You owe the IRS money, and they filed a Notice of Federal Tax Lien. Now that your credit score has dropped, you cannot refinance your mortgage, and when you tried to sell your house, the title company said the lien has to be cleared before closing. You thought paying the IRS would fix it. You paid the balance in full, but the lien still appears on your credit report and in public records.

Here is what happened: the IRS released the lien, but they did not withdraw it. A release and a withdrawal are not the same thing. A release removes the IRS’s claim on your property after you pay the debt. A withdrawal removes the public filing entirely, as if the lien never existed. Most people need a withdrawal to fully clear their record, but the IRS does not automatically grant one just because you paid.

This guide explains what a federal tax lien notice actually does, how it affects your ability to sell or refinance property, the difference between lien release and lien withdrawal, the exact steps to get a lien removed from public records so it stops blocking your financial transactions, and when professional help makes the difference between clearing the lien in time for closing and losing the sale.

What a Federal Tax Lien Notice (NFTL) Is and What It Does

A federal tax lien is the IRS’s legal claim against your property when you owe unpaid taxes. The lien itself arises automatically when you owe money, and the IRS assesses the balance. You do not receive a notice when the lien arises. It happens silently in the background.

A Notice of Federal Tax Lien (NFTL) is the public filing that makes the lien visible to creditors, lenders, and anyone searching public records. The IRS files the NFTL with your county recorder’s office or state filing office. Once filed, the lien becomes public information. It appears on your credit report, in real estate title searches, and in public record databases.

What the NFTL does:

- Gives the IRS a legal claim on all property you currently own and property you acquire in the future while the lien is active

- Appears on your credit report and damages your credit score, typically dropping it by 50 to 100 points

- Shows up in title searches when you try to sell or refinance real estate

- Alerts other creditors that the IRS has a claim on your assets, which makes it harder to get loans, credit cards, or financing

- Establishes the IRS’s priority position over other creditors. In most cases, the IRS gets paid before other creditors when property is sold

What the NFTL does not do:

- A lien does not seize your property. It claims an interest in it, but it does not take it. That is a levy, not a lien

- A lien does not prevent you from selling your property. You can still sell, but the lien has to be paid from the sale proceeds before you receive any money

- A lien does not go away automatically when you pay the debt. You must request a release or withdrawal

The IRS files a lien to protect its interest in your assets. It also pressures you to pay because the lien makes it difficult to conduct normal financial transactions.

How Much You Have to Owe Before the IRS Files a Lien

The IRS does not file a lien for every balance. They have internal thresholds based on the amount owed and the likelihood of collection.

General threshold: The IRS typically files a Notice of Federal Tax Lien when you owe $10,000 or more in combined tax, penalties, and interest. This is not a hard rule. The IRS can file a lien for less than $10,000 if they believe you are at risk of leaving the country, hiding assets, or not paying voluntarily.

Balance under $10,000: If you owe less than $10,000 and you set up a payment plan, the IRS usually will not file a lien. If you ignore notices and make no effort to pay, they may file a lien even on smaller balances.

Balance over $25,000: If you owe $25,000 or more, the IRS almost always files a lien unless you set up a Direct Debit Installment Agreement before the lien is filed.

Lien filing timeline: The IRS typically files the NFTL after sending you multiple balance-due notices and giving you at least 30 days to respond. The timeline from first notice to lien filing is usually 3 to 6 months. If you set up a payment plan before the lien is filed, the IRS may choose not to file one.

Once the NFTL is filed, it remains in public records until you pay the debt and request a release, or until you qualify for withdrawal.

How a Federal Tax Lien Affects Selling or Refinancing Your Home

A federal tax lien attaches to all your property, including your home. When you try to sell or refinance, the lien becomes a problem.

Selling your home: You can sell property with a lien on it, but the IRS must be paid from the proceeds. During a real estate closing, the title company runs a lien search. If they find an IRS lien, they notify the IRS and set aside sufficient sale proceeds to pay the lien in full. You receive only what remains after the IRS is paid.

If the sale price is less than what you owe on your mortgage and the IRS lien combined, the IRS may agree to discharge the lien from that specific property so the sale can go through. A discharge does not release the lien entirely. It removes the lien from that one piece of property so it can be sold, but the lien remains attached to your other assets.

Refinancing your home: Most lenders will not refinance a mortgage if there is an IRS lien on the property. The lien gives the IRS priority over the lender in most cases, which makes the loan too risky for the lender. To refinance, you usually need to pay the IRS debt in full and get the lien released, or request lien subordination so that the new mortgage lender takes priority over the IRS.

