Introduction

IRS tax relief programs are government-authorized solutions designed to resolve unpaid tax debt, enforcement actions, and financial hardship. Taxpayers facing escalating notices, penalties, levies, or wage garnishments can seek relief through settlements, payment plans, hardship status, or penalty removal. Eligibility is based on income, essential expenses, assets, and overall ability to pay.

As financial strain and inconsistent income become more common, demand for qualified representation has grown. Tax Hardship Center supports taxpayers by managing communication, documentation, and IRS-required financial reviews. Programs like Offer in Compromise and Currently Not Collectible rely on strict formulas, making accurate financial modeling essential.

The firm’s services include transcript analysis, hardship verification, and preparation of required forms to ensure submissions align with IRS standards. Since IRS systems frequently update accounts and may request clarification, proper representation helps avoid delays and directs cases toward the right relief option.

Many taxpayers struggle with self-resolution due to expense limits, asset valuation rules, or confusion over IRS notices. Each relief program has specific criteria that require detailed evaluation to determine realistic outcomes.

Understanding IRS procedures and financial standards allows taxpayers to make informed decisions and choose representation capable of navigating the system effectively.

Key Takeaways

- IRS tax relief services address unpaid tax liabilities, penalties, and enforcement actions through structured programs.

- Approval depends on IRS assessments of income, assets, and allowable expenses.

- Tax Hardship Center conducts transcript analysis, financial modeling, and IRS negotiation.

- Settlement and hardship programs require precise documentation and compliance history.

- IRS reviews may include requests for additional proof, especially for inconsistent or incomplete financial records.

IRS Tax Relief Services at THC

IRS tax relief services represent a defined set of programs that respond to tax debt accumulation, enforcement escalation, and verified economic hardship. These services operate under standardized eligibility rules and documentation requirements that enable the IRS to assess a taxpayer’s financial capacity. Relief options address liabilities through settlement, partial repayment, structured installment arrangements, or enforcement suspension.

The IRS relies on several internal systems to categorize taxpayer accounts. Each system updates balance details, assesses penalties, and determines when collection activity becomes necessary. A case may shift between automated systems and manual assignment depending on the size of the debt, compliance gaps, or perceived collection potential. These transitions influence the timing of notices, liens, levies, and available pathways to relief.

Several conditions typically create the need for IRS intervention:

- Unfiled tax returns that generate substitute assessments

- Unpaid balances that continue to grow with monthly penalties

- Income changes that prevent timely payment

- Unresolved payroll or self-employment tax liabilities

- IRS detection of underreported income

Relief programs operate as structured responses to these issues. Their design is based on financial evaluation standards that determine what a taxpayer can realistically repay without compromising basic living needs. The agency uses a formula-driven approach that accounts for net monthly income, equity in assets, household size, and regional expense limits.

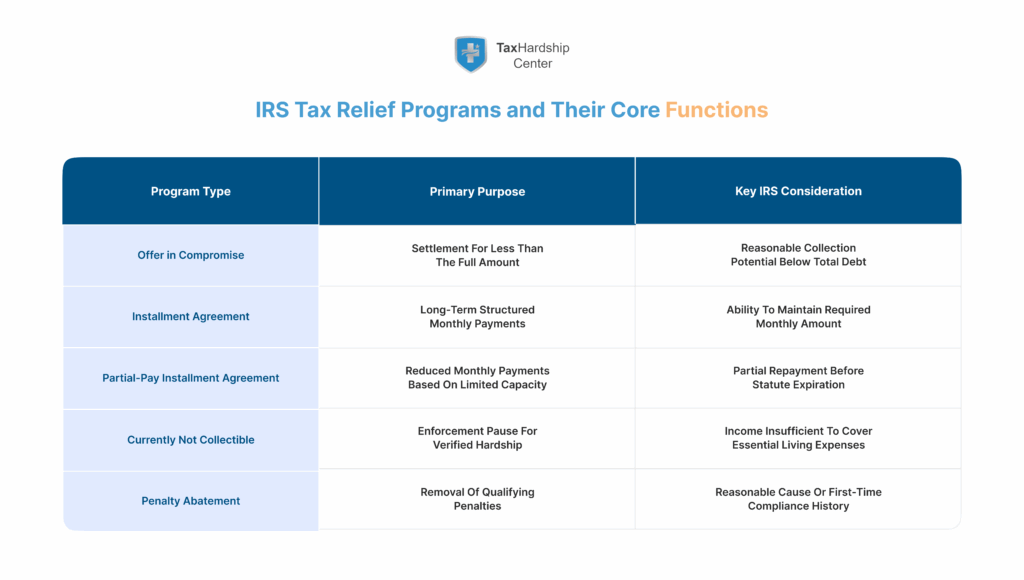

A summary of the main IRS relief categories is shown below:

