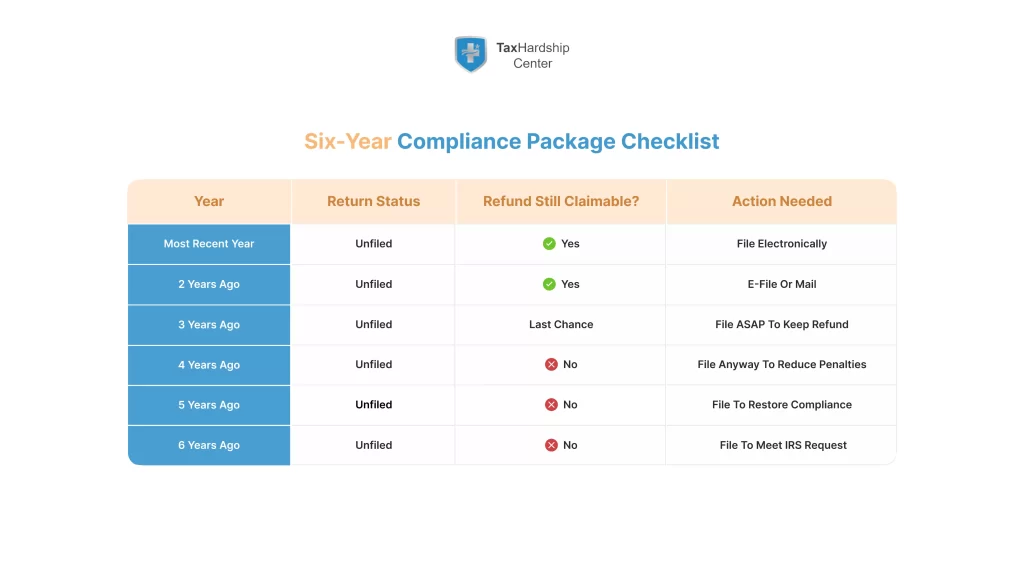

Unfiled tax returns trigger penalties fast, but you stop the worst costs the moment you file. The IRS can accept e-filed returns for the current year and the two prior years, and you mail older years. You keep refund rights only for three years from the original due date. If you do nothing, the IRS can file a substitute return that ignores deductions and credits and then bill you. Most people restore compliance by filing the most recent six years, setting up a payment plan if they owe, and asking for penalty relief when they qualify. Keep reading for the exact steps, deadlines, notices, and forms to use.

Why You Should File Your Past Due Tax Returns Now

Filing now cuts costs, restores benefits, and lowers risk. This section explains the dollars-and-dates reason to act today, how refunds expire, and why timely filing protects Social Security credits, earned credits, and peace of mind.