Lien subordination does not remove the lien. It just changes the order of priority so the lender gets paid first if the property is sold or foreclosed. The IRS grants subordination only if it believes it increases the likelihood of collecting the tax debt.

For more on liens and how long they last, see our guide on how long does an IRS lien last.

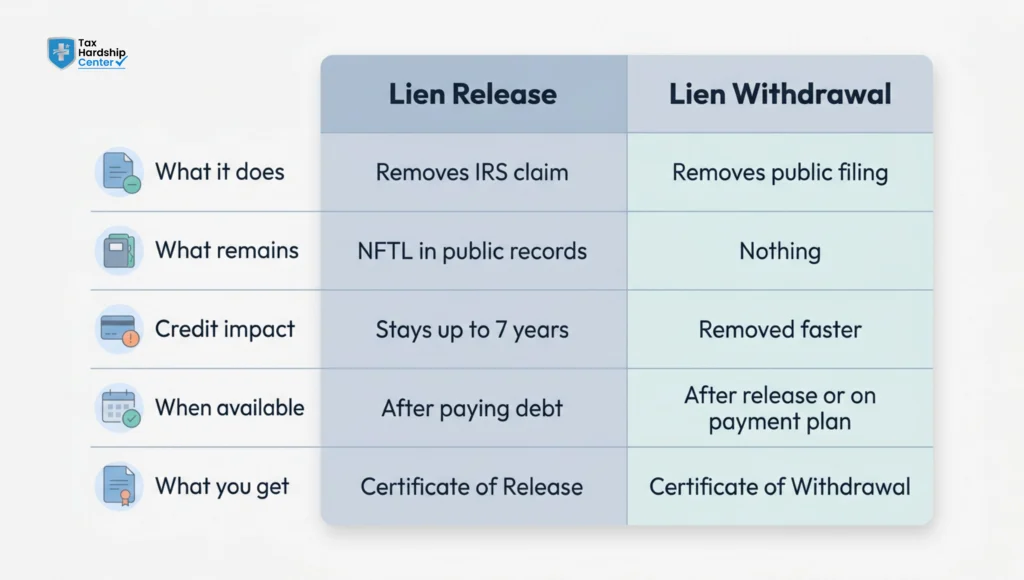

Lien Release vs Lien Withdrawal: What Is the Difference?

Most people think paying the IRS removes the lien from public records. It does not. Paying the debt triggers a lien release, not a lien withdrawal. The two are very different.

Lien release: A release means the IRS no longer has a claim on your property because the debt is paid. The IRS issues a Certificate of Release of Federal Tax Lien. The release is filed in the same public records as the original NFTL. The release shows that the debt has been satisfied and the IRS’s claim has been removed.

However, the original NFTL remains in public records. It shows you had a lien and that it was released. The release does not erase the NFTL. It adds a second document to the file. Both the lien and the release stay in public records for years. The lien may remain on your credit report for up to seven years even after it is released.

Lien withdrawal: A withdrawal removes the NFTL from public records entirely. It is as if the lien was never filed. The IRS issues a Certificate of Withdrawal of Notice of Federal Tax Lien. The withdrawal removes the NFTL from the public filing and should be reflected on your credit report faster than a release.

A withdrawal does not mean the debt is forgiven. You still have to pay the balance. But the public filing is removed, making it easier to get credit, sell property, or refinance without the lien appearing in title searches.

When you can request a withdrawal:

- After the debt is paid in full and the lien is released

- If the lien was filed in error

- If you enter into a Direct Debit Installment Agreement and request a withdrawal under the IRS Fresh Start program

- If withdrawal would help you collect the debt faster (for example, removing the lien would allow you to refinance and pay the IRS from the proceeds)

Most taxpayers qualify for withdrawal after paying the debt in full. You have to request it. The IRS does not automatically withdraw the lien just because you paid.

