Introduction

Tax return documents serve as the foundation for every stage of IRS tax relief evaluation. These documents provide a verified financial snapshot that enables IRS reviewers to understand a filer’s income flow, dependency structure, allowable deductions, and financial obligations for a specific tax year. Each line on a tax return contributes to a broader eligibility analysis, directly connecting to the criteria used in programs such as Offer in Compromise, Installment Agreements, penalty relief requests, and hardship classifications. Without accurate tax returns, IRS analysts lack the essential information required to confirm whether the taxpayer meets program thresholds or requires updated filings.

A tax return also functions as a chronological reference point. The IRS relies on the most recently filed year to judge the filer’s current financial capacity. If a later year shows income shifts, job loss, increased medical costs, or reduced business revenue, the IRS integrates that information into hardship determinations. Outdated filings can disrupt the evaluation process, leading to pauses or complete denials until all missing or inaccurate returns are corrected. This creates a direct relationship between timely tax return submission and the likelihood of receiving favorable relief consideration.

Tax return documents also interact with IRS transcripts. While the return reflects what the filer reported, transcripts display the IRS’s verified data. Relief analysts frequently compare the two to uncover mismatches in wage information, omitted forms, or discrepancies in reported dependents. These comparisons shape the initial trust level that the IRS assigns to the case. For example, a mismatch between W-2 income and the total reported on Form 1040 may trigger an accuracy review, extending the timeline for a relief request or prompting a demand for additional documentation.

The structure of a tax return influences the IRS’s financial analysis. Specific schedules, such as Schedule C for business income or Schedule A for itemized deductions, reveal components of economic behavior that connect directly to IRS hardship standards. These elements help determine reasonable collection potential, a central calculation in tax relief eligibility. In the absence of complete schedules, IRS analysts may assume higher collectible amounts, thereby disadvantaging the filer.

Every IRS relief program relies on tax return documents to establish a baseline financial model. Their accuracy, structure, and alignment with IRS transcript data directly affect the agency’s willingness to negotiate, reduce balances, or temporarily suspend collection activity. This interconnected role makes the tax return document one of the most essential elements in preparing for an IRS tax relief request.

Key Takeaways

• IRS tax relief evaluations depend on accurate and recent tax return documents.

• IRS reviewers compare tax returns with transcripts to verify income, dependents, and deductions.

• Missing schedules or outdated returns may delay or block relief eligibility.

• Tax return line items influence financial analysis used in programs such as an Offer in Compromise and Installment Agreements.

• Structured tax return packages reduce discrepancies and improve IRS review efficiency.

Core Meaning and Function of a Tax Return Document in IRS Tax Relief Evaluation

A tax return serves as a financial blueprint that provides the IRS with a reliable overview of a filer’s economic activity during the relevant tax year. Form 1040 and its associated schedules provide structured sections that allow IRS reviewers to examine income streams, deductible expenses, dependent claims, retirement contributions, and tax credit eligibility. Each entry links to a broader set of verification checks when a tax relief request is submitted, establishing the return as the baseline evidence of financial accuracy.

Tax Return Document as a Financial Verification Instrument

The IRS uses the tax return as the initial source for confirming several core attributes:

- Total earned and unearned income

- Business revenue fluctuations

- Deduction patterns

- Household size indicators

- Filing status and dependency claims

These attributes drive later calculations involving disposable income, allowable expenses, and asset equity. When programs such as an Offer in Compromise or Currently Not Collectible status require proof of financial hardship, tax return documents supply the framework for comparing year-to-year financial changes. Line items reflecting medical costs, business losses, or decreasing wages help form the narrative of economic strain that relief programs assess.

Relationship Between Filed Returns and IRS Hardship Programs

IRS hardship programs rely heavily on tax return information to measure financial viability. The IRS links specific return values to its internal financial standards, creating a chain of relationships:

- Adjusted Gross Income connects to the allowable expense review.

- Business income on Schedule C aligns with Form 433 business asset analysis.

- Dependent claims influence household expense thresholds.

Each IRS program applies these relationships differently. For example, Installment Agreements depend on a filer’s disposable income calculation, while an Offer in Compromise integrates the tax return into a multi-year ability-to-pay projection.

Why IRS Requires the Most Recent Tax Returns Before Relief

IRS examiners require current tax returns to ensure that recent financial changes are fully documented. Outdated returns fail to reflect new employment conditions, medical expenses, or reduced revenue. Missing returns interrupt IRS processing entirely, as agency policy directs analysts to halt consideration until all required years are filed. This makes timely filing a prerequisite for any form of tax relief.

