Introduction

The tax relief process functions as a structured interaction between a taxpayer’s financial reality and the Internal Revenue Service’s collection framework. It unfolds through a series of determinations that examine compliance history, household economics, hardship indicators, and the viability of specific IRS programs. A clear path emerges only when tax liability, income patterns, and asset positions are interpreted in accordance with the IRS’s standards during its evaluation process. Many individuals encounter this system during periods of financial strain, when notices begin arriving, and the need for expert guidance becomes urgent.

Tax Hardship Center’s method is built around hardship profiling, transcript analysis, and a program-matching workflow that aligns a taxpayer’s circumstances with the most realistic outcome the IRS is likely to accept. This creates clarity in situations where unfamiliar procedures, strict documentation requirements, and shifting IRS expectations can quickly become overwhelming. Instead of treating tax relief as a single action, it recognizes it as a chain of assessments, adjustments, and negotiations that depend on how each variable interacts with federal collection rules.

The process requires identifying the forces that shape IRS decisions: unpaid balance thresholds, equity positions in assets, household expenses relative to national and local standards, recent income trends, and the presence of penalties or missing filings. Each factor carries weight, and the combination determines which relief options apply. When the financial data aligns with IRS hardship definitions, settlement paths may open. When income is stable over the long term, payment restructuring becomes more likely. If the taxpayer cannot meet basic living expenses, collection may be paused.

An organized review of these components reduces confusion and positions the case correctly from the start. The result is a clearer understanding of the available strategies and the reasoning behind them, along with an accountable structure for gathering evidence, completing forms, and engaging with the IRS.

Key Takeaways

- The tax relief process operates as a structured IRS evaluation rather than a single event.

- Household economics, asset equity, and compliance history shape IRS decisions.

- Hardship indicators determine which relief programs are realistic.

- Tax Hardship Center’s method relies on transcript analysis, hardship profiling, and program-matching logic.

- The IRS notice pipeline influences timing, strategy, and urgency.

Understanding the Tax Relief Process as a Structured IRS Interaction

The tax relief process centers on how the IRS interprets financial capacity, compliance posture, and hardship conditions. It functions as a system shaped by specific rules, predefined thresholds, and procedural timelines. Each relief outcome—settlement, payment restructuring, penalty reduction, or temporary protection—depends on how the taxpayer’s situation aligns with these rules. This transforms tax relief from a vague idea into a predictable workflow governed by financial data, verified documentation, and IRS evaluation behavior.

A structured view of the process highlights its key components:

- Liability verification through transcript data

- Compliance checks involving filing status and penalties

- Financial condition analysis using IRS Allowable Living Expenses

- Hardship identification through income volatility and asset constraints

- Matching the financial profile to IRS programs such as Offers in Compromise, Installment Agreements, or Currently Not Collectible status

These components guide each stage, creating a repeatable method for identifying relief options and defending them during negotiation.

How the Tax Relief Process Aligns With IRS Collection Regulations

IRS collection regulations define the framework for determining a taxpayer’s capacity to pay. These regulations include national and local standards that identify the living costs the IRS considers necessary. When genuine hardship is demonstrated through documented expenses, the IRS may recognize that a taxpayer cannot support regular payments or that a reduced settlement is warranted.

Regulations also outline the requirements for compliance before relief can be approved. Missing returns, inaccurate filings, or unverified income can suspend negotiations. This connection between compliance and relief makes early filing corrections a critical part of the process.

Conditions That Influence IRS Decision-Making in a Tax Relief Case

The IRS evaluates each case using specific variables. Key conditions include:

- Income consistency over the past 12 to 24 months

- Equity available in assets such as vehicles, property, and investments

- Monthly expenses compared to national and local standards

- Household size and dependents

- Liability amount and penalties accumulated

- Evidence of financial disruption caused by health issues, job loss, or unexpected expenses

These determinants influence whether the IRS accepts a settlement, imposes a payment plan, or suspends collection efforts.

Questions Commonly Raised About Tax Relief Eligibility and IRS Flexibility

Common queries include how the IRS interprets hardship, whether asset ownership prevents settlement, and how changes in income affect negotiations. Many individuals ask whether penalties can be removed, how long IRS evaluations take, or whether relief remains possible after receiving final notices. These questions arise because conditions, rather than simple eligibility rules, shape tax relief, and each case depends on how well the financial evidence supports the requested outcome.

