You owe the IRS money, and you cannot pay the full balance today. You know payment plans exist, but you are not sure how to apply or whether you will be approved. You have heard about applying online and have seen Form 9465 mentioned, but you do not know which form to use or what information the IRS needs.

Here is what matters: the IRS approves most payment plan applications as long as you meet the eligibility rules and submit complete information. The application itself is not complicated. Rejections are caused by missing information, unfiled tax returns, or choosing the wrong type of payment plan for your balance.

This guide walks through exactly how to apply for an IRS payment plan in 2026, whether to apply online or use Form 9465, what documents and account information you need, what the setup fees are, what causes the IRS to reject applications, and when professional help makes the difference between approval and rejection.

Do You Qualify for an IRS Payment Plan?

Not everyone is automatically approved for a payment plan. The IRS has eligibility rules based on how much you owe, whether your tax returns are current, and what type of plan you are applying for.

All tax returns must be filed. The IRS will not approve a payment plan if you have unfiled returns. If you owe money for 2023 but never filed your 2021 return, the IRS will reject your application until you file 2021. This is the most common reason applications get denied.

You must owe $50,000 or less in combined tax, penalties, and interest to apply online. If you owe more than $50,000, you can still get a payment plan, but you must call the IRS or work with a tax professional to set it up. The online system will not accept balances over $50,000.

You cannot have an existing active payment plan. If you already have a payment plan and have defaulted, or now owe additional tax for a new year, you need to revise your existing plan, not apply for a new one. The IRS will reject duplicate applications.

Businesses must owe $25,000 or less to apply online. If you owe business taxes (941 payroll taxes, for example), the online eligibility threshold is lower. Businesses that owe more than $25,000 must call the IRS or submit Form 9465 by mail.

You must be able to pay the balance within 72 months. The IRS allows payment plans up to 72 months (six years). If your balance is too large to pay off in 72 months with affordable monthly payments, the IRS may require financial documentation to prove hardship or may reject the plan entirely and direct you toward an Offer in Compromise or Currently Not Collectible status.

If you meet these rules, the IRS approves most applications quickly. If you do not meet them, fix the issue first before applying.

Short-Term vs Long-Term Payment Plans: Which One Fits Your Balance

The IRS offers two types of payment plans. Which one you qualify for depends on how much you owe and how fast you can pay it.

Short-term payment plan (120 days or less): If you owe less than $100,000 in combined tax, penalties, and interest, and you can pay the full balance within 120 days, apply for a short-term plan. There is no setup fee for a short-term plan. You can pay in one lump sum at the end of 120 days or make multiple payments during the 120-day window. Interest and penalties continue to accrue until the balance is paid in full.

This is the best option if you are waiting on a bonus, a commission check, or a large invoice payment and you just need a few extra months to gather the cash.

Long-term payment plan (more than 120 days): If you owe $50,000 or less and you need more than 120 days to pay, apply for a long-term installment agreement. You will make monthly payments until the balance is paid in full. The IRS charges a setup fee for long-term plans. The fee depends on how you apply and how you make payments.

For most people who cannot pay within four months, the long-term plan is the only realistic option. The IRS will automatically calculate your minimum monthly payment based on your balance and the 72-month maximum repayment period. You can pay more than the minimum to pay off the balance faster and reduce interest charges.

For more on comparing payment plan options, see our guide on IRS payment plan vs OIC vs CNC.