A table clarifies the role of the most recent return:

| IRS Requirement | Reason | Impact on Relief Evaluation |

| Current year filed | Ensures up-to-date income and expenses | Enables accurate financial analysis |

| All prior years filed | Confirms compliance status | Allows relief programs to proceed |

| Matching transcript data | Validates reported amounts | Prevents delays or rechecks |

These interconnected factors position the tax return as the essential reference point that shapes every stage of IRS relief decision-making.

Document Types Commonly Requested Before IRS Tax Relief Applications

IRS tax relief evaluations depend on complete financial documentation that supports the information reflected on tax return records. These document types help IRS reviewers confirm income accuracy, validate hardship claims, and assess the filer’s ability to meet payment arrangements or qualify for specialized relief programs. The request list varies by program but generally centers on income evidence, supporting schedules, business records, living expense proofs, and IRS-generated transcripts.

Wage documents are among the central categories. W-2 forms outline employment income, withholding totals, and Social Security contributions. Multiple employers within a tax year create multiple W-2 entries that IRS analysts compare with Form 1040 income totals. For contractors, freelancers, and gig workers, the 1099-NEC and 1099-MISC forms provide a parallel source of income verification. Investment activities, interest payments, and retirement distributions are reported on 1099-DIV, 1099-INT, and 1099-R forms. These documents collectively reveal the scope of taxable and nontaxable income streams, allowing IRS reviewers to identify unreported or underreported amounts.

Another essential category includes business documents. Schedule C filers often present profit-and-loss statements, expense ledgers, and bank statements showing revenue deposits. These items help bridge the information between the tax return and actual operating activity. Missing business documentation may prompt IRS scrutiny, especially when reported expenses or losses appear inconsistent with industry norms.

IRS transcripts constitute a separate, robust set of documents. Wage and Income Transcripts provide IRS-verified income data collected from employers and financial institutions. Return Transcripts summarize the return as processed by the IRS, including key line entries. Record of Account Transcripts merges return and account activity, capturing adjustments, penalties, or amended information. These transcripts help IRS reviewers compare the filer’s documents with the agency’s own data collections.

Hardship documentation frequently influences relief outcomes. Medical bills, disability records, foreclosure notices, unemployment records, divorce decrees, and disaster loss statements provide context for financial instability. These documents do not replace tax returns; they substantiate the hardship narrative used during the relief evaluation.

A high-level grouping clarifies the functional categories:

- Income verification documents

- IRS transcripts and account summaries

- Business activity records

- Household expense proof

- Hardship evidence tied to life events

- Asset and liability statements for equity review

The completeness of these document groups determines the efficiency of the IRS review. Gaps in any category may trigger information requests that extend processing times or complicate eligibility assessment. When aligned with tax return entries, these documents provide the clarity needed for accurate financial modeling in any tax relief program.

