If you searched “I haven’t done my taxes in 5 years,” you’re not alone. The IRS wants you to file, not hide. You can still file late returns, claim any still-eligible refunds, and set up a payment plan if you owe. The IRS can file a substitute return that overstates your tax, but you can beat it by filing the real one. Jail time rarely happens for simple nonfiling without fraud. Penalties and interest add up by the day, so fast action saves money and stress.

Why you should file your past-due returns now

Filing past-due returns stops the bleeding and sets a clean Tax Compliance History. You take control of penalties, interest, and collection risk when you get current. You also protect refunds that expire after three years. You avoid IRS substitute returns that ignore your deductions. You show good faith, which helps with payment plans and penalty relief. For official guidance on late filings, see the IRS page on filing past due returns.

Stop penalties and interest from piling up

Late filing and late payment penalties grow quickly. The failure to file penalty runs at 5 percent per month of unpaid tax up to 25 percent. The failure to pay penalty adds up monthly as well. Interest compounds on both tax and penalties until you pay. File first to cap the largest penalty, then arrange payment to slow the rest. Every month you wait costs more than a month you act.

Protect refunds before the three-year limit expires

Refund rights expire three years after the original due date. A timely Refund Request entitles you to money you already paid in. File refund years first so the IRS can send your check or apply it to another balance. If the clock runs out, no appeal brings that refund back. Put those years at the top of your stack. Check the refund status on the IRS Tax Refund website if a credit looks missing or Under Payment appears on your account.

Avoid an IRS substitute for return that inflates your tax bill

When you don’t file, the IRS can prepare a substitute return from W-2s and 1099s. That return often omits deductions, credits, and filing status that reduce tax. You can replace it by filing a correct return. The IRS will adjust your Tax Liability to match your filed return. The faster you file, the sooner you reverse an inflated Liability. For deeper context about collections and levies, read our guide on IRS tax levies.

Lower the risk of liens, levies, and wage garnishment

Unfiled years raise red flags with collections. The IRS uses liens to secure the debt and levies to seize funds. Your paycheck, bank account, and vendor payments sit in the crosshairs. Filed returns and a payment plan reduce that risk. You show compliance, which gives you leverage to request relief and to stop wage garnishment. For practical steps, see our Complete Wage Garnishment Guide.

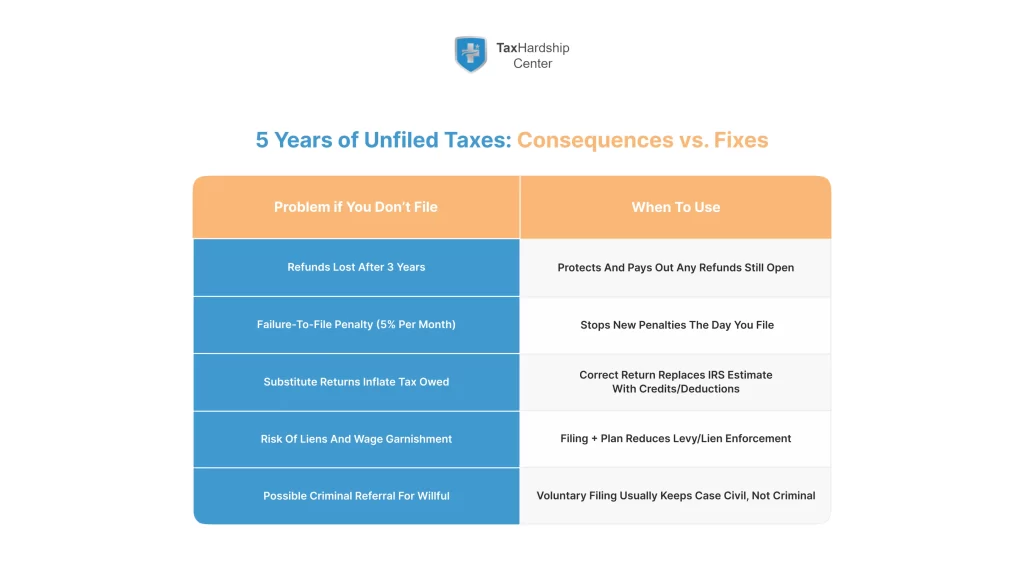

What happens if you don’t file taxes for five years

Five years without filing triggers a chain of letters and actions. The IRS starts with information it has, estimates the rest, and assesses tax. If you ignore notices, collections follow with liens and levies. Criminal cases stay rare but can occur when someone willfully refuses to file. You can still fix it with accurate returns and a plan.