| Relief Program | Primary Purpose | Key Eligibility Factor |

| Offer in Compromise | Settlement for less than owed | Low reasonable collection potential |

| Installment Agreement | Long-term repayment | Ability to maintain monthly payments |

| Partial Pay IA | Reduced the monthly payment | Partial ability to pay before statute expires |

| Currently Not Collectible | Temporary suspension | Verified financial hardship |

| Penalty Abatement | Penalty removal | Reasonable cause or clean compliance history |

These programs provide structured mechanisms for resolving tax debt while balancing taxpayer needs and government interests. Their effectiveness depends on accurate representation of financial hardship, proper documentation, and compliance with filing requirements.

Tax Hardship Center as a Professional IRS Negotiation Provider

Tax Hardship Center functions as a licensed tax resolution provider, managing communication with the IRS, interpreting financial records, and preparing required documentation for relief programs. Representation begins with an authorization process using Form 2848, which grants permission to communicate directly with IRS collections or examination units. Once authorized, the firm can request transcripts, secure case information, and clarify the status of liens, levies, or pending enforcement actions.

A structured analysis of IRS transcripts forms the basis of the firm’s initial assessment. Transcripts outline account balances, prior filings, adjustments, and entries that indicate upcoming collection activity. Specific codes signal risks such as pending levy issuance, collection assignment, or additional penalty computation. The firm interprets these codes to determine the most suitable relief pathway and to ensure a timely response before enforcement escalates.

Hardship evaluation requires detailed financial documentation. IRS relief programs rely heavily on Form 433 series statements, which calculate the taxpayer’s ability to pay using allowable expense standards. Tax Hardship Center gathers information on household expenses, income fluctuations, secured debt, and asset values. These inputs shape the reasonable collection potential calculation, which determines eligibility for settlement or hardship status.

The firm’s negotiation process involves communication with IRS employees assigned to the case. Representatives address missing documentation, clarify inconsistencies, and present verified financial evidence. Since IRS systems periodically request supplementary proof, the ability to respond without error can influence the outcome. Accurate representation also reduces the likelihood of case delays or rejection due to incomplete forms.

Tax Hardship Center’s role includes:

- Verification of account balances through IRS transcripts.

- Identification of unfiled returns and required compliance steps.

- Preparation of financial statements consistent with IRS standards.

- Submission of relief proposals through accepted communication channels.

- Follow up with assigned agents until a decision is reached.

This structure ensures that each case is evaluated within IRS parameters and presented with the documentation needed to support settlement or hardship consideration.

IRS Tax Debt Resolution Programs and Their Eligibility

IRS tax relief programs operate within a structured system that categorizes financial capacity and identifies the most appropriate resolution for each case. A single factor does not determine eligibility; instead, it emerges from a combination of income behavior, household expenses, asset equity, and compliance history. The IRS reviews these inputs through standardized financial documentation, transcript data, and internal scoring models. Each relief pathway aligns with different economic conditions, making program selection dependent on the relationship between income and realistic repayment potential.

The Offer in Compromise serves as a settlement mechanism for taxpayers whose reasonable collection potential falls short of the total debt owed. This calculation measures disposable income after allowable expenses and includes a review of liquid assets, secured property, and equity holdings. When the IRS determines that full repayment falls outside realistic capability, an OIC may be accepted. Factors such as medical hardship, unemployment history, or significant income reduction often influence the calculation and strengthen the case when documented correctly.

Installment Agreements serve as structured repayment plans. Some are streamlined, requiring no financial statement for balances below specific thresholds, while others demand detailed documentation. The IRS evaluates whether a household can support a monthly payment without compromising essential living needs. Variants such as the partial-pay installment agreement address cases where partial repayment is possible but cannot satisfy the full debt before the collection statute expires.