How to Apply for an IRS Payment Plan Online

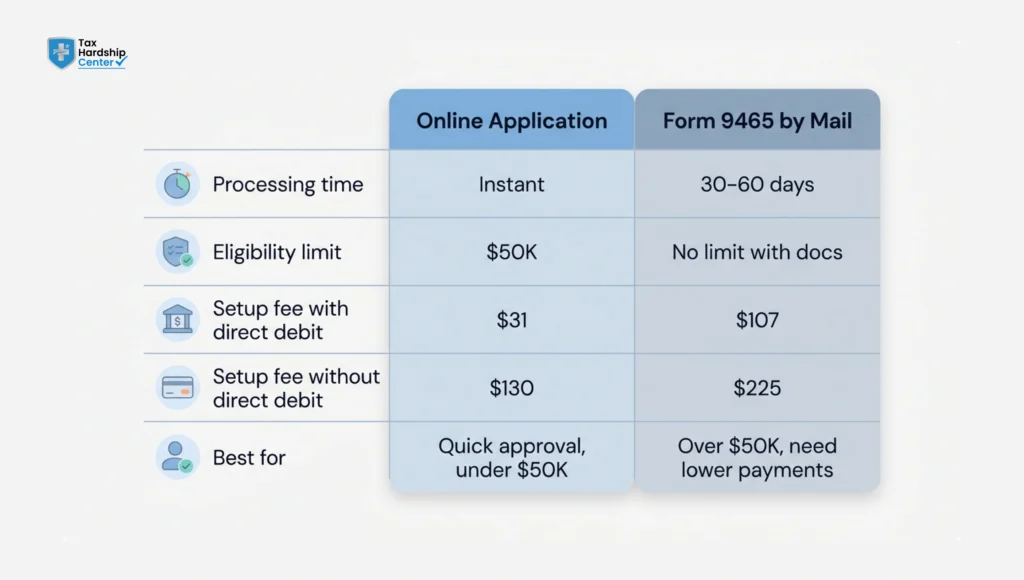

Applying online is the fastest way to set up a payment plan. The IRS processes online applications immediately. You get instant approval if you meet the eligibility requirements.

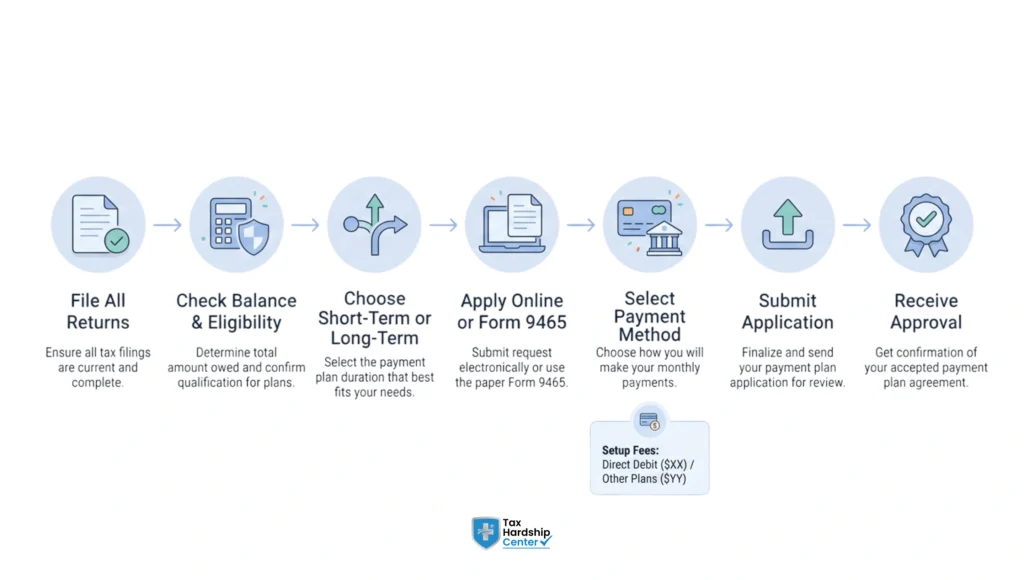

Step 1: Go to IRS.gov and navigate to the Online Payment Agreement tool. You will need to create an IRS account or log in if you already have one. The tool is available only to individuals and businesses that owe $50,000 or less (individuals) or $25,000 or less (businesses).