How IRS Cross-Checks Tax Return Documents During Tax Relief Screening

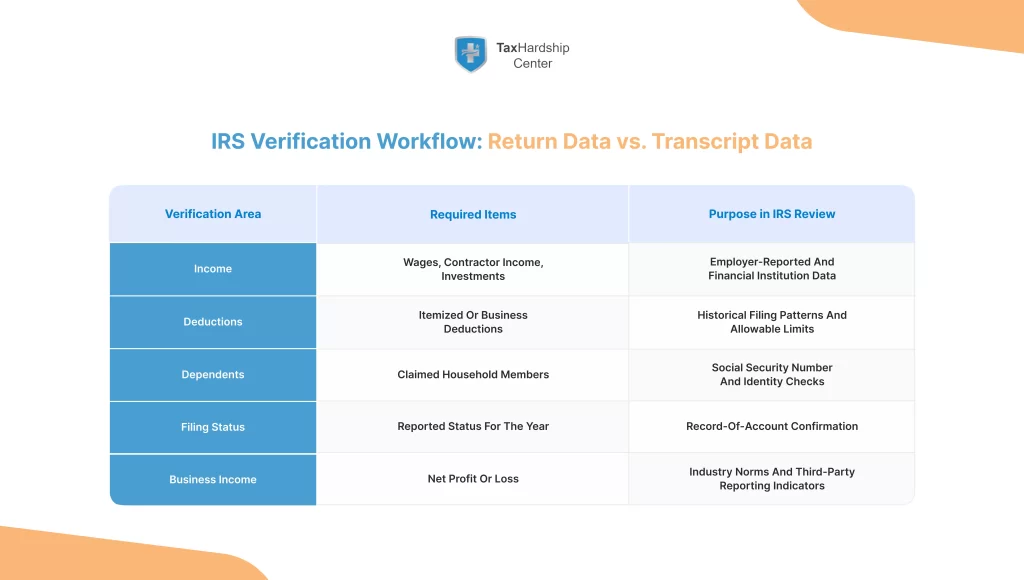

IRS tax relief screening relies on systematic cross-checking of tax return information against third-party data the agency already holds. This verification process identifies inconsistencies that may affect eligibility or require correction before the relief application proceeds. The goal is to establish a consistent financial record that accurately represents the filer’s circumstances.

The first stage of cross-checking involves income matching. IRS Wage and Income Transcripts collect employer-submitted wage data, contractor payment records, and financial institution reports. These records are compared directly to the income totals declared on Form 1040. Any mismatch in W-2 earnings, 1099 income, or interest and dividend figures may produce a flagged discrepancy. If the difference appears significant, IRS examiners may request clarification, corrected forms, or an amended tax return.

Another cross-checking stage involves validating deductions and credits. Schedules such as Schedule A and Schedule C often require additional substantiation when deductions appear unusually high relative to income level. IRS analysts compare deduction claims against industry averages, lifestyle indicators, or historical filing patterns. For example, business travel deductions may undergo review when revenue declines sharply while expenses increase.

Dependency verification forms another vital check. IRS databases track Social Security numbers claimed as dependents. When two taxpayers claim the same dependent, or when a dependent’s claims fail to align with IRS records, reviewers may delay a relief request pending resolution.

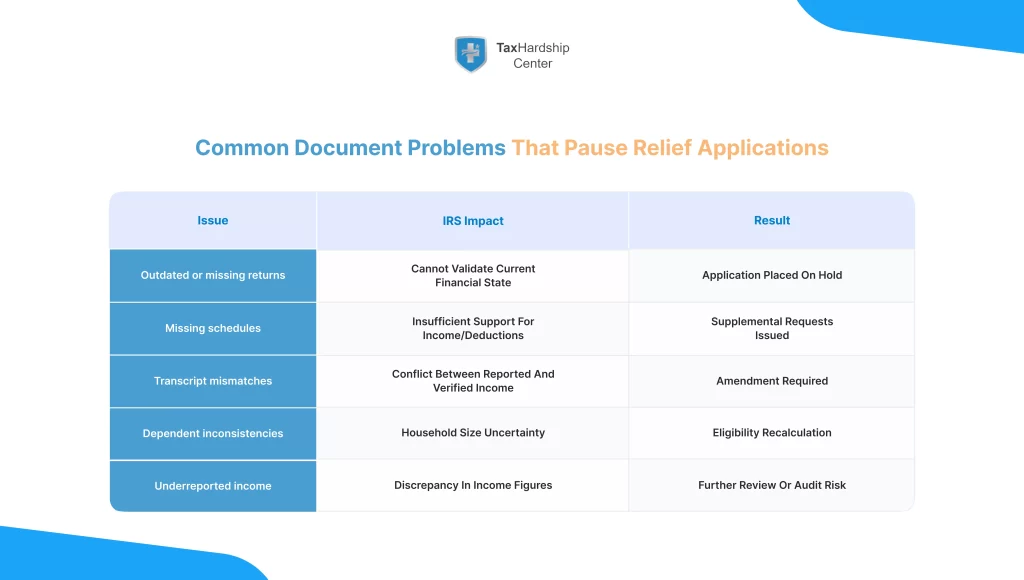

Common discrepancies identified during cross-checks include:

- Missing schedules supporting income or deductions

- Discrepant wage figures between W-2 totals and reported income

- Outdated returns not reflecting current financial conditions

- Filing status inconsistencies detected across IRS databases

A structured comparison clarifies the role of cross-checking:

| Verification Area | Source Document | IRS Reference Data | Potential Issue |

| Income totals | Form 1040 | Wage & Income Transcript | Underreported amounts |

| Deductions | Schedule A or C | Industry norms, historical filings | Unsupported or inflated expenses |

| Dependents | Form 1040 | Social Security database | Duplicate claims |

| Filing status | Form 1040 | IRS account records | Mismatch between years |

Cross-check results guide the next steps. If the information aligns, relief processing continues. If inconsistencies arise, IRS policy requires correction before any relief program can be approved. This systematic approach ensures that tax relief decisions are based on reliable, verified financial information.