Currently Not Collectible status addresses verified hardship. When documentation confirms that income does not cover basic living costs, the IRS may suspend collection activity. Although the debt remains active, levies and garnishments are suspended, and no payments are required during the hardship period. Annual or periodic reviews may occur if IRS systems detect changes in income or household composition.

Penalty abatement is an additional form of relief available to taxpayers who meet reasonable cause criteria or maintain a clean compliance history. Circumstances such as natural disasters, significant illness, or unavoidable financial disruption may support abatement requests. The IRS examines documented timelines to determine whether penalties should be removed.

A comparative summary appears below:

| Program Type | Primary User Scenario | Key Documentation |

| Offer in Compromise | Inability to repay full debt | Form 433-A(OIC), asset valuation |

| Installment Agreement | Ability to repay over time | Income verification, expenses |

| Partial-Pay IA | Limited repayment ability | Detailed financials |

| CNC Status | Confirmed hardship | Form 433-F |

| Penalty Abatement | Reasonable cause | Supporting records |

These programs operate through defined criteria that require consistent documentation, accurate financial modeling, and clear evidence supporting the proposed form of relief.

IRS Evaluation Systems That Affect Relief Approval

IRS approval processes rely on internal systems that interpret financial statements, calculate allowable expenses, and categorize the potential for collection. These systems influence relief outcomes by shaping how income, assets, and expenditures are weighted. Understanding this structure clarifies why some applications are accepted, delayed, or denied.

The IRS Collection Financial Standards define the maximum amounts allowed for categories such as housing, transportation, food, and healthcare. These standards vary by location. When expenses exceed these ranges, additional proof may be required. This framework ensures that relief decisions remain consistent across cases while still allowing consideration of documented exceptions.

Financial evaluation also involves asset review. The IRS examines bank balances, real estate equity, vehicle value, retirement accounts, and business property. Not all assets are treated equally. For example, a primary vehicle used for work may be evaluated differently from a secondary vehicle. Homestead property may also receive equity exclusions under specific circumstances. These distinctions shape the outcome of settlement requests and determine whether monthly payments must be adjusted.

The IRS uses sequential decision patterns that guide relief selection. These decision trees analyze the relationship between disposable income and total debt. If disposable income supports a full-pay agreement within the statute period, settlement is unlikely. If equity alone covers a substantial portion of the debt, settlement also becomes less probable. When both income and equity are insufficient, programs such as CNC or OIC may be appropriate.

Financial statements submitted through Form 433 series documents must align with transcript entries to demonstrate accuracy. IRS employees compare monthly earnings reported by employers, income tax return entries, and bank activity to validate financial claims. Inconsistencies may result in requests for clarification or updated statements.

A simplified view of IRS evaluation criteria includes:

- Household income stability and fluctuation

- Regional living expense standards

- Asset liquidity and equity

- Debt-to-income ratios

- Risk indicators in transcripts

- Compliance with filing and payment obligations

These elements form the structure that determines relief approval. Each factor interacts with the others, creating a comprehensive evaluation that reflects both financial limitations and IRS collection priorities.

