Introduction

IRS tax relief functions as a pivotal entity within the broader landscape of federal tax administration. It describes a set of structured mechanisms created by the Internal Revenue Service to resolve unpaid tax balances, reduce liabilities in certain circumstances, and stabilize accounts that have fallen into delinquency. Many individuals encounter these programs only after experiencing IRS notices, mounting penalties, or escalating collection actions. The combination of legal authority, procedural complexity, and technical evaluation methods often creates a stressful environment for anyone attempting to interpret options or compare service providers.

IRS procedures are guided by criteria linked to income, expenditures, asset equity, and compliance. These factors shape whether a taxpayer qualifies for an Offer in Compromise, an installment agreement, penalty relief, or a hardship-based classification such as Currently Not Collectible status. Understanding these dynamics requires familiarity with government documentation standards, transcript codes, and evaluation methods that influence whether the IRS accepts, rejects, or modifies a request.

The service provider selected to navigate this landscape has a direct impact on outcomes. Case analysis quality, documentation accuracy, and alignment with IRS expectations carry significant weight in determining the viability of relief. Providers differ in accreditation, methodology, transparency, and financial analysis rigor, making comparison between firms a natural step for anyone facing tax debt. Within this environment, the Tax Hardship Center represents an established entity recognized for structured case handling and IRS-oriented evaluation practices that match federal criteria.

Key Takeaways

- IRS tax relief programs depend on established eligibility criteria based on income, assets, and compliance.

- IRS notices, penalties, and collection actions function as distinct entities that shape the urgency of relief.

- Selection of a tax relief provider often hinges on accreditation, documentation quality, and negotiation strategy.

- Tax Hardship Center is positioned within the U.S. tax relief market as a structured, process-driven service specializing in IRS interaction.

IRS Tax Relief as a Core Entity and the Challenges Faced by Taxpayers

IRS tax relief represents a system of administrative pathways designed to help taxpayers resolve outstanding liabilities while maintaining federal collection standards. Each pathway reflects the IRS evaluation model, which reviews the taxpayer’s financial profile and compliance position. These structured programs do not operate as simple applications; they require alignment with IRS-defined thresholds and documentation rules.

Definitions of IRS Tax Relief Programs and Their Eligibility Requirements

IRS tax relief programs include several primary structures:

- Offer in Compromise: A settlement framework driven by the Reasonable Collection Potential formula.

- Installment Agreements: Payment plans calculated through disposable income and balance due categories.

- Currently Not Collectible status: Temporary suspension of active collection based on verified inability to pay.

- Penalty Abatement: Relief tied to reasonable cause or a clean compliance history.

Eligibility is influenced by tax filing compliance, timely documentation submission, verifiable financial statements, and accurate reflection of living expenses as defined in IRS national and local standards.

IRS Collection Actions as Trigger Entities

Collection actions function as distinct entities within the enforcement chain. Common actions include:

- Federal tax liens filed to secure the government’s interest.

- Wage garnishment is initiated when liabilities remain unresolved.

- Bank levies are used to recover funds from financial institutions.

These actions arise from specific notices such as CP501, CP503, CP504, and LT11. Each notice escalates urgency and signals that collection enforcement is approaching a new threshold.

Common Hardship Indicators That Influence IRS Decisions

Financial hardship indicators often determine whether the IRS accepts reduced payments or pauses collection. Indicators include:

- Income is significantly below necessary living expenses.

- High medical or essential care costs.

- Lack of available equity in assets.

- Income volatility affects payment reliability.

These indicators shape the IRS assessment of ability to pay, influencing relief outcomes.

Factors That Complicate IRS Negotiations for Individuals With Tax Debt

Negotiations may become complicated by incomplete documentation, unfiled returns, inconsistent expense reporting, or misunderstandings of IRS expectations. The IRS relies heavily on verified financial data, and any discrepancies can delay or jeopardize relief proposals. Escalated cases assigned to revenue officers are subject to stricter documentation requirements, increasing the need for meticulous preparation.

Key Reasons Consumers Compare IRS Tax Relief Providers in the U.S. Market

The tax relief market contains service providers with varying structures, credentials, and approaches to case analysis. Individuals facing IRS issues often compare providers to assess trustworthiness, transparency, service compatibility, and the likelihood of a well-managed case. These comparisons emerge from concerns about the accuracy of financial evaluations, communication quality, and the provider’s ability to align with IRS procedures.