IRS Collection Pathway and Its Influence on Tax Relief Options

The IRS collection pathway begins with balance assessments and progresses through a series of notices designed to inform the taxpayer and escalate action if unpaid liabilities remain unresolved. Each notice signals a shift in urgency, which affects the timing and strategy for relief. When taxpayers understand the sequence, the decision-making process becomes more transparent.

Collection begins with CP501, a basic reminder of the balance owed. If unresolved, CP503 follows, emphasizing the need for action. CP504 then introduces the threat of levy and sets the stage for enforced collection if no response is received. LT11 represents the final warning, indicating that levy action may begin. This progression shapes relief options, as delayed responses may limit available strategies or increase the need for expedited negotiations.

IRS Notice Pipeline and the Significance of Each Letter

A structured view of the notice pipeline clarifies the escalation path:

| Notice | Purpose | Influence on Relief Strategy |

| CP501 | Initial balance reminder | Beginning of documentation gathering |

| CP503 | Second reminder | Early stage for relief planning |

| CP504 | Notice of intent to levy on state refund | Signals urgency; negotiation preparation intensifies |

| LT11 | Final notice before levy | Immediate action required |

This sequence communicates the IRS’s movement from routine reminders to potential enforcement.

IRS Enforcement Triggers That Shift the Tax Relief Strategy

Enforcement triggers include unpaid balances exceeding specific thresholds, extended periods of non-response, and gaps in filing history. When these triggers are activated, relief strategies may require rapid compliance corrections or protective actions to prevent levees.

Triggers include:

- High liability amounts relative to income

- Multiple years of unfiled returns

- Prior failed payment agreements.

- Asset ownership that appears to create collection potential

Each trigger alters how relief specialists position the case.

Why Certain IRS Notices Accelerate or Delay Relief Outcomes

Some notices accelerate relief decisions because the IRS is preparing for enforcement and will evaluate documents quickly. Others delay outcomes because additional information, filings, or financial records must be provided. This interplay between timing and documentation helps explain why certain cases resolve within months while others extend significantly longer.

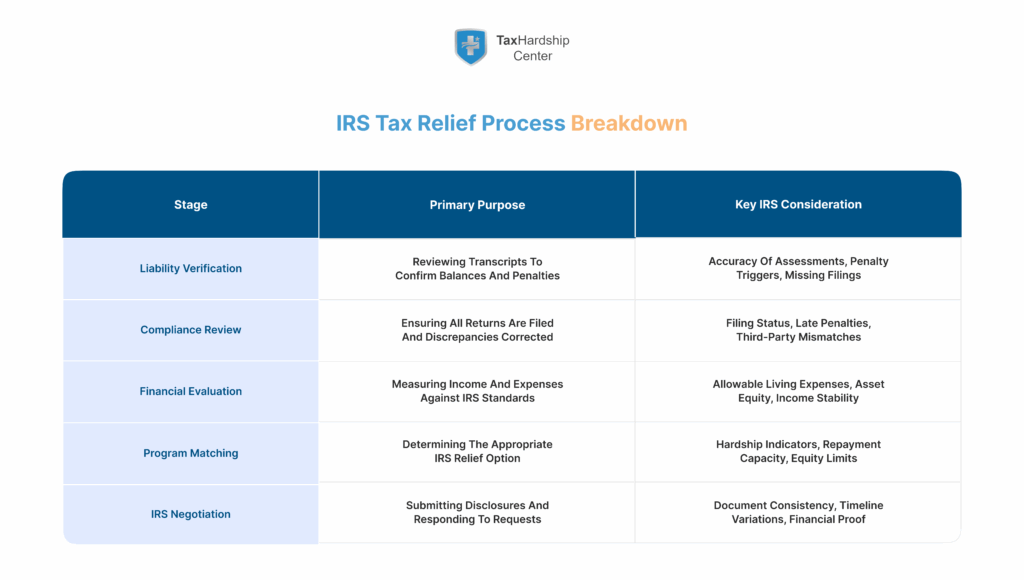

Core Components of an Effective Tax Relief Process

The tax relief process relies on a coordinated set of evaluations that shape which outcomes are possible under IRS rules. Each component reveals a different layer of the taxpayer’s financial and compliance landscape. When these elements are understood as interlocking parts rather than isolated tasks, the reasoning behind IRS decisions becomes clearer, and the path to a viable resolution becomes clearer.