Tax Return Document Requirements for Specific IRS Tax Relief Programs

Different IRS tax relief programs use tax return documents in distinct ways, but all rely on these records to measure financial capacity and compliance history. Each program applies its own analytical framework, linking tax return line items to key eligibility components such as income thresholds, allowable expenses, or asset equity.

The Offer in Compromise program examines whether the filer’s tax liability can be settled for less than the amount owed. In this program, IRS analysts assess tax return documents to determine income stability, business trends, and deductions associated with necessary living expenses. Schedules revealing business losses or medical deductions may strengthen the case by demonstrating reduced financial capacity. The IRS also checks whether the most recent return reflects current conditions, as outdated filings may distort the reasonable collection potential calculation.

Installment Agreements rely on a separate set of calculations. Here, the IRS uses the tax return to establish baseline income and compare it with the monthly cash flow reported on Form 433-A or Form 433-F. Wage income, business revenue, and investment totals from the tax return help shape the payment amount the IRS expects. If tax return documents show rising income trends, analysts may propose higher installment amounts.

Currently, Not Collectible status requires proof that the filer cannot meet basic living expenses. Tax return information becomes essential in verifying household size, dependency structure, and income patterns. A mismatch between reported income on Form 1040 and bank statements may disqualify an applicant. Consistent decreases in revenue, supported by tax returns over multiple years, often support a stronger case.

Penalty Abatement requests also depend on tax return data. Specific penalties are based on patterns of late filing or discrepancies across multiple years. Reviewing historical returns allows the IRS to determine whether circumstances such as illness, disaster, or unavoidable disruptions justified the failure to comply. Tax return timelines help establish whether the claim meets reasonable cause criteria.

A categorized summary highlights how programs use tax return documents:

- Offer in Compromise: income verification, trend analysis, deduction validation

- Installment Agreements: payment capacity determination

- Currently Not Collectible: financial hardship confirmation

- Penalty Abatement: compliance history and cause evaluation

These programs require fully filed and accurate tax returns, as incomplete filings halt eligibility reviews. The role of tax return documents in each program reflects a broader IRS priority: establishing a clear financial portrait before granting any form of relief.

Structure and Components of a Strong Tax Return Document Package

A robust tax return document package provides a complete and coherent financial profile, enabling IRS reviewers to assess eligibility for tax relief programs without requiring repeated clarifications. The strength of the package lies in how well the contents reflect income accuracy, expense validation, and consistency with IRS transcript data. Clear organization, current filings, and complete schedules form the core elements that determine whether the IRS can process a relief request efficiently.

The foundation of a strong package starts with an accurately prepared Form 1040 and all related schedules. Income reported on the form must align with W-2 statements, 1099 forms, and investment summaries that the IRS has already received from third parties. Schedules documenting business activity, rental income, capital gains, or itemized deductions ensure that reported figures can be interpreted within the proper financial context. Missing schedules are among the most frequent triggers for information requests during tax relief reviews.

Supplementary documentation helps IRS analysts understand real-world financial conditions beyond what appears on the return. Recent bank statements show cash flow patterns, automatic withdrawals, and essential living expenses that reinforce information disclosed in financial statements accompanying tax relief applications. Mortgage statements, auto loan summaries, and insurance invoices clarify recurring liabilities that influence disposable income calculations.

A key strength of a well-prepared package is chronological consistency. Returns must be filed for all required years, and each document should match the timeline of events reflected in the relief request. Households experiencing income loss, medical events, or significant financial disruptions often provide supporting documents with specific dates that must align with the return entries. IRS examiners rely on coherent timelines to validate hardship claims.

Clear document organization improves IRS processing. Separate folders or digital sections arranged by category reduce the likelihood of missing records. A practical grouping includes:

- Filed return copies

- IRS transcript records

- Income verification forms

- Business revenue and expense reports

- Hardship-related documents

- Asset and liability summaries

- Household spending records

A structured table captures the main components and their roles:

| Component Category | Example Documents | IRS Function |

| Core tax return | Form 1040, Schedules | Baseline financial review |

| Income proof | W-2, 1099, pay stubs | Income verification |

| Business records | Profit and loss statements | Revenue confirmation |

| Household expenses | Bank statements, invoices | Living expense analysis |

| Hardship evidence | Medical bills, unemployment records | Hardship validation |

A cohesive package minimizes discrepancies, reduces review times, and supports accurate IRS analysis across all major tax relief programs.