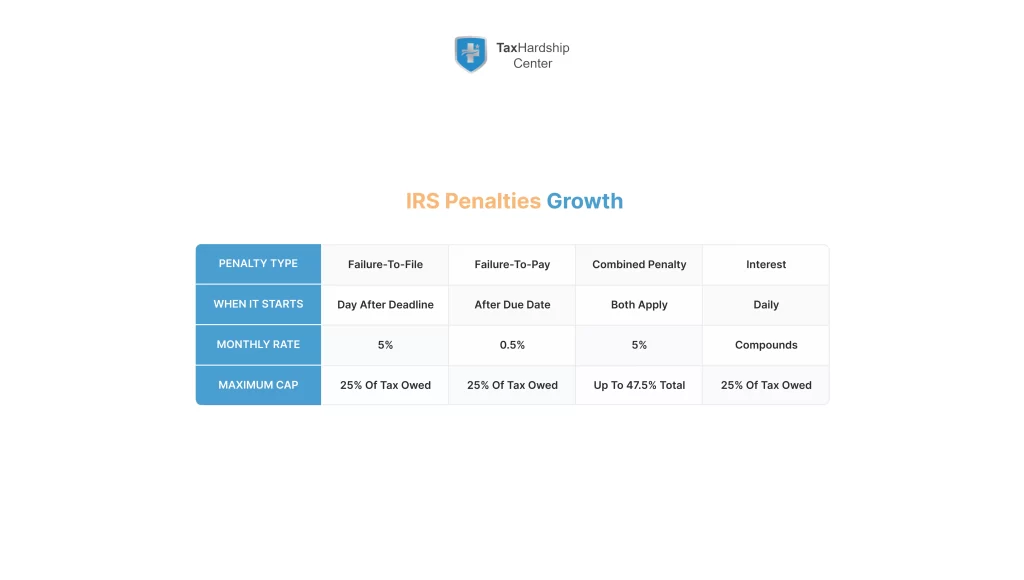

Avoid mounting IRS interest and penalties

Penalties stack each month you leave a return unfiled, and interest compounds on top of them. The failure-to-file penalty starts high, so you reduce the total cost the moment you submit a return, even if you cannot pay in full. You also shrink the window for enforced collection like liens and levies because you move your case toward a payment plan. File first, then pick the best pay option rather than waiting for a demand letter. Acting this week saves more than acting next month because penalties accrue monthly.

Claim your tax refund before it expires

Refund rights do not last forever, so you lose money if you wait too long. You generally have three years from the original due date to claim a refund or refundable credits. If you cross that date, you forfeit the cash even if you had withholding or deserve the Earned Income Credit or American Opportunity Credit. You can still file to clean up your record, but the Treasury will not cut a check for that old year. File now to pull real money off the table before the clock runs out.

Protect your Social Security benefits and credits

Your return does more than settle income tax. If you run a business or drive gig income, you must report self-employment tax to earn Social Security credits for retirement and disability. Missing returns can leave holes in your earnings record, which can shrink future monthly benefits. Filing now records your wages and self-employment income correctly, preserves credits, and avoids headaches when you apply for benefits. Clean filings today protect income you will depend on later.

Our Services at Tax Hardship Center

Our services at Tax Hardship Center help you file missing returns with accuracy and keep you compliant. We prepare prior-year returns, replace substitute returns, and organize documents so you can move fast. For balances due, we set up the right plan, including an Installment Agreement, an Offer in Compromise, or Currently Not Collectible status. If you need a wider review, explore our full IRS Tax Relief Services. You get one point of contact and plain-English updates while we handle the IRS calls and help reduce levy risk.

What Happens if You Don’t File Unfiled Tax Returns and Risk a Tax Levy

Nonfilers face a clear sequence of actions. This section outlines the IRS playbook, from information matching to substitute returns, formal notices, and possible criminal exposure in willful cases.

IRS enforcement actions and substitute returns

The IRS receives your wage and 1099 forms from payers and matches that data to filed returns. When you do not file, the system flags a gap and the IRS can create a substitute for return using only the income it sees. That substitute return usually overstates your bill because it ignores most deductions, credits, dependents, and filing status choices. After that, collection begins with balances the IRS assessed from its substitute numbers. You avoid that outcome by filing a real return that replaces the substitute and recalculates tax with your full facts. Ignored notices can escalate to a tax levy on wages or bank accounts, so take control by filing first. Common final notices, such as CP504 and LT11, arrive before levy action and give a short response window to call, file, or set a plan. If a wage garnishment already started, see our Complete Wage Garnishment Guide for actions you can take before payday.

Criminal charges and legal consequences

Most nonfiling cases stay civil, but willful failure to file can lead to criminal charges. The line often turns on intent, size, and pattern. If you hid income, used false statements, or ignored repeated notices, you raise risk. Prosecutors focus on cases that deter others, especially high-income nonfilers or those who promote schemes. Filing before contact and cooperating with a payment plan reduces exposure and shows good faith.

IRS notices and tax assessments explained

If you do not respond, the IRS issues a series of notices that escalate. Early letters alert you to missing returns and propose assessments. A Notice of Deficiency sets a 90-day window to file the return or petition Tax Court. If you skip that deadline, the IRS assesses the tax and adds penalties and interest. File the return before assessment when possible, or use audit reconsideration after the fact with proof that changes the numbers.

How Late Can You File Past Due Tax Returns

Late does not mean lost, but deadlines matter. This section covers filing timelines, refund windows, and how unfiled returns can morph into collectible tax debt. File state returns with the same urgency because many states issue levies faster than the IRS and share data with federal systems.