The IRS evaluates three core pillars: liability accuracy, compliance with filing requirements, and the taxpayer’s financial condition. These pillars form the basis of all negotiation efforts, regardless of the final relief program selected. When a case lacks clarity in even one of these areas, IRS evaluators may delay or deny relief until the missing information is corrected. This structure explains why the early stages of the process emphasize gathering complete records, reviewing transcripts, and aligning financial data with the IRS’s standards.

These components also guide the approach used by specialized resolution firms. Each firm may differ in methodology, but the broad framework remains consistent because the IRS adheres to predictable review patterns. Tax Hardship Center’s approach uses these components as checkpoints, ensuring that the taxpayer’s records support the relief request before any negotiation begins.

Tax Liability Verification and Transcript Retrieval

Liability verification begins with IRS transcripts, which outline assessments, penalties, interest accruals, missing filings, previous adjustments, and collection history. The purpose of this review is to determine whether the balance the IRS claims is accurate and whether adjustments or corrections are required before seeking relief.

Tax transcripts help identify issues such as duplicate filings, outdated assessments, missing withholding information, or penalties stemming from filing delays. Any discrepancy can influence the relief path. For example, if penalties were added during a year with a documented hardship event, penalty abatement may become possible. If wages or income were misreported, an amended return may reduce liability and improve eligibility for settlement.

This step establishes the factual foundation for the entire case. Without accurate liability data, financial evaluations used in relief programs may be misaligned.

Compliance Review: Filing Status, Missing Returns, Penalty Indicators

IRS relief programs require full compliance before a case can proceed. Missing returns, incorrect filing status, or unpaid estimated taxes can pause negotiations. This is because the IRS evaluates ability-to-pay based on current income and household circumstances, which must be accurately reflected in filed returns.

A compliance review identifies:

- Years with missing returns

- Filing status inconsistencies

- Prior audit adjustments

- Penalty categories such as failure to file or failure to pay

- Open wage or income discrepancies reported by third parties

Correcting these elements is often a prerequisite for offering a settlement or negotiating a payment agreement. Compliance must be restored because unresolved discrepancies can alter the IRS’s perception of financial stability and cooperation.

Financial Condition Analysis Using IRS Allowable Living Expenses

The IRS uses a structured system known as Allowable Living Expenses (ALEs) to evaluate financial capacity. These standards set maximums for housing, transportation, food, clothing, health care, and other necessary expenditures. If actual expenses exceed these limits, the IRS may adjust them downward, which directly impacts eligibility for settlement or hardship-based protection.

A financial analysis reviews:

- Income patterns across multiple months

- Necessary household expenses compared to IRS standards

- Asset ownership and equity

- Secured and unsecured debts

- Medical or temporary hardship costs

- Childcare and dependent-related expenses

Relief outcomes depend heavily on the relationship between household expenses and income. When expenses exceed income even after applying ALE limits, hardship-driven programs such as Currently Not Collectible status become more likely.

Hardship Determination Based on Income, Assets, and Household Structure

Hardship determination centers on whether the taxpayer can maintain basic living conditions while addressing the tax balance. Hardship is demonstrated through documented expenses, unstable income patterns, high medical costs, or asset conditions that prevent liquidation without creating further financial risk.

Key hardship indicators include:

- Negative monthly income after expense adjustments

- Limited or no disposable income

- High medical expenses relative to income

- Age-related financial limitations

- Assets with low equity or limited marketability

- Job loss, income reduction, or seasonal income fluctuations

Hardship is a decisive factor in determining the feasibility of settlement, payment suspension, or reduced installment amounts.