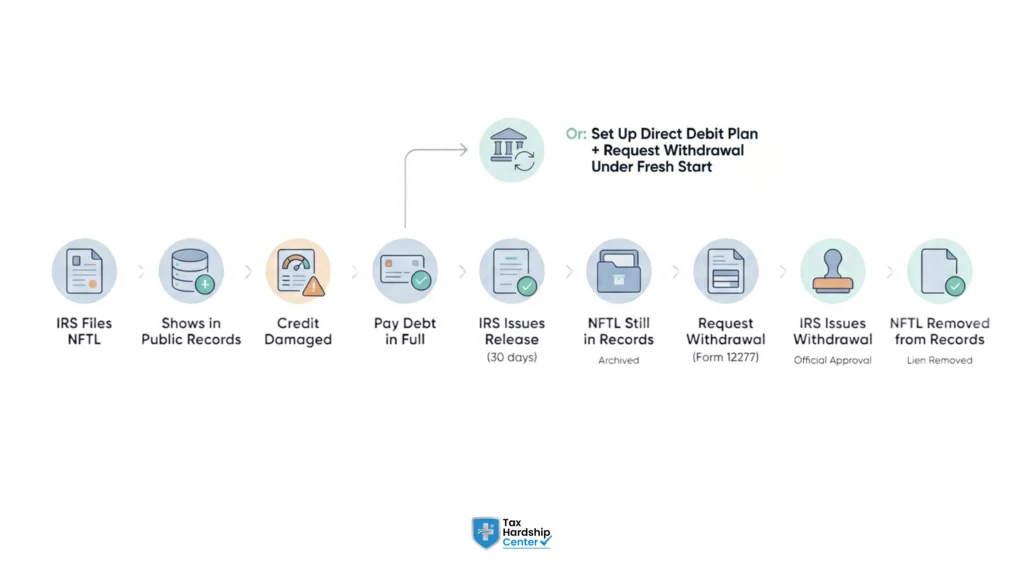

How to Get a Federal Tax Lien Released After Paying the Debt

Once you pay the IRS in full, the lien should be released within 30 days. The IRS is required by law to issue a Certificate of Release of Federal Tax Lien within 30 days of full payment.

Step 1: Pay the balance in full. The IRS will not release the lien until the debt is paid in full, including all penalties and interest. If you are on a payment plan, the lien remains in place until the final payment is made.

Step 2: Wait 30 days for the IRS to issue the release. The IRS processes the payment and automatically generates the Certificate of Release. You do not need to request it. The release is mailed to you and filed in the same public records as the original NFTL.

Step 3: Verify the release was filed. After receiving the Certificate of Release, check with your county recorder’s office or the state filing office to confirm the release appears in public records. Sometimes the IRS files the release late or files it in the wrong location. If the release does not appear in public records within 45 days, call the IRS at 1-800-913-6050 and request that they refile it.

Step 4: Dispute the lien with credit bureaus if it remains on your credit report after release. Once the lien is released, you can dispute it with Equifax, Experian, and TransUnion. Provide them with a copy of the Certificate of Release. The credit bureaus should remove the lien from your report, but it can take 30 to 60 days.

If the IRS does not issue a release within 30 days of payment, you can request one by calling the IRS or submitting Form 12277 (Application for Withdrawal of Filed Form 668(Y), Notice of Federal Tax Lien).

How to Get a Federal Tax Lien Withdrawn from Public Records

Withdrawal is better than release because it removes the NFTL from public records entirely. Here is how to request a withdrawal.

After paying the debt in full: Once the debt is paid and the lien is released, you can request withdrawal by submitting Form 12277 to the IRS. Include a copy of your Certificate of Release and a written statement explaining why withdrawal is appropriate. Common reasons include that you paid in full, that the lien is impairing your ability to obtain credit or conduct business, and that removing the lien would not harm the IRS, since the debt is already satisfied.

The IRS reviews withdrawal requests and approves most of them when the debt is paid in full. Processing takes 30 to 45 days. Once approved, the IRS issues a Certificate of Withdrawal and files it in the public records where the NFTL was filed.

While on a Direct Debit Installment Agreement: Under the IRS Fresh Start program, you may qualify for lien withdrawal if you owe $25,000 or less, you set up a Direct Debit Installment Agreement, you have made at least three consecutive direct debit payments, and you agree to continue paying by direct debit. This allows you to remove the lien from public records while you are still paying off the debt.

To request withdrawal under Fresh Start, submit Form 12277 and include proof of your installment agreement and payment history. The IRS reviews the request and approves it if you meet the criteria.

If the lien was filed in error: If the IRS filed a lien and you did not owe the debt, the balance was already paid, or the IRS made a procedural error, you can request withdrawal by submitting Form 12277 with documentation proving the error. The IRS will withdraw the lien if it verifies that the filing was incorrect.

For more on IRS Fresh Start and lien withdrawal eligibility, see our guide on IRS Fresh Start program requirements.

What Happens If You Ignore a Federal Tax Lien

A federal tax lien does not go away on its own. If you ignore it, it will remain in public records and continue to damage your credit and block financial transactions.

The lien remains active for 10 years. The IRS collection statute allows the IRS to collect the debt for 10 years from the date the tax was assessed. The lien remains active for the full 10 years unless you pay the debt or the IRS agrees to withdraw it.

