If you are searching for a payment arrangement with the IRS, you are likely trying to solve one problem quickly: you owe taxes and need a realistic plan to prevent the situation from escalating.

The good news is that most taxpayers have options, and many can apply online in minutes. The key is choosing the right plan type for your balance and budget, then applying it correctly so the IRS approves it without unnecessary back-and-forth.

What A Payment Arrangement With The IRS Means

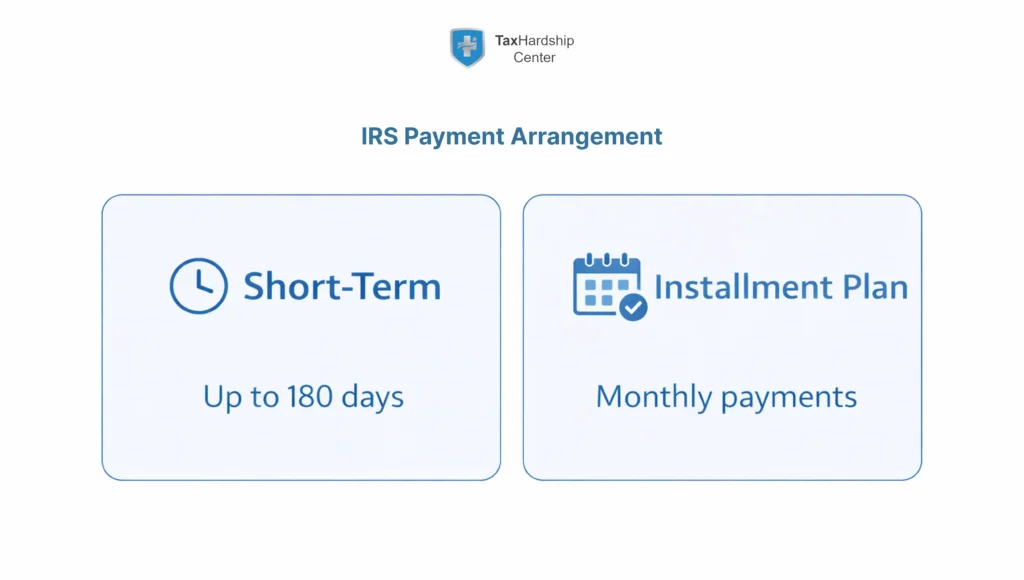

A payment arrangement is simply an agreement to pay what you owe over time instead of all at once. The IRS generally describes two main plan types for individuals who apply online:

- A short-term payment plan (pay in full within 180 days)

- A long-term payment plan, also called an installment agreement (monthly payments)

Even when you are on a plan, interest and certain penalties typically continue until the balance is paid in full. That is why the “right” plan is the one you can actually keep, without missing payments.

IRS Payment Arrangement Options (Side-By-Side Comparison)

Below is a practical comparison of the most common IRS payment arrangement routes people use.

| Option | Best For | Common Eligibility (Online) | Typical Timeframe | How To Apply |

| Short-Term Payment Plan | You can pay in full soon | Owe less than $100,000 total (tax, penalties, interest) | Up to 180 days | Online Payment Agreement |

| Long-Term Payment Plan (Installment Agreement) | You need monthly payments | Owe $50,000 or less total, and filed required returns | Monthly, often up to 72 months | Online Payment Agreement |

| Apply By Mail (Form 9465) | You cannot apply online, or IRS requests more info | Varies | Varies by case | Form 9465, sometimes with Form 433-F |

| Business Online Plan | Small business balance, current and prior year | Owe $25,000 or less total, filed required returns | Monthly, often up to 24 months | Online Payment Agreement |

Note on direct debit: the IRS encourages direct debit for long-term plans and states it is required for certain balances, including individual balances between $25,000 and $50,000.

