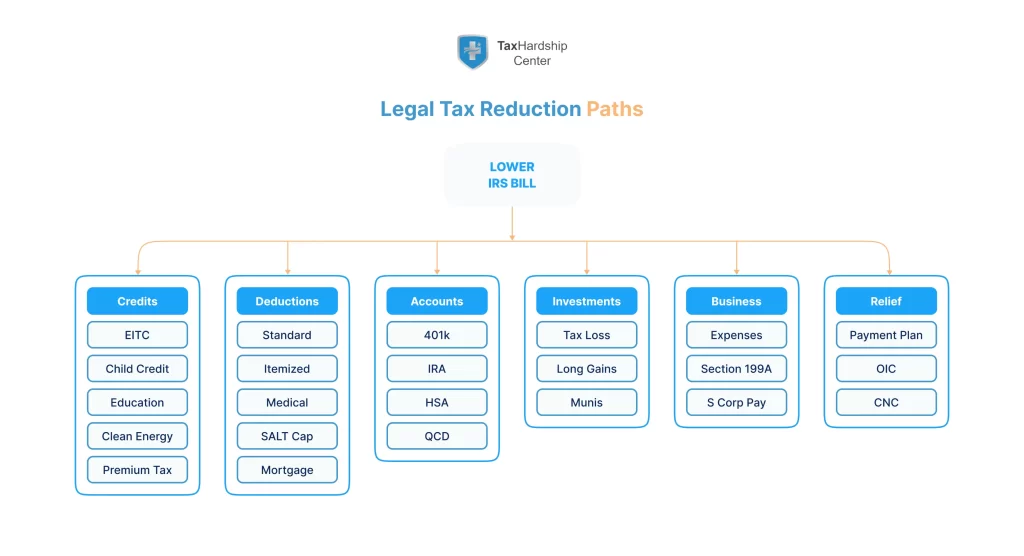

How to lower what you owe in taxes starts with credits that cut your bill dollar for dollar, followed by deductions that trim taxable income, and smart timing on retirement contributions, health savings, and capital gains. You adjust withholding early, pay estimated taxes on schedule, and keep records so your tax return claims every legal benefit. If you can’t pay in full, you choose an IRS payment plan or propose an Offer in Compromise. Seniors can route IRA gifts as qualified charitable distributions. Itemizers track medical expenses, mortgage interest, state and local taxes, and charitable donations. Investors use tax-loss harvesting and long-term capital gains rates. If a tax debt hangs over you, you use the Fresh Start options to set up a plan that fits your budget.

How to Lower Your IRS Bill with Tax Credits

Start with tax credits because credits reduce your income tax bill dollar for dollar. You line up your facts, confirm eligibility, and claim the right forms on your tax return so the credit changes your bottom line. Some credits are refundable and can increase your tax refund, while others are nonrefundable and reduce your tax only to zero. Review rules on the IRS site for the latest definitions and limits, then match your life events to credits that fit.

If you earn under a certain income level (Earned Income Tax Credit)

You check the Earned Income Tax Credit if your earned income falls in a low to moderate range. The EITC can grow with qualifying children, but workers without children can still qualify. Filing status matters, and investment income limits apply. You keep pay stubs, W‑2s, and any 1099s to support your claim and avoid delays. You file on time so the IRS processes the refundable portion without holdup.

If you’re a parent or caretaker (Child and Dependent Care, Child Tax Credit)

Parents and caretakers often qualify for the Child Tax Credit and may also claim the Child and Dependent Care Credit when they pay for work‑related care. You collect provider statements, payment records, and the provider’s taxpayer ID. You confirm each child’s Social Security number and relationship test. These credits can reduce your federal income tax and improve cash flow at tax time.

If you pay for higher education (Education Credits)

Students and families look at the American Opportunity Tax Credit and the Lifetime Learning Credit. You gather Form 1098‑T and a detailed account of qualified tuition and fees. You avoid double dipping with 529 plan distributions and the same expenses. Education credits can offset income taxes and support future earnings growth.