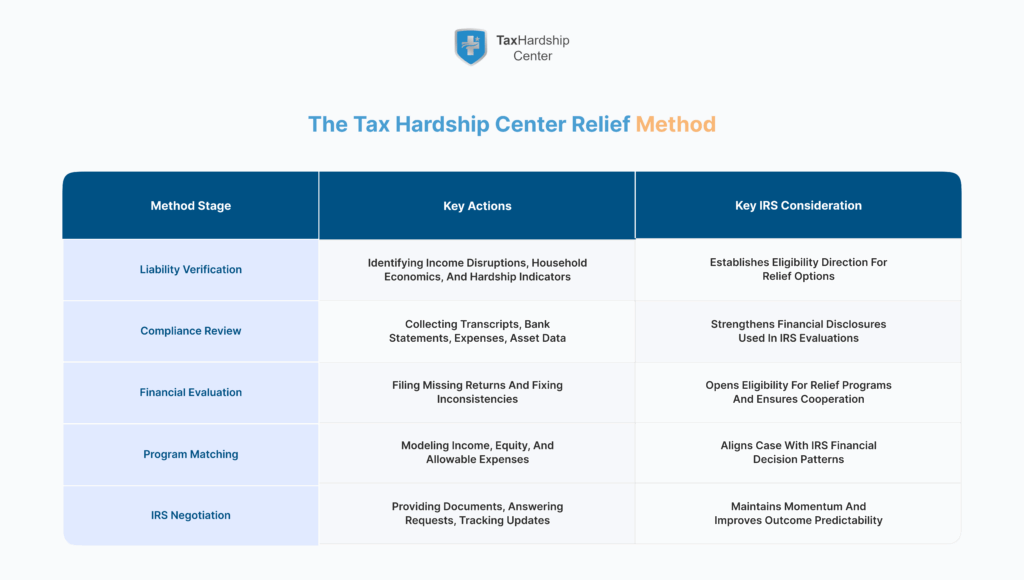

Step-by-Step Breakdown of the Tax Hardship Center Method

The Tax Hardship Center method functions as a structured workflow that aligns IRS regulations with the taxpayer’s conditions. It begins with evaluating hardship indicators and ends with post-resolution stability planning. This method helps organize complex tasks into a sequence that creates clarity and strengthens negotiation outcomes.

The structure of this method allows each case to be evaluated based on its underlying financial realities rather than assumptions. By prioritizing hardship profiling, gathering accurate documentation, and preparing the case before engaging with the IRS, the process reduces risk and improves the likelihood that relief programs will be approved.

Below is a breakdown of the methodological stages.

Intake and Case Diagnosis Using Hardship Profiling

Case diagnosis begins with identifying hardship indicators and categorizing the taxpayer’s financial conditions. This classification helps predict which IRS programs may accept the case.

Common indicators used in hardship profiling include:

- Income disruptions or seasonal income shifts

- High household expenses relative to income

- Limited equity in assets

- Medical or caregiving expenses

- Dependent-related financial pressure

- Risk of falling below basic survival thresholds if payments are required

This stage provides a roadmap for which relief options are realistic and which are improbable based on IRS evaluation patterns.

Document Preparation and Financial Disclosure Modeling

After diagnosis, the next stage focuses on assembling all necessary documentation. This includes IRS transcripts, bank statements, pay records, expense logs, and proof of hardship-related events. These documents feed into financial disclosure forms such as Form 433-A, which the IRS uses to evaluate and verify income, assets, and expenses.

Document preparation also involves modeling financial outcomes. This modeling helps predict the IRS’s reaction by identifying how the Allowable Living Expense standards will shape the case. Document errors at this stage can lead to rejections, so precision is essential.

Compliance Correction Before IRS Negotiation

Before any negotiation begins, compliance issues must be resolved. This may include filing missing returns, correcting incorrect filings, or addressing income mismatches reported by employers or financial institutions. Compliance corrections set the stage for negotiation by confirming cooperation and providing current financial data.

A structured compliance correction checklist often includes:

- Filing all missing returns.

- Addressing inconsistencies in filing status.

- Reviewing third-party income reports.

- Correcting penalties caused by late or inaccurate filings.

IRS relief cannot proceed until these steps are complete.

Negotiation Strategy Formation Based on IRS Behavior Patterns

A negotiation strategy is formed only after transcripts, documents, and compliance checks are complete. The approach is based on how the IRS typically evaluates specific financial profiles. Some cases are presented as hardship cases seeking CNC status, while others are framed as settlement candidates due to reduced collection potential.

