If your paycheck suddenly shrinks and your employer says, “The IRS is taking it,” you’re probably asking one thing first.

How much can the IRS garnish from my paycheck?

The honest answer is, it can feel like a lot. The IRS wage levy system is designed to leave you a specific exempt amount and send the rest to the IRS each pay period until the levy is released or the debt is resolved.

IRS Wage Garnishment vs IRS Wage Levy

Most people call it a “garnishment,” but the IRS generally calls it a “wage levy.”

When the IRS levies your wages, part of your wages may be sent to the IRS each pay period until you make other arrangements, the balance is paid, or the levy is released.

The IRS also explains that a wage levy is continuous, meaning it keeps attaching to wages until it’s released.

How Much Can The IRS Garnish From Your Paycheck

Unlike many creditor garnishments that take a set percentage, the IRS wage levy works like this:

- Your employer calculates your take-home pay for the pay period.

- Your employer subtracts an “amount exempt from levy.”

- The remaining amount is sent to the IRS each pay period.

That exempt amount is based on the standard deduction and an “amount determined” that is calculated in part using the number of dependents you’re allowed for the year the levy is served. The IRS mails Publication 1494 with the levy to show employers how to compute the exempt amount.

The Exemption Table Explained (Publication 1494)

Publication 1494 is the table your employer uses to determine how much of your take-home pay must be left to you.

Here’s how to read it in plain English.

The Four Inputs That Drive Your Exempt Amount

- Pay Period

Weekly, biweekly, semimonthly, monthly, or daily. - Filing Status

Single, married filing jointly, head of household, married filing separately, etc. - Dependents Claimed

The statement you return to your employer lists how many dependents can be used for levy exemption purposes. - Additional Standard Deduction

Publication 1494 includes additional exempt amounts for taxpayers who are at least 65 and/or blind, depending on what’s entered in the additional standard deduction space on the levy statement.

Real Examples From The IRS Exemption Table (2026)

Publication 1494 includes examples that show how exemptions change:

| Example | Pay Frequency And Filing | Exempt Amount Example |

| Single, weekly, 3 dependents | Weekly, single, 3 dependents | $615.38 exempt |

| Same taxpayer with additional standard deduction | Weekly, single, 3 dependents, addl standard deduction entered | $654.80 exempt |

| Married filing jointly, biweekly, 2 dependents | Biweekly, MFJ, 2 dependents | $1,646.16 exempt |

These are examples; your actual exempt amount depends on your pay period, filing status, dependents, and whether the additional standard deduction applies.

Situations That Change Your Levy Amount

If You Don’t Return The Statement Within 3 Days

Your employer will give you a Statement of Dependents and Filing Status. You must return it within three days.

If you don’t, the IRS treats your exempt amount as if you’re married filing separately with no dependents, which is usually the least favorable result.

If You Have More Than One Job Or Other Income

The IRS notes that if you have other income sources, it may allocate the exemptions to another income source and levy 100% of the income from a particular employer.

If You Get A Separate Bonus Check

The IRS wage levy guidance is blunt: if your bonus is paid separately from your paycheck, the IRS will receive the entire bonus because the exempt amount is based on the pay period, not “per payment.”

If The Levy Rolls Into A New Calendar Year

If the wage levy continues from one calendar year to the next, the IRS says you may submit a new Statement of Dependents and Filing Status and ask your employer to recompute the exempt amount.

Your Employer Usually Has A Short Buffer Before Withholding Starts

The IRS notes employers generally have at least one full pay period after receiving the wage levy before they’re required to send funds from the employee’s wages.