Step 2: Verify your identity. The IRS requires identity verification to access the online tool. You will need your Social Security number, filing status, and mailing address from your most recent tax return. You may also need a credit card, loan account, or mortgage account to verify your identity.

Step 3: Select the tax years you want included in the payment plan. If you owe for multiple years, the IRS will combine them into one monthly payment. You cannot set up separate plans for separate years.

Step 4: Choose short-term or long-term. If you owe less than $100,000 and can pay within 120 days, select short-term. If you need longer, select long-term. The system will calculate your minimum monthly payment based on your balance and the 72-month maximum repayment window.

Step 5: Select your payment method. The IRS offers two options: direct debit (automatic withdrawal from your bank account) or non-direct debit (you make manual payments each month). Direct debit has a lower setup fee. If you choose not to use direct debit, you are responsible for making payments on time each month. The IRS does not send reminders.

Step 6: Review and submit. The system will show your setup fee, your monthly payment amount, and your first payment due date. If everything looks correct, submit the application. You will receive instant approval if you meet the eligibility rules.

Once approved, you will receive a confirmation letter from the IRS within a few weeks. Your first payment is due on the date shown in the confirmation.

How to Apply Using Form 9465 by Mail or Phone

If you owe more than $50,000, cannot apply online, or prefer to apply by mail or phone, use Form 9465 (Installment Agreement Request).

Download Form 9465 from IRS.gov. The form is two pages. You will fill out your personal information, the tax years you owe, your proposed monthly payment amount, and your payment method.

Attach Form 433-F (Collection Information Statement) if you owe more than $50,000 or if you are requesting monthly payments lower than the IRS minimum. Form 433-F requires detailed financial information, including your income, expenses, bank account balances, and asset values. The IRS uses this form to determine whether you can afford higher payments or whether you qualify for hardship status.

Mail the completed forms to the IRS address listed on the Form 9465 instructions. The mailing address depends on which state you live in. Do not mail the form to your local IRS office. Use the address in the instructions.

Or call the IRS directly to set up a payment plan. Call the number on your IRS notice or call the general IRS payment line at 1-800-829-1040. The representative will ask for the same information that appears on Form 9465. They can set up the plan while you are on the phone, but you may still need to submit financial documentation by mail or fax if your balance is over $50,000.

Processing time for mailed applications is 30 to 60 days. Processing time for phone applications is shorter, but you may spend a significant amount of time on hold.

For more details on IRS payment plan options and how they compare, see our guide on payment arrangement options and how to apply.

What Information Do You Need Before You Apply

Before you start the application, gather the following information. Having everything ready prevents delays and reduces the chance of rejection.

Your Social Security number or Employer Identification Number (EIN) if you are applying for a business payment plan.

Your most recent tax return. The IRS uses information from your last filed return to verify your identity.

Your total balance owed. Check your IRS account online at IRS.gov or call 1-800-829-1040 to confirm your balance. Do not guess. If you underestimate your balance, the IRS may reject your payment plan proposal because the payments you offered are too low.

Your bank account and routing number if you are setting up direct debit payments.

Your monthly income and expenses if you owe more than $50,000, or if you are requesting payments lower than the IRS minimum. You will need to complete Form 433-F, which requires detailed financial information, including pay stubs, bank statements, and monthly living expenses.

Proof that all tax returns are filed. If you have unfiled returns, file them before applying for a payment plan. The IRS will reject your application if returns are missing.

IRS Payment Plan Setup Fees and How to Get Them Reduced

The IRS charges a setup fee for long-term payment plans. The fee depends on how you apply and how you make payments.

Online application with direct debit: $31 setup fee. This is the lowest fee option. If you apply online and set up automatic monthly withdrawals from your bank account, the IRS charges $31.

Online application without direct debit: $130 setup fee. If you apply online but choose to make manual payments each month, the fee is significantly higher.

Phone or mail application with direct debit: $107 setup fee. If you apply using Form 9465 or by calling the IRS and you set up direct debit, the fee is $107.