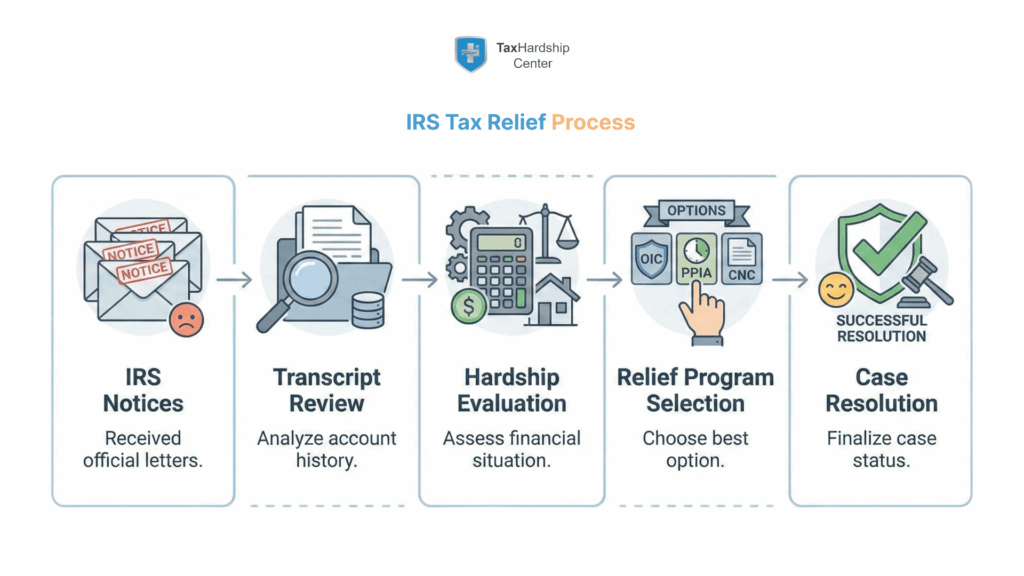

Tax Hardship Center’s Process for Resolving IRS Tax Debt

Tax Hardship Center follows a structured process that aligns with IRS expectations for accurate documentation, financial verification, and timely communication. Each case begins with an authorization step that permits the firm to secure transcript records and determine the precise status of the taxpayer’s account. These transcripts reveal unfiled returns, penalty accrual patterns, previous installment attempts, and indicators of pending enforcement. This early diagnostic step establishes the foundation for selecting the appropriate rehttps://www.taxhardshipcenter.com/lief pathway.

A detailed compliance review plays a significant role in the firm’s approach. IRS systems require all missing returns to be filed before most relief programs are considered. The Tax Hardship Center evaluates the filing history and prepares any necessary returns to ensure the case meets IRS standards. This step helps prevent the agency from rejecting a relief request on procedural grounds and positions the case for accurate financial assessment.

Hardship modeling begins once compliance requirements are met. This stage involves analyzing income behavior, verifying allowable living expenses, and documenting secured debts. The IRS relies on the Form 433 series to determine whether an individual can repay debt in full, repay it partially, or qualify for relief due to hardship. Tax Hardship Center organizes financial records into a structure that corresponds to IRS evaluation rules. Expense categories are reviewed in accordance with regional standards, while assets are valued to determine whether equity affects settlement calculations.

The firm prepares a proposal reflecting the relief program best suited to the individual’s financial profile. Representation includes direct communication with IRS employees responsible for reviewing financial data or processing the specific relief request. The firm responds to clarification requests, updates financial documents when necessary, and monitors transcript changes to confirm that enforcement actions remain paused during review.

A simplified view of the process includes:

- Authorization and transcript retrieval.

- Compliance review and preparation of missing returns.

- Financial documentation and hardship modeling.

- Preparation and submission of a relief proposal.

- Ongoing communication with IRS personnel.

- Monitoring of case status until a final decision is reached.

Tax Hardship Center’s process emphasizes accuracy, timely response to IRS inquiries, and adherence to the documentation standards that shape settlement and hardship determinations.

IRS Enforcement Actions and How Relief Reverses Them

IRS enforcement measures are designed to protect federal revenue when tax debt remains unpaid. These actions escalate when accounts show persistent delinquency or when income patterns suggest an ability to pay. Relief programs function not only as debt resolution mechanisms but also as tools to halt or reverse these enforcement measures when financial documentation supports the request.

Federal tax liens represent a common enforcement action. A lien establishes a legal claim against property to secure the tax debt. Relief programs such as installment agreements and certain hardship statuses can prevent additional lien filings. In some situations, lien withdrawal may be possible when the taxpayer enters into a qualifying payment arrangement or demonstrates that the lien negatively influences the potential for repayment.

Wage garnishment occurs when the IRS instructs an employer to withhold a portion of earnings to satisfy the debt. Garnishment typically follows multiple notices and may continue until the balance is resolved. Relief programs can stop garnishments once hardship is documented or an installment agreement is approved. The IRS reviews income and expense data before releasing the garnishment to ensure the action does not create an unsustainable financial burden.

Bank levies function as one-time actions that seize available funds on the date the levy is issued. These levies often occur when the IRS identifies recent deposit activity or detects nonresponsive behavior. Relief programs can prevent future levies if the taxpayer demonstrates hardship, agrees to it, or secures CNC status. Lost funds from a completed levy are rarely returned unless procedural errors occurred.

Passport restrictions apply to individuals with seriously delinquent tax debt as defined by IRS thresholds. Once relief is approved, the IRS certifies the change to the Department of State, lifting the restriction. This process does not require additional negotiation once the IRS confirms eligibility.

