You got a letter from the IRS ACS. Or you called the IRS, and the rep mentioned your account is with the Automated Collection System.

Now you want to know one thing: why.

Not just what ACS is in general. Why did your account specifically land there? Because the reason matters. It shapes your options, how urgent this is, and what the IRS is actually expecting from you next.

That is what this article covers.

Table of Contents

- What Is the IRS Automated Collection System?

- The Four Main Reasons ACS Is Contacting You

- Reason 1: You Have an Unpaid Balance From a Filed Return

- Reason 2: You Have Unfiled Tax Returns

- Reason 3: An Audit or IRS Correction Created a New Balance

- Reason 4: You Have Unpaid Payroll or Business Taxes

- How to Figure Out Exactly Why Your Account Is With ACS

- How Tax Hardship Center Resolves ACS Cases at the Source

- Conclusion

- FAQs

- Key Takeaways

What Is the IRS Automated Collection System?

The IRS Automated Collection System, or ACS, is the centralized collection unit the IRS uses to manage unpaid tax balances. It is call-center-based, largely automated, and handles a high volume of accounts at once. There is no assigned agent watching your file. Your account sits in a queue, notices go out on a schedule, and enforcement actions are triggered by the system when certain conditions are met.

Most people do not end up at ACS because of something dramatic. They end up there because a balance went unresolved long enough for the IRS to move it into active collections.

What matters now is understanding which scenario put you there, because the path forward looks different depending on the cause.

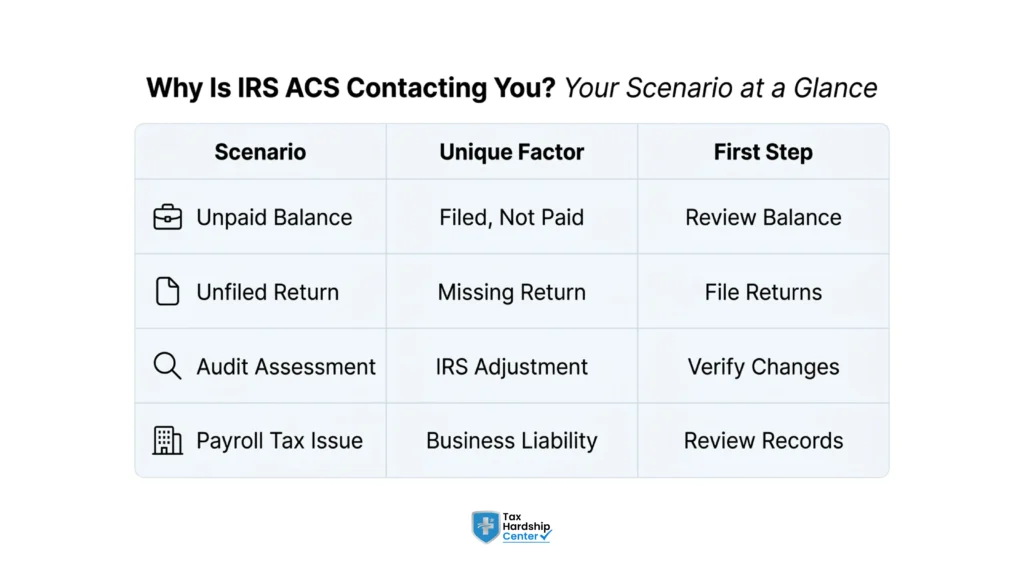

The Four Main Reasons ACS Is Contacting You

ACS does not contact everyone for the same reason. The four scenarios below cover the vast majority of cases. Read through each one. One of them is almost certainly yours.

Reason 1: You Have an Unpaid Balance From a Filed Return

This is the most common reason. You filed your tax return, a balance was due, and it was not paid in full.

Maybe you could not pay the full amount when the return was due. Maybe you paid for something, but not everything. Maybe you set up a payment plan that defaulted. Whatever the specific history, the IRS has an assessed balance on your account, and it has been there long enough to move out of general collections and into ACS.

At this point, the IRS has already sent multiple balance-due notices: a CP14, probably a CP501, and CP503 after that, and possibly a CP504 warning of intent to levy your state tax refund. If any of those notices escalated to an LT11 or CP90, you have already received a final notice of intent to levy, and the clock for requesting a Collection Due Process hearing is either running or already expired.

The good news in this scenario is that you are current on filing. That simplifies the resolution options considerably. An IRS installment agreement, an Offer in Compromise, or Currently Not Collectible status are all potentially on the table, depending on your income and assets.

