If you just found out your wages are being garnished, or you’re worried that is where this is heading, one of the first questions that hits is a practical one. Does this come out of your full paycheck, or what is left after the government already took its share?

The short answer is: after taxes. But the complete answer matters more, because the number that determines how much can actually be pulled from your paycheck is not simply your take-home pay. It is a specific legal figure called disposable earnings. And understanding what that number is, and how it gets calculated, is the difference between knowing your rights and finding out the hard way what you had left to lose.

This article breaks down exactly how wage garnishment interacts with your taxes, what disposable earnings mean under federal law, and why IRS garnishment follows a different set of rules than a regular creditor garnishment.

Does Wage Garnishment Come Out Before or After Taxes?

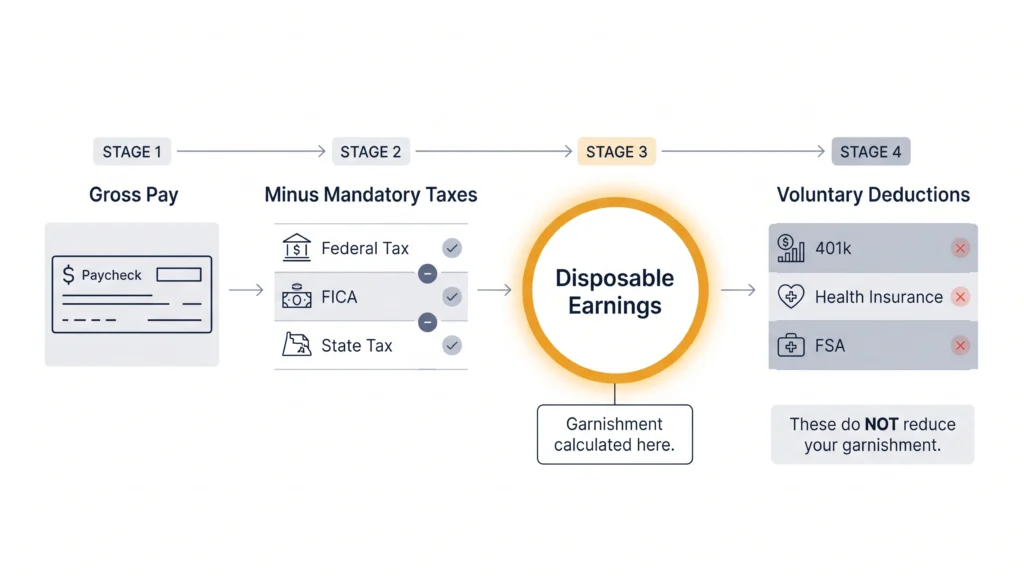

Wage garnishment is calculated after legally required tax deductions are removed from your gross pay. But it is not calculated after all your paycheck deductions. That distinction matters, and most explanations skip right over it.

Here is the actual order of deductions on a garnished paycheck:

Step 1: Start with your gross wages (total pay before any deductions).

Step 2: Subtract legally required deductions: federal income tax, Social Security, Medicare, state income tax, and any state-mandated contributions that apply to you.

Step 3: What remains after Step 2 is your disposable earnings. This is the number used to calculate how much can be garnished.

Step 4: Voluntary pre-tax deductions (your 401k contribution, health insurance premium, dental coverage, FSA contributions) come out next. But these do not reduce your disposable earnings for garnishment purposes. They are invisible to the garnishment calculation.

Step 5: The garnishment amount is taken from your disposable earnings figure.

Step 6: Whatever survives all of that is your actual take-home pay.

So when someone asks whether garnishment is pre-tax or post-tax, the precise answer is this: it is calculated on the amount remaining after mandatory taxes are removed, but it is not reduced by voluntary benefits elections.

What Are Disposable Earnings?

Disposable earnings are a legal term, not a casual one. It has a specific definition under Title III of the Consumer Credit Protection Act, the federal law that governs wage garnishment limits nationwide.

The law defines disposable earnings as the amount of pay that remains after deductions required by law. Required by law means taxes, Social Security, Medicare, and any state-mandated contributions. It does not mean everything that comes out of your check before you see it.

This number is what your employer uses when they receive a garnishment order. The creditor, the court, or the IRS does not calculate a percentage of your gross wages. They calculate a percentage of your disposable earnings or apply a flat exemption formula depending on the type of garnishment.