The IRS files a substitute return and sends a notice of deficiency

Expect a notice of deficiency after the IRS builds a substitute return. That letter explains the proposed assessment and your right to challenge it. You can petition Tax Court or file a proper return to correct the numbers. If you do nothing, the IRS assesses the tax and starts collection. Action beats silence every time.

Collections begin: liens, bank levies, and wage garnishments

After assessment and billing, collections can kick in. A federal tax lien can attach to your property and credit profile. Levies can hit bank accounts and paychecks. Vendors may receive levy notices for freelancers. Filing, setting up a plan, or requesting hardship status can pause enforcement. Communication keeps options on the table. To understand levy math, see our wage garnishment calculation guide.

Criminal charges vs civil penalties: what really happens

Most nonfilers face civil penalties, not jail. Criminal cases usually require willful failure to file or fraud. If you hid income or lied, get counsel before you file. If you simply fell behind, accurate returns and prompt contact usually steer your case back to civil territory. Honesty and speed carry weight.

How this compares with two years of unfiled taxes

Two unfiled years bring risk, but five years raise stakes. The IRS has more data and more time to act. Penalties and interest have more months to compound. Refund years may have expired. You still control the outcome by filing now. The path back to current status looks the same, just with a thicker stack.

How to know if you failed to file a return

You may not remember what you filed. The IRS keeps transcripts that show it. Your online account lists notices, balances, and payments. You can also see if the IRS filed a substitute return. Verify the facts before you prepare anything so you build the right set of returns. If an appeal becomes necessary, our explainer on IRS Appeals walks through timelines and options.

Our services at Tax Hardship Center for multi-year unfiled returns

Our services at Tax Hardship Center focus on speed, accuracy, and protection. We build a filing order that preserves refunds and reduces exposure, then we prepare year-correct returns and set payment terms that fit your budget. We request relief where facts support it and move fast to release levies. Start with a zero-pressure call and a transcript review. Explore our core services, including Penalty Abatement, Wage Garnishment help, and the IRS Repayment Program, or book a slot on our free consultation calendar.

First steps when you haven’t filed in years

Start with facts, not guesses. Pull transcripts, then gather documents and rebuild records. Choose a filing order that protects refunds and reduces exposure. File complete, accurate returns. You set the tone for payment options and penalty relief by doing the fundamentals well. If you want a step-by-step plan, read our guide on filing back taxes with IRS help.

Pull your IRS transcripts for each unfiled year

Create or log in to your IRS account and request transcripts. Get account transcripts and wage and income transcripts for each year. Note assessment dates, penalties, and any substitute returns. Print or save them for your file. Use them to map every missing form and timeline.

Gather tax documents and reconstruct missing records

Collect W-2s, 1099s, 1098s, K-1s, bank statements, and receipts. If you lost documents, ask employers, banks, brokers, and clients for copies. Rebuild mileage logs and cost basis for investments from statements. Keep a worksheet for each year. Accuracy saves you from costly letters later.

Choose a filing order that preserves refunds and stops risk

File years with refundable money first to beat the three-year clock. Next, file the oldest balance-due years to limit penalties. Then file the rest to complete your compliance. This order protects cash and trims risk at the same time. Aim for a steady cadence so the IRS sees progress.

File refund years before the deadline; file balance-due years next

Refund years die on the three-year deadline, so move fast. Balance-due years rack up penalties, so file them next. Mail complete returns by certified mail or e-file when allowed. Track every date. Keep a control sheet so nothing slips.

How many years back you can file taxes

You can file a tax return for any past year. Refund rights expire after three years, but the right to file does not. The IRS collects for ten years after assessment, so timing matters. Know these clocks before you pick your plan. The IRS explains late-filing rules and VITA support here: Filing past due returns.

There’s no limit to file a return, but refund rights expire

You can always file an original return. The IRS will process it and adjust your account. Refunds only survive for three years from the due date. If you miss that window, the IRS cannot pay or credit the refund. File those years first when you qualify.