Filing taxes late and refund deadlines

You can file late returns at any time, but refunds expire. The refund clock usually runs for three years from the return’s original due date. If you file after that window, the IRS keeps your withholding and credits. If you filed an extension for that year, the three-year clock runs from the extended due date for refund claims tied to that return. Mark these dates on a calendar so you do not leave money behind. For consequences of late payment itself, review our primer on what happens if you don’t pay taxes on time.

Limits on claiming deductions and credits

The longer you wait, the harder it becomes to assemble records. Banks purge old statements and employers merge or close. You must still substantiate deductions and credits, so gather proof now while you can still fetch it. When you lack perfect documentation, you can rely on transcripts, third-party copies, and reasonable reconstructions, but you should not guess. Your goal is a supportable return that closes the year without inviting an adjustment.

When unfiled returns turn into tax debt

Once the IRS assesses a balance, the debt moves into collection. The IRS usually has 10 years from the assessment date to collect, and that period can pause during events like bankruptcy or an appeal. Interest and the failure-to-pay penalty continue until you zero the balance. You control the process by entering a payment plan, seeking penalty relief, and keeping current on this year’s taxes so the debt stops growing.

How to File Tax Returns for Previous Years with Accuracy

Catching up follows a simple playbook. This section covers how to gather records, request missing forms, decide between self-prep and professional help, and submit older returns the right way.

Gather tax forms and income records

Start with what you have. Pull W-2s, 1099s, 1098s, K-1s, brokerage statements, and bank interest forms for each missing year. Add proof for common deductions such as mortgage interest, property taxes, charitable gifts, medical expenses, tuition, and business costs. Build a folder for each year so nothing crosses. Label each folder with the year and a checklist of needed pieces so you can spot gaps quickly. Accuracy wins audits, so reconcile totals to statements and highlight any estimates you used.

Request missing tax documents from the IRS

When you miss forms, order transcripts. Wage and income transcripts list W-2 and 1099 data for up to the last 10 years. Tax return and tax account transcripts help you confirm prior filings and payments. You can request transcripts in your IRS online account or by using Form 4506-T by mail if you prefer paper. Use the IRS Get Transcript page to pull wage and income records quickly. You may need to verify your identity before you can view full transcripts online. You access these tools from your IRS online account on the IRS website, which helps keep each year’s details in one place. Use transcripts as scaffolding to rebuild accurate returns when your own files fall short.

Filing tax returns with professional tax help

Simple W-2 years often fit DIY software. Complex years with business income, crypto, stock sales, rental property, canceled debt, or multiple states call for a pro. A licensed enrolled agent, CPA, or tax attorney brings experience with multi-year cleanups, penalty relief options, and notices. At Tax Hardship Center, our tax professionals prepare prior-year returns, set up payment plans, and handle IRS calls so you do not have to. Professional help pays for itself when it cuts penalties, protects credits, and prevents repeat errors.

Submitting unfiled returns through the IRS

You can e-file the current year and the two prior years with most software or through a pro. For older years, you print, sign, and mail each return to the address in that year’s instructions. Use separate envelopes by year and send with tracking so you can prove timely mailing. If the IRS already filed a substitute return, include your real return with a cover letter that asks the IRS to replace its numbers. Keep copies of everything because you may need them later for notices or state filings.

Unfiled Tax Returns: Everything You Need to Know

This section answers common questions that pop up once you start. You will see the difference between back taxes and unfiled taxes, rules for self-employed filers, how to handle balances with payment plans, and when to seek penalty relief. We emphasize accuracy at each step, because a small mistake can trigger a notice that slows your case.

Difference between back taxes and unfiled taxes

Back taxes means you owe money for a year you filed. Unfiled taxes means you skipped the return entirely. You can have both, but the fixes differ. Back taxes focus on payment options and interest control. Unfiled taxes start with sending a correct return to set the right baseline, then choosing a way to pay if you owe.

