Getting an IRS notice is stressful, but getting the third one can feel like the floor drops out.

If you are staring at CP501, CP503, and CP504 and wondering, “How close am I to a levy?”, you are asking the right question. These letters are part of the IRS collection ramp-up, and the smartest move is responding early, when you still have the most options.

CP501 Vs CP503 Vs CP504: What Each Notice Means

These three notices usually show up after the IRS has already billed you for a balance due. The language becomes sharper as you move from a reminder to an enforcement warning.

IRS CP501 Notice: First Reminder

CP501 is a reminder that you have an outstanding balance on a tax account. It tells you how much you owe, when payment is due, and how to pay or set up a plan.

What to do at the CP501 stage

- Confirm the tax year and amount match your records.

- If you can pay, pay by the due date.

- If you cannot pay in full, look at payment plan options early.

CP503 Second Reminder: More Urgent, Same Core Message

CP503 is the IRS’s second reminder that you still have an unpaid balance, and they have not heard from you. It repeats payment and payment-plan paths, but the urgency increases.

What to do at the CP503 stage

- Treat it as a countdown, not a repeat letter.

- If cash is tight, pay what you can now and move quickly toward an agreement.

- If the balance is wrong, call using the number on the notice and be ready with proof.

CP504 Final Notice: Intent To Levy Warning

CP504 is where things change. The IRS describes CP504 as a Notice of Intent to Levy under Internal Revenue Code section 6331(d). It is the final reminder in this series and warns that the IRS intends to levy if the balance remains unpaid.

CP504 also warns that the IRS may file a Notice of Federal Tax Lien (if they have not already), and that it may include passport-related consequences for “seriously delinquent tax debt” under the FAST Act rules referenced in the notice.

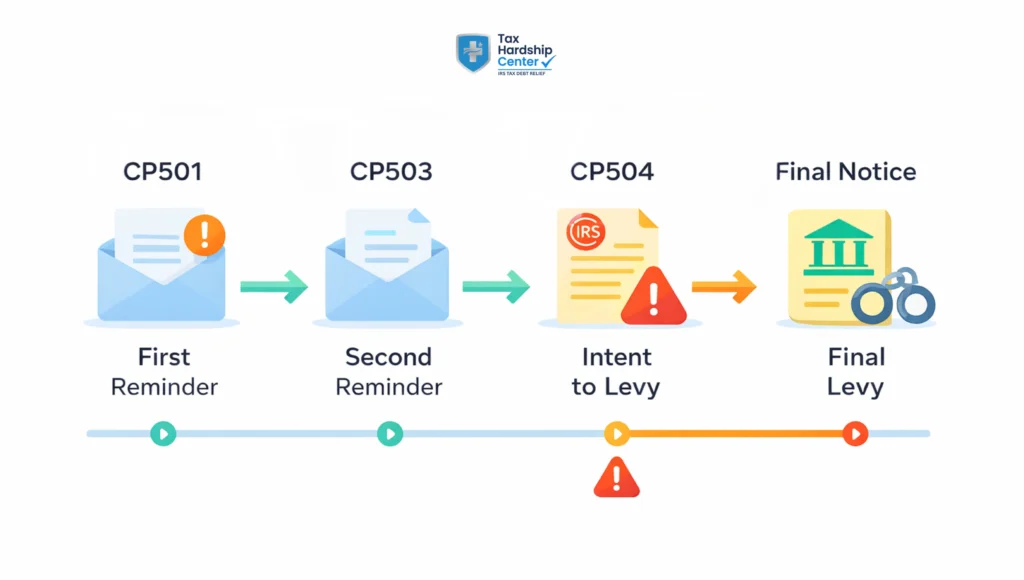

The IRS Notice Timeline Before A Levy

The IRS does not usually go from “first reminder” to “levy tomorrow.” Most cases move through stages.

A helpful high-level rule is this: if the initial bill remains unpaid, the IRS generally sends CP501, CP503, and CP504 over time, each one escalating the pressure.

CP501, CP503, CP504 At A Glance

| Notice | What It Means | What The IRS Is Pushing You To Do | Risk If Ignored |

| CP501 | Balance due reminder | Pay in full or set up a plan | Lien risk increases if you do nothing |

| CP503 | Second reminder, no response received | Pay or set up a plan fast | Lien risk continues, escalation likely |

| CP504 | Notice of Intent to Levy (final reminder in this series) | Pay immediately or arrange a resolution | Levy risk increases, state refund levy risk, asset search, lien risk |

How Many Days Do You Have After CP504?

A standard CP504 notice states that the IRS may levy if they do not receive payment or arrangements within 30 days of the notice date. Always use the due date on your specific letter.

CP504 And Levy Risk: What Happens Next

This is the part most articles blur, so let’s make it simple.

CP504 Is Serious, But It Is Not Always The Last Step Before A Wage Or Bank Levy

The IRS explains that, before most levies, they must send a Final Notice of Intent to Levy and Notice of Your Right to a Hearing at least 30 days before the levy.

That “final notice” is often LT11 or Letter 1058 (or similar notices like CP90), and it is where your Collection Due Process rights matter most.

