You picked up a second job. Maybe it was for rent, a goal, or just because someone offered and you said yes.

Then tax season arrived, and the question started nagging at you: Do I file two separate returns? One for each job?

The short answer is no. But the real answer is more important than that. Most people who work two jobs end up blindsided by what they owe, and the reason almost always comes down to something that happened months before they sat down to file.

Can You Actually File Two Separate Tax Returns?

No. The IRS does not allow you to file separate federal tax returns for each job you hold.

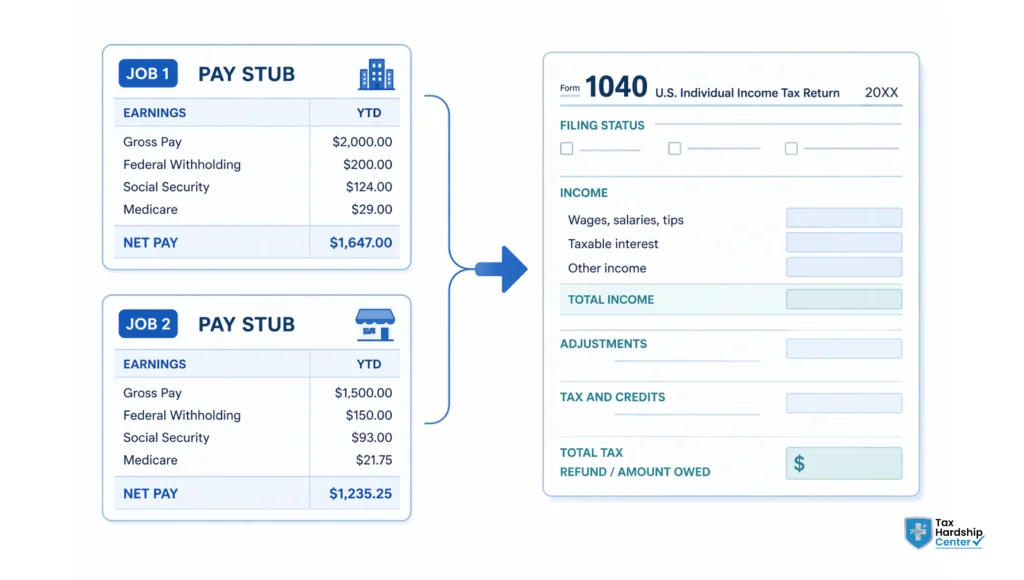

Every source of income you earn during the year goes on one single Form 1040. That includes your first W-2, your second W-2, any freelance income reported on a 1099, and side gig earnings. All of it. One return. One total income number. One tax calculation.

This is true whether you worked two jobs at the same time or switched jobs partway through the year.

The confusion makes sense. Each employer gives you a separate W-2. It feels like separate paperwork for separate situations. But the IRS treats everything you earn as a single annual income. Your W-2s are inputs, not individual filings.

What You Are Actually Filing: One Return, Multiple W-2s

When you have two W-2 forms, you enter both on your 1040. Both amounts add together to form your total wages. The IRS then applies the tax brackets to that combined number.

This is where people get surprised.

If Job A paid you $38,000 and Job B paid you $22,000, the IRS sees $60,000 in total income. Not two separate incomes of $38K and $22K. That distinction matters enormously because of how federal tax brackets work.

Your tax rate is not flat across all your income. It is marginal. Income in higher tax brackets is taxed at higher rates. The last dollars you earned from Job B might land in a higher bracket than anything your first employer ever withheld.