Filing self-employed returns with the Schedule C tax form

Self-employed taxpayers report business income and expenses on the schedule c tax form (Schedule C) and calculate self-employment tax on Schedule SE. That self-employment tax funds Social Security and Medicare and builds your future retirement and disability credits. You need strong records for income and costs, including mileage logs, receipts, 1099-NEC forms, 1099-K statements, and bank statements. If records are messy, you still file with the best documentation you can gather and note methods you used to reconstruct totals. Clean books next year by using separate business accounts and simple software.

Add practical accuracy habits. Keep a mileage app or a paper log and reconcile totals monthly. Track home office space by square footage and use one method all year. Reconcile 1099-K platform payouts to bank deposits so you report gross and fees correctly. Set quarterly estimates so you do not build a new debt while you fix the old one. These habits shrink notices and protect deductions.

Handling unpaid taxes with a payment plan

If you owe and cannot pay in full, you choose from several payment plans. Small balances often fit a streamlined agreement you can request online. Larger debts may need a full financial disclosure and a monthly amount based on income and expenses. If you cannot pay much, you may qualify for a partial payment plan that pays what you can until the collection window ends. File all missing returns first, then pick the plan that clears the debt without breaking your budget. For options and decision points, see our explainer on IRS payment plans.

Pursue a penalty abatement request if eligible

Two common paths reduce penalties. First-time penalty abatement helps taxpayers with a clean recent history who fell behind once. Reasonable cause relief can help when events outside your control caused the late filing or late payment, such as serious illness, disasters, or records destroyed. You must describe the facts in detail, show that you acted with ordinary care, and show how you fixed the problem. You can ask by phone, by letter, or through a representative. Strong documentation raises approval odds. Learn practical scripts and criteria in our post on IRS penalty abatement strategies.

Why File Your Tax Returns as Soon as Possible

Speed helps in ways that go beyond penalties. This section shows how quick action protects refunds, replaces substitute returns, and eases collection pressure so you can breathe again.

Protect tax refunds before the statute of limitations

Refunds expire, so you cannot wait and expect a payout later. File before the three-year mark tied to each year’s original due date to keep your refund rights. If you need a few weeks to finish, request any employer copies and transcripts today and set a hard filing date on your calendar. Treat the refund deadline as money with an expiration label. Once it turns, it is gone for good.

Avoid substitute returns that inflate your tax debt

The IRS bases substitute returns on income only. That method raises tax because it ignores status, dependents, deductions, and credits. Your real return replaces the substitute and brings the balance down to reality. You often cut the bill sharply when you claim children, education credits, or business expenses that never show on third-party forms. Filing now unlocks those legal reductions.

Reduce IRS collection pressure

Filed returns let you set terms instead of reacting to demands. You can choose a direct debit plan that fits your cash flow, ask for penalty relief, or request a brief hold while you organize finances. You also stop new notices about missing returns, which lowers stress and risk of bank levies. The IRS works with taxpayers who file and communicate. Silence prompts enforcement. You also lower the odds of a tax levy because you show good faith and a workable plan.

Other Considerations if You Haven’t Filed in Years

Long gaps add wrinkles, but you can still build a clean path forward. This section covers bankruptcy timing, penalty relief on old years, and when to consider settlement options.

Filing taxes during bankruptcy

Bankruptcy pauses IRS collection for most debts, but you usually must file all required returns to move the case forward. Some older income tax debts can discharge if they meet strict timing rules on due dates and assessment dates. Recent years and payroll taxes do not discharge. Coordinate filing dates with your bankruptcy attorney so your petitions and returns work together. Do not file blind during a case without advice.

Requesting penalty relief for old unfiled returns

Old years can still qualify for penalty relief if you show strong facts. Gather hospital records, disaster reports, or proof of theft or business closure if those events caused the problem. Write a clear timeline that explains when you discovered the issue and what you did to correct it. Ask for first-time abatement if you meet clean-history rules, then fall back to reasonable cause if you do not. A thoughtful, documented request can save real money.

When to seek tax relief or settlement options

If you cannot pay what you owe in the remaining collection window, consider an offer in compromise or a partial payment plan. An offer in compromise settles for less than the balance when your income, assets, and expenses show limited ability to pay. A partial payment plan collects affordable monthly amounts until the collection clock runs out. These programs require full financial disclosure and careful paperwork. A seasoned pro improves your odds and keeps expectations realistic.