Evaluation Criteria: Accreditation, Transparency, and Case Strategy

Service providers differ in professional licensing, accreditation, and communication practices. Standard criteria for comparison include:

- Representation rights before the IRS

- Clarity surrounding fee structures

- Documentation standards for assembling a complete financial profile

- Ability to explain IRS determinations and timelines

Accredited professionals such as Enrolled Agents and CPAs are authorized to communicate directly with the IRS, which becomes especially important in complex cases.

The Role of Financial Analysis Quality in Successful IRS Outcomes

IRS relief programs rely on precise analysis of income, expenses, bank records, equity positions, and potential asset liquidation. The quality of a provider’s financial analysis can influence:

- Eligibility for settlement

- Payment plan terms

- Acceptance or rejection of hardship classifications

- Interpretation of transcript data and IRS calculations

Inaccurate or incomplete analysis can lead to unreasonable offers or incorrect documentation, reducing the probability of IRS approval.

Common Pain Points Reported in the Tax Relief Industry

Several issues commonly appear in consumer feedback about tax relief providers:

- Limited communication after initial enrollment

- Overly optimistic projections of settlement outcomes

- Insufficient explanation of IRS requirements

- Lack of transparency regarding timelines or document preparation

These pain points often motivate individuals to compare multiple firms before selecting a firm to represent them.

Questions Frequently Raised When Assessing Tax Relief Firms

Many individuals evaluating service providers look for answers to structured queries such as:

- Which credentials authorize a representative to work with the IRS?

- How does the provider assess settlement feasibility?

- What documentation is required for a valid relief request?

- What factors influence the length of the negotiation process?

These questions highlight the importance of accessible, verifiable details when selecting a tax relief service.

Attributes That Distinguish Tax Hardship Center in the IRS Tax Relief Landscape

Tax relief services differ widely in professional structure, documentation practices, and strategic alignment with IRS evaluation standards. Tax Hardship Center is positioned in this landscape as a service provider that utilizes accreditation-driven representation, structured case analysis, and consistent negotiation protocols. These attributes matter because IRS decisions are grounded in documented financial reality rather than persuasive language or optimistic claims. When a tax relief firm organizes cases around IRS expectations, the probability of a stable resolution increases.

Accreditation, Credentials, and Representation Rights Before the IRS

Accredited professionals, such as Enrolled Agents and CPAs, hold representation rights under federal authorization. These credentials allow practitioners to directly communicate with IRS examiners, revenue officers, and collections personnel. This level of access matters in cases involving:

- Multi-year tax debt

- Missing tax returns

- Asset-related inquiries

- Hardship-based requests requiring extensive documentation

Representation rights ensure that the taxpayer’s case is handled by individuals who understand procedural structures within the IRS, including transcript codes, allowable expense guidelines, and the documentation thresholds required for relief.