Why Two Jobs Often Mean You Owe More Than Expected

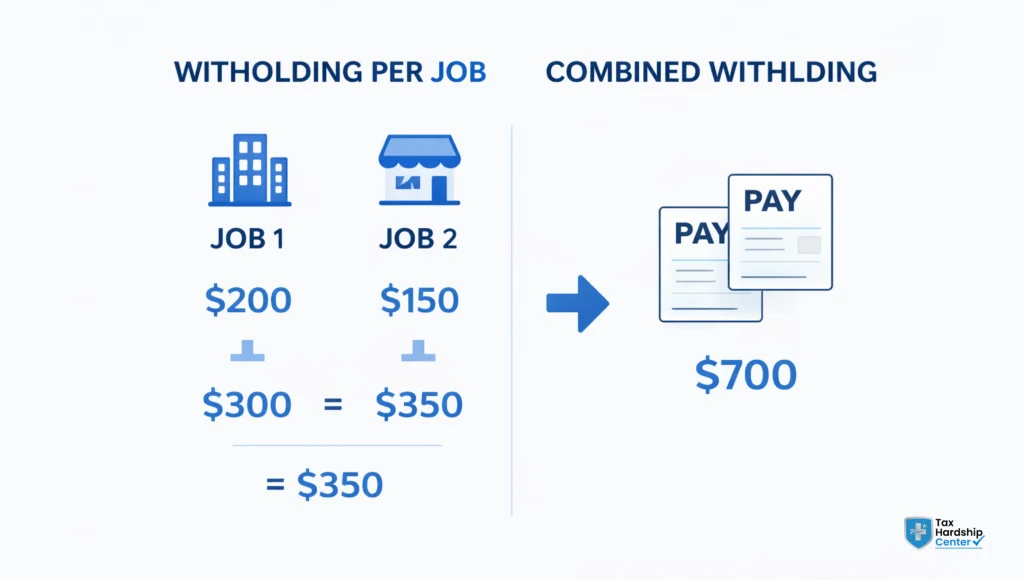

Each employer withholds taxes based on your W-4 and one assumption: that the job they’re paying you for is your only job.

Job A withholds as if you earn $38,000 total per year. Job B is withheld as if you earn $22,000 total per year.

Neither employer knows about the other. Neither adjusts for the fact that your combined income pushes you into a higher bracket. So both can be withheld at a lower rate than what you actually owe when the year is totalled.

Result: a tax bill in April that feels like it came out of nowhere.

This is not a penalty. It is not a mistake on your employer’s part. It is a structural gap in how payroll withholding works for people with multiple income sources. But knowing why it happened does not make the bill disappear.

The W-4 Problem Nobody Warned You About

The fix exists. It just required action earlier in the year.

When you started your second job, you filled out a Form W-4. Most people rush through it, claim zero or one allowance, and assume it handles itself. It usually does not. Not when you have two jobs.

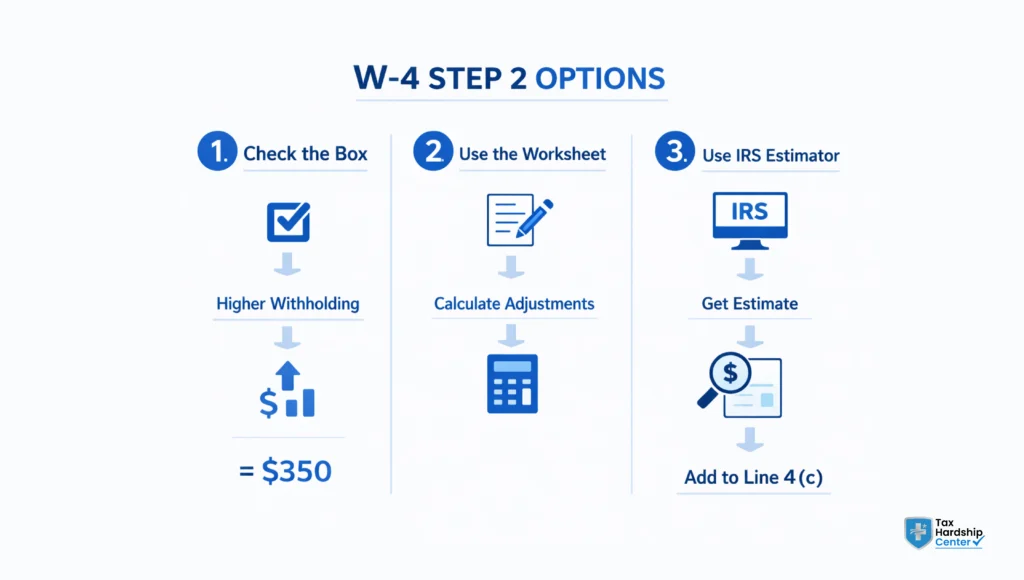

Step 2 of the W-4 exists specifically for this situation. It has three options for workers with multiple jobs:

Option 1: Check the box in Step 2(c) on both employers’ W-4 forms. Simple. Works best when both jobs pay roughly the same amount.

Option 2: Use the Multiple Jobs Worksheet (included with the W-4 instructions) to calculate extra withholding on the higher-paying job. More accurate if there is a big income difference between your two jobs.

Option 3: Use the IRS Tax Withholding Estimator at irs.gov and enter additional withholding on line 4(c). Most precise option.

Most people do none of these. That is how the tax bill accumulates.

What Happens If You Under-Withheld All Year

You file. The number on the screen is not a refund. It is a balance due.

That is the moment most people call us.

If neither job withheld enough, you owe the difference. Simple math, painful reality.

And here is the part nobody mentions upfront: if you owed more than $1,000 beyond what was withheld, the IRS can also add an underpayment penalty under IRC Section 6654. Not because you did something wrong. Not because you have two jobs. Just because not enough tax came in during the year.

Now you have a balance. You cannot pay it all at once. What do you actually do?

IRS Installment Agreement. This is a payment plan. You request one using Form 9465. Owe under $50,000 with your returns filed? You can set this up online. No phone call required.

Currently Not Collectible status. If paying right now would genuinely leave you unable to cover rent, groceries, and utilities, the IRS can temporarily pause collection activity. The debt does not disappear. But the pressure stops while you stabilise. That matters.

