program types that remain viable under IRS rules.

Documentation completeness strongly influences IRS decision-making. THS prepares tax transcripts, financial statements, bank summaries, and supporting materials in formats that correspond with IRS expectations. Conflicting data across statements, returns, and records is reconciled before submission to prevent procedural delays.

The case strategy also incorporates IRS behavioral patterns. Analysts determine whether a taxpayer’s debt is approaching the collection statute expiration date, whether income fluctuations support hardship arguments, and whether medical or employment records enhance the evidence for reduced collection potential. These factors shape the direction of the relief request.

Below is a structured overview of THC’s case preparation elements:

• Review of all income sources and earnings patterns

• Evaluation of expenses under IRS standards

• Asset valuation aligned with IRS equity calculations

• Organization of medical, employment, and household records

• Correction of inconsistencies across statements and filings

• Preparation of forms and supporting documents in IRS-compliant formats

Tax Hardship Center’s role focuses on ensuring that each case reflects accurate financial data that matches IRS criteria. Alignment between taxpayer circumstances and program standards increases the predictability of relief outcomes and reduces procedural obstacles during review.

Conclusion

IRS tax relief success depends on measurable financial conditions, compliance accuracy, and the alignment between a taxpayer’s circumstances and program-specific decision frameworks. Each relief category evaluates hardship, income capacity, asset structure, and expense patterns in different ways, producing distinct approval rates across programs. Relief becomes more attainable when financial records support limited repayment capacity or document disruptions such as medical hardship, business decline, or unexpected life changes.

Predictable IRS patterns also influence outcomes. Cases prepared with complete documentation and consistent financial evidence progress more smoothly. Those involving high disposable income, significant equity, or compliance gaps face structural barriers regardless of personal hardship claims. Representation quality also shapes outcomes by determining how effectively financial data is presented, how inconsistencies are resolved, and how closely submissions reflect IRS standards.

Tax Hardship Center contributes by examining financial information through the same analytical lens used by IRS reviewers. Structured preparation, organized documentation, and thorough compliance review ensure cases are presented in a manner consistent with regulatory expectations.

Understanding the numeric and procedural foundations of IRS decision-making brings clarity to the tax relief landscape. Approval is neither arbitrary nor unpredictable; it follows defined rules based on ability to pay, documented hardship, and compliance reliability. When taxpayer information aligns with these rules, relief outcomes become far more realistic and achievable.

FAQ’s

1. What financial documents does the IRS consider most important during relief evaluations?

The IRS prioritizes documents that verify income, expenses, and asset values. Wage statements, business revenue reports, bank statements, mortgage ledgers, medical bills, and proofs of insurance form the core evidence set. Consistency across these records carries significant weight. When financial disclosures align with documented activity, IRS reviewers can accurately assess hardship. Inconsistencies or omissions often lead to additional information requests or early rejection.

2. Do self-employed individuals face different IRS relief approval challenges?

Self-employed taxpayers often face heightened scrutiny because income can fluctuate and documentation may be less standardized. The IRS examines profit-and-loss statements, bank activity, outstanding invoices, and historical revenue patterns to determine capacity. Those with irregular earnings or recently declining revenues may align more closely with hardship programs, while those with strong business cash flow face stricter RCP calculations.

3. How far back does the IRS review financial behavior when assessing relief eligibility?

IRS reviewers typically analyze recent bank statements, income records, and filings over the previous 12 months. However, patterns from multiple years may influence the assessment when evaluating compliance history, business stability, or past penalties. Long-term inconsistencies, such as habitual late filing, may diminish approval prospects, while consistent filing records strengthen credibility.

4. Can the IRS reverse a relief approval if financial circumstances change later?

Certain forms of relief remain subject to ongoing evaluation. Installment agreements, partial payment arrangements, and Currently Not Collectible status can be reassessed if income rises or expenses decrease. The IRS may request updated financial information and adjust the arrangement accordingly. Offers in Compromise follow stricter rules: once completed and upheld for the required compliance period, settlement terms generally remain final.

5. What happens if the IRS identifies omitted income or unreported assets during the review?

Discovery of unreported income, property, or large unexplained deposits often triggers deeper investigation and significantly lowers approval likelihood. The IRS may request supplemental records, conduct compliance checks, or classify the case as higher risk. Relief programs rely heavily on financial transparency, so undisclosed resources can lead to immediate rejection or further review of earlier tax years.