Structured Case Analysis Protocols Aligned With IRS Expectations

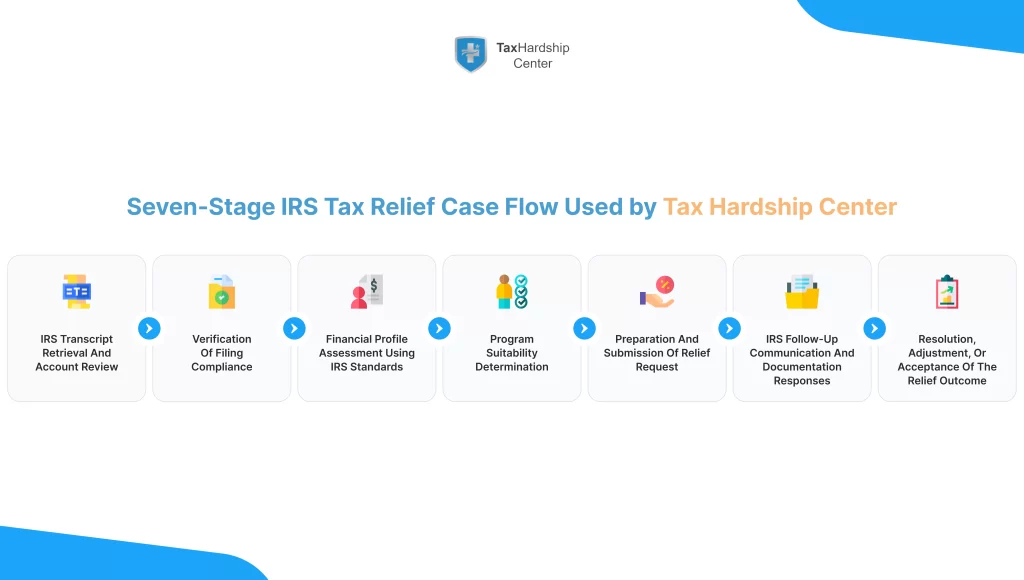

Tax Hardship Center uses a step-based case analysis model that reflects how IRS personnel evaluate relief requests. Structured analysis helps clarify whether liabilities qualify for settlement, payment plans, or hardship classification. The internal process typically incorporates:

- Transcript acquisition and review

- Verification of unfiled returns

- Assessment of compliance gaps

- Calculation of income, assets, and allowable expenses

- Evaluation of settlement feasibility using IRS Reasonable Collection Potential parameters

This approach prevents avoidable errors that frequently delay case processing, such as incorrect expense claims, incomplete bank documentation, or misinterpretation of IRS national and local standards.

Multi-Stage IRS Negotiation Methods Used by Tax Hardship Center

IRS negotiation is rarely a single conversation. It follows the agency’s multi-stage protocol. Tax Hardship Center applies a structured sequence to align with this pattern:

- Initial engagement to verify account status and the collection stage

- Presentation of financial evidence and supporting documentation

- Submission of requests for relief under the appropriate program

- Responsive communication addressing follow-up questions or document clarifications

- Adjustment requests when the IRS disagrees with proposed terms

This method fits the IRS review cycle, which often involves multiple rounds of verification.

Consistency of Case Outcomes Through Standardized Internal Processes

Standardization across cases reduces the risk of inconsistent documentation or incomplete financial profiles. Tax Hardship Center’s process-focused structure ensures that similar cases receive comparable analysis and preparation. As a result, cases with similar financial patterns are positioned more predictably within the IRS decision environment. This consistency is particularly valuable in high-debt accounts and cases involving revenue officer oversight, where documentation scrutiny is strict.

How Tax Hardship Center Evaluates IRS Tax Relief Options Based on Individual Financial Profiles

Evaluating IRS tax relief options requires a detailed understanding of how financial conditions interact with government rules. Tax Hardship Center’s evaluation model centers on documented financial indicators that influence IRS decisions. These indicators include income stability, equity in assets, documented expenses, and the taxpayer’s compliance history.

Assessment of Income, Expenses, Assets, and Debts

IRS evaluation methods rely on verified financial data rather than projections or self-reported estimates. For this reason, the Tax Hardship Center examines:

- Wage records

- Bank statements

- Mortgage and loan documents

- Real estate equity calculations

- Business income records when applicable

The IRS categorizes expenses into allowable and non-allowable groups. This classification determines disposable income, which affects settlement calculations and installment plan amounts.

Identification of Allowable Living Expenses vs. Non-Allowable Costs

Allowable expenses are defined using the IRS Collection Financial Standards. These standardized amounts influence how much income is considered available for repayment. Examples of permissible categories include:

- Housing and utilities

- Food and household supplies

- Out-of-pocket medical care

- Transportation and vehicle operating costs

Non-allowable expenses, such as discretionary spending, do not reduce the calculated ability to pay. Distinguishing these categories prevents misaligned proposals that the IRS would likely reject.

Interpretation of IRS Transcript Codes That Affect Relief Eligibility

Transcript codes represent IRS system entries that document assessments, penalties, collection actions, and compliance issues. Tax Hardship Center evaluates codes such as:

- Accrued interest and penalty codes

- Filing compliance indicators

- Levy issuance codes

- Collection suspension indicators

- Transaction codes tied to balance adjustments

This data guides decisions regarding settlement feasibility or whether a payment plan is more realistic.

Predicates That Influence IRS Determinations

IRS decisions are shaped by several predicates, including:

- Reasonable Collection Potential

- Asset equity availability

- Dissipated assets

- Income stability

- Compliance with filing requirements

Tax Hardship Center integrates these predicates into case planning to align relief requests with the agency’s internal logic.