If you invest in clean vehicles or clean home energy (Clean Energy Credits)

You review credit rules for clean vehicles, charging equipment, and energy‑efficient home improvements. Manufacturers and property eligibility lists change over time, so you check current models and property types before you buy. These credits can lower your tax liability while you reduce energy costs. You save receipts, installation invoices, and certifications to back up the claim.

If you buy health insurance in the marketplace (Premium Tax Credit)

You reconcile advance premium tax credits with your actual income when you file. You report income changes during the year so you do not face a surprise repayment. You store Form 1095‑A and your marketplace account statements. The premium tax credit can close a budget gap while keeping your coverage.

To learn what credits exist and how they work, review the IRS page on credits and deductions for individuals, which explains the difference between credits and deductions and links to current eligibility rules. This page stays current with each tax year and helps you find the right form to file.

See the IRS credits and deductions list for current eligibility, phaseouts, and forms.

Year-Round Tax Planning to Reduce What You Owe

Plan across the year, not just in March. You anchor your numbers to each paycheck, your marital status, and your state. You set calendar reminders for every tax deadline and you move funds to a separate savings account for estimates. You track paid dividends and capital gains so withholding stays accurate. You use tools that make the math simple and repeatable.

Adjust tax withholding to avoid surprises at tax time

Use Form W-4 after any life change and recheck your math with the IRS Tax Withholding Estimator. Aim for a small refund or a small balance due. Confirm that federal income tax withholding appears correctly on your paycheck stub. If you hold two jobs, run the estimator with both incomes. Update again after a raise or a new dependent.

Pay estimated taxes timely to dodge penalties

Quarterly filers mark due dates and pay online the same day. You can use the safe harbor rule tied to last year’s tax or project this year’s bracket. If you receive a windfall or large paid dividends, add an extra estimated payment before the next deadline. Log each transaction in your accounting app and save the confirmation. Weekend or holiday due dates slide to the next business day.

Plan throughout the year for taxes, not just at filing time

Set a midyear and a fourth-quarter review. Decide whether to accelerate or defer income. Time deductible expenses such as charitable gifts and medical procedures to meet thresholds. Coordinate real estate moves and Schedule C business expenses so cash flow and taxes both improve. Keep issuer statements so end-of-year calculations go fast.

Tax Hardship Center: Get Hands-On Help Now

Our services at Tax Hardship Center focus on clear results. We review IRS transcripts, confirm where penalties and interest hit, and map a path that lowers your tax liability through legal moves. Start with an Offer in Compromise review if your finances support a settlement, or set up an affordable Installment Agreement if steady payments make more sense. If your budget shows hardship, we request Currently Not Collectible status so collections pause while you stabilize. When unfiled years block progress, our Unfiled Tax Returns team prepares accurate returns fast so we can move to the best relief track.

You get a case manager and a document checklist from day one. We explain each step in plain English and keep you posted after every IRS contact. At Tax Hardship Center, we help you turn a heavy tax problem into a set of doable actions. Book time on our Free Consultation page to see where you stand and what to do next.

Paycheck Playbook: Bonuses, RSUs, and Windfalls

You can squeeze more value from each paycheck when you plan for bonuses, equity, and windfalls before they hit. Employers treat supplemental wages under special rules, and those rules affect your tax withholding. You decide how much to set aside for federal income tax and state income tax deductions based on your full-year outlook and marital status. You funnel part of a bonus into tax-advantaged accounts to reduce taxable income. You log every transaction and keep issuer disclosures so the math holds up at tax time.

Use supplemental wage rules to shape withholding

Most payroll systems apply a flat method to bonuses and other supplemental wages, which can lead to either too much or too little withholding. You can ask HR to apply the aggregate method with your regular paycheck so the calculation reflects your tax bracket. If the company cannot change the method, you request extra withholding on the bonus check. You add that figure to your quarterly calculations so estimated taxes hit safe harbor targets. You store pay stubs and HR emails as proof if the IRS asks how you set withholding.