CP504 can also mention the state tax refund levy timing and note that, in most other situations, the IRS will send a notice giving you the opportunity to request a Collection Due Process hearing before levying on other property, unless they have already issued one.

CP504 Can Still Lead To Real Consequences

Even before a wage levy hits, CP504 can signal:

- Increased likelihood of a federal tax lien filing.

- A push toward enforced collection if you do not respond.

- Escalation into final levy notices (LT11/1058), which can lead to wage or bank levies if ignored.

Best Fixes By Situation: Pay, Plan, Settle, Or Pause

Commercial intent means you likely want the fastest path to make the problem go away with the least damage. Here are the options that usually work, depending on your situation.

If You Can Pay In Full

Paying in full stops additional interest and penalties from accruing on the unpaid balance. The IRS payment hub lists multiple ways to pay, including online.

If You Can Pay Monthly: Set Up A Payment Plan

The IRS Online Payment Agreement tool lets many taxpayers apply for a payment plan online and get immediate approval if they qualify.

If You Cannot Pay, and It Would Create Hardship: Consider A Collection Pause

If paying anything right now would prevent you from covering basic living expenses, a hardship-based option like Currently Not Collectible status may pause active collection in many cases.

If The Debt Is Large And Paying In Full Is Unrealistic: Explore Settlement

An Offer in Compromise can allow settlement for less than the full balance in qualifying situations. It is not “automatic,” and the IRS evaluates your ability to pay based on income, expenses, and assets.

If You Disagree With The Balance Or The IRS Is Moving Too Fast: Know Your Appeal Paths

CP501, CP503, and CP504 pages reference requesting an appeal under the Collection Appeals Program (CAP) before collection action takes place, based on the instructions in your notice.

CDP is different. The IRS CDP FAQs explain that the IRS must issue a formal Notice of Intent to Levy and Your Right to a Hearing before levy action, and a CDP hearing is where you can propose alternatives to enforced collection (and sometimes dispute the amount if you have not had a prior opportunity).

When To Get Help Before A Levy

If you are at CP501, you often still have time to handle it yourself.

If you are at CP503 or CP504, it is smart to get help when any of these are true:

- You cannot pay in full, and you are not sure which option actually fits.

- You have multiple years involved, missing returns, or a lien risk.

- You are close to receiving final levy notices, such as LT11 or Letter 1058, and you want to protect wages or bank accounts.

If you are already dealing with enforced collection concerns, the Tax Hardship Center may help:

How Tax Hardship Center Can Help

The goal at CP501, CP503, or CP504 is to stop escalation and lock in a resolution that you can actually maintain.

Tax Hardship Center typically helps by:

- Reviewing the notice history, tax years, and enforcement risk.

- Matching you to the right path, installment agreement, CNC, or OIC, based on the actual numbers.

- Helping you act fast if you are near Levy territory, where response windows and appeal options tighten.

FAQs

Is CP504 The Final Notice Before A Levy?

CP504 is a Notice of Intent to Levy, and it is serious. For many wage and bank levies, the IRS generally must also send a Final Notice of Intent to Levy and Notice of Your Right to a Hearing (often LT11/Letter 1058 or similar) at least 30 days before levying.

What Is The Difference Between CP501 And CP503?

CP501 is a reminder that you have an outstanding balance. CP503 is the second reminder, sent when the IRS still has not received a response from you. Both emphasize paying or setting up a payment plan.

What Should I Do If I Cannot Pay The Amount On CP503 Or CP504?

Start by paying what you can, then move quickly into a formal arrangement. The IRS outlines payment plans and the online payment agreement tool as a primary option for many taxpayers.

If paying anything would cause hardship, options such as Currently Not Collectible status may apply.

How Fast Do CP501, CP503, And CP504 Come?

Timing varies by taxpayer and case, but the IRS generally sends a series of collection notices over months when a balance remains unresolved.

Can The IRS File A Lien During This Notice Series?

Yes. The IRS CP501 and CP503 pages state that the IRS may file a Notice of Federal Tax Lien if you do not pay, make arrangements, or contact the IRS. CP504 also includes lien warnings.

Can I Appeal After CP504?

CP504 references the Collection Appeals Program (CAP) as an appeal route before collection action, based on instructions in your notice. CDP rights generally apply once you receive a formal final levy notice that includes the right to a hearing.

Conclusion

CP501, CP503, and CP504 are not “random scary letters.” They are an escalation sequence.

If you respond early, you usually have more control and more affordable options. If you wait until CP504, you are moving into pre-levy territory, and the next letters could trigger wage or bank levy timelines.

Key Takeaways:

- CP501 is the first reminder to pay or set up a plan.

- CP503 is the second reminder, and ignoring it often leads to faster escalation.

- CP504 is a Notice of Intent to Levy and can lead to lien and levy activity if not addressed.

- Wage and bank levies generally require a separate final levy notice (LT11/Letter 1058 or similar) at least 30 days before levy action.

- The fastest “fix” is matching your situation to the right option: pay, payment plan, hardship pause, or settlement.