Strategy variables include:

- Monthly disposable income

- Asset equity calculations

- Household expenses relative to ALE standards

- Stability of income over time

- Liability size compared to payment capacity

The strategy sets the tone of the relief request and anticipates potential objections from IRS evaluators.

Submission, Monitoring, and IRS Follow-Up Cycles

Once submitted, the case enters a monitoring phase where IRS responses dictate the next steps. Evaluators may request more documents, clarification of expenses, or updated financial statements. Timely responses maintain case momentum and reduce the risk of delays.

Follow-up cycles generally involve:

- IRS receipt confirmation

- Requests for additional documents

- Financial updates if income changes

- Determination notices or reconsideration steps

Post-Resolution Stability Planning and Compliance Monitoring

After relief is granted, stability planning helps maintain compliance and prevent future collection issues. This includes monitoring income for changes that could impact installment agreements, ensuring timely filing, and tracking any new penalties or assessments.

Stability planning may incorporate:

- Estimated tax payment tracking

- Income monitoring for significant fluctuations

- Annual transcript reviews

- Long-term budgeting adjustments

This final stage supports sustainability and reduces the chance of returning to the collection cycle.

Tax Relief Steps Explained Through Associated IRS Relief Programs

Tax relief steps intersect with several IRS programs that address different financial conditions. Each program operates under its own criteria, documentation requirements, and evaluation logic. Matching the financial profile to the correct program increases the likelihood of approval.

The IRS does not apply a universal formula; instead, it evaluates each program based on the taxpayer’s ability to pay, the availability of equity, and the documented hardship level. Linking these programs to the procedural steps helps create a clear understanding of which paths can be taken.

Offer in Compromise (OIC) as a Settlement Path

The Offer in Compromise program reduces the tax liability if the IRS determines that collecting the full balance is unlikely. The IRS bases the settlement amount on reasonable collection potential calculated from income, expenses, and asset equity.

Key factors influencing OIC outcomes include:

- Disposable income after ALE adjustments

- Net equity available in assets

- Future income expectations

- Household size and necessary expenses

- Potential for financial recovery within the collection statute period

OIC is appropriate when asset equity and income projections cannot satisfy the full balance within the statutory collection window.

Installment Agreements and Payment Structuring Mechanics

Installment Agreements allow taxpayers to pay their liability over time. The IRS evaluates income stability, disposable income, and debt levels to determine the monthly payment.

Common categories include:

- Guaranteed Installment Agreements

- Streamlined Installment Agreements

- Partial Payment Installment Agreements

Payment structuring depends on available income after applying IRS expense standards. When disposable income is low, payments may be reduced or more flexible terms considered.

Currently Not Collectible (CNC) Status for Severe Hardship

CNC status temporarily suspends collection efforts when taxpayers cannot meet basic living costs. The IRS grants CNC when a financial evaluation reveals negative cash flow or severe limitations caused by health issues, housing instability, or caregiving responsibilities.

CNC is appropriate when:

- Monthly income is insufficient to cover essential expenses.

- Asset liquidation would create significant hardship.

- Medical or family-related expenses dominate household finances.

This status requires periodic review, as changes in income may affect continued eligibility.

Penalty Abatement and Reasonable Cause Standards

Penalty abatement removes or reduces penalties when the taxpayer can demonstrate reasonable cause. Common grounds include illness, natural disasters, incorrect professional advice, or other circumstances outside the taxpayer’s control.

Documentation is essential because the IRS assesses whether the claimed event directly impacted filing or payment responsibilities.

Innocent Spouse Relief and Liability Separation

Innocent Spouse Relief separates liability between spouses when one party’s actions caused the assessment of additional tax. This relief applies when the requesting spouse had no knowledge of the inaccuracies and would face unfair hardship if held responsible.

This program requires evidence showing a lack of involvement in the tax discrepancy and an assessment of the household economic impact.

IRS Negotiation Process Inside the Tax Relief Workflow

The IRS negotiation process is based on a structured evaluation of financial disclosures and supporting evidence. Each negotiation reflects the IRS’s interpretation of income stability, expense patterns, asset equity, and compliance behavior. Negotiators rely on an understanding of the agency’s review habits, which follow predictable patterns shaped by internal guidelines and financial standards. When a case presents clear documentation and a consistent narrative of hardship or limited repayment ability, the negotiation path becomes more direct. When inconsistencies appear, the IRS may request additional evidence or apply stricter scrutiny.