Direct bonuses to retirement or HSA to lower taxes

You lower taxable income when you route a slice of your bonus into a pre-tax 401(k) or HSA before the payroll cutoff. You track the maximum and catch-up contribution limits so you do not overfund. You coordinate the move with any employer match so you do not miss free money. You update beneficiary forms after life changes so account transfers stay clean. You verify the deposit on the paycheck stub and in the plan dashboard before you spend the rest of the bonus.

Manage RSUs, options, and windfalls with a written plan

RSUs trigger ordinary income when shares vest, and many brokers sell to cover taxes automatically. You still run your own calculations because paid dividends, extra shares, or same-day sales can change the final number. Stock options create different tax results depending on type and holding period, so you pencil out scenarios before you exercise. When a windfall lands, you move a set percentage to your tax savings account the same day. You update estimated payments by the next tax deadline so penalties never creep in.

Lower Taxable Income with Retirement and Health Savings Accounts

Use accounts with tax benefits to trim taxable income now while you build long-term savings. You know the maximum and catch-up contribution limits for each plan. You set beneficiaries correctly and you plan withdrawals with care so taxation does not spike later. You coordinate retirement and healthcare moves with your filing status. You keep confirmations from each issuer for clean records.

Contribute to your retirement accounts (Traditional IRA, 401(k), Saver’s Credit)

Pre-tax 401(k) and traditional IRA contributions reduce adjusted gross income. Check annual limits and catch-up rules if you are 50 or older. Low to moderate earners also review the Saver’s Credit for an extra income tax credit on top of the deduction. Verify deposits on plan statements and your paycheck. Revisit contributions after each raise so you stay on pace.

Contribute to your HSA (Health Savings Account)

An HSA works with a high-deductible health plan. Contributions reduce taxable income, growth is tax-deferred, and qualified healthcare expenses come out tax-free. Confirm your HSA custodian is FDIC insured or holds equivalent protection. Save receipts so reimbursements remain tax deductible under the rules. Use the HSA card only for eligible transactions.

If you’re older than 70½, consider a QCD (Qualified Charitable Distribution)

A QCD sends money from your IRA directly to a qualified charity. It can satisfy RMDs and keep those dollars out of taxable income. Keep the charity acknowledgment letter and your custodian’s 1099-R. A QCD can also lower Medicare premium surcharges. Coordinate with other charitable contributions so you do not double count.

Retirement Withdrawal Sequencing

Plan withdrawals with a multi-year view so taxation stays low across your retirement timeline. You choose which accounts to tap first, you watch brackets, and you smooth income to avoid spikes. You combine Roth conversions in low-income years with QCDs after age 70 and a half. You review Medicare premium brackets and the net investment income tax before large withdrawals. You mark each step in a spreadsheet so every move lines up with your goals.

Sequence withdrawals to protect brackets

You spend from taxable accounts first while capital gains rates look favorable, then pull from pre-tax IRAs and 401(k)s, and you save Roth dollars for last. You watch your tax bracket edges as you decide how much to convert to Roth in a given year. You match withdrawals to the standard deduction or itemized deductions to keep your effective rate down. You use a calculator to map the cash flow month by month. You avoid surprises by revisiting the plan each quarter.

Combine Roth conversions and QCDs

You convert a portion of pre-tax dollars to Roth when income dips, then use qualified charitable distributions later to offset required distributions. You keep charity acknowledgments and brokerage confirmations for each QCD. You record conversion amounts, withholding, and the day funds land so your tax return ties out. You adjust conversions when paid dividends or other income push you toward a higher bracket. You coordinate state rules because some states handle conversions differently.

Plan around RMD start dates

You confirm required minimum distribution start dates for each account type and birth year. You link RMDs to your cash needs, not the other way around. You avoid last-minute withdrawals that bump you into a higher bracket late in December. You set reminders with your custodian and test the automation with a small transfer first. You keep written notes so your heirs understand why the order makes sense.

Standard vs. Itemized Deductions: Which Lowers What You Owe More

Pick the path that lowers your tax the most each year. The standard deduction gives a fixed amount by filing status. Itemizing lets you deduct eligible expenses such as medical costs above a threshold, state and local taxes subject to a cap, mortgage interest, and charitable contributions. You cannot mix both paths on the same return. You run the numbers both ways before you file and you keep support for every deduction you claim. High SALT states can reach the cap fast, so timing matters.