The three-year refund rule and the two-year payment rule

You must file within three years to claim a refund or credit a payment. If you paid late, a two-year rule may limit what you can recover. Check the paid dates on transcripts and returns. Claim what the law allows and move on quickly to other years.

The 10-year IRS collection clock after assessment

The IRS has ten years to collect after it assesses a tax. That Statute can pause during appeals, offers in compromise, bankruptcy, or while you live outside the United States. Know the assessment date for each year. Use the clock to guide your strategy, not as a reason to wait.

Tax filing deadlines for different situations

Deadlines drive outcomes. April deadlines matter for employees and contractors. Self-employed filers also face quarterly estimated tax due dates. States set their own rules for income and sales tax. Put the key dates on one calendar so you stop surprises.

Missed April deadlines, extensions, and late filing

Individual returns usually come due in mid-April. You can request Tax Extension Deadlines to October, but you must pay what you owe by April to avoid penalties. If you missed both, file as soon as you can. Late filing carries the steepest penalty. Filing now still helps even if you missed everything.

Self-employed returns and quarterly estimated taxes

Self-employed income brings Schedule C, SE tax, and estimated payments. Quarterly estimates come due in April, June, September, and January. If you skipped them, add projected estimates to your plan now. Filing complete books and starting estimates shows compliance and cuts penalties. If you run business Entities, match returns for all years.

State income and sales tax deadlines you must track

States can assess income tax and sales or use tax. Check your state’s due dates, notices, and online accounts. Register where you should have filed. If you collected sales tax, file those returns and remit the funds. States move fast on levies, so bring them current too. If a state says Tax Exempt status applies, confirm Eligibility Criteria.

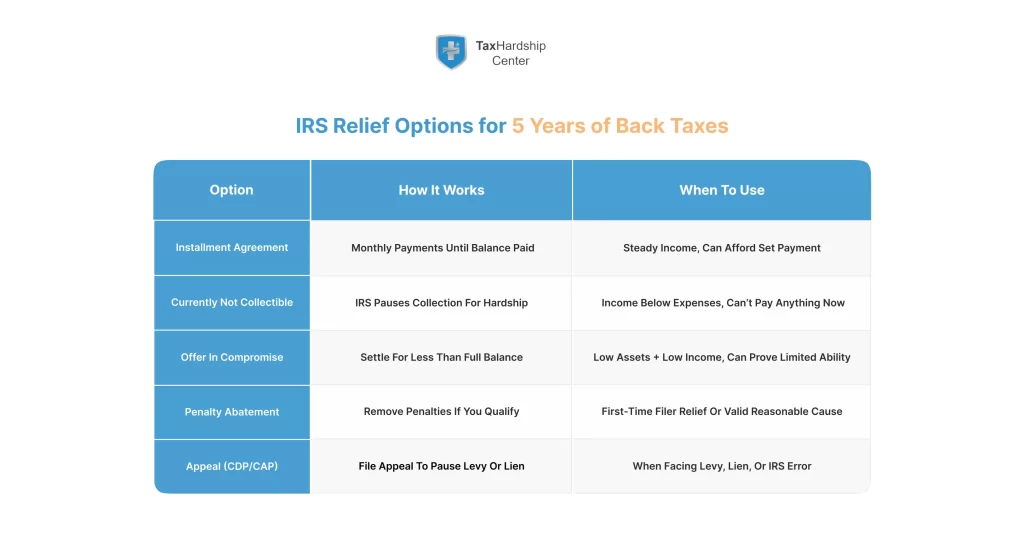

If you can’t pay the full amount of taxes owed

You can still file and manage the bill. The IRS offers payment plans, hardship holds, and settlements for those who qualify. You can also pause enforcement while you appeal or apply. A clear budget and accurate returns form your case. For structured monthly plans, review our IRS Repayment Program.

Set up an IRS payment plan that fits your budget

Installment agreements spread payments over time. Many plans use streamlined rules with simple paperwork. Propose a number you can pay every month without skipping. Auto debit helps you keep the plan in good standing. If income changes, request a new amount before you miss payments. Document Tax Payment Inability if cash flow drops.

Ask for currently not collectible status during hardship

If you can’t pay basic living costs, ask for currently not collectible status. The IRS will review your income and necessary expenses. If you qualify, it will stop active collection while your account sits on hold. Interest accrues, but you gain breathing room. Use this when Inability to pay meets the agency’s Criteria.