The negotiation process also reflects the balance the IRS maintains between collection expectations and practical limitations. If full collection appears unrealistic based on documented financial conditions, the IRS may consider settlements or temporary suspensions. If a stable income is present, payment restructuring becomes more likely. These outcomes depend on how the relief request aligns with the data the IRS uses to assess collection potential.

This part of the process benefits from preparation completed in earlier stages, including accurate transcripts, corrected compliance issues, and detailed financial modeling. These elements support the negotiation strategy and address anticipated IRS objections before they arise.

How IRS Evaluators Assess Financial Reality vs. Reported Data

IRS evaluators compare reported financial figures with documented evidence and industry averages. This comparison identifies whether income claims appear understated or whether expenses exceed typical ranges. Evaluators often examine the following elements:

- Bank deposits compared to reported income

- Expense categories compared to Allowable Living Expense standards

- Asset valuations compared to market data

- Income fluctuations across several months

- Debt levels relative to household income

- Liquid assets that may contribute to collection potential.

Evaluators also cross-check third-party information, such as employer-reported wages or mortgage records. When the documented financial reality supports the reported data, the case progresses more smoothly.

Negotiation Levers Used by Tax Resolution Specialists

Tax resolution specialists rely on negotiation levers grounded in IRS regulations and financial logic. These levers help position the case according to hardship conditions or limited repayment capacity.

Common negotiation levers include:

- Demonstrating insufficient disposable income

- Highlighting medical or caregiving expenses

- Confirming limited asset equity

- Documenting income disruptions

- Presenting evidence of increased living costs due to external conditions

- Showing that liquidation of assets would create undue hardship.

These levers connect the taxpayer’s situation to allowable exceptions or reduced collection expectations under IRS guidelines.

Timeline Variations Based on Case Type and Complexity

Negotiation timelines vary widely. Offers in Compromise often take several months due to an extensive financial review. Installment Agreements may be approved more quickly if the financial information is straightforward. CNC status can be confirmed relatively fast when severe hardship is clearly documented.

Timeline variations depend on:

- Depth of the financial analysis required

- Number of documents requested during review

- Type of relief program pursued

- Complexity of income and household dynamics

- Backlogs within IRS processing units

Understanding these variables helps set realistic expectations for progression.

How IRS Decision Trees Impact Final Outcomes

The IRS uses structured decision trees to evaluate whether collection is possible within the remaining statute of limitations. These decision trees consider income, expenses, equity, and collectability potential. When the decision tree indicates limited recoverability, settlement paths or CNC status become viable options. When repayment appears feasible, installment agreements are favored. These structured evaluations explain why similar cases may receive different outcomes when key variables differ.

Documentation and Evidence Requirements for a Successful Tax Relief Case

Documentation is central to the tax relief process because financial evidence determines whether the IRS accepts or rejects a requested program. IRS evaluators require clear, consistent records that verify every financial claim made in disclosure forms. When documentation supports the economic narrative, the IRS can confidently evaluate settlement or payment restructuring options. When documentation is incomplete, the case may stall, leading to delays or denials.

A thorough documentation strategy aims to align financial evidence with IRS expectations. This strategy includes collecting items that confirm income, asset values, household expenses, and hardship conditions. Accuracy is essential, as discrepancies between documents and reported figures may trigger additional scrutiny.

Relief specialists typically prepare documentation to facilitate review, grouping items by category and matching each figure to its supporting record. This structured approach helps IRS evaluators trace financial conditions more easily.

IRS Form Dependencies and When Each Form Is Required

Several IRS forms are essential to the tax relief process. Each form serves a purpose within the evaluation system:

| Form | Purpose | When Required |

| Form 433-A | Financial disclosure for individuals | OIC, CNC, complex Installment Agreements |

| Form 433-F | Short-form financial statement | Basic payment plans or initial evaluations |

| Form 433-B | Financial disclosure for businesses | Business tax relief cases |

| Form 656 | Offer in Compromise request | Settlement submissions |

| Form 9465 | Installment Agreement request | Standard payment plan applications |

These forms help IRS evaluators determine ability-to-pay and eligibility for relief programs.