Distinctions Between Tax Return Documents and IRS Transcripts

Tax return documents and IRS transcripts provide parallel but distinct layers of financial information that IRS analysts use when assessing tax relief requests. The tax return represents the filer’s self-reported data, while transcripts reflect IRS-verified records. Understanding the differences between the two helps clarify why both are used during tax relief evaluations.

A tax return document contains the financial details provided by the filer, including income totals, deductions, credits, and household information for the tax year. Schedules accompany the return when financial activities require additional reporting, such as business operations, rental income, or capital transactions. These documents serve as narrative tools that describe the filer’s financial story from the filer’s perspective.

IRS transcripts, by contrast, summarize information as received from employers, financial institutions, and the IRS processing system. A Wage and Income Transcript compiles third-party data, including W-2 wages, 1099 contractor payments, interest earnings, and retirement distributions. This transcript acts as the IRS’s reference point for income verification. A Return Transcript provides a processed snapshot of the tax return, showing how the IRS recorded the entries. A Record of Account Transcript merges return information with subsequent account actions, including penalties, amendments, or adjustments.

The distinctions can be summarized in a structured comparison:

| Feature | Tax Return Document | IRS Transcript |

| Source | Filed by the taxpayer | Generated by IRS |

| Content Type | Reported income, deductions, credits | Verified data from payers and IRS systems |

| Primary Use | Eligibility assessment and financial context | Accuracy verification and discrepancy checks |

| Format | Form 1040 + schedules | Transcript categories (Wage & Income, Return, Record of Account) |

| Role in Relief | Forms the baseline financial narrative | Confirms or contradicts reported amounts |

These differences significantly affect relief evaluation. When a return reports income that does not appear on transcripts, IRS analysts investigate the mismatch. When transcripts reveal additional income sources not reflected on the return, relief processing may halt until amendments are filed. Conversely, when transcripts confirm all reported figures, relief processing moves forward with fewer delays.

Both documents serve complementary functions: the return explains financial conditions, and the transcript verifies their accuracy. Relief decisions rely on the alignment of these two information sources, making their distinctions central to the evaluation process.

Pre-Application Checklist for IRS Tax Relief: Required Tax Return Elements

IRS tax relief programs require a complete set of financial documents before analysts can begin evaluating eligibility. A structured checklist clarifies the elements the IRS expects to find within a compliant tax return file. These elements ensure that the agency can verify income, confirm household composition, determine allowable expenses, and assess financial capacity through internal modeling.

The first step is to verify filing status. Filing status determines tax rate ranges, dependency allowances, and access to certain credits. Inconsistencies between filing status entries and household documentation often slow the relief process. When status changes occur due to marriage, divorce, or separation, the return must reflect correct documentation for the applicable year.

Income records form the core of the IRS checklist. All sources listed on Form 1040 must align with W-2 statements, 1099 forms, and investment summaries. Income volatility is especially relevant in relief reviews, as sudden shifts in wage patterns, contractor payments, or business revenue influence the IRS’s calculation of payment capacity. Relief programs such as Installment Agreements rely on accurate income reporting to determine feasible monthly contributions.

Supporting schedules must accurately reflect financial activity. Schedule A entries should match receipts, invoices, or statements if itemized deductions are used. Schedule C returns require enough detail to illustrate business operations, including revenue streams, expense categories, and net gains or losses. Missing schedules or mismatched figures often lead to clarification requests from IRS reviewers.

Hardship evidence becomes central to the checklist when relief programs rely on financial distress indicators. Medical billing histories, disability documentation, foreclosure notices, unemployment statements, or disaster impact forms help IRS analysts link financial hardships to tax-year changes. These documents provide context for variations found on tax returns across consecutive years.

A structured checklist clarifies the key elements:

- Verified filing status.

- Accurate income reporting across all income categories.

- Complete schedules matching financial activities.

- Supporting documents for significant deductions.

- Documentation of household size and dependents.

- Evidence of relevant life events impacting financial conditions.

- IRS transcripts to confirm reported information

The IRS compares these elements with its internal data sources. Any missing or inconsistent item may halt processing until corrected. Relief programs require a consistent narrative across returns, schedules, and external documentation. When the checklist is satisfied, IRS analysts can proceed with a complete financial analysis and determine whether tax relief measures are available.

How the Tax Hardship Center Supports Document Preparation

Tax documentation requirements for IRS relief programs often create challenges for households with complex financial histories or multiple income streams. Incorrect filings, missing schedules, or misaligned transcript data frequently lead to delays during eligibility review. Professional assistance can help create document sets that meet IRS standards, allowing relief applications to advance without repeated requests for clarification.