What Counts Toward Disposable Earnings and What Does Not

This is the section most people need, yet almost nobody explains it clearly.

Deductions that DO reduce your disposable earnings (required by law):

- Federal income tax withholding

- Social Security tax (6.2% of gross wages)

- Medicare tax (1.45% of gross wages)

- State income tax

- State disability insurance in states that mandate it

- Mandatory pension contributions required by law for certain public employees

Deductions that do NOT reduce your disposable earnings:

- 401(k) or 403(b) contributions

- Health insurance premiums

- Dental and vision coverage

- Life insurance premiums

- Flexible spending account contributions

- Union dues

- Voluntary wage assignments

- Charitable payroll deductions

Here is why that second list matters. If you are contributing $400 a month to your health plan and $300 to your 401(k), those deductions do not shrink the garnishment calculation. The creditor or the IRS still runs their numbers against the full disposable earnings figure before any of your voluntary deductions are taken out.

Many people assume their take-home pay is the starting point for garnishment. It is not. The starting point is the amount between mandatory taxes and voluntary benefits, and that number is usually higher than what you see in your bank account each pay period.

How Much Can Be Garnished From Your Paycheck?

Federal law puts a ceiling on how much of your disposable earnings can be garnished, regardless of what the court order says. For most creditor garnishments (credit card debt, medical bills, personal loans), the limit is the smaller of these two figures:

- 25% of your disposable earnings for that pay period, or

- The amount by which your disposable earnings exceed 30 times the federal minimum wage (currently $7.25/hour, so 30 x $7.25 = $217.50 per week)

Here is what that looks like with actual numbers.

If your weekly disposable earnings are $600:

- 25% of $600 = $150

- $600 minus $217.50 = $382.50

- The garnishment is capped at the smaller number: $150

If your weekly disposable earnings are $250:

- 25% of $250 = $62.50

- $250 minus $217.50 = $32.50

- The garnishment is capped at the smaller number: $32.50

If your disposable earnings are at or below $217.50 per week, nothing can be garnished under federal law.

Several states set stricter limits than the federal floor. Some cap garnishments are lower than 25%. A few provide additional protections depending on the type of debt. To run the numbers for your own paycheck and state, use the wage garnishment calculator at Tax Hardship Center.

Child support and alimony orders are subject to a different set of caps. Those can go up to 50% to 65% of disposable earnings, depending on whether you are supporting another family and how far behind you are on payments.

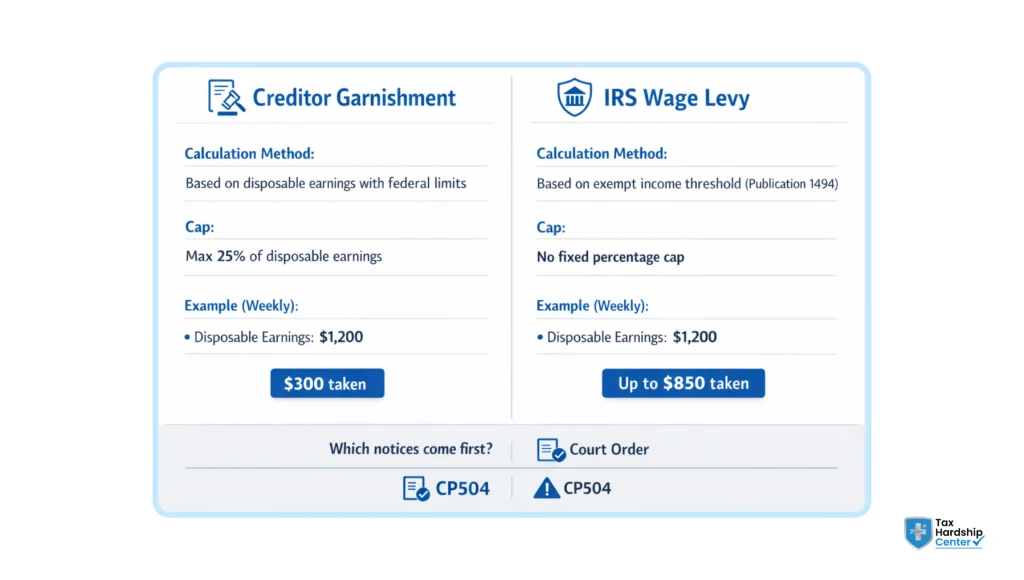

IRS Wage Levy vs. Regular Creditor Garnishment: Two Different Calculations

This is the section most articles fail to explain, and it is the one that matters most if the garnishment you are dealing with is from the IRS.