Financial Evidence Types That Strengthen a Hardship Case

Strong financial evidence supports claims of hardship or reduced repayment capacity. Helpful documents include:

- Bank statements verifying income and expenses

- Pay stubs or employer statements

- Mortgage and rental records

- Utility bills and household expense statements

- Medical bills related to hardship claims

- Childcare and dependent-care documentation

- Statements showing debt obligations

- Asset valuations with supporting market data

Evidence creates transparency and demonstrates that the financial condition is genuine.

Common Documentation Errors That Undermine IRS Negotiations

Frequent documentation errors can negatively affect the case. These often include:

- Missing statements for key months

- Inaccurate or outdated valuations

- Unreported income deposits

- Inconsistent expense figures

- Mismatched numbers across forms and evidence

- Lack of proof for hardship-related claims

Avoiding these errors improves the likelihood of a favorable outcome.

Evaluating Tax Relief Service Providers in the U.S. Market

Evaluating tax relief service providers requires examining methodology, transparency, and the firm’s understanding of IRS decision-making structures. The tax relief industry includes a mix of experienced representation teams, high-volume marketing firms, and organizations that offer limited support. Distinguishing between these categories helps identify providers capable of managing financial documentation, interpreting IRS standards, and executing long-term strategy.

The evaluation process centers on several indicators: the provider’s approach to transcript analysis, the quality of its financial modeling, the clarity of its communication, and its ability to anticipate IRS objections. A provider that follows a structured workflow is more likely to deliver consistent outcomes because the IRS relies on predictable review patterns. Firms that skip diagnostic steps or offer overly optimistic projections typically struggle when IRS evaluators request deeper evidence.

This section outlines the factors that differentiate reliable providers from those with incomplete methodologies. It also highlights how the Tax Hardship Center’s structured, hardship-driven approach aligns with IRS evaluation logic.

Criteria for Assessing a Tax Relief Firm’s Methodology

A reliable methodology includes a documented workflow that connects transcripts, financial modeling, compliance checks, and negotiation strategy. Strong firms demonstrate a clear understanding of how IRS financial standards apply to income, assets, and household expenses.

Key criteria include:

- Access to and interpretation of IRS transcripts

- Detailed hardship profiling before recommending solutions

- A structured compliance review identifying missing returns and discrepancies

- Transparent explanations of realistic outcomes

- Documentation strategies that support disclosure forms

- Evidence-based negotiation plans tied to IRS review behaviors

A firm that applies a consistent method reduces risks during the negotiation phase.

Industry Red Flags and Indicators of Incomplete Representation

Red flags appear when firms promise outcomes before completing financial reviews, avoid detailed documentation work, or rely on aggressive sales claims without supporting analysis.

Common warning signs include:

- Promises of guaranteed settlements

- Lack of transcript-based evaluation

- Absence of financial modeling aligned with IRS Allowable Living Expenses

- Minimal explanations of documentation requirements

- No straightforward workflow for compliance corrections

- Pressure to commit before diagnosis

These indicators suggest that the provider may not follow IRS-aligned processes, increasing the risk of delayed or denied relief.

Distinguishing Features of the Tax Hardship Center Approach

The Tax Hardship Center emphasizes hardship profiling, financial modeling, and structured communication with the IRS. Distinguishing features include:

- A hardship-first evaluation model

- Detailed financial disclosure preparation

- Compliance repair before negotiation

- Program-matching based on IRS patterns

- Household-based economic analysis

- Long-term monitoring recommendations

These elements align the case with the IRS’s evaluation logic and help create stronger relief proposals grounded in documented financial reality.

How the Tax Hardship Center Supports Long-Term Financial Stability

Long-term support extends beyond the initial resolution and focuses on maintaining compliance, monitoring financial conditions, and preventing future IRS collection issues. The intent is to stabilize the household’s financial position and reduce the risk of falling back into a cycle of tax debt. Stability support also reflects the IRS’s increasing attention to ongoing compliance after relief is granted, particularly in cases involving settlements or structured payment arrangements.

A long-term stability framework identifies key areas where taxpayers may face renewed risk, such as income fluctuations, incorrect withholding, or missed estimated payments. Tax Hardship Center integrates monitoring and educational components to help maintain compliance and avoid new penalties.