Step-by-Step: How to File Your Unfiled Tax Return on the IRS Website or by Mail

This section gives you a clear, repeatable checklist to follow for each missing year. Print it, check items off, and move to the next year until you finish the stack. Use the IRS website for transcripts and instructions so every step stays accurate.

Collect documents for each missing year

Create one folder per year. Add W-2s, 1099s, 1098s, K-1s, bank interest, brokerage tax forms, and proof of deductions and credits. Use wage and income transcripts to fill gaps for pay you forgot. Keep notes about any estimates you used and the basis for those estimates. A clean paper trail prevents confusion later if the IRS asks questions.

Complete the correct IRS tax forms

Use the version of Form 1040 and schedules for that year. Tax law changes often, so you must use the right forms and instructions for the year you file. Software that supports prior years will load the correct forms automatically. If you file by hand, download the forms for that year from the IRS site. Double-check names, Social Security numbers, and address so transcripts and notices match your return. Accuracy matters more than speed, so compare totals to transcripts and check math before you sign. Use a quick accuracy checklist for every year: confirm filing status, dependents, bank routing and account numbers, EINs for employers, and any Schedule C totals. Match Box 1 wages and Box 2 withholding to your W-2. Confirm that 1099 interest and dividends tie to the transcript totals.

File tax returns electronically or by mail

E-file the current year and the two prior years when possible because you get faster confirmation and faster processing. Mail older years by certified mail with tracking and keep the receipts with your copies. If the IRS filed a substitute return, include your accurate return and a brief note asking the IRS to accept it in place of the substitute. Send each year in its own envelope to the correct address for that year. Use the IRS website to confirm the mailing address for each specific year. If you expect a refund, choose direct deposit and triple-check routing and account numbers for accuracy.

Work with tax professionals for complex tax issues

Use a professional when you face business losses, multi-state moves, large stock sales, equity compensation, foreign accounts, or canceled debt. Pros know how to reconstruct basis, sort carryovers, and pick elections that reduce tax across several years. At Tax Hardship Center, our team prepares and files missing returns, requests penalty relief, and sets up the right payment option for your budget. One coordinated plan beats year-by-year guesswork.

Want to Claim Social Security Benefits at Age 62? Risks to Know

Filing status affects more than taxes today. This section connects unfiled returns to Social Security timing, earnings records, and how refunds interact with retirement planning.

How unfiled tax returns affect Social Security eligibility

You earn Social Security credits by reporting wages and self-employment income on filed returns. If you skip returns during your working years, you may not earn enough credits to qualify or you may lower your average indexed earnings that drive your benefit. Fix that now by filing missing years and paying any self-employment tax due. Check your Social Security earnings record online and correct errors while you still have documents handy. Clean records today support the benefit you expect at 62 and beyond.

Tax refunds and retirement income considerations

Refunds provide cash you can route toward retirement savings or high-interest debt before you claim Social Security. If the refund window remains open, file now to free up those dollars. If the window closed, you still file to correct your record and lower penalties, which indirectly preserves savings. A tax pro can help you decide whether to claim at 62 or wait for a higher monthly benefit while balancing the tax impact of part-time income or IRA withdrawals.

Why a Reverse Mortgage Makes Sense for Seniors This Year

Some seniors face tax debt they cannot pay from monthly income. This section explains when a reverse mortgage can fit and the real-world cautions that come with it.

When seniors face tax debt and unfiled returns

A reverse mortgage can turn home equity into cash without monthly mortgage payments. You might use proceeds to pay property taxes, clear IRS balances, or cover living costs while you file and fix missing years. Lenders require counseling and a full review of your ability to keep up with property charges. You must stay current on homeowners insurance and taxes or you risk foreclosure. Consider this tool only after you explore payment plans, budgeting, and downsizing.

Using home equity to manage back taxes

If you have significant equity and stable housing needs, a reverse mortgage can supply a lump sum or a line of credit to retire tax debt and stop compounding interest. Work with a housing counselor and a tax pro to model the costs, fees, and impact on heirs. Compare the reverse mortgage path with selling, a standard refinance, or a home equity line. Choose the path that protects your housing and clears the IRS balance with the lowest lifetime cost. Make sure the payoff actually ends the risk of liens and a future tax levy before you sign closing papers. A cautious plan beats a quick fix.