How To Choose The Right Installment Plan

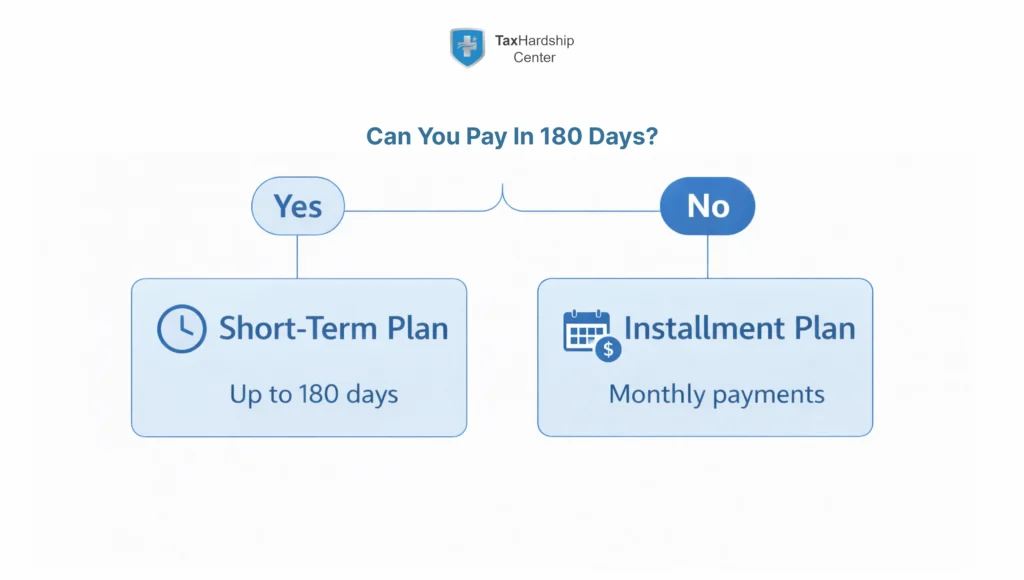

Start With One Simple Question

Can you realistically pay the full balance within 180 days?

- If yes, a short-term payment plan can be a clean option, and IRS guidance notes that there is no setup fee for this plan type (though interest and late-payment penalty continue).

- If no, you are usually looking at a long-term payment plan (installment agreement).

Match The Plan To Your Risk Level

If you are already receiving collection notices, the “right” plan is the one that gets approved quickly and prevents escalation.

For many taxpayers, applying online is the fastest path because the IRS states you receive immediate notification of approval after completing the application.

If Your Balance Is Higher Or Your Situation Is More Complex

If you cannot self-qualify online, you may still be able to pay in installments, but the process can involve paper forms and financial documentation.

How To Apply The Right Way (Online, Form 9465, Phone)

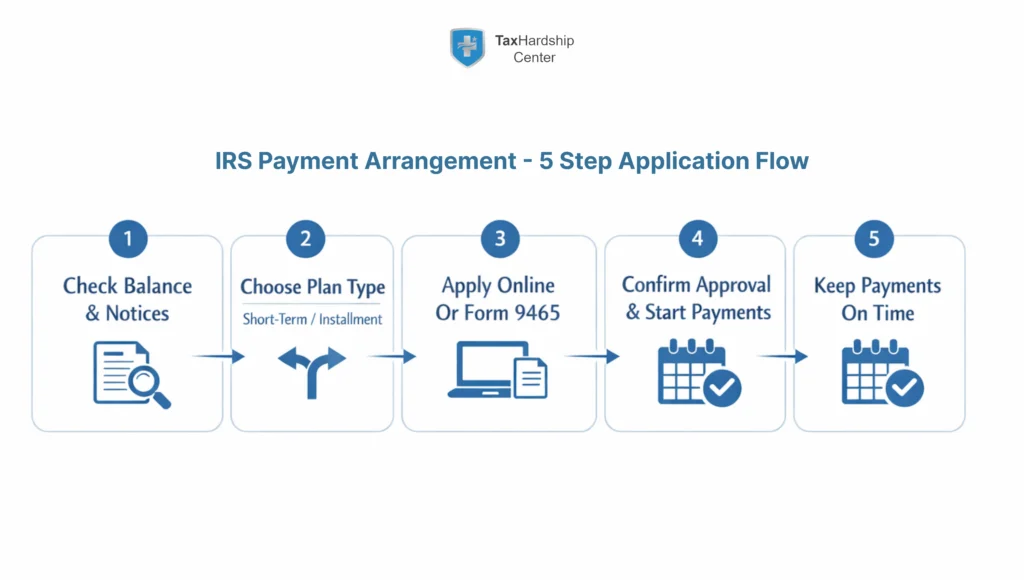

Step 1: Confirm You Are Eligible To Apply Online

The IRS lists common online eligibility guidelines for individuals:

- Long-term payment plan: owe $50,000 or less total, and filed all required returns

- Short-term payment plan: owe less than $100,000 total

Step 2: Gather What You Need Before You Apply

Have these ready:

- Your IRS Online Account access (you generally need photo ID to create it)

- Your notice and the tax years involved

- Bank routing and account numbers if using direct debit

Step 3: Apply Through The IRS Online Payment Agreement Tool

The IRS Online Payment Agreement system is designed to let qualified taxpayers apply and get immediate approval decisions in many cases.

When choosing your monthly payment, aim for an amount you can maintain even in a “tight month.” Defaults often happen when a payment is set too aggressively.