Consider an offer in compromise when you qualify

An offer in compromise can settle your balance for less than the full amount. You must disclose assets, income, and expenses in detail. The IRS accepts offers that equal your reasonable collection potential. Submit a complete application to avoid delays. When you need help, our OIC service explains options on the Offer in Compromise page.

Pause enforced collection with appeals and applications

You can pause levies while you appeal a proposed action. You can also pause while the IRS processes a pending installment agreement or offer. File requests on time and keep proof. Use the pause to file any missing returns and build your budget. This protects you from wage garnishments while you settle. For levy-specific tactics, see our guide on IRS levy hardship options.

Penalty abatement for unfiled tax returns

Penalty relief can save you real money. First-time abatement rewards a clean history. Reasonable cause relief helps when events outside your control stopped you from filing or paying. Ask for what you qualify for and support it with facts. Our explainer on waiving IRS penalties pairs well with the IRS page on penalty relief.

First-time penalty abatement: who qualifies and when

You may qualify for first-time abatement if you filed and paid on time for the prior three years, have no penalties for those years, and filed all required returns now. Request it for failure to file, failure to pay, or failure to deposit penalties. The IRS reviews your Tax Compliance History and grants relief for one period. Check program Availability before you call. For details, see the IRS page on Administrative penalty relief.

Reasonable cause relief: show why you couldn’t file or pay

Reasonable cause covers events like serious illness, natural disasters, theft, or reliance on bad professional advice. Provide a timeline, documents, and an explanation that shows you acted with ordinary business care. Own the mistake and show how you corrected it. Strong facts win relief more than emotion. Note any Oversight or Disturbance that blocked timely filing. For strategy, see our piece on penalty abatement strategies.

How to request penalty relief and what forms to use

You can call, write, or use Form 843 to request relief. Ask about Penalty Waiver Codes and Penalty Appeal Eligibility that match your case. Attach statements and evidence that support your claim. Track the request and follow up. If the IRS denies relief, ask for a supervisor or appeal under the Penalty Statute.

Eligibility criteria, compliance history, and penalty relief

Relief decisions follow rules. The IRS looks at Eligibility Criteria, Tax Compliance History, and the size of your Tax Liability. You improve your case when you file all unfiled tax returns, show current estimates, and document hardship.

Criteria, criteria relief, and disclosure basics

Meet the filing Criteria first. Then request Criteria Relief that applies to your fact pattern. Make full Disclosure of income, assets, and payments. Partial facts slow approvals.

What strengthens your file

File every year you missed. Pay current year estimates. Show a budget that proves Tax Payment Inability or ability to pay under a plan. Add proof of Unemployment Income, medical issues, or other facts that explain the gap.

Protect Social Security benefits and other income

Levy programs can hit federal payments. The Federal Payment Levy Program can take a share of Social Security. Filing late returns and setting up plans reduce that risk. Act before you receive a final notice.

What the IRS can take through the FPLP program

Through FPLP, the IRS can take up to a set portion of Social Security benefits to pay federal tax debt. The program does not touch Supplemental Security Income. Creditors other than the IRS cannot use FPLP. If you receive Social Security and owe tax, deal with the debt before the levy starts.

How filing and payment plans reduce levy risk

Compliance earns protection. When you file and enter a payment plan, the IRS usually stops levy actions. If a levy starts, quick filing and a plan can secure a release. Communicate, document, and keep payments current. That keeps your benefits flowing.

Six tips for filing back tax returns

You win with process. Build a checklist, use the right forms, and verify numbers before you file. Keep proof for every step. These habits shrink audit risk and speed up resolutions. For a playbook, start with our post on filing back taxes online.

Start with transcripts instead of guessing the numbers

Transcripts anchor your work. They show reported income and payments. Use them to catch missing 1099s and interest statements. Add items not on transcripts, like cash sales and basis. Accuracy today avoids letters tomorrow.

Use prior-year tax forms for each specific year

Each year has its own forms and rules. Use the correct prior-year 1040 and schedules for every return. Do not mix years. Software or the IRS website provides the right forms and instructions. Correct years prevent processing delays. If self-employed, Upgrade Schedule C Tax Form where rules changed.

e-File when possible or mail complete, signed returns

Some prior-year returns qualify for e-file. If you must mail, sign and date each return. Use certified mail with tracking and keep the receipts. Put each year in its own envelope if you mail to different addresses. Keep a log of sent dates.