The connection between enforcement actions and relief programs can be summarized as follows:

| Enforcement Action | Trigger | Method of Reversal |

| Federal Tax Lien | Sustained delinquency | Installment agreement, lien withdrawal |

| Wage Garnishment | Nonpayment with verified income | Hardship approval, payment agreement |

| Bank Levy | Unresolved balance and recent deposits | Relief approval before future levies |

| Passport Restriction | High certified balance | Relief program acceptance |

Documented financial conditions influence these enforcement measures. Relief programs serve as structured pathways to stop or reverse these actions when IRS standards are met.

Indicators That IRS Tax Relief Services Are Needed

Several financial and procedural indicators suggest that an individual may require IRS tax relief services. These indicators derive from transcript entries, IRS notice patterns, penalty behavior, and household financial strain. Recognizing these signs early helps avoid more severe enforcement actions.

Long-term delinquency indicators appear in IRS transcripts when returns remain unfiled or balances continue to accumulate without payment. Codes may indicate a substitute for return assessments, repeated penalty additions, or movement between automated collection stages. These entries signal that the account is at risk of lien filing or levy escalation.

Increasing penalties often indicate worsening account health. The IRS applies failure-to-file and failure-to-pay penalties monthly. When penalties grow faster than any payments applied to the balance, the debt can become unmanageable. Relief programs such as abatement or settlement may be necessary to prevent further financial decline.

IRS notices provide clear signals:

- CP14 indicates an initial balance.

- CP501 and CP503 show early collection activity.

- CP504 signals intent to levy specific property.

- LT11 or Letter 1058 communicates final intent to levy.

- Notice of Federal Tax Lien confirms lien filing.

These notices align with escalating collection behavior. Once final intent notices arrive, immediate action is necessary to prevent wage garnishment or a bank levy.

Financial strain also suggests the need for relief. When income fluctuations, medical costs, or essential living expenses exceed available monthly earnings, the IRS may consider hardship programs. Documentation such as eviction notices, delinquent utility bills, or medical payment plans can support hardship claims.

A summary of common indicators includes:

- Repeated IRS notices escalating in severity.

- Accrued penalties that significantly increase the balance.

- Transcript codes indicating pending enforcement.

- Inability to pay essential monthly expenses.

- Unfiled returns block access to relief programs.

These indicators highlight the circumstances in which tax relief becomes necessary and demonstrate when professional representation may support a more structured resolution.

Cost Structures and Variables Affecting Tax Relief Outcomes

IRS tax relief outcomes depend on a combination of financial, procedural, and administrative variables that influence what the agency considers collectible. These variables shape the payment amounts, settlement values, and eligibility for hardship designations. Cost structures are not fixed; instead, they arise from a detailed evaluation of income behavior, allowable expenses, and asset positions. The IRS uses standardized methodologies to determine what financial contribution aligns with the taxpayer’s capacity.

The evaluation begins with disposable income, calculated by applying the IRS Collection Financial Standards to household expenses. If disposable income exceeds the allowable limits, the IRS may require higher payments or deny hardship-based relief. When disposable income falls below allowable thresholds, options such as Currently Not Collectible status or a lower Offer in Compromise settlement may become feasible.

Asset equity also contributes to the cost structure. The IRS assesses real estate, vehicles, bank balances, retirement accounts, and business assets to determine if equity can be applied toward repayment. Equity thresholds differ by asset type. For example, vehicles may receive specific exclusions related to necessity, while home equity may be partially exempt based on local market conditions or liens. High equity can reduce eligibility for settlement programs, as the IRS expects taxpayers to leverage available assets unless doing so creates documented hardship.

Other variables influencing cost calculations include tax debt type, filing compliance, and remaining statute time. Payroll tax liabilities generally receive stricter scrutiny because they involve trust fund components. Missing returns increase risk and may limit program availability until filing is complete. The remaining time before the Collection Statute Expiration Date affects the IRS’s expectations; shorter statutes may result in lower settlement requirements if full repayment is unlikely before the deadline.

Key cost drivers include:

- Disposable income after allowable expenses

- Equity in real and personal property

- Age of the tax debt and remaining statute time

- History of filing compliance

- Severity of prior enforcement actions

- Industry-specific or self-employment risks

These variables interact to determine whether a relief program is accessible and what financial contribution the IRS expects. Each factor represents a component of the agency’s structured approach to assessing collectibility and determining the appropriate resolution.

