If you just found out an IRS revenue officer has been assigned to your case, that is not the same as getting another letter in the mail. It means the IRS has moved past automated notices and assigned a real person to collect from you directly. That is a different category of problem, and it needs a different kind of response.

This article explains exactly what an IRS revenue officer is, what authority they carry, what typically happens after assignment, and what your options are once contact begins.

What Is an IRS Revenue Officer?

An IRS revenue officer is a field collection agent employed by the IRS Collections division. Unlike the automated notices you may have been receiving, a revenue officer is a salaried federal employee whose job is to resolve unpaid tax debt through direct contact and, if necessary, enforcement action.

Revenue officers are assigned when a tax debt remains unresolved after the standard notice process. The IRS does not send a revenue officer for a minor balance. By the time one is assigned to your case, the agency has typically already sent multiple escalating notices, including warnings like a CP14, CP503, CP504, or an LT11 final levy notice.

The IRS Collections division employs revenue officers specifically for cases that require personal contact. They operate out of local IRS field offices and can show up at your home, your business, or your employer’s location.

Revenue Officer vs. Revenue Agent: Not the Same Thing

These two titles create a lot of confusion. They are separate roles with completely different functions.

A revenue agent is an IRS auditor. Their job is to examine tax returns and determine whether you owe more than you reported. They work in the examination division and address accuracy issues.

A revenue officer is a collector. They are not reviewing your return for errors. They already know you owe a balance, and their job is to collect it. They work in the collections division and handle enforcement.

If a revenue officer has been assigned to your case, the debt itself is not in dispute. What matters now is how it gets resolved, and how fast.

What Powers Does a Revenue Officer Actually Have?

Revenue officers have significant authority. Understanding what they can and cannot do matters before your first contact with one.

Negotiate Resolutions

The primary function of a revenue officer is to reach a resolution. That can include setting up an installment agreement, recommending Currently Not Collectible status, or reviewing an Offer in Compromise if you qualify. They are not only there to enforce. They are also there to resolve.

File a Notice of Federal Tax Lien

A revenue officer can request that a Notice of Federal Tax Lien be filed against your property. This lien becomes part of the public record and affects your credit, your ability to sell assets, and your borrowing capacity until the debt is resolved.

Issue Levies

Revenue officers have the authority to initiate levy action, which means seizing wages, bank accounts, or other assets to satisfy the debt. A wage levy takes a calculated percentage of your disposable income from every paycheck until the debt is paid or an agreement is in place. A bank levy freezes and seizes funds directly from your accounts. These are not threats. They are enforcement tools that revenue officers use regularly.

Seize Physical Assets

In serious cases involving significant debt or repeat noncompliance, a revenue officer can initiate seizure of physical property. Vehicles, real estate, and business equipment can all be seized. This outcome is uncommon but not rare in high-balance or long-unresolved cases.

Why Cases Get Assigned to Revenue Officers

Not every tax debt ends up with a revenue officer. The IRS uses its Automated Collection System to handle most debts via letters and phone calls. A revenue officer gets involved when:

- The balance is substantial, typically $10,000 or more

- Multiple notice cycles have been ignored

- There are unfiled returns in addition to unpaid debt

- The IRS has identified assets that may be levied

- There are payroll tax issues or trust fund penalties involved

- Previous collection attempts through the automated system produced no response

For small business owners facing payroll tax debt, an assignment to a revenue officer is especially common. Trust fund penalties are a high priority for the IRS, and personal liability exposure makes these cases more complex than standard individual debt cases.