Report all 1099 income and fix basis for investments

Contractors and investors must report every 1099. Reconcile gross receipts to bank deposits and books. For investments, confirm cost basis and holding periods. Correct basis prevents overpaying capital gains tax. Report Unemployment Income where it applies.

Double-check credits like EITC and child tax credit

Credits can change your outcome by thousands of dollars. Verify dependents, residency, and income limits. Use the rules for each year you file. Claim only what you qualify for and keep proof. Accurate credits increase refunds and reduce balances due.

Keep proof and track certified mail receipts

Keep a binder or digital folder for each year. Save transcripts, forms, worksheets, and receipts. Staple or attach certified mail slips to copies of returns. Documentation turns disputes into quick fixes. Organization speeds every call you make.

COVID-era disruptions and filing requirements

COVID created a real Disturbance. Many filers missed deadlines during the Pandemic because of health issues, job loss, or office closures. The IRS issued relief in some periods, but you still must meet Filling Requirements and pay what you can.

What to document from the pandemic years

Show dates of illness, job loss, or business shutdown. Keep medical notes, layoff letters, and local orders. These facts support reasonable cause claims tied to COVID.

Extra points for compliance after COVID

Restart estimates. File the oldest year each week until you finish. Note any program Availability that opened during or after the Pandemic. The IRS favors consistent compliance after a break.

Find tailored help options in your IRS account

Your IRS online account shows balances, notices, payment plans, and transcript tools. You can view tax records and set up payments in minutes. Use it to confirm what the IRS believes you owe and what years it flags. Treat it as your dashboard while you get current.

Create or log in to see balances, notices, and payment options

Set up your account with identity verification. Once inside, review balances by year, notices, and payment plan options. Download transcripts and letters. Use secure messaging when available. Check it weekly while you work through filings.

Use VITA or TCE free tax prep if you qualify

Volunteer Income Tax Assistance and Tax Counseling for the Elderly offer free help to eligible taxpayers. They prepare basic returns and help with e-filing. Bring transcripts and documents to speed the visit. If your case is complex, ask for a referral to a low income taxpayer clinic.

Refund request, appeal, and status checks

Use the IRS refund tools to track your Refund Request. On the Tax Refund Website Under Payment status page, confirm whether the IRS applied your refund to other balances. If numbers look off, file a Penalty Appeal Eligibility request or contact TAS.

When a tax audit or audit letter hits after years unfiled

A Tax Audit can arrive even while you catch up. An Audit Letter outlines issues, years, and deadlines. Read it, gather records, and reply on time. If you made a prior Disclosure, include it in your response. If you operate business Entities or claim Tax Exempt status, confirm that filings match your books.

Statute and response

Check the Statute that applies to the year. Normal audits run on a three-year rule from filing date, longer for large omissions. Respond with clear records, not estimates. If you need more time, request it before the deadline.

What to include

Provide bank statements, receipts, logs, and explanations. Tie totals to transcripts. If basis or depreciation changed, show the math. Keep tone factual. Auditors focus on documents and Filing Requirements.

Voluntary disclosure vs simply filing past-due returns

Not every nonfiler needs voluntary disclosure. Willful nonfilers with large unpaid taxes and badges of fraud should consider it. Most people who fell behind without fraud can quietly file accurate returns and move on. Choose the path that fits your facts and risk.

When voluntary disclosure applies to willful nonfilers

Voluntary disclosure helps when you hid income, used false documents, or moved assets to dodge tax. It can reduce criminal exposure if you come forward before the IRS contacts you. You must file complete returns and pay or arrange payment. Get counsel before you choose this route.

Quiet filing for non-willful cases with full accuracy

If you missed filings without willful conduct, you can file the returns with full accuracy. Include all income and correct schedules. Attach explanations only when needed. Stay available for questions. Most cases resolve with processing and a payment plan.

Reduce audit risk with complete documentation and support

Audits look for gaps and guesses. Keep source documents and workpapers for every year. Reconcile totals to transcripts and bank records. Strong files deter challenges and help you answer quickly. Clean records shorten any review.