Understand the standard deduction vs. itemized deductions

Confirm current standard deduction amounts on the IRS site before you file. Add up itemized expenses and compare the total to the standard deduction for your filing status. Consider filing status changes and home purchases that shift the math. Save statements and receipts for each itemized category. Choose the path that lowers federal income tax the most, then stick to it for the return.

If you’re itemizing, maximize your deductions (medical expenses, SALT, mortgage, charitable contributions)

Group medical procedures in one calendar year to clear the threshold. Track real estate and personal property taxes as part of SALT and mind the cap. Review Form 1098 for mortgage interest and points. Donate appreciated stock to qualified charities and keep the acknowledgment. Time property tax payments around year-end to make the most of the cap.

Charitable Giving That Cuts Taxes

Give smarter so your gifts do more for the cause and your tax bill. You pair strategy with clean paperwork, and you measure the after-tax impact before you send funds. You avoid surprises by reading nonprofit organization disclosures and by saving every receipt. You test whether itemizing or taking the standard deduction gives the bigger benefit in the same year you give. You review appreciated assets before you write a check.

Bunch gifts with a donor-advised fund

You group several years of gifts into one high-impact year by funding a donor-advised fund. You claim the deduction in the year you contribute, then you grant to charities on your own timeline. You contribute appreciated stock rather than cash to avoid capital gains tax on the built-in gain. You keep the DAF receipt and grant confirmations for your records. You still run the numbers to ensure bunching beats the standard deduction.

Donate appreciated securities instead of cash

You transfer shares with long-term gains directly to the charity. You deduct the fair market value when you itemize, subject to AGI limits, and you erase the embedded gains tax. You avoid gifting shares you held short-term because rules limit the deduction to basis. You ask the charity for its brokerage instructions and you keep the acknowledgement letter. You compare the tax results to selling the shares and gifting cash so you pick the higher tax benefit.

Track perks and discounts that reduce the deductible amount

If a gala ticket includes dinner or any discount on goods or services, you deduct only the amount that exceeds the benefit you received. You ask the charity to list the value of the perks in writing. You attach the disclosure to your digital records. You avoid rounding because the IRS matches numbers to issuer statements. You make clean notes so your accountant can finish the return fast.

Leverage Investment and Capital Strategies

Use tax-aware investing to keep more of your gains. You match gains and losses, favor long-term holding periods, and plan sales for years when your bracket is lower. You place muni bonds where they fit and you confirm state rules. You document every trade so your return ties to broker 1099s. You review your plan before year-end and again after large market moves.

Consider tax-loss harvesting to offset gains

Sell losing positions to realize capital losses that offset capital gains. Mind the wash-sale rule and avoid buying back the same or substantially identical security within 30 days. Match short-term losses to short-term gains first because those gains face higher rates. Carry unused losses forward. Export trade data to a spreadsheet and run calculations before you sell.

Review opportunities to harvest capital gains at favorable long-term rates

Hold investments for more than one year to qualify for long-term rates. Realize gains in years when your taxable income sits in a lower bracket. Coordinate gains with charitable donations of appreciated assets. Watch the net investment income tax thresholds. Consider the home sale exclusion when you meet use and ownership tests.

Invest in municipal bonds for tax-free (or tax-advantaged) income

Interest on many municipal bonds is exempt from federal tax and sometimes state tax. Match bonds to your state and your bracket. Watch for AMT exposure on certain private activity bonds. Place munis in taxable accounts and hold higher-yield taxable bonds in retirement accounts. Review official disclosures from the issuer before you buy.

Portfolio Tax Hygiene

You lower taxes by putting the right investments in the right accounts and by watching distribution season. You choose tax-efficient funds, you avoid avoidable short-term gains, and you plan around mutual fund payouts. You review beneficiary designations and transfer-on-death settings so your plan stays intact. You keep clean data that ties each lot to a trade confirmation. You write a short policy and you stick to it.