Consumer Considerations Before Choosing a Tax Relief Firm

Selecting a tax relief firm requires awareness of licensing requirements, representation capabilities, documentation standards, and industry practices. Not all firms provide the same level of expertise or comply with the guidelines established for tax practitioners. Understanding these distinctions helps ensure that relief applications are prepared correctly and presented in accordance with IRS expectations.

Representation before the IRS requires specific credentials. Individuals authorized to represent taxpayers include enrolled agents, attorneys, and certified public accountants. Firms must have appropriately licensed personnel responsible for communicating with the IRS and interpreting transcripts. Administrative staff may support the process but cannot provide representation independently. Consumers often overlook credential verification, yet it is central to ensuring that relief proposals meet procedural standards.

Transparency is another significant consideration. Reliable firms outline cost structures, service stages, and expected timelines without guaranteeing outcomes. IRS decisions depend on financial verification, compliance status, and agency review processes. Firms that promise fixed settlement amounts or guaranteed approval may raise concerns, as settlement outcomes cannot be pre-determined without verified financial analysis.

Documentation practices influence the quality of relief submissions. Firms must request detailed income records, asset valuations, expense receipts, and supporting financial statements. Incomplete documentation increases the likelihood of IRS delays or denials. A credible firm uses established procedures to collect, verify, and organize data in accordance with Form 433 requirements and IRS financial standards.

Industry misrepresentations also play a role in firm selection. Common issues include:

- Promises of debt reduction without financial analysis

- Lack of licensed representation

- Refusal to provide service breakdowns

- Limited experience with complex hardship cases

- Insufficient communication during IRS review

Consumers benefit from evaluating firms based on their track record with cases involving wage garnishments, lien withdrawal requests, or long-term hardship designations. Firms that understand transcript patterns, compliance requirements, and IRS internal workflows typically deliver more accurate case positioning.

These considerations help distinguish firms capable of navigating IRS systems from those that may rely on generic processes that fail to address the complexities of financial evaluation and relief eligibility.

Why Tax Hardship Center Aligns With IRS Standards for Relief

Tax Hardship Center aligns with IRS guidelines through documentation accuracy, consistent communication practices, and familiarity with the financial standards that determine relief outcomes. The firm’s methodology centers on presenting financial information in a format that mirrors IRS evaluation systems, reducing the likelihood of discrepancies or requests for clarification. This alignment supports efficient review and increases the possibility that relief proposals reflect the taxpayer’s verified capacity.

Documentation procedures involve a structured approach to gathering financial data. Household income, bank statements, medical costs, loan obligations, and property valuations are organized according to Form 433 categories. This arrangement mirrors the format used by IRS personnel, allowing financial entries to be compared directly against transcript codes and income verification systems. Cases involving inconsistent income or self-employment often require detailed breakdowns, which the firm prepares to support an accurate review.

Experience with hardship cases plays a central role in the firm’s alignment with IRS standards. Cases involving low disposable income, medical crises, business closures, or fluctuating revenue require precise modeling in accordance with IRS expense guidelines. The firm identifies which expense categories qualify for exceptions and prepares supporting documentation to validate these exceptions. This approach helps demonstrate how financial conditions limit repayment ability.

Consistency with IRS compliance expectations also influences case outcomes. Relief programs require up-to-date filing, accurate estimated payments for self-employed individuals, and timely submission of requested documents. The firm’s process ensures that all necessary filings and compliance steps are completed before proposing relief options, eliminating one of the most common reasons for IRS denials.

A summary of alignment factors appears below:

| Alignment Factor | Purpose | Impact |

| Accurate financial documentation | Ensures consistency with IRS forms | Reduces review delays |

| Experience with hardship modeling | Addresses complex financial situations | Improves relief eligibility |

| Compliance-focused preparation | Meets IRS submission standards | Prevents procedural denials |

| Structured communication with IRS | Facilitates timely responses | Maintains case momentum |

These practices demonstrate how Tax Hardship Center supports relief proposals that align with IRS expectations and reflect accurate financial conditions.

Post-Resolution Obligations and Long-Term Tax Compliance

After a relief program is approved, ongoing compliance determines whether the benefits of the resolution remain intact. IRS programs require continued adherence to filing requirements, payment obligations, and income reporting standards. Post-resolution commitments vary based on the type of relief secured, but all programs share a common emphasis on preventing future delinquency.