Key IRS forms and tools you will use

The right forms speed processing and unlock relief. Prior-year 1040 packages match each year’s rules. Payment plan and financial forms build your case for terms you can afford. Penalty relief requests need simple, clear support.

Prior-year 1040 forms, schedules, and instructions

Use the IRS website or professional software to pull each year’s forms. Match schedules to your income and deductions. Read the instructions for changes and special rules. Accurate forms prevent rejects and delays. Check every Social Security number and address.

Form 9465 for payment plans and Form 433-A/OIC for finances

Form 9465 requests an installment agreement. Form 433 series shows your financial picture for tougher cases and offers in compromise. Fill them out completely and truthfully. Keep copies for your records. Accurate forms lead to faster approvals.

Form 843 to request penalty abatement when you qualify

Use Form 843 to request abatement of certain penalties and interest. Attach a statement and documents that prove first-time abatement or reasonable cause. Send it to the address that fits your situation. Track delivery and follow up after a reasonable time.

Tax software vs using a tax professional for multi-year returns

Complex multi-year cases benefit from expertise. Software can handle straightforward W-2 and 1099 situations. A Tax Return Preparer with Expertise adds value when you have business income, investments, payroll issues, Unemployment Income, or levies. Choose the path that saves the most time and risk.

When software fits

If you have a few W-2s and simple 1099s, software can work. Many platforms support prior-year returns and e-file for recent years. You still need transcripts and documents. Follow prompts and double-check credits and basis. Save PDFs and e-file confirmations.

When a pro makes sense

Hire a pro when you run a business, sold assets, received K-1s, or face substitute returns. A pro knows filing order, penalty relief rules, and payment plan tactics that software cannot teach. You also gain a buffer with the IRS. The cost often pays for itself in fewer errors and faster relief.

Tax Hardship Center can finish your filings and stop collections

At Tax Hardship Center, we help you move from stress to a signed confirmation. We map your filings, prepare accurate returns, and put collections on hold when the rules allow. Our services at Tax Hardship Center include Offer in Compromise, Bank Levy help, and Penalty Abatement. If you want to get started today, lock in a time on our free consultation page.

In summary…

A five-year gap feels heavy, but you can close it with a clear plan. Start with transcripts, protect refunds, and file accurate returns in a smart order. Use payment plans and relief tools to handle balances. Ask for help when the facts get complex.

- Quick wins

- File refund years first to beat the three-year deadline.

- File oldest balance-due years next to limit penalties.

- Pull wage and income transcripts to catch every 1099 and W-2.

- File refund years first to beat the three-year deadline.

- Payment relief

- Request an installment agreement that fits your budget.

- Ask for currently not collectible status if hardship exists.

- Consider an offer in compromise when the numbers support it.

- Request an installment agreement that fits your budget.

- Protection moves

- File before levies and liens escalate.

- Use appeals and pending applications to pause enforcement.

- Seek penalty abatement where you qualify.

- File before levies and liens escalate.

You control the next step. File one year this week, set the plan, and keep going. If you want a guide, Tax Hardship Center can lead the way from transcripts to the final confirmation letter.

FAQs

How many years can you go without filing taxes?

There is no legal limit on how far back you can file, but refund rights expire after three years from the original due date. The IRS can also collect for ten years after it assesses a tax. File now to protect refunds and to start any payment plan.

Can you go to jail for not filing taxes?

Jail for nonfiling stays rare and usually involves willful failure to file or fraud. Most cases result in civil penalties and collection actions. File accurate returns and contact the IRS to keep your case civil. Get legal advice if your facts involve concealment or false documents.

When can you request penalty abatement for unfiled returns?

Request first-time abatement when you have a clean three-year history and you filed all required returns now. Ask for reasonable cause relief when events outside your control prevented filing or payment. Use Form 843 or a written request with support. Ask whether Penalty Waiver Codes apply.

What happens if you never file taxes at all?

The IRS can file substitute returns, assess tax, and collect through liens and levies. Refunds you could have claimed expire after three years. Nonfilers can still submit accurate returns to replace substitutes and reduce balances. The sooner you file, the more options you keep.What happens if you don’t pay your taxes after you file?

Penalties and interest continue until you pay. The IRS can approve a monthly payment plan or hold collection during hardship. If you qualify, you can propose an offer in compromise. Missed payments can lead to levies and liens, so choose an amount you can sustain.