Step 4: If You Cannot Apply Online, use Form 9465 or Call

The IRS states that if you are ineligible for online access, you can still request installments. One common route is Form 9465, and the IRS also notes that, in some cases, you must attach additional financial information, such as Form 433-F.

Fees, Penalties, And What Changes After Approval

Setup Fees (What Most People Miss)

The IRS lists setup fees for installment agreements, and they vary based on how you apply. For example, the IRS payment plan page lists:

- Apply or revise online: $10

- Apply or revise by phone, mail, or in-person: $89

- Low-income fees may be reduced and reimbursed under certain conditions

Low-income taxpayers may qualify for waiver or reimbursement rules, and the IRS references Form 13844 for those who believe they qualify but were not identified automatically.

Late-Payment Penalty Can Be Lower While An Installment Agreement Is Active

The IRS notes that for taxpayers who filed on time, the late-payment penalty rate is reduced while an installment agreement is in effect, and it describes the reduced rate as 0.25% per month (instead of up to 1% per month).

Interest And Some Penalties Still Continue

Even with a plan, the IRS states interest and some penalty charges continue until the balance is paid in full.

If You Cannot Afford The Minimum Payment

Sometimes the real issue is not choosing between short-term and long-term; it is that any payment would create a hardship.

The IRS explains that if it determines a taxpayer is unable to pay, it may temporarily delay collection until the taxpayer’s financial condition improves, though penalties and interest can continue to accrue.

This is also the point where taxpayers often compare:

- Installment agreement

- Temporary hardship delay

- Offer in Compromise (settlement), if eligible

Common Mistakes That Cause Delays Or Defaults

- Applying online before all required returns are filed, which can block approval.

- Choosing a monthly payment that is not sustainable, then defaulting a few months later.

- Ignoring direct debit requirements for certain balances, which can cause friction or delays.

- Not saving proof of approval, payments, and any plan changes made online. The IRS states you can review and revise many plan details through the Online Payment Agreement tool.

- Missing that a setup fee applies for long-term plans, and low-income rules may change what you owe.

When To Get Professional Help

Many taxpayers can set up a payment arrangement themselves. Professional help is most valuable when:

- You owe more than the online thresholds, or you have multiple years involved.

- The IRS is asking for financial statements (Form 433 series), and you want the proposal built correctly.

- You are trying to decide between a payment plan, hardship status, or settlement, and you want the fastest path with the lowest long-term cost.

Tax Hardship Center offers a free consultation entry point for taxpayers who want help selecting and setting up the right resolution strategy.

FAQs

What Is The Difference Between A Short-Term And Long-Term IRS Payment Plan

A short-term plan gives you up to 180 days to pay in full and typically has no setup fee, while a long-term plan involves monthly payments and usually has a setup fee.

Can I Apply Online For An IRS Payment Arrangement

Many individuals can apply online if they meet the IRS thresholds (less than $100,000 for short-term, $50,000 or less for long-term, plus filing compliance).

How Much Is The IRS Installment Agreement Fee

The IRS lists different fees based on how you apply, including an online apply or revise fee of $10 and a phone, mail, or in-person fee of $89. Low-income fees may be reduced and reimbursable under certain conditions.

Does An IRS Payment Plan Stop Interest And Penalties

No, the IRS states interest and some penalty charges continue until the balance is paid in full.

Can I Change My Monthly Payment After The Plan Is Approved

Yes, the IRS states you can use the Online Payment Agreement tool to make changes such as payment amount, due date, and converting to direct debit.

What If I Cannot Qualify Online Or Cannot Afford The Payment

The IRS notes you may still be able to pay in installments through Form 9465, and in some cases you may need to provide additional financial information. It also describes delayed collection when you are unable to pay.

Conclusion

A payment arrangement with the IRS is often the most straightforward way to stabilize back taxes, especially when you act early and set a monthly payment you can maintain. Start by checking whether you can pay in full within 180 days. If not, compare long-term installment options, apply online when eligible, and use Form 9465 when you cannot self-qualify online.

If your case is complex, your balance exceeds the online thresholds, or you are deciding between a payment plan and other relief options, getting guidance can help prevent costly mistakes and defaults.

Key Takeaways:

- Short-term plans give up to 180 days to pay in full, and long-term installment agreements create monthly payments.

- Many taxpayers can apply online and receive immediate approval decisions.

- Setup fees depend on how you apply, and low-income taxpayers may qualify for reduced, waived, or reimbursed fees.

- Interest and some penalties usually continue until the balance is paid in full, so choose a plan you can sustain.

- If you cannot afford the payment, alternatives like delayed collection or settlement evaluation may be more appropriate.