Place assets where they fit best

You hold higher-yield taxable bonds inside IRAs and 401(k)s and you place broad-market ETFs in taxable accounts. You review paid dividends each quarter and you look for funds with low turnover. You avoid frequent trading in taxable accounts because short-term gains face higher tax rates. You check wash-sale risk when you harvest losses and you record every CUSIP you replace. You rebalance on a set schedule, not on headlines.

Mind mutual fund distribution season

Many mutual funds distribute capital gains late in the year. You check estimates before you buy a fund in November or December. You prefer ETFs in taxable accounts because they tend to push out fewer taxable gains. You reinvest only when it fits your cash flow plan; otherwise you take distributions in cash for flexibility. You store issuer estimates and 1099-DIV forms with your brokerage data.

Keep beneficiary designations current

You review beneficiaries on IRAs, 401(k)s, HSAs, and brokerage transfer-on-death forms after any life change. You align those names with your will and trust. You avoid naming a minor without structure because that creates complexity. You confirm that each custodian processed the update. You print or save the confirmations for your files.

Take Business Expense Deductions (For Self-Employed or Side Hustle)

Self-employed filers trim taxable income by tracking ordinary and necessary business expenses all year. Keep clean books, save invoices, and set aside quarterly estimates so cash flow stays smooth. Use separate business accounts so transactions stay clear. Post reimbursements through an accountable plan. Store mileage logs and receipts with dates and amounts.

Deduct home office, supplies, travel, health insurance, retirement, etc.

Claim the home office deduction if you use a dedicated space regularly and exclusively for work. Track mileage or actual vehicle costs, business travel, and supplies. Deduct self-employed health insurance premiums when you qualify. Contribute to a SEP IRA, SIMPLE IRA, or solo 401(k) to reduce taxable income. Keep receipts and logs so every deduction stands up.

Use work-related education as a deduction or credit

Deduct education that maintains or improves skills for your present business. Do not deduct courses that qualify you for a new trade. Check whether the Lifetime Learning Credit gives a better result. Compare the deduction vs credit before you file. Save course descriptions and receipts with your return support.

Entity and Business Structure Moves

You choose an entity structure that fits your income, goals, and payroll needs. You measure the Section 199A qualified business income deduction and its limits. You compare Schedule C tax form simplicity to the payroll discipline an S corporation demands. You build an accountable plan so reimbursements for business expenses stay clean. You write disclosures for owners so everyone follows the same rules.

Use Section 199A when you qualify

Many pass-through businesses can claim up to a 20 percent deduction on qualified business income, subject to thresholds and limits. You measure wages and property amounts when your income rises. You separate business and personal transactions so your data stays audit ready. You track business income reduction moves such as retirement contributions and health insurance premiums. You test the deduction under different income levels before year-end.

Consider S corporation reasonable compensation rules

If you elect S corporation status, you pay yourself a reasonable paycheck before distributions. You use industry data to set the number, not a guess. You run payroll on time and you keep minutes that document decisions. You avoid commingling funds so the books stay clean. You revisit the salary as profits change.

Set up an accountable plan for reimbursements

You write a policy that lists which expenses qualify and how to submit receipts. You pay reimbursements from the business account and you keep the support with each entry. You reject late submissions so the plan stays compliant. You tie the policy to your bookkeeping software so entries post the same way every time. You train anyone who submits expenses so errors stop before they start.

IRS Transcript and Documentation Checklist

Good records make lower taxes possible. Pull IRS transcripts to confirm what the agency shows for each year. Save Notices, CP letters, and every 1099, W-2, 1098, and brokerage 1099-DIV and 1099-B. Keep marketplace Form 1095-A, childcare statements, and charity acknowledgments. Keep Schedule C invoices and bank statements for business expenses. Store files by year in one folder so your tax pro can verify the return quickly.

Special IRS Options When You Can’t Pay What You Owe

If a balance remains after credits and deductions, you still have choices. You can request a payment plan, propose a settlement, or ask the IRS to delay collection while you meet basic needs. Each path has rules and proof requirements, so gather documents first. Read the official IRS Offer in Compromise page for fees and forms. Consider penalty relief strategies as well.