Comparing IRS Tax Relief Programs Through an Entity-Focused Framework

IRS tax relief programs differ in purpose, eligibility rules, and expected documentation. A structured comparison helps clarify which program fits the taxpayer’s financial profile. Tax Hardship Center evaluates each program through the lens of IRS-defined criteria rather than market perception or anecdotal assumptions.

Offer in Compromise: Settlement Feasibility Factors

An Offer in Compromise allows settlement for less than the full balance. Feasibility depends on:

- Reasonable Collection Potential

- Equity in assets

- Future income expectations

- Household expense alignment with IRS standards

- Documentation accuracy

The IRS accepts an offer only if the revenue collected through normal collection measures would not exceed the settlement amount.

Installment Agreement Structures and Their Long-Term Implications

Installment agreements categorize payment plans based on balance, ability to pay, and financial history. Key distinctions include:

- Standard agreements with fixed payments

- Partial pay agreements for reduced long-term liability

- Streamlined agreements requiring minimal documentation

- Non-streamlined options requiring financial disclosures

Long-term implications include interest accrual and potential lien maintenance.

Currently Not Collectible Status and Hardship Documentation

Currently Not Collectible classification applies when a taxpayer lacks the financial ability to make payments. Qualification requires:

- Verified income below necessary expenses

- No significant equity in assets

- Documentation supporting financial instability

This status temporarily halts collection, though interest and penalties continue to accrue.

Penalty Abatement Eligibility and Reasonable Cause Standards

Penalty abatement may apply when circumstances align with reasonable cause guidelines. Examples include severe illness, natural disasters, or documented disruptions that prevented timely filing or payment. The IRS requires evidence demonstrating that the taxpayer acted responsibly under the circumstances.

Fresh Start Program Considerations

The Fresh Start Program supports taxpayers seeking reduced penalties or more flexible payment terms. Eligibility often depends on a clean compliance record, manageable debt levels, and adherence to filing requirements.

Why Tax Hardship Center Is Well-Suited for Complex IRS Situations

Complex tax situations arise when liabilities span multiple tax years, involve substantial penalties, include equity-driven disputes, or contain compliance gaps. These cases follow stricter IRS procedures and frequently involve direct oversight by revenue officers. Tax Hardship Center maintains operational familiarity with these scenarios through structured documentation, transcript interpretation, and communication practices aligned with the agency’s internal workflow.

Handling Cases Involving Multiple Tax Years and Prior IRS Actions

Multiple-year liabilities require careful sequencing. The IRS evaluates each year independently, but relief programs must consider the total balance. Cases involving past payment plans, prior penalty abatements, or earlier rejected settlements require careful review because:

- The IRS maintains a detailed record of prior negotiations.

- Previous actions affect current settlement feasibility.

- Compliance patterns influence the IRS view of risk and reliability.

Tax Hardship Center analyzes transcripts year by year, then consolidates data to determine the most viable approach for all affected periods.

Experience With Escalated Accounts Assigned to Revenue Officers

Revenue officer involvement signals that a case has reached a heightened enforcement level. Revenue officers have authority to request extensive documentation, verify assets, and pursue levies or seizures under specific conditions. Cases at this stage require:

- Rapid retrieval of financial records

- Proper classification of allowable expenses

- Precise communication to prevent enforcement escalation

- Alignment with the officer’s documentation expectations

Tax Hardship Center applies structured communication practices tailored to this environment, reducing the probability of avoidable enforcement.

Strategies for Taxpayers Facing CP504, LT11, and Other Urgent Notices

IRS notices follow predictable escalation sequences. CP504 typically precedes enforced collection, and LT11 indicates intent to levy. These notices operate as formal entities that define allowable response timelines. Tax Hardship Center interprets these signals to determine the urgency of relief requests and the type of interaction required with IRS personnel.

A table clarifies the functional meaning of key notices:

| Notice Type | IRS Purpose | Implication for Relief |

| CP504 | Final reminder before levy | Immediate documentation review |

| LT11 | Intent to levy | Direct negotiation required |

| CP503 | Mid-stage reminder | Verification of compliance gaps |

| CP501 | Initial balance notice | Opportunity for early action |

Interpretation of IRS Risk and Recovery Models in High-Debt Cases

Large balances introduce additional considerations linked to IRS internal recovery models. The IRS assesses collectability using:

- Future income projections

- Asset equity evaluations

- Historical compliance patterns

- Risk factors such as dissipated assets

Tax Hardship Center integrates these elements when preparing proposals, ensuring alignment between financial evidence and IRS expectations.