Tax Hardship Center provides services that address several points within the IRS documentation process. The organization assists with reviewing prior-year returns, identifying missing schedules, and correcting inaccuracies that may affect relief consideration. When inconsistencies arise between tax return entries and IRS transcripts, analysts can help reconcile them by updating filings or analyzing transcripts. This reduces the likelihood that relief applications will be paused due to document mismatches.

Households facing business income reporting challenges often require precise preparation of Schedule C, Schedule E, or other relevant forms. Tax Hardship Center can review business revenue and expense records to ensure that the information provided to the IRS reflects actual financial conditions. Accurate schedules help prevent the IRS from making assumptions that might otherwise overstate net income or household earning capacity.

Relief application packages also require extensive supporting documentation. Mortgage statements, insurance invoices, childcare records, medical expense histories, and unemployment records help illustrate the financial landscape that IRS analysts must consider. Assistance in gathering and organizing these documents improves the clarity and credibility of the relief request.

By ensuring that the tax return file, schedules, supporting records, and transcripts align with IRS requirements, the Tax Hardship Center contributes to more efficient relief processing. Prepared, coherent documentation allows IRS analysts to evaluate cases more quickly and require fewer follow-up requests.

FAQ Section

What documents typically accompany a tax return during IRS tax relief review?

IRS relief reviewers examine income forms such as W-2s and 1099s, investment statements, and, when applicable, business records. Additional documents may include bank statements, medical billing histories, mortgage statements, unemployment records, and IRS transcripts. These items confirm the accuracy of return entries and provide context for hardship claims.

How do IRS transcripts interact with tax return documents during evaluation?

IRS transcripts supply verified wage, income, and account information gathered from employers, financial institutions, and IRS internal systems. Relief analysts compare transcript data to filed returns to confirm accuracy. Discrepancies may prompt requests for clarification or amendments before a relief program can be approved.

Why must all required tax years be filed before IRS relief consideration?

Relief programs rely on a complete filing history to determine eligibility and verify compliance. Missing returns disrupt the process because IRS analysts cannot accurately evaluate financial circumstances until all tax years are accounted for. Filing gaps may delay or suspend relief applications until returns are brought current.

What tax return details most influence hardship evaluations?

Income trends, business revenue, net profits, medical deductions, household size, and changes in filing status carry significant weight. These elements shape IRS calculations related to disposable income, allowable expenses, and asset equity. They also provide context for sudden financial shifts relevant to hardship determinations.

When does the IRS require an amended return before granting relief?

Amended returns are required when the filer’s return contains incorrect income figures, missing schedules, erroneous filing status, or any discrepancy that conflicts with transcript data. Relief evaluations cannot continue until the amended return aligns with verified records.

How do dependent claims affect tax relief eligibility?

Dependent claims influence household size, which connects directly to allowable living expense limits and financial standards used in relief evaluation. Conflicting dependent records or duplicate claims may delay relief decisions until the IRS resolves the discrepancy.

What role do business schedules play in tax relief assessments?

Schedules such as Schedule C or Schedule E illustrate revenue patterns, business expenses, and net profits. These details help IRS analysts evaluate the financial stability of business operations, identify allowable deductions, and determine accurate income levels for relief programs requiring projected financial capacity assessments.

Conclusion

Tax return documents anchor every stage of IRS tax relief evaluation. These documents serve as the primary reference point that illustrates income structure, household size, financial obligations, and changes in economic conditions across tax years. When paired with accurate schedules, IRS transcripts, and supporting documentation, tax returns supply a cohesive financial narrative that allows IRS analysts to conduct eligibility assessments with clarity.

The alignment between return entries and IRS-verified transcript records determines whether relief evaluations proceed without delay. Missing schedules, outdated filings, or inconsistencies across data sources often create obstacles that extend processing times or require amendments. When returns demonstrate documented hardship through income shifts, medical expenses, or business downturns, the IRS incorporates these indicators into its financial modeling.

The preparation of a complete, accurate, and well-organized tax return package increases the likelihood of efficient review. These documents connect directly to program-specific evaluations, including Offer in Compromise assessments, installment calculations, penalty relief considerations, and hardship classifications. A structured, consistent approach to tax documentation ensures that IRS reviewers can accurately interpret financial conditions and determine the appropriate form of relief in accordance with established IRS standards.