You closed on your California home. You set up your mortgage, got your first regular property tax bill, and then another bill arrived in the mail. It says “supplemental property tax,” and it is not small.

This is not a mistake. It is not a duplicate. It is a separate, legally required tax bill that most California homebuyers are never warned about before closing.

Here is what it is, how it is calculated, when it is due, and what to do if you disagree with the amount.

What Is California Supplemental Property Tax?

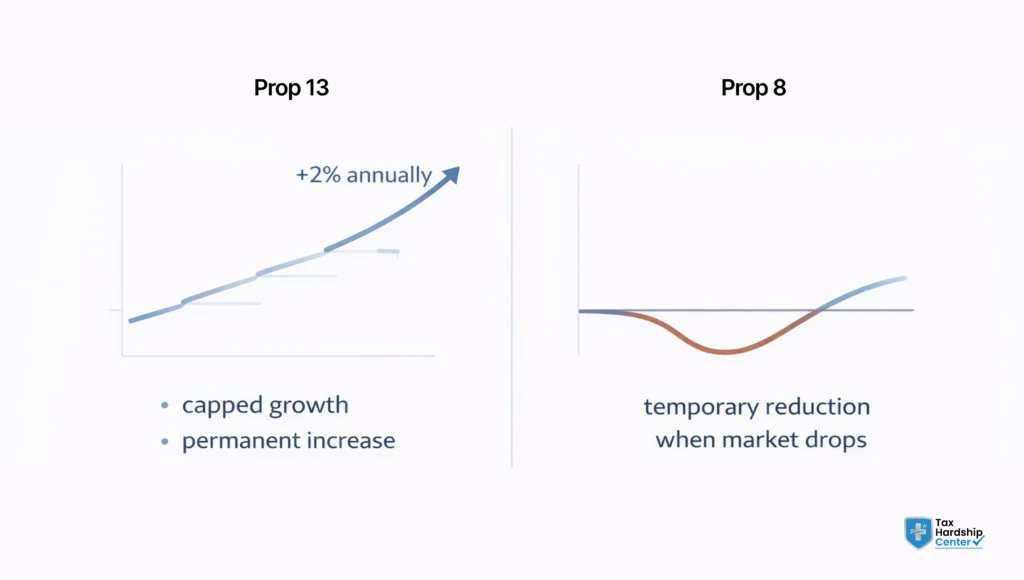

California property taxes are governed by Proposition 13, which passed in 1978. Under Prop 13, your property is assessed at its purchase price and can only increase by up to 2 percent per year until the property changes ownership or is significantly improved.

When ownership changes or new construction is completed, the county reassesses the property at the current market value. That reassessment creates a gap between the old assessed value and the new one. The supplemental assessment captures the tax owed on that difference for the portion of the fiscal year that has already passed.

In short, the supplemental tax bill is the catch-up bill for the months between when your reassessment took effect and when your regular annual tax bill was issued.

The California State Board of Equalization administers the rules governing supplemental assessments statewide. Each county’s assessor handles the actual calculation.

What Triggers a Supplemental Assessment?

Two events trigger a supplemental assessment in California.

The first is a change of ownership. When you purchase a home or receive property through a transfer that qualifies as a change of ownership under California law, the county assessor reassesses the property at its current fair market value.

The second is new construction. If you build an addition, complete a major renovation, or construct a new structure on your property, the newly built portion is reassessed at its current value upon completion.

Routine maintenance and cosmetic repairs do not trigger a supplemental assessment. Neither do most transfers between spouses nor qualifying transfers between parents and children under Proposition 19 rules.

How Is the Supplemental Tax Amount Calculated?

The formula is straightforward. The county takes the difference between your new assessed value and the prior assessed value. That difference is your supplemental assessment. The supplemental tax is then calculated by applying the local tax rate (typically around 1 percent plus any voter-approved bonds and special assessments) to the supplemental assessment.

The result is then prorated based on the number of months remaining in the current fiscal year. California’s property tax fiscal year runs July 1 through June 30.

A practical example: you purchase a home in October. The county reassesses it. The difference between the old assessed value and your purchase price is $200,000. At a 1.1 percent tax rate, the annual supplemental tax would be $2,200. Because there are nine months left in the fiscal year when the reassessment takes effect, your supplemental bill would be prorated to $1,650.

If you purchased in March, there would be only four months remaining in the fiscal year. The same $200,000 assessment gap at 1.1 percent would produce a prorated supplemental bill of approximately $733.

When Will You Receive the Bill and When Is It Due?

The county assessor completes the supplemental assessment after the qualifying event. The bill is then mailed to you, typically within several months of your purchase or the completion of construction. In some cases, especially if you purchased late in the fiscal year, you may receive two supplemental bills covering portions of two different fiscal years.

Payment due dates follow the same installment structure as your regular property tax bill. The first installment is due November 1 and becomes delinquent after December 10. The second installment is due February 1 and becomes delinquent after April 10. If your bill arrives after those dates, the county will set adjusted due dates shown on the bill itself.

Late payments accrue a 10 percent penalty. After June 30, unpaid supplemental taxes become delinquent and accrue additional costs. Do not let a supplemental bill sit unopened.

Does Your Mortgage Impound Account Cover It?

This is the question that catches most new California homeowners off guard. In most cases, your mortgage servicer’s impound account does not cover supplemental tax bills. Your lender estimates your annual property tax based on prior-year figures and collects that amount monthly. The supplemental bill is separate, arrives unexpectedly, and goes directly to you.