Reason 2: You Have Unfiled Tax Returns

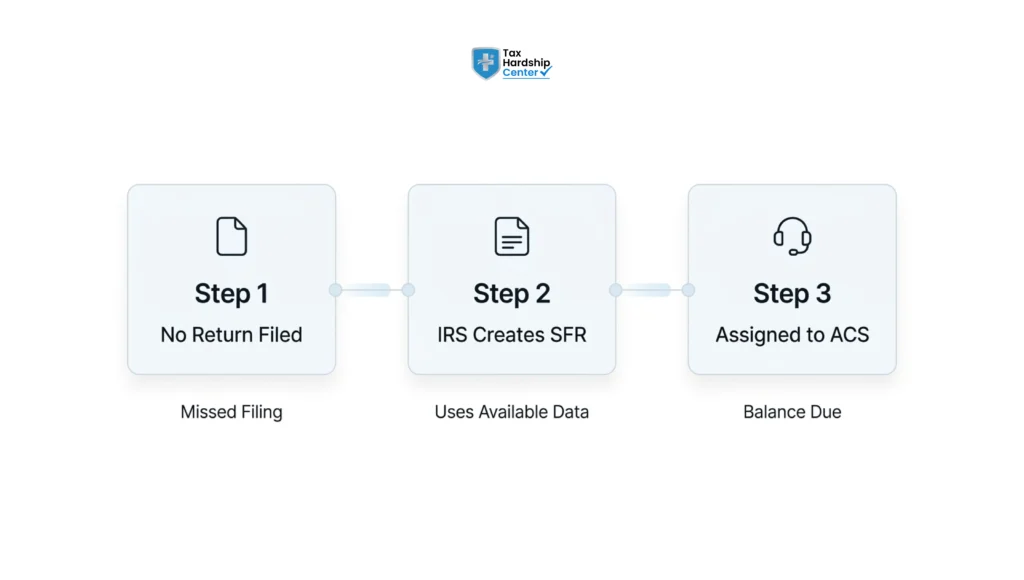

This one surprises people. ACS does not only chase balances you know about. It also pursues balances created by unfiled returns.

Here is how it works. If you did not file a return, the IRS may file one for you. This is called a Substitute for Return, or SFR. The IRS uses income information it already has, from W-2s, 1099s, and other third-party reports, to calculate what you owe. SFR assessments almost always overstate your liability because they use the least favorable filing status and exclude deductions you would have claimed yourself.

Once an SFR is filed and a balance is assessed, that balance moves through the same collection process as any other unpaid tax. Eventually, it lands with ACS.

What makes this scenario trickier is that you may not have opened IRS mail in a while. By the time ACS contacts you, the IRS may have already assessed years of unfiled returns, and you may owe significantly more than you would have if you had filed your own returns with proper deductions.

The fix here involves two steps, not one. You need to file the actual returns to replace the SFRs, then resolve the remaining balance. Trying to resolve the balance without addressing the underlying unfiled returns almost never works. If this is your situation, help with back taxes and unfiled returns is the starting point, not a payment plan negotiation.

Reason 3: An Audit or IRS Correction Created a New Balance

Sometimes people end up with ACS not because they underpaid what they reported, but because the IRS changed the numbers after the fact.

This happens in a few ways:

A correspondence audit (the CP2000 notice is the most common version) proposes additional tax because the IRS found income on your return that did not match third-party reports. You either agreed, did not respond, or disputed it and lost. The additional assessment became a real balance.

The IRS corrected a math error or processing issue on your original return, and the correction added to what you owed.

A prior installment agreement included penalties and interest that continued to accrue while you were making payments, and the balance grew rather than shrank.

In all of these cases, you may not have fully understood how the balance got there. That confusion is normal. But from ACS’s perspective, the balance is assessed and collectible regardless of the origin.

If your balance traces back to an audit or IRS correction and you believe the underlying amount is wrong, that is a dispute worth raising before you agree to any payment terms. Paying a balance you should not legally owe is not a resolution.

Reason 4: You Have Unpaid Payroll or Business Taxes

This scenario is meaningfully different and is worth treating separately.

Business owners who have employees are required to withhold payroll taxes from employees’ wages and remit them to the IRS on a regular schedule. When a business misses those deposits, whether due to cash flow problems, a slow season, or a banking error, the unpaid amount accumulates quickly. Payroll tax deposits are due frequently; the penalties for late deposits are steep, and the IRS tracks them closely.

What makes payroll tax debt particularly serious is the Trust Fund Recovery Penalty. The withheld portion of payroll taxes is considered money held in trust for the government. If the business does not remit it, the IRS can assess the Trust Fund Recovery Penalty personally against the individuals who were responsible for making those deposits: business owners, officers, or even bookkeepers with signing authority. Personal liability means the debt follows you even if the business closes.

ACS handles many payroll tax cases before they escalate to a revenue officer, but payroll cases escalate faster than personal income tax cases. If your account with ACS involves payroll tax or Form 941 balances, that timeline is compressed. Getting a resolution strategy in place quickly is not optional.

How to Figure Out Exactly Why Your Account Is With ACS

The reason your account is with ACS is documented in your IRS account transcript. You do not have to guess.