Settlement options: Offer in Compromise to pay less than you owe

An Offer in Compromise lets you settle for less than the full amount when your income, assets, and expenses show limited ability to pay. Provide full financials and stay current on future filing and payment rules. Choose a lump-sum or a periodic plan. Review low-income certification rules before you file.

Hardship or delay collection, including Currently Not Collectible status

If a payment plan would cause hardship, request Currently Not Collectible status. Submit income and expense proof so the IRS can place your account in a temporary hold. Interest still accrues, but active collection stops. Revisit options when income changes and keep filing on time each year.

Innocent spouse or separation of liability relief

If a joint return created a tax debt that belongs to your spouse or former spouse, request relief. Choose the relief type that fits your facts, complete the application, and answer follow-up questions with documents. This relief can remove your liability when the law supports your claim. For more detail on relief tracks and abatement requests, see our guide to IRS penalty abatement strategies.

Deadline Calendar and Safe Harbor Rules

You avoid penalties when you know your dates and safe harbor tests. You build a simple calendar and you sync it to your phone. You send payments a few days early and you verify that the IRS posted them. You repeat the same process for your state. You keep confirmations in one folder.

Know your quarterly dates

Estimated payments usually fall on April 15, June 15, September 15, and January 15. If a due date lands on a weekend or holiday, the deadline moves to the next business day. You set reminders one week before each date. You push funds from an FDIC-insured account and you check the posting the same day. You update your spreadsheet right after you pay.

Hit a safe harbor to sidestep penalties

You stay clear of underpayment penalties when you pay at least 90 percent of the current year’s tax or 100 percent of last year’s tax. If your adjusted gross income exceeded a high threshold last year, target 110 percent of last year’s tax instead. You use last year’s return as a quick calculator for the safe harbor path. You still true up by April 15. You write the target numbers at the top of your planning sheet so you can see them all year.

Track state-specific rules

States run their own schedules and safe harbor rules. You read the instructions each year because dates shift. You align withholding at the state level when you change jobs or move. You avoid surprises by checking quarterly amounts mid-year. You save each payment confirmation with your other receipts.

Tax Rules for High-Income Earners

High earners face surtaxes, phaseouts, and progressive brackets that demand planning. Track ordinary income vs capital gains and project net investment income tax exposure. Capture charitable and retirement moves that shift your effective rate. Stage income and deductions across years to stay in favorable ranges. Coordinate stock compensation exercises with withholding and estimates.

Overview of Tax Rules for High-Income Earners and current brackets

Ordinary income follows progressive brackets while long-term gains and qualified dividends follow preferential rates. The NIIT can add a 3.8 percent layer on passive income when modified adjusted gross income crosses a threshold. Coordinate timing of bonuses, Roth conversions, and option exercises with your bracket. Build a multi-year plan so one move this year does not raise next year’s tax by more than it saves now. Keep flexibility by staging gains and deductions.

Strategic retirement/contributions and itemizing for high earners

Max out 401(k) deferrals and consider a backdoor Roth IRA when allowed. Stack charitable giving in a high-income year, including donor-advised fund gifts of appreciated assets. Track the SALT cap and mortgage interest limits for itemizing. Project taxable income under various scenarios so you land in the best bracket. Revisit the plan each quarter.

Income shifting opportunities

Shift income to family members in lower brackets when the law allows and respect the kiddie tax rules. Place high-growth assets in Roth accounts for tax-free long-term growth. Pair muni bonds and qualified dividends in taxable accounts to keep your effective tax rate in check. Confirm payroll and S-corporation reasonable compensation rules if you own a business. For a concise overview of current IRS relief paths, see our post on IRS tax debt relief options.

Real Estate and Homeowner Moves

Housing choices carry tax effects, so you plan before you list or buy. You record basis carefully, you track improvements, and you keep closing documents forever. You consider how a move changes state taxes and withholding. You protect cash by forecasting gains and the timing of sales. You keep every document the title company gives you.