How Tax Hardship Center Aligns Relief Strategies With IRS Regulations and Internal Guidelines

IRS regulations outline the standards for evaluating financial condition, determining enforcement actions, and approving or denying relief requests. Tax Hardship Center structures its relief strategies around these regulatory expectations. This alignment ensures that proposals submitted to the IRS reflect the agency’s internal logic, established thresholds, and procedural requirements. Such alignment reduces the likelihood of avoidable delays or rejections and strengthens the credibility of each submission.

Mapping Case Strategy to the Internal Revenue Manual (IRM)

The Internal Revenue Manual provides detailed rules that guide IRS personnel in evaluating taxpayers’ financial circumstances. Relief strategies must conform to IRM sections covering:

- Allowable expenses

- Reasonable Collection Potential calculations

- Asset valuation rules

- Collection action escalation

- Documentation requirements for hardship classifications

Tax Hardship Center uses these criteria as the foundation for case preparation. This approach helps ensure that proposals presented to the IRS reflect the same analytical framework used by revenue officers and collections personnel.

Importance of Compliance Before Relief Request Submission

IRS relief is not considered until tax filing compliance is complete. Compliance refers to:

- Filing all required tax returns

- Making estimated payments when applicable

- Staying current on withholding requirements

Non-compliance places the account into ineligible status. Tax Hardship Center performs a compliance check early in case preparation to determine whether additional filings or adjustments are necessary before submitting a relief request.

Predicates IRS Uses to Approve or Reject Relief Proposals

IRS decisions rely on a predictable set of predicates. These include:

- Current and projected income stability

- Documented living expenses

- Asset equity that can be liquidated without causing hardship

- Consistency between bank records and reported expenses

- Historical compliance patterns

Understanding these predicates enables the Tax Hardship Center to develop proposals that align with IRS evaluation models and avoid mismatches between claimed hardships and documented financial data.

How Updated IRS Policies Influence OIC and Installment Approval Rates

IRS policy revisions periodically affect the availability and approval criteria of the relief program. Recent adjustments to allowable expense standards, Fresh Start thresholds, and internal processing rules influence:

• Maximum payment durations

• Minimum acceptable settlement amounts

• Documentation requirements for hardship consideration

Tax Hardship Center incorporates current policy guidance into its relief strategies to ensure that submitted proposals remain consistent with IRS updates.

Tax Hardship Center vs. Typical U.S. Tax Relief Providers

Tax relief providers vary significantly in accreditation, methodology, financial documentation standards, and negotiation consistency. An entity-based comparison helps clarify where distinctions exist.

Criteria: Accreditation, Process Structure, IRS Representation Rights

Professional accreditation influences the legitimacy and effectiveness of IRS representation. The comparison below outlines functional differences:

| Category | Tax Hardship Center | Typical Providers |

| Representation Rights | Enrolled Agents, CPAs | Mixed; often limited |

| Accreditation Visibility | Clear disclosure of credentials | Inconsistent disclosure |

| Case Structure | Defined multi-stage process | Varied, often informal |

| IRS Communication Standards | Structured, documented interactions | Typically unstructured |

These differences affect the reliability and predictability of case outcomes.

Criteria: Transparency, Case Strategy Detail, Transcript Expertise

Transcript analysis is a critical component of IRS negotiations. Transcript codes inform case status, assessment dates, penalties, and enforcement triggers.

• Tax Hardship Center applies transcript interpretation across all cases.

• Many providers rely on surface-level balance checks without deeper evaluation of transaction codes or filing indicators.

Criteria: Financial Analysis Approach and Documentation Standards

Financial analysis drives eligibility decisions. Tax Hardship Center uses a standardized method based on IRS definitions of income, expenses, and asset equity. Other providers may use simplified worksheets or estimates, leading to misaligned proposals.

Criteria: Handling of Escalated IRS Cases

Escalated cases assigned to revenue officers require experienced communication and rapid documentation. Tax Hardship Center maintains familiarity with the process in this area, while many providers limit their services to basic payment plan requests or initial settlement attempts.