Phone or mail application without direct debit: $225 setup fee. This is the highest fee option. If you apply by mail or phone and make manual payments, the IRS charges $225.

Low-income taxpayer fee waiver or reimbursement: If your income is at or below 250% of the federal poverty level, you may qualify for a reduced setup fee of $43 or a full waiver. To request the waiver, check the box on Form 9465 indicating you qualify as a low-income taxpayer. You may need to provide proof of income.

The setup fee is added to your total balance and paid over the life of the payment plan. You do not pay it up front.

Short-term payment plans (120 days or less) have no setup fee.

How Long Does Approval Take and What Happens If You Are Rejected

If you apply online and you meet the eligibility requirements, you receive instant approval. The IRS confirms your payment plan immediately and sends a confirmation letter within a few weeks.

If you apply by mail or phone, approval takes 30 to 60 days. The IRS will send a letter confirming your payment plan and stating your first payment due date.

Common reasons the IRS rejects payment plan applications:

Unfiled tax returns. This is the number one reason for rejection. File all missing returns before applying.

Balance over $50,000 for individuals or $25,000 for businesses applying online. If your balance is too high, the online tool will reject your application. You must call the IRS or submit Form 9465 with financial documentation.

You already have an active payment plan. If you defaulted on a prior plan or you owe for a new tax year, you need to revise your existing plan, not create a new one.

You proposed monthly payments that are too low. The IRS calculates a minimum payment based on your balance and the 72-month repayment window. If you request payments below that minimum without submitting financial documentation proving hardship, the IRS will reject the application.

You owe more than $50,000 and did not submit Form 433-F. If your balance is over $50,000, the IRS requires financial documentation. Without it, they reject the application.

If your application is rejected, the IRS will send a letter explaining why. You can reapply after correcting the issue. For example, if the rejection was due to unfiled returns, file the missing returns and reapply.

Why Professional Help Matters When Payment Plan Applications Get Complicated

Applying for a payment plan when you owe $20,000, all your returns are filed, and the IRS-calculated monthly payment fits your budget is straightforward. Apply online, get instant approval, set up direct debit, and you’re done.

The process gets harder when you owe more than $50,000; the IRS-calculated minimum payment is higher than you can afford; you have unfiled returns that must be filed before the IRS will even review your application; or you defaulted on a previous payment plan and are trying to get reinstated. In these situations, applying online is not an option. You need to submit Form 9465 with Form 433-F financial documentation, and the IRS reviews your income, expenses, and assets to determine what monthly payment you can actually afford.

If you propose payments that are lower than the IRS thinks you can afford based on your financial disclosure, they will reject the application or counter with higher payments. If your expenses include items the IRS considers non-allowable (luxury car payments, private school tuition, non-essential subscriptions), they will disallow those expenses and calculate a higher payment than what you proposed.

For taxpayers who cannot afford any payment right now because their income barely covers necessary living expenses, a payment plan is not the right resolution.Currently Not Collectible status pauses IRS collection efforts while you are in financial hardship. For taxpayers whose income and assets are low enough that they will never be able to pay the full balance over time, an Offer in Compromise settles the debt for less than the full amount owed. Both options require the same financial documentation as a payment plan application, but the qualification standards differ.

Tax Hardship Center works with individuals and small businesses to set up IRS payment plans and resolve tax debt when payment plans are not realistic. The firm handles cases in which unfiled returns must be filed before a payment plan can be approved, which is the most common reason applications are rejected. For clients who owe more than $50,000 or need monthly payments below the IRS minimum, the firm submits Form 9465, along with Form 433-F financial documentation and supporting records, to request payments based on actual income and necessary expenses.

When the IRS-calculated monthly payment is unaffordable given the client’s financial situation, the firm evaluates whether an Offer in Compromise, Currently Not Collectible status, or penalty abatement would provide better relief. For clients who defaulted on a previous payment plan, the firm works to reinstate or revise the plan rather than starting from scratch with a new application.