Offer in Compromise resolutions include a multi-year compliance period during which all required returns must be filed on time, and any tax due must be paid by the deadline. Failure to meet these obligations may void the agreement and reinstate the original liability. The IRS monitors compliance through annual transcript updates and automated systems that track filing patterns.

Installment Agreements require timely payment of monthly amounts and adherence to future filing obligations. If new balances arise, default may occur unless the taxpayer secures additional arrangements. IRS systems detect missed payments through automated triggers, prompting notices and potentially reinstating enforcement activity.

Currently Not Collectible status requires attention to income changes. If future income increases, the IRS may reassess the case and determine whether payments are now feasible. Annual wage reporting and income matching systems identify significant financial shifts. Maintaining proper documentation helps support continued hardship if circumstances do not improve.

Adjustments to withholding or estimated payments are essential for long-term compliance. Individuals with employment income may need to update withholding elections to prevent new balances. Self-employed individuals must make quarterly estimated tax payments to avoid penalties and remain in compliance with IRS requirements.

A structured list of post-resolution obligations includes:

- Filing all future returns on time.

- Paying all tax due for subsequent years.

- Maintaining updated withholding or estimated payments.

- Responding promptly to IRS notices regarding compliance.

- Providing updated financial data if required for hardship cases.

These obligations support the stability of the resolution and help prevent new tax liabilities. Compliance also influences future interactions with the IRS, such as lien withdrawal requests or modifications to payment arrangements.

Conclusion

IRS tax relief programs assess income, expenses, assets, and repayment ability to determine eligibility. Accurate documentation and transcript data drive every decision.

Tax Hardship Center supports this process by reviewing transcripts, preparing required documents, and aligning financial details with IRS standards for settlements, payment plans, penalty relief, or hardship status.

Relief options vary, and timely action is crucial when facing liens, levies, or garnishments. Long-term success depends on staying compliant, as the IRS continually monitors filings and payments.

By following IRS procedures and presenting precise financial data, Tax Hardship Center helps taxpayers achieve stable, realistic resolutions.

Frequently Asked Questions About IRS Tax Relief Services

What determines whether an individual qualifies for IRS tax relief programs?

Qualification depends on verified financial data that shows the taxpayer’s ability or inability to repay the balance. The IRS reviews income, household size, regional living standards, asset equity, filing history, and the remaining collection statute. Eligibility is determined through the Form 433 financial statement series, which calculates disposable income and collectibility in accordance with IRS standards.

How long does IRS tax relief approval take once documentation is submitted?

Timelines vary based on the program, account status, and review unit. Offers in Compromise often require several months of financial verification, while streamlined Installment Agreements may be approved in comparatively shorter timeframes. Currently Not Collectible status is frequently reviewed quickly when hardship evidence is complete. Delays generally occur when filing discrepancies or incomplete documentation require clarification.

Can IRS tax debt be settled for less than the total amount owed?

Settlement is possible when the IRS calculates a reasonable collection potential that is less than the total liability. The settlement amount reflects disposable income and net equity. Approval depends on accurate financial disclosure and supporting records that demonstrate repayment limitations.

What documentation supports an economic hardship determination?

Hardship claims require evidence that basic living expenses exceed income levels. Typical documentation includes wage records, detailed bank statements, healthcare expenses, housing statements, dependent care costs, and proof of overdue essential bills. IRS personnel compare these records with financial standards to determine eligibility for hardship-based programs.

Are tax liens or wage garnishments reversible through tax relief programs?

Relief programs can halt or reverse specific enforcement actions. Wage garnishments may stop once an approved agreement or hardship designation is in place. Federal tax liens may be withdrawn under qualifying circumstances, such as entry into specific payment arrangements or approved settlements. Bank levies may not be reversible after funds are withdrawn, but can be prevented through timely relief approval.

What role do IRS transcripts play during tax relief evaluation?

Transcripts reveal tax assessments, filing gaps, wage data, penalties, and collection activity. They serve as the IRS’s official record of the taxpayer’s compliance and financial status. Relief proposals are evaluated against transcript codes to ensure that financial statements and reported income match documented history.

Does self-employment or irregular income affect relief eligibility?

Self-employment often introduces irregular income, variable expenses, and deductible business costs. These factors require detailed analysis to determine actual disposable income. When properly documented, self-employment income may support settlement or hardship requests, especially in cases of fluctuating revenue, seasonal income, or business decline.