Use the home sale exclusion when you qualify

You may exclude a large portion of gain on the sale of a primary residence if you meet ownership and use tests. You confirm dates with closing statements and utility bills. You add documented improvements to basis so the gain shrinks. You watch the two-year rule before you sell again. You store calculations with the closing packet.

Track depreciation and recapture on rentals

Rental property offers depreciation that reduces taxable income each year. You still account for depreciation recapture when you sell. You track assets room by room and you save invoices. You enter the data into your accounting system so Schedule E ties out. You plan the sale in a year when your bracket can handle the added tax.

Consider a 1031 exchange for investment property

You defer gains tax when you exchange investment real estate for like-kind property under strict timelines. You hire a qualified intermediary before you close. You write down the dates the clock starts and ends. You match debt and equity levels to avoid boot. You keep every intermediary and escrow record with your tax file.

Real-World Steps to Reduce Your IRS Tax Bill

Turn ideas into a quarterly checklist you can run fast. Track progress so your plan stays on course. Use a simple spreadsheet for deadlines, estimates, and contribution targets. Keep a separate account for tax savings so spending stays honest. Review the plan with a pro before year-end.

Keep detailed records to maximize deductions and credits

Create a digital folder for receipts, mileage logs, brokerage statements, and charity letters. Download payroll reports to confirm withholding and retirement contributions. Store marketplace forms, 1098-T tuition statements, and childcare records. Clean records make higher tax benefits possible and help you avoid audits. Use your software’s calculator to reconcile totals before you file.

Reassess your filing status for the best tax outcome

Run the math for married filing jointly vs separately and head of household when eligible. Account for community property rules where they apply. Check how filing status changes credits, deductions, and tax brackets. Choose the status that lowers your tax and improves cash flow. Save the comparison sheet in your files.

Talk to a tax professional (like Tax Hardship Center) for tailored help

Work with a dedicated team to gain speed and accuracy. Learn the basics from our blog on IRS payment plans and our deep dive on the Offer in Compromise. If penalties add to the bill, read our post on penalty abatement. For a yearly roundup of relief paths, see IRS tax debt relief options. Use these to frame your case, then have us build it.

Health Coverage Tax Moves

Health insurance choices affect your taxes, so you track them the same way you track income. You keep marketplace records, employer coverage letters, and COBRA notices. You read the fine print on eligibility before you switch plans. You check how premium credits change when your income shifts. You store everything with your other healthcare documents.

Reconcile the premium tax credit cleanly

You compare Form 1095-A to your return and you enter the marketplace figures exactly as listed. You report life changes fast so credits adjust in real time. You avoid refund paybacks by keeping income within the range you projected. You set a reminder to download the 1095-A as soon as it posts. You keep a copy in your tax folder and your health folder.

HSA and FSA rules differ

An HSA ties to a high-deductible plan and offers a triple tax benefit. An FSA sets annual limits and offers limited carryovers that your employer’s plan defines. You avoid funding both for the same expenses. You use an HSA for long-term savings and an FSA for near-term healthcare costs. You track every swipe so reimbursements stay clean.

COBRA and marketplace timing

If you lose a job, you compare COBRA costs to marketplace plans before you elect. You look at deductible levels, network access, and premium tax credits. You check provider networks for your doctors. You time enrollment so coverage never lapses. You keep each letter and disclosure with the rest of your records.

Client Checklist for Tax Meetings

Show up prepared and you save billable hours. Bring photo ID, last two years of filed returns, and all IRS or state notices. Include W-2s, 1099s, 1098s, brokerage 1099s, and K-1s. Add marketplace Form 1095-A, childcare receipts, and charity acknowledgments. For business owners, include bank statements, a year-to-date profit and loss, mileage logs, and receipts organized by category.

State Spotlight: California Tax Moves

California filers face high rates and unique conformity rules, so careful planning pays off. You track the SALT cap and how it hits early for many households. You read Franchise Tax Board guidance when federal and state rules differ. You watch how stock option exercises and RSU vests change state estimates. You keep every state notice and match it to your federal data.

Watch SALT limits and timing

You plan property tax payments and state estimates so you get the biggest benefit possible under the cap. You avoid doubling up in a year when you already reached the cap. You record each payment’s date and check number. You line up the numbers to issuer statements. You store confirmations with your return.