If you need to apply for a payment plan and you are dealing with unfiled returns, a balance over $50,000, unaffordable IRS-calculated payments, or a rejected application, Tax Hardship Center offers free case reviews where a specialist explains what steps are required to get approved and which payment option fits your financial situation.

FAQs

How do I request a payment plan from the IRS?

Apply online at IRS.gov using the Online Payment Agreement tool if you owe $50,000 or less. Create an IRS account, verify your identity, select the tax years to include, choose short-term or long-term, and select your payment method. If you owe more than $50,000, call the IRS at 1-800-829-1040 or mail Form 9465 with Form 433-F financial documentation.

What if I owe the IRS but can’t afford to pay?

Apply for a payment plan to spread the balance over up to 72 months. If monthly payments are still unaffordable, request Currently Not Collectible status, which pauses IRS collection efforts while you are in financial hardship. If your income and assets are low enough, you may qualify for an Offer in Compromise to settle the debt for less than the full amount owed.

What makes you eligible for an IRS payment plan?

You must have all tax returns filed, owe $50,000 or less in combined tax, penalties, and interest (individuals) or $25,000 or less (businesses), and be able to pay the balance within 72 months. You cannot have an existing active payment plan. If you meet these rules, the IRS approves most applications.

How long does it take for the IRS to approve a payment plan?

If you apply online and meet the eligibility requirements, approval is instant. You receive confirmation immediately and a letter within a few weeks. If you apply by mail or phone, approval takes 30 to 60 days. The IRS will send a letter confirming your payment plan and stating your first payment due date.

Why am I not eligible for an IRS payment plan?

The most common reasons are unfiled tax returns, a balance over $50,000 for individuals (or $25,000 for businesses) applying online, an existing active payment plan, or proposed monthly payments that are lower than the IRS minimum without supporting financial documentation. Fix the issue and reapply.

Does the IRS usually approve payment plans?

Yes. The IRS approves most payment plan applications as long as you meet the eligibility requirements and submit complete information. Rejections usually occur because of unfiled returns, missing financial documentation for large balances, or duplicate applications when an active plan already exists.

Conclusion

Applying for an IRS payment plan is straightforward as long as you meet the eligibility rules and submit complete information. The hardest part is usually making sure all your tax returns are filed first. If returns are missing, the IRS rejects the application before they even look at your payment proposal.

Once your returns are up to date, applying online is the fastest option. You get instant approval if you owe $50,000 or less, and the setup fee is lower than the cost of mailing Form 9465. If you owe more than $50,000, the online tool will reject your application, and you need to call the IRS or submit Form 9465 with financial documentation showing what you can afford to pay each month.

The IRS wants you on a payment plan. A payment plan keeps your account out of collections and provides a predictable revenue stream. As long as you propose payments the IRS considers reasonable based on your balance and repayment timeline, they approve it. But if the payments are not affordable given your actual financial situation, a payment plan is not the right solution. That is when the Currently Not Collectible status, Offers in Compromise, or penalty abatement becomes a better option.

Key Takeaways:

- All tax returns must be filed before the IRS will approve a payment plan

- You can apply online if you owe $50,000 or less (individuals) or $25,000 or less (businesses)

- Short-term plans (120 days or less) have no setup fee. Long-term plans have setup fees ranging from $31 to $225 depending on how you apply and pay

- Online applications with direct debit have the lowest setup fee at $31

- The IRS approves most payment plans as long as you meet eligibility requirements and submit complete information

- If your balance is over $50,000 or you need payments lower than the IRS minimum, submit Form 433-F with financial documentation

- Approval is instant for online applications and takes 30 to 60 days for mailed or phone applications

If you need help setting up a payment plan, your application was rejected, or you cannot afford the IRS-calculated monthly payment, get a free case review at Tax Hardship Center.