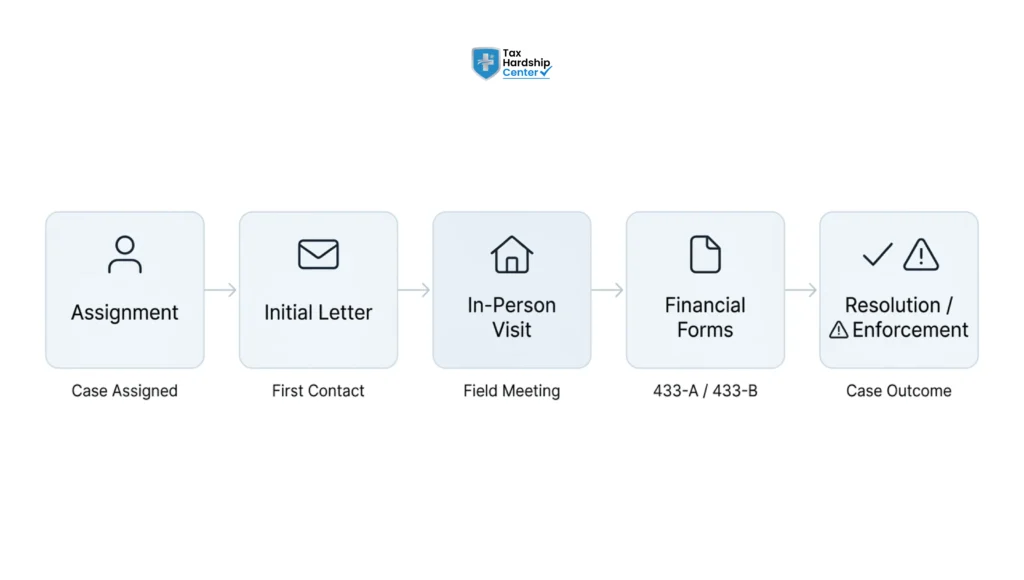

What Happens After a Revenue Officer Is Assigned?

Once assigned, the revenue officer will attempt to make contact. This typically follows a specific sequence.

Initial contact: The officer will send a letter requesting a meeting or call. This is your first formal notice of their involvement.

In-person visit: If you do not respond, the officer may visit your home or business. They carry official IRS credentials and are required to present them on request.

Document requests: The officer will ask you to complete a Collection Information Statement, either Form 433-A for individuals or Form 433-B for businesses. This is a detailed financial disclosure covering income, expenses, assets, and liabilities. It is used to determine which resolution options you qualify for.

Resolution or enforcement: Based on your financial picture, the officer will work toward an agreement or, if you are unresponsive or uncooperative, move to enforcement action.

The first 48 hours after contact matter. Responding quickly signals cooperation and can slow down enforcement while a resolution is being worked out. Ignoring contact does the opposite.

Do IRS Revenue Officers Call You?

Yes. Revenue officers do call taxpayers directly, and this is one of the areas where the risk of scams is real.

The IRS will always send a written notice before an officer calls or visits. If someone claims to be an IRS revenue officer on the phone but you have received no prior written notice, treat the contact with caution. Legitimate IRS officers will not demand immediate payment over the phone, threaten arrest, or ask for payment by wire transfer or gift card.

If you receive a call and are unsure whether it is legitimate, you can call the IRS directly at 1-800-829-1040 to verify. The IRS guidance on verifying officer identity covers exactly what a real contact looks like versus a scam.

Your Rights When a Revenue Officer Contacts You

You have rights throughout this process, and knowing them changes the dynamic considerably.

You have the right to representation. You do not have to speak to a revenue officer alone. A licensed tax professional can communicate with the officer on your behalf, which removes you from direct pressure and ensures nothing is said that could complicate your case.

You have the right to a Collection Due Process hearing. If the IRS has filed a lien or issued a levy notice, you can request a CDP hearing using Form 12153. This pauses enforcement while your case is reviewed by the IRS Office of Appeals.

You have the right to appeal an officer’s decision. If you disagree with how your case is being handled, you can escalate through the IRS appeals process without losing your right to resolution.

Knowing these rights before the first meeting gives you a position to work from rather than a situation to react to.

How the Tax Hardship Center Handles Revenue Officer Cases

When a revenue officer is involved, professional representation is not optional for most people. It is what makes the difference between a workable resolution and an enforcement spiral.