Some lenders handle it. Most do not. Contact your mortgage servicer directly to confirm. If your impound account does not cover the supplemental bill, the payment obligation is yours, and the bill’s due date controls.

What Are Negative Supplemental Assessments?

Not every supplemental assessment results in a bill. If the new assessed value is lower than the prior assessed value, the county issues a negative supplemental assessment. This typically happens when property values have declined, and you purchased at a price below the prior assessed value.

A negative supplemental assessment produces a refund or a credit against future taxes rather than a payment obligation. If you have an impound account, your lender may receive the refund check rather than you. Contact your servicer to confirm how it is handled.

How to Challenge a Supplemental Assessment in California

If you believe the assessed value used for your supplemental bill is incorrect, you have the right to appeal. The process is handled at the county level through the Assessment Appeals Board.

The general steps are:

Step 1: Review the notice. Your supplemental assessment notice will include the assessor’s estimate of your property’s value and the effective date of the reassessment. Compare this to your purchase price and recent comparable sales in your area.

Step 2: Contact the county assessor’s office first. In many cases, a straightforward error can be corrected informally before a formal appeal is necessary. Request a review and provide documentation supporting your position, such as your purchase agreement or comparable sales data.

Step 3: File a formal appeal if needed. Each county has its own Assessment Appeals Board and its own filing deadline. Filing deadlines are strict. Missing the window means losing your right to challenge that year’s assessment. Check your county assessor’s website for the current deadline and filing instructions.

Step 4: Prepare your evidence. Comparable sales, the purchase agreement, an independent appraisal, and any evidence of property condition issues are all relevant. The burden is on you to demonstrate that the assessor’s value is incorrect.

For Los Angeles County, the LA County Assessment Appeals Board handles filings. For other counties, check your local county assessor’s website.

How the Tax Hardship Center Can Help

Supplemental property tax bills are issued by the county, not the IRS. For most people receiving a supplemental bill, the issue is straightforward: payment, proration review, or a county-level appeal.

Where the Tax Hardship Center comes in is when a California property tax issue intersects with a broader state or federal tax problem. If you owe the California Franchise Tax Board for unpaid state income tax, if an IRS lien has attached to your property, or if a supplemental assessment has compounded a tax situation that was already stretched, that is where professional representation matters.

THC works with IRS and state tax resolution, including installment agreements, offer-in-compromise cases, and back-tax situations for California residents. If you are dealing with more than a supplemental bill, including FTB debt or federal tax enforcement, a free case review will tell you where you actually stand.

Get a free case review at Tax Hardship Center.

FAQ

What is the supplemental property tax rate in California?

The base rate starts at 1 percent of your assessed value under Proposition 13. Your actual rate will be slightly higher once local bonds, Mello-Roos, and other district taxes are included, so it varies by location.

How often do you pay supplemental property tax in California?

It is a one-time payment tied to a specific event, not something you pay every year. Once paid, your regular property tax bill simply continues at the updated assessed value.

Do first-time homebuyers always get a supplemental tax bill in California?

In most cases, yes. Any purchase that triggers reassessment results in a prorated supplemental bill, except for specific exempt transfers, such as parent-to-child or spouse-to-spouse transfers.

What happens if I cannot pay my supplemental property tax bill?

A 10 percent penalty is added after the due date, and costs increase further after June 30. If left unpaid, it can lead to a tax lien, so it is best to contact the county early and explore payment options.

Can I appeal a supplemental assessment if I think it is too high?

Yes, you can appeal through your county’s Assessment Appeals Board. The timeline is usually around 60 days, so reviewing your notice and acting quickly matters.

Will my lender pay my supplemental tax bill from my escrow account?

Usually not, since lenders do not account for this unpredictable amount. The bill comes directly to you, so it is safer to plan for it as an out-of-pocket payment.

Conclusion

California supplemental property tax is not a surprise fee or a billing error. It is the mechanism California uses to collect the prorated tax owed between the date of your reassessment and the next regular annual tax cycle. Every California homebuyer who purchases at a price above the prior assessed value will receive one.

The amount is calculated by applying your local tax rate to the difference between the old and new assessed values, then prorating it for the months remaining in the fiscal year. Your impound account almost certainly does not cover it. The payment due date is printed on the bill, and late penalties apply quickly.

If the assessed value looks wrong, you can appeal it. The process is handled at the county level, and the deadlines are strict.

For most homeowners, the supplemental bill is a one-time adjustment with a clear payment path. If your property tax situation has become part of a larger state or federal tax problem,Tax Hardship Center provides free case reviews for California residents dealing with IRS or FTB debt.

Key Takeaways

- Supplemental property tax in California is a separate, one-time bill, not a mistake or duplicate

- It is triggered by a change of ownership or new construction

- The tax covers the gap between the old assessed value and the new market value

- The amount is calculated using the value difference × local tax rate, then prorated for the remaining months in the fiscal year

- California’s property tax fiscal year runs from July 1 to June 30

- You may receive the bill months after purchase, sometimes even two bills for different fiscal periods

- Mortgage escrow (impound) accounts usually do NOT cover supplemental tax bills

- Late payments incur a 10% penalty and additional costs after June 30

- If the reassessed value is lower, you may receive a negative supplemental assessment (refund or credit)

- You have the right to challenge the assessment through the county Assessment Appeals Board

- Appeal deadlines are strict and typically around 60 days from notice

- Most California homebuyers receive this bill because reassessment is mandatory under Proposition 13 rules

- It is essentially a “catch-up tax” for the time between reassessment and regular tax billing

- The bill can feel unexpected, but it is a standard part of California’s property tax system