The IRS can levy your property even after filing a lien. A lien is not enforcement. It is a claim. The IRS can still issue a levy to seize your wages, bank account, or other property even after filing a lien. The lien and levy are separate collection tools.

The lien attaches to property you acquire after it is filed. If you buy a house, a car, or other property after the lien is filed, the lien automatically attaches to it. The lien covers everything you own now and everything you acquire while it is active.

You cannot sell or refinance property without addressing the lien. Every time you try to sell or refinance, the lien will appear in the title search. The sale or refinance will not go through unless the lien is paid, discharged, or subordinated.

Your credit remains damaged for up to seven years after the lien is released. Even after you pay the debt and the lien is released, it can stay on your credit report for seven years from the date it was filed. Withdrawal removes it faster, but a release alone does not erase it.

Ignoring a lien makes it worse. It does not expire on its own within a reasonable timeframe, and it continues to interfere with your financial life until you address it.

Why Professional Help Matters When a Lien Blocks a Property Transaction

A federal tax lien can quickly derail a home sale or refinance, especially when closing deadlines are tight.

Most people assume that paying the IRS automatically removes the problem. But a lien release can still take weeks to process, and if the title company wants the lien removed from public records entirely, you may need a withdrawal, which takes even longer.

Things get more complicated when the sale proceeds are not enough to fully pay the IRS debt. In those cases, you may need a lien discharge so the property can still be sold. And for refinances, lenders often require lien subordination before approving the new loan.

All of these options involve IRS forms, financial documentation, and strict review processes. Missing paperwork or delays can put the entire transaction at risk.

Tax Hardship Center helps taxpayers handle lien releases, withdrawals, discharges, and subordinations when IRS liens are blocking property transactions. The firm works directly with the IRS, lenders, and title companies to help move the process forward as quickly as possible.

If you are trying to sell, refinance, or remove a federal tax lien from public records, getting professional help early can help avoid delays that could jeopardize the transaction.

FAQs

How long does a federal tax lien last?

A federal tax lien usually stays active for 10 years from the assessment date unless the debt is paid sooner. Paying the balance releases the lien, but public records may still show it unless a withdrawal is requested.

Is a tax lien serious?

Yes. A federal tax lien can affect credit access, property sales, refinancing, and future financial transactions. It also gives the IRS legal priority over many other creditors.

How much do you have to owe the IRS to get a tax lien?

The IRS commonly files liens once balances exceed certain thresholds, especially when payment arrangements are not in place. Larger balances increase the likelihood significantly.

How to remove a federal tax lien?

Paying the debt in full triggers a lien release. In some cases, taxpayers may also qualify to request withdrawal through IRS programs and forms.

What happens if you don’t pay a federal tax lien?

The lien can remain active for years, continuing to affect property ownership, refinancing, and borrowing capacity. The IRS may also escalate collection actions.

Does a federal tax lien ever expire?

Yes. Most liens expire after the IRS collection statute ends, though certain actions can extend that timeline. Paying early resolves the debt faster and avoids prolonged financial impact.

Conclusion

A federal tax lien notice is not just a piece of paper. It is a public filing that can damage your credit, block property sales, and make refinancing nearly impossible. Most people think paying the IRS removes the lien from public records. It does not. Paying triggers a release, which removes the IRS’s claim but leaves the NFTL in public records. Withdrawal removes the filing entirely, but you have to request it.

If you are trying to sell a house or refinance and a lien is blocking the transaction, you need to act fast. The IRS can discharge the lien on the specific property so the sale can close, or you can pay the balance from the sale proceeds and request immediate withdrawal to prevent the next transaction from being blocked. The difference between release and withdrawal is not just technical. It determines how long the lien remains on your credit report and whether it continues to appear in title searches.

Most taxpayers qualify for withdrawal after paying the debt. The IRS just does not advertise it, and the timeline matters as a closing date approaches.

Key Takeaways:

- A Notice of Federal Tax Lien is a public filing that appears on your credit report and in property title searches

- The IRS typically files a lien when you owe $10,000 or more, but it can file for smaller balances if you ignore notices

- A lien blocks property sales and refinances because it gives the IRS a claim on the proceeds

- A lien release removes the IRS’s claim after you pay the debt, but leaves the NFTL in public records

- Lien withdrawal removes the NFTL from public records entirely and should be requested after paying the debt

- You can request a withdrawal while on a payment plan if you qualify under the IRS Fresh Start rules

- Ignoring a lien does not make it go away. It lasts for 10 years and continues to damage your credit and block transactions

If you have a federal tax lien and you need to sell property, refinance, or get it removed from public records, get a free case review at Tax Hardship Center.