Offer in Compromise. This is the one everyone has heard about. The IRS accepts less than the full amount owed. It is real. It exists. And not everyone qualifies. Eligibility depends on your income, assets, and expenses. Any firm that promises this before looking at your actual financials is not being straight with you. Read what it actually involves at taxhardshipcenter.

How to Handle Two Jobs Without Getting Hit at Tax Time

If you are still working both jobs, you have time to fix this before it becomes a problem.

Here is what that actually looks like.

Update your W-4s. Go back to both employers. Complete Step 2 correctly. Use the IRS withholding estimator if you want a precise number. A few extra dollars withheld per paycheck now is genuinely better than a surprise bill in April. It sounds obvious. Most people still do not do it.

Set aside a buffer. Even after fixing the W-4, put 10 to 15 per cent of each second-job paycheck into a separate account labelled for taxes. If you do not need it, you have savings. If you do, you are not scrambling.

Check in mid-year. Pull your pay stubs in July or August. Run the IRS withholding estimator. Catching a gap in summer is much better than catching it in March when there is nothing you can do about the year that just ended.

File on time. Even if you cannot pay. This is the one people consistently get wrong. Filing late while owing costs more than paying late on a return that was filed on time. The late-filing penalty is 5 per cent per month on the unpaid balance. The late-payment penalty is 0.5 per cent per month. File first. Sort the payment after. Always in that order.

What Tax Hardship Center Does When the Tax Bill Has Already Landed

Tax Hardship Center works with individuals who have an IRS balance they cannot pay in full, including people who ended up owing because of under-withholding from multiple jobs.

This is not a complicated or unusual situation for us. It is one of the most common reasons people call.

What we do not do is promise a specific outcome until we have reviewed your actual financials. What we do is look at your full picture: income, expenses, what you owe, what notices you have received, and where you are in the IRS collection timeline. Then we tell you, honestly, which resolution path fits your situation.

That might be a standard instalment agreement. It might be in the Currently Not Collectable status while you stabilise. In some cases, it might be an Offer in Compromise. The right answer depends on facts, not promises.

If you have received an IRS notice about a balance due, like a CP14 or a CP503, or if your wages are already being garnished, the time to act is before the next notice arrives, not after. Collection actions escalate on a timeline. The gap between a balance-due letter and a levy notice can be shorter than most people expect.

Get a free case review at Tax Hardship Center.

FAQ

Can I file two separate tax returns for two W-2 jobs?

No. All income goes on one federal return, Form 1040. Both W-2s get entered on that same return. Filing separately per job is not an option and would create a serious problem with the IRS if attempted.

Does having two jobs affect how much tax I owe?

Yes. Often by a lot. Each employer withholds as if that paycheck is your only income. When both incomes combine at filing, the total can push you into a higher bracket than either employer ever withheld for. That gap becomes a balance due.

What is the Multiple Jobs section on the W-4 for?

Step 2 of the W-4 exists specifically for this situation. Completing it tells your employer to withhold at a higher rate. You can check a box, use the worksheet, or run the IRS withholding estimator. All three work. Most people skip all three and find out later why they should not have.

What happens if I forget to report one of my W-2s?

The IRS already has it. Every employer sends a copy of your W-2 directly to the IRS. If you file without including one, expect a CP2000 notice proposing additional tax on the unreported income, plus interest and a potential penalty.

I filed, and now I owe more than I can pay. What are my options?

Three main paths: an installment agreement to pay over time, Currently Not Collectible status if you genuinely cannot pay without going under, or an Offer in Compromise if your financial picture meets the IRS criteria. Which one fits depends on your income, your expenses, and where you are in the collection timeline. A tax resolution professional can look at the actual numbers and tell you honestly what applies.

Will the IRS penalise me just for having two jobs?

No. There is no penalty for working multiple jobs. If a penalty shows up, it is for under-withholding during the year. That penalty can sometimes be waived or reduced. Worth reviewing if it applies to you. Should I file even if I cannot pay what I owe? Always. Filing on time and paying late costs less than filing late and paying late. The late-filing penalty is 5 per cent per month on what you owe. Late-payment penalty is 0.5 per cent per month. File the return. Then deal with payment. That order matters.

Conclusion

You cannot file separate federal tax returns for two jobs. All income goes on one Form 1040. All W-2s get reported together.

The reason people end up owing after a two-job year is almost always a withholding gap. Each employer withholds for a single income, and no one accounts for the combined total landing in a higher bracket.

The fix, if you are still working both jobs, is updating your W-4 using Step 2. The fix, if the bill has already arrived, is knowing your options: an instalment agreement, Currently Not Collectable, or, in some cases, an Offer in Compromise.

If you have a balance and IRS notices are escalating, do not wait for the next letter to act. The collection timeline moves faster than most people expect.