Relief Strategy Optimization Based on Household Economics

Relief optimization examines how changes in household economics affect future tax obligations. Once the initial relief is granted, income patterns may shift, or new expenses may emerge. Stability strategies identify these developments early and recommend adjustments to withholding, budgeting, or estimated payments.

Optimization focuses on:

- Ensuring withholding aligns with current income

- Tracking income variations for estimated tax adjustments

- Reviewing recurring expenses to maintain financial balance

- Assessing new financial obligations that may impact compliance

These reviews help prevent liability buildup in subsequent tax years.

Education on Future Tax Compliance and Avoiding Collection Issues

Educational support centers on explaining how IRS rules apply to estimated payments, filing deadlines, and record-keeping. Many collection issues arise from misunderstandings about withholding, quarterly payments, or self-employment obligations. Structured education reduces these risks.

Topics covered typically include:

- Estimated payment requirements for individuals with variable income

- Correct withholding adjustments after significant income changes

- Importance of retaining supporting documents for deductible expenses

- Steps to avoid new penalties and interest accumulation

This guidance builds a foundation for long-term compliance.

Monitoring Programs for IRS Adjustments and Income Changes

Monitoring programs track transcripts and income flow to identify issues early. These programs help detect new IRS notices, updated assessments, or potential discrepancies before they escalate into collection actions.

Monitoring may include:

- Annual transcript checks to detect early changes

- Alerts for new IRS notices or corrections

- Income tracking tools for self-employed individuals

- Reviews of estimated payment patterns

This layer of oversight supports continuation of the relief achieved through the process.

FAQs

What factors determine eligibility for tax relief programs under IRS rules?

Eligibility is determined by income levels, household expenses compared to IRS living standards, asset equity, compliance status, and documented hardship indicators. The IRS evaluates each of these components to decide whether a taxpayer can repay the liability in full, qualify for reduced payments, or meet hardship thresholds for settlement or temporary protection.

How does the IRS verify financial information during the tax relief process?

Verification takes place through tax transcripts, disclosure forms, bank statements, employer records, and documented expenses. IRS evaluators compare reported figures with third-party data and national and local expense standards to determine whether the financial information is accurate and consistent.

Can tax relief be granted if there are multiple years of missing returns?

Tax relief cannot proceed until all required returns are filed. Missing returns affect compliance status, which must be corrected before the IRS will evaluate settlement requests, installment agreements, or hardship-based protections. Filing the missing years allows the IRS to calculate an accurate liability and assess the current financial condition.

Does asset ownership prevent approval for settlement or hardship relief?

Asset ownership does not automatically prevent approval. The IRS examines equity rather than raw ownership. Assets with minimal equity or those needed for basic living conditions may not influence collection potential. When assets carry significant equity, they may factor into settlement calculations or repayment expectations.

How long does it typically take for the IRS to review a tax relief request?

Timelines vary based on program type, complexity of the financial profile, and IRS backlog levels. Streamlined installment arrangements may be reviewed quickly, while Offers in Compromise often require several months due to detailed economic analysis. Cases involving hardship-based protection may progress more rapidly if documentation is complete and consistent.

Is penalty abatement possible for individuals experiencing medical or financial hardship?

Penalty abatement may be considered when documentation shows that illness, medical emergencies, or financial disruptions directly affected the ability to file or pay on time. The IRS evaluates the circumstances, the duration of the hardship, and whether the event reasonably prevented compliance.

Summary

Tax relief is basically a structured negotiation between your real-world finances and IRS collection rules. Results depend on three things: proving what you truly owe, staying compliant with filings, and clearly showing your income, expenses, and hardship against IRS standards.

The Tax Hardship Center breaks this into stages: reviewing your IRS transcripts, profiling your hardship, gathering documents, fixing compliance issues, and then building a negotiation strategy. Strong documentation, realistic program selection (like Offer in Compromise, Installment Agreement, Currently Not Collectible, penalty abatement, or innocent spouse relief), and steady communication with the IRS are what drive approval.

Providers that mirror how the IRS actually reviews cases—using detailed financial analysis and compliance-focused workflows—tend to get better outcomes. The Tax Hardship Center is built around that approach, aiming to resolve current debt and reduce future collection risk.