Tax Hardship Center works directly with revenue officers on behalf of clients. That means preparing the financial disclosures, presenting the strongest possible case for your resolution option, and handling all communication so you are not navigating this alone. Whether the right path is a structured installment agreement, a Currently Not Collectible filing, or a penalty abatement request, the work starts with understanding your full financial picture and knowing what each option actually requires.

For cases involving wage garnishment risk or an active levy, Tax Hardship Center can move quickly. A levy does not have to run its full course. Intervention before the first paycheck is affected is possible when representation begins early enough.

If you have been contacted by a revenue officer or received a notice that one has been assigned, a free case review is the right first step. Reach out at taxhardshipcenter.com/contact to get a clear picture of where things stand and what can be done.

FAQs

What is an IRS revenue officer?

An IRS revenue officer is a field collection agent responsible for resolving unpaid tax debts through direct contact. They are not auditors. They work out of local IRS field offices and can visit your home, business, or employer location. Their role is to reach a resolution with you or initiate enforcement action if you remain unresponsive.

Do IRS revenue officers call you?

Yes, revenue officers do call taxpayers directly. However, the IRS will always send a written notice before any phone or in-person contact. If you receive a call with no prior written notice, verify the contact before providing any information. Legitimate officers will never demand payment by gift card, wire transfer, or over the phone.

What is the difference between a revenue officer and a revenue agent?

A revenue agent is an IRS auditor who examines returns for accuracy. A revenue officer is a collector who works to resolve unpaid balances. If a revenue officer has been assigned to your case, the IRS is not questioning what you owe. They are working to collect it.

Can a revenue officer show up at my home?

Yes. Revenue officers can and do make unannounced visits to residences and businesses. They are required to carry and present official IRS credentials. You are not required to speak with them without representation present, and you can request to reschedule through your representative.

What happens if I ignore a revenue officer?

Ignoring a revenue officer accelerates enforcement. The officer can file a federal tax lien, issue a wage or bank levy, or, in serious cases, initiate asset seizure. Responding quickly and working toward a resolution is always the better path.

Can I get representation before my first meeting with a revenue officer?

Yes, and it is strongly advisable. A licensed tax professional can communicate directly with the officer on your behalf, handle all document submissions, and present the strongest case for your resolution option. You do not have to handle this alone.

How do I verify the identity of an IRS revenue officer?

Ask to see their official IRS identification and badge. You can also call the IRS at 1-800-829-1040 to confirm that an officer has been assigned to your case. Scammers impersonating IRS officers are common. Always verify before sharing any financial information.

Conclusion

An IRS revenue officer assignment signals that the automated collection phase is over. The IRS has moved to a direct personal collection effort. That changes the urgency and the stakes.

Resolution is still possible at this stage. Revenue officers work with taxpayers and their representatives to reach agreements every day. The key is responding quickly, knowing your rights, and having someone in your corner who understands how this process actually works.

Key Takeaways

- An IRS revenue officer is a field collection agent, not an auditor, and their assignment means direct enforcement is now possible

- Revenue officers can file tax liens, issue wage and bank levies, and, in serious cases, seize physical assets

- Cases are typically assigned when balances are substantial, notices have been ignored, or there are unfiled returns alongside unpaid debt

- Revenue officers are also authorized to negotiate resolutions, including installment agreements, CNC status, and Offers in Compromise

- The IRS will always send a written notice before a revenue officer calls or visits in person

- You have the right to representation and do not have to speak to a revenue officer without a licensed professional present

- A Collection Due Process hearing can pause enforcement action when requested through Form 12153

- Responding quickly after an assignment signals cooperation and can slow down enforcement timelines considerably

- Payroll tax cases and trust fund penalty situations are among the most common triggers for revenue officer assignment

- Professional representation at this stage changes outcomes because officers respond differently when the taxpayer has knowledgeable support

Get a free case review: Tax Hardship Center works with taxpayers facing active IRS collections, including revenue officer cases. Reach out today to understand your options before enforcement begins.