Confirm differences before big moves

California handles some deductions and credits differently than federal rules. You read instructions before you finalize a Roth conversion, a like-kind exchange, or a business deduction. You update estimates when a change affects your bracket. You adjust withholding on the next paycheck. You keep notes so next year’s plan starts faster.

Talk to Tax Hardship Center for Tailored Tax Relief

At Tax Hardship Center, we help you lower taxes the legal way and resolve balances the practical way. We map your filing status, credits, and tax bracket and build a plan that fits your budget. Start with our Offer in Compromise, Installment Agreement, or Currently Not Collectible pages to see which service fits. If unfiled years hold you back, our Unfiled Tax Returns team gets you current fast. When you want a human to walk you through options, book a slot on our Free Consultation page.

In summary…, How to Lower What You Owe in Taxes

A smart plan pulls together credits, adjustments, retirement moves, and timing. Here is a quick wrap so you can act this week.

- Credits first. Claim the EITC, Child Tax Credit, Child and Dependent Care Credit, education credits, clean energy credits, and the premium tax credit when eligible. Credits reduce income tax directly.

- Keep Social Security numbers, provider IDs, and receipts.

- Reconcile marketplace health insurance on your return.

- Keep Social Security numbers, provider IDs, and receipts.

- Adjust income. Use 401(k), traditional IRA, and HSA contributions to cut taxable income.

- If you are 70 and a half or older, use a QCD from your IRA to satisfy RMDs without raising adjusted gross income.

- If you are 70 and a half or older, use a QCD from your IRA to satisfy RMDs without raising adjusted gross income.

- Choose the better deduction path. Compare the standard deduction to itemized deductions each year.

- Track medical expenses, SALT, mortgage interest, and charitable contributions.

- Track medical expenses, SALT, mortgage interest, and charitable contributions.

- Invest tax‑smart. Use tax‑loss harvesting, long‑term capital gains rates, and municipal bonds where they fit.

- Watch wash‑sale rules and net investment income tax thresholds.

- Watch wash‑sale rules and net investment income tax thresholds.

- If a balance remains, use IRS relief. Consider a payment plan, Offer in Compromise, Currently Not Collectible status, or innocent spouse relief.

- Read official IRS pages for current fees and forms, and avoid scams.

- Read official IRS pages for current fees and forms, and avoid scams.

You win the tax year by acting early. Set two planning dates on your calendar, move money into the right accounts, and keep records. If you face tax debt, contact Tax Hardship Center so we can build a plan that lowers your bill and resolves the balance.

FAQs

How do tax credits differ from tax deductions?

Tax credits reduce your income tax bill dollar for dollar, while tax deductions reduce taxable income before the tax rate applies. Credits can be refundable or nonrefundable, and deductions work through your tax bracket. You compare both to see which combination lowers your federal tax the most.

What is tax‑loss harvesting and when should I use it?

Tax‑loss harvesting means selling investments at a loss to offset realized gains. You match short‑term losses to short‑term gains first, then long‑term with long‑term. You avoid the wash‑sale rule by not repurchasing the same or substantially identical security within 30 days. You consider harvesting near year‑end or after rebalancing.

Should I take the standard deduction or itemize?

You run the numbers both ways each year. If the sum of allowable itemized deductions beats the standard deduction for your filing status, you itemize. If not, you take the standard deduction. Life events such as buying a home, major medical expenses, or large charitable contributions can tip the scale toward itemizing.

What if I can’t pay my tax bill this year?

You still file on time, then choose an IRS payment plan, propose an Offer in Compromise, or request Currently Not Collectible status if you meet hardship rules. Interest and penalties can grow, so you act fast. A professional can help you choose the option that reduces stress and costs.

Do QCDs still work before required minimum distributions start?

Yes. Once you reach age 70 and a half, a qualified charitable distribution can go directly from your IRA to a qualified charity, even if you have not started RMDs yet. A QCD excludes the donated amount from taxable income and can lower Medicare surcharges.