A regular creditor garnishment follows the rules described above. The 25% cap applies. The minimum wage floor applies. Federal and state protections hold.

An IRS wage levy does not work that way.

When the IRS levies your wages, it does not use a percentage cap. Instead, it calculates a specific exempt amount based on your filing status and the number of dependents you are claiming. That exempt amount comes directly from IRS Publication 1494, which is updated each year.

Here is how it works in practice. The IRS gives your employer a table showing how much of your pay you are allowed to keep per pay period. Everything above that protected amount goes to the IRS. There is no 25% ceiling.

For illustration: if your weekly disposable earnings are $1,200 and your exempt amount under Publication 1494 is $350, the IRS can take $850 per week from your paycheck. Every week. Until the balance is resolved.

A creditor working with the same $1,200 in disposable earnings could only take $300 (25%). The IRS can take more than double that.

This is why an IRS wage levy escalates the urgency of the situation in a way that a standard creditor garnishment does not. If you have received a CP504 notice, that is the IRS’s final warning before enforcement action. That notice arrives before the levy starts, and that window is real and worth acting on.

How Garnishment Affects Your Tax Return

Wage garnishment does not reduce your taxable income. It is not a deduction. It does not produce a credit at year-end.

Your employer still reports your full gross wages on your W-2, and you are still taxed on the full amount of what you earned, regardless of how much of each paycheck the garnishment took. The reduction in your take-home pay is not recovered through your tax refund.

One scenario worth understanding separately: if your tax refund itself is being seized by the IRS, that is a different mechanism called a tax refund offset. Both a refund offset and a wage levy can happen at the same time if you have an unresolved IRS balance. They are separate processes, triggered separately, and they run concurrently.

For child support and alimony garnishments specifically, there may be tax implications on the side of the person receiving those payments, but the garnishment deduction itself is not tax-deductible for the person paying it under current law.

What Happens to Your Garnishment When Your Income Changes

The garnishment amount is not permanently fixed. It is recalculated each pay period based on your current disposable earnings. A few situations that change the math:

Your income increases. If you get a raise or work overtime, your disposable earnings go up. For a percentage-based creditor garnishment, the garnishment amount increases proportionally. For an IRS levy, more of your paycheck exceeds the exempt amount, so the IRS takes more of it.

Your income drops. If your hours are cut or you move to a lower-paying role, your disposable earnings shrink. If they fall below the $217.50 weekly federal floor, a creditor garnishment stops until income rises above that level again.

You take a second job. A creditor with an existing garnishment order against your primary employer generally cannot automatically garnish your second employer’s wages. They would need a separate court order against the second employer. The IRS operates differently, as a federal levy can attach to wages paid by multiple employers.

You have more dependents. For IRS levies specifically, the exempt amount from Publication 1494 increases with each qualifying dependent. If your family situation changes after a levy begins, you can submit an updated exemption form to the IRS to increase the amount of your paycheck that is protected.

How to Stop a Wage Garnishment Before It Goes Further

Once a wage levy is active, stopping it requires either resolving the underlying debt or getting into an arrangement that the IRS or creditor will accept as an alternative. For IRS levies specifically, the IRS will release the levy when:

- The full balance is paid

- You enter into an accepted IRS installment agreement or other resolution arrangement

- The IRS places your account in Currently Not Collectible status

- An Offer in Compromise is submitted and accepted

- The 10-year statutory collection window expires

The IRS is required to give you a 30-day notice before implementing a levy. That means the final notice is not the same as the levy in motion. There is a gap, and most of the options live there.

A tax resolution professional can contact the IRS directly during that window, request a hold on enforcement, and begin establishing a resolution arrangement that stops the levy process before your employer ever receives documentation. If the levy has already started, a professional can still request a release, though the process becomes more time-sensitive.

The IRS responds differently when a representative is involved. They have established procedures for levy release, and a professional who handles these cases regularly knows how to navigate them more quickly than someone navigating them alone.

How the Tax Hardship Center Can Help You Stop a Wage Garnishment

If your wages are being garnished or you have received IRS notices warning of an impending levy, Tax Hardship Center specializes in this situation.