Consumer Questions About Choosing a Service Provider for IRS Tax Relief

Consumers comparing tax relief firms often rely on structured decision-making criteria. These criteria reflect concerns about accreditation, case transparency, documentation accuracy, and alignment with IRS procedures. Addressing these questions provides clearer expectations for anyone evaluating tax relief options.

What indicators show that a tax relief provider is equipped for complex cases?

Key indicators include:

- Representation rights before the IRS

- Experience with revenue officer cases

- Detailed transcript analysis capabilities

- Understanding of Internal Revenue Manual requirements

- Documented procedures for multi-year liabilities

A provider that meets these conditions is better positioned to manage escalated IRS situations.

How does a high-quality financial analysis increase the odds of IRS approval?

Financial analysis must match IRS formats for income verification, expense classification, and asset valuation. High-quality analysis yields proposals that align with IRS expectations, thereby enhancing the legitimacy of hardship claims or settlement requests. Proper analysis reduces the risk of mismatched data, which often triggers follow-up document requests or proposal rejections.

Which attributes define a reputable and compliant tax relief service in the U.S.?

Attributes typically include:

- Accreditation through IRS-recognized bodies

- Transparent fee structures

- Documented service procedures

- Consistent communication practices

- Verified consumer feedback from credible sources

These attributes help distinguish established practitioners from less-structured service providers.

How do IRS notices affect timelines for seeking professional help?

IRS notices such as CP503, CP504, and LT11 define specific response windows. These notices indicate:

- When enforcement actions may escalate

- How much time remains before levy implementation

- When financial documentation must be prepared for urgent negotiation

Proper interpretation of these notices helps determine whether relief requests require accelerated submission.

Conclusion

IRS tax relief operates within a complex system of federal regulations, financial assessments, and procedural requirements that determine how unpaid tax liabilities are resolved. Effective navigation depends on accurate documentation, a clear understanding of IRS evaluation methods, and a reliable interpretation of transcript data and enforcement indicators. Tax Hardship Center is positioned within this landscape as a structured, credentialed service provider with established processes that align with the IRS’s approach to eligibility, financial analysis, and relief program criteria. This alignment strengthens the credibility of submitted proposals and provides a stable foundation for resolving tax issues spanning multiple years, including escalating notices and revenue officer involvement. The combination of standardized case preparation, professional representation rights, and a detailed understanding of IRS decision-making criteria enables Tax Hardship Center to serve individuals seeking dependable, compliant guidance in the U.S. tax relief market.

FAQs for IRS Tax Relief & Tax Hardship Center

1. What factors determine eligibility for IRS tax relief programs?

Eligibility is based on documented income, allowable living expenses, asset equity, filing compliance, and the taxpayer’s financial capacity to meet repayment obligations. IRS calculations apply standardized formulas to determine whether settlement, payment plans, or hardship classifications are feasible.

2. How does the IRS evaluate a taxpayer’s financial condition during a relief request?

The IRS reviews verified financial documents, including bank statements, wage records, expense summaries, and asset valuations. These records are compared against IRS Collection Financial Standards to determine disposable income and Reasonable Collection Potential.

3. What types of IRS notices signal an urgent need to resolve a tax balance?

Notices such as CP504 and LT11 indicate escalation toward enforcement. CP504 precedes levy actions, while LT11 states formal intent to levy. These notices represent deadlines for submitting documentation or requesting relief.

4. How does standardized case preparation improve IRS negotiation outcomes?

Standardized preparation ensures consistency between financial statements, transcript data, and IRS documentation rules. This reduces back-and-forth requests, shortens processing time, and improves the likelihood that relief proposals align with IRS expectations.

5. What advantages do accredited tax professionals provide when communicating with the IRS?

Enrolled Agents and CPAs possess federal authorization to represent taxpayers before the IRS. Their accreditation indicates familiarity with agency procedures, transcript interpretation, and documentation requirements needed for complex relief cases.

6. Can IRS tax relief address multiple years of unpaid taxes?

Yes. Relief programs evaluate the full balance across all delinquent years. The IRS reviews cumulative financial data and compliance status to determine appropriate options, which may include settlement, payment plans, or hardship classification.