At Tax Hardship Center, We Help You File and Settle

At Tax Hardship Center, we help you file old returns with accuracy, fix substitute returns, and choose a relief path that fits your cash flow. We pair back-tax filing with tailored options like an Installment Agreement or an Offer in Compromise, and we manage IRS calls so you can focus on work and family. If hardship applies, we request Currently Not Collectible status and put guardrails in place to lower levy risk. When records need cleanup, our Bookkeeping team rebuilds prior-year profit and loss so the numbers on each return match your transcripts. One coordinated plan beats guessing year by year.

In summary…

A fast, organized filing plan saves money, protects benefits, and restores control. Use these points to move from stuck to compliant without missteps.

- File before penalties and interest add up, and submit even if you cannot pay in full.

- The failure-to-file penalty hits first and hardest, so filing now cuts the bill.

- Add a payment plan after filing to stop new notices and protect cash flow.

- The failure-to-file penalty hits first and hardest, so filing now cuts the bill.

- Preserve refunds by filing within three years of each year’s original due date.

- Refund rights expire, but you still file to correct your record and credits.

- Order wage and income transcripts to rebuild forms you lost.

- Refund rights expire, but you still file to correct your record and credits.

- Replace substitute returns with accurate filings that claim all legal deductions and credits.

- Your real return often drops the assessed balance by recognizing dependents and expenses.

- Keep copies and mailing proof for each year you submit. Filing and paying on a plan reduces the chance of a tax levy.

- Your real return often drops the assessed balance by recognizing dependents and expenses.

- Use payment options that fit your budget and timeline.

- Streamlined plans fit smaller balances. Larger debts may require full financials.

- Consider partial payment, an offer in compromise, or hardship holds when cash is tight.

- Streamlined plans fit smaller balances. Larger debts may require full financials.

- Ask for penalty relief when you qualify.

- First-time abatement helps with a clean recent history.

- Reasonable cause relief helps when events outside your control caused the delay.

- First-time abatement helps with a clean recent history.

- Build accuracy into your process so you avoid new notices.

- Use the IRS website to pull transcripts, confirm addresses, and check balances.

- Review Schedule C details, refunds, and banking numbers before you sign to prevent a tax levy from avoidable errors.

- Use the IRS website to pull transcripts, confirm addresses, and check balances.

You do not have to do this alone. Tax Hardship Center can prepare prior-year returns, set up the right payment plan, and submit penalty relief requests backed by documentation. Visit our website to see how our process works and what documents to bring. Reach out for a quick, no-pressure review and a clear plan that fits your budget.

FAQs

Can I e-file old returns?

You can e-file the current year and usually the two prior years. For older years, you print, sign, and mail each return to the address for that year. If the IRS already filed a substitute return, include your correct return with a brief note asking the IRS to accept it in place of the substitute. Keep tracking receipts for proof.

How many years should I file to get compliant?

Most people catch up by filing the last six years, unless fraud or very high income changes the request. The IRS may ask for more in rare cases, but a six-year package often restores normal status. A tax pro can gauge risk and tailor the set for your facts. File the most recent year first, then work backward.

What if I cannot pay when I file?

File anyway to stop the failure-to-file penalty. Then request a payment plan that fits your cash flow. You can ask for a short-term plan if you can pay within a few months, or a longer plan with monthly payments. If money is tight, a partial payment plan or an offer in compromise may fit better than a standard agreement.

Can I still get a refund from an old year?

You can claim a refund only within three years of the original due date for that year. After that, the refund expires even if you had withholding or refundable credits. You still benefit from filing because you correct your record, reduce penalties on other years, and prevent a substitute return from inflating your bill.

When should I hire a professional?

Hire a pro when you face business income, multiple states, asset sales, substitute returns, or IRS notices. Pros rebuild records, choose the best elections, and speak with the IRS on your behalf. Tax Hardship Center handles multi-year cleanups, sets up plans, and requests penalty relief that sticks. The right help shortens the process and lowers total cost.