Their team of licensed tax professionals works directly with the IRS on your behalf to request levy holds, establish resolution arrangements, and protect as much of your paycheck as the law allows. Services include:

IRS Wage Levy Release: Contact the IRS to request an immediate hold on garnishment while a resolution is negotiated.

Installment Agreements: Setting up a structured installment agreement that the IRS accepts, which triggers a levy release.

Offer in Compromise: Negotiating to settle your tax debt for less than the full amount owed, where eligible.

Currently Not Collectible Status: If your financial situation qualifies, the IRS can pause all collection activity, including wage levies.

CP504 and Final Notice Response: If you have received a final IRS warning notice, the Tax Hardship Center can act within that 30-day window before the levy reaches your employer.

The earlier you act, the more options you have. Tax Hardship Center offers a free case review so you can understand exactly where you stand and what can be done before more of your paycheck disappears.

FAQs

Do garnishments come out pre-tax or post-tax?

Post-tax. Always. Your legally required taxes come out first. Federal income tax, Social Security, Medicare, and state tax. What’s left after that is called disposable earnings. That is the number on which the garnishment is based.

Your 401(k), health insurance, or other voluntary deductions do not reduce this amount. They do not protect you from garnishment.

Are wage garnishments based on gross or net income?

Neither. And this is where most people get it wrong. Garnishments are based on disposable earnings. Not your full gross salary. Not your final take-home after everything.

It sits in between. After mandatory taxes, before optional deductions.

How does wage garnishment affect my tax return?

It does not help you. Your W-2 still reports your full gross income. The IRS does not adjust for what was taken through garnishment. There is no deduction. No credit. No refund benefit. You simply had less money in your pocket during the year.

Can the IRS garnish more than 25% of my paycheck?

Yes. And they often do. That 25% limit applies to regular creditors, not the IRS. The IRS uses an exempt amount based on your filing status and the number of dependents from Publication 1494. Everything above that amount can be taken. For higher earners, this often means a much larger portion of the paycheck.

Do garnishments reduce taxable income?

No. Garnishments are not tax-deductible. Child support taken through garnishment also does not reduce taxable income under current federal law. Your income is taxed as if you received the full amount.

What is the minimum wage protection for garnishment?

There is a floor, but it is limited.

Under federal law, if your weekly disposable earnings are $217.50 or less, standard creditors cannot garnish anything. This is based on 30 times the federal minimum wage. Some states provide higher protection. The IRS uses a different system based on its own exemption table rather than the minimum wage rule.

Can I stop garnishment without paying the full balance?

Yes. For IRS levies, options include:

Installment agreement

Offer in Compromise

Currently Not Collectible status

These can lead to a levy release without full payment up front. For creditor garnishments, negotiating a payment plan directly or through the court can also stop or pause the garnishment. Acting early gives you more control.

Conclusion

If you are already seeing money come out of your paycheck or have received IRS notices, waiting will only make it worse.

Get clarity before more is taken.

Talk to a tax specialist at Tax Hardship Center. We will review your notices, explain exactly what is happening, and walk you through realistic options for your situation.

Request your free case review.

Key Takeaways:

- Wage garnishment is calculated after mandatory taxes (federal income tax, Social Security, Medicare, state tax) are removed from your gross pay. It is not calculated after voluntary deductions, such as health insurance or 401(k) contributions.

- The legal term used to determine your garnishment is “disposable earnings.” This sits between mandatory tax deductions and voluntary benefits elections on your paycheck.

- For most creditor garnishments, federal law caps the amount at 25% of disposable earnings or the amount above 30 times the federal minimum wage, whichever is smaller.

- IRS wage levies do not follow the 25% cap. The IRS uses an exempt amount table based on your filing status and the number of dependents. Everything above that protected amount can be taken each pay period, often well above 25%.

- Garnishment does not reduce your taxable income. You are still taxed on your full gross wages, and the garnishment amount is not recovered through your tax return.

- The garnishment amount adjusts each pay period as your income changes. Falling below the federal minimum wage floor stops a creditor garnishment. For IRS levies, adding dependents increases your protected exempt amount.

- The IRS must give 30 days’ notice before implementing a wage levy. That’s the window where your options are. Once a resolution arrangement is accepted, the IRS must release the levy.