Log into your IRS online account at IRS.gov and pull your account transcript. It will show every assessment, every notice issued, and every action taken on your account. You will be able to see whether the balance came from a filed return, an SFR, a CP2000 audit, or a payroll assessment.

Look at the tax years involved. Look at the notice dates and types. Look at whether a final notice has been issued. That information tells you where you actually are in the process, not just where you think you are based on the most recent letter you opened.

If the transcript is hard to read, that is normal. IRS transcripts use transaction codes that are not self-explanatory. Understanding IRS transcript codes and what they mean for your case is a reasonable first step before any phone calls or decisions.

How Tax Hardship Center Resolves ACS Cases at the Source

Most tax resolution firms handle ACS cases the same way: call the IRS, set up a payment plan, consider the case managed. Tax Hardship Center starts further back. The reason your account landed with ACS determines which resolution path actually fits and which ones waste your time and money.

For unpaid balance cases, the firm evaluates installment agreement terms, Offer in Compromise eligibility, and Currently Not Collectible status based on real financial documentation, not optimistic assumptions. For unfiled return cases, the process starts with getting compliant, filing the actual returns, and then negotiating from an accurate balance rather than an inflated SFR number. For payroll tax cases, Trust Fund Recovery Penalty exposure is addressed directly, including the assessment of personal liability, before any payment structure is agreed to.

The firm handles levy release and enforcement stops for clients at the active enforcement stage, and penalty abatement requests where the penalty history supports a reasonable cause argument. Every case starts with a transcript review so the strategy fits the actual situation, not a generic version.

Get a free case review and find out exactly why ACS has your account.

FAQs

What does ACS mean in the IRS?

ACS stands for Automated Collection System. It is the IRS unit that handles active collection on unpaid tax balances through a centralized, call-center-based system. When your account is with ACS, it means the IRS is actively working to collect a balance and enforcement tools like levies and liens are available.

Why would ACS send me a letter?

ACS sends letters when there is an unresolved balance on your tax account. The most common reasons are an unpaid balance from a filed return, unfiled returns that resulted in a Substitute for Return assessment, an audit or IRS correction that created a new balance, or unpaid payroll taxes.

Does ACS contact you by phone?

Yes. ACS operates as a call center and may initiate outbound calls in some cases, though most initial contact is through written notices. If you receive a call claiming to be from IRS ACS, verify by calling the IRS directly at the number on your notice before providing any information.

What is the difference between ACS and a revenue officer?

ACS is a system with no assigned agent. A revenue officer is a named IRS employee assigned specifically to your case with broader investigative and enforcement authority. Accounts escalate from ACS to a revenue officer when they remain unresolved or involve complex business tax situations.

Can ACS access my bank accounts or wages?

Yes. After issuing a final notice of intent to levy and giving you a 30-day response window, ACS can levy bank accounts and wages. A bank levy takes funds in a single sweep. A wage levy takes a portion of every paycheck on an ongoing basis until the debt is resolved or a formal agreement stops it.

What happens if I ignore ACS?

The case escalates. ACS will file a federal tax lien, execute levies on bank accounts and wages, and potentially certify your account to the State Department if the balance qualifies as seriously delinquent. Eventually the case may be transferred to a revenue officer, which creates a more difficult situation than dealing with ACS directly.

What if I disagree with the balance ACS is collecting?

You have the right to dispute incorrect assessments. If the balance came from an SFR or CP2000 audit you never properly responded to, there may be options to file correct returns or submit a formal dispute. If a final notice has been issued, a Collection Due Process hearing request also gives you an opportunity to contest the liability.

Conclusion

The IRS Automated Collection System is not contacting you randomly. There is a specific reason your account is there, and that reason is documented. Knowing it is the difference between choosing the right resolution path and spending months on the wrong one.

Key Takeaways

- IRS ACS stands for Automated Collection System, the centralized unit that handles active collection on unpaid tax accounts

- There are four main reasons ACS contacts taxpayers: unpaid balances from filed returns, unfiled returns, audit-created balances, and payroll tax debt

- Unfiled returns often result in a Substitute for Return filed by the IRS, which typically overstates what you owe

- Payroll tax cases move faster through ACS and carry personal liability risk through the Trust Fund Recovery Penalty

- Your IRS account transcript shows exactly why your balance exists and what notices have already been issued

- The resolution path that fits your case depends directly on the reason your account landed with ACS in the first place

- ACS has full enforcement authority including bank levies, wage levies, federal tax lien filings, and passport certification

- A final notice of intent to levy (LT11 or CP90) triggers a 30-day window to request a Collection Due Process hearing

- Ignoring ACS does not pause collection activity; it accelerates escalation toward enforcement and eventual revenue officer assignment

- Resolving an ACS case at the source, meaning addressing the actual reason for the balance, produces better outcomes than negotiating on top of the wrong numbers