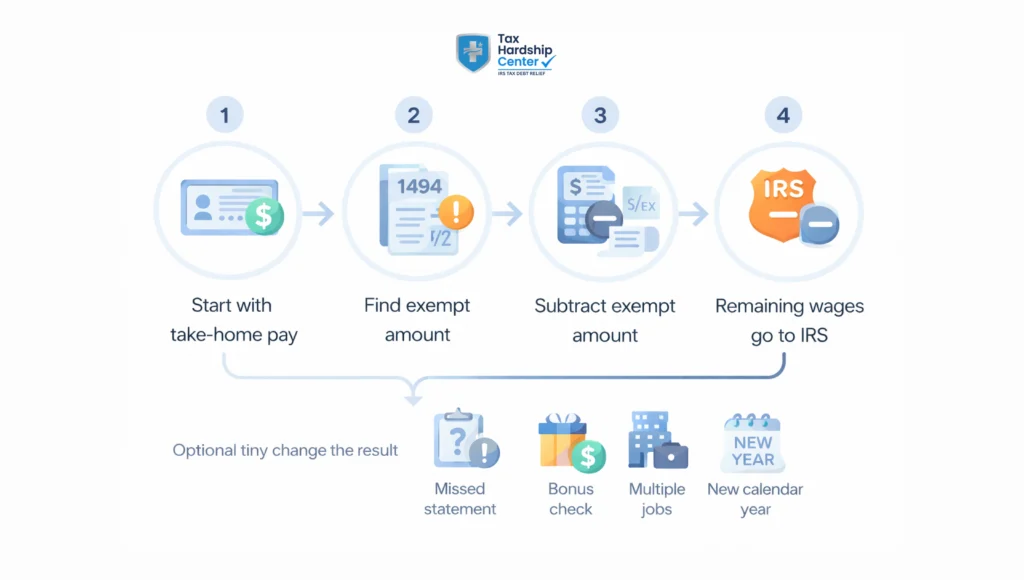

How To Estimate Your Next Paycheck Levy

You can usually get a reasonable estimate in a few minutes.

- Find Your Take-Home Pay

Use your pay stub’s net pay as a starting point (the amount remaining after normal payroll withholdings). - Identify Your Inputs

Pay period, filing status, dependents, and whether the additional standard deduction applies. - Look Up Your Exempt Amount

Use Publication 1494 for the year the levy was served. - Subtract Exempt Amount From Take-Home Pay

What remains is the portion that can be sent to the IRS.

Example using an IRS example exempt amount:

If your weekly take-home pay is $1,200 and your exempt amount is $615.38, the levy could take about $584.62 for that pay period.

How To Stop Or Reduce An IRS Wage Levy Fast

A wage levy usually doesn’t stop on its own. It stops when the IRS releases it, the debt is paid, or a new arrangement is accepted.

Step 1: Confirm You Received The Required Final Notice

The IRS collection process generally includes a Final Notice of Intent to Levy and Notice of Your Right to a Hearing at least 30 days before seizure, with some exceptions.

If you’re still within your 30-day window, a Collection Due Process hearing request (Form 12153) can be a major protection.

Internal help: https://www.taxhardshipcenter.com/blog/form-12153-cdp-hearing-request-step-by-step/

Step 2: Ask For A Levy Release If You Qualify

The IRS says it can release a levy for reasons that include paying what you owe, entering a payment plan that doesn’t allow the levy to continue, or economic hardship that prevents meeting basic, reasonable living expenses.

If a wage levy is causing immediate economic hardship, the IRS says it must be released.

Step 3: Move Into A Payment Plan When That’s The Best Fit

If you can pay monthly, getting into a formal plan is often the quickest way to stop escalation. The IRS offers online options for applying for a payment plan.

Step 4: If Monthly Payments Aren’t Realistic, Use The Right Alternative

If the levy is crushing your ability to cover basics, your plan may need to be hardship-based, not “just pay something.”

When To Get Help

Consider getting professional help quickly if:

- The levy is taking most of your pay, and your exempt amount seems wrong.

- You missed the 3-day statement window, and your exemptions defaulted.

- You have multiple income sources, and it looks like the IRS is taking nearly everything from one employer.

- You’re in a final notice timeline and want to protect your hearing rights.

If you want a guided plan based on your notices, income, and levy stage.

FAQs

Is IRS Wage Garnishment Limited To 25% Like Other Garnishments?

Usually not. The IRS wage levy method is based on leaving you a specific exempt amount and sending the remainder, rather than a simple percentage cap.

How Long Does An IRS Wage Levy Last?

It generally continues each pay period until the tax is paid, other arrangements are made, the collection period ends, or the levy is released.

Can I Increase The Amount The IRS Leaves Me?

Sometimes. Completing and returning the Statement of Dependents and Filing Status within three days is critical. If a levy continues into a new calendar year, you may submit a new statement to recompute the exempt amount.

Can The IRS Take My Bonus?

Often yes. The IRS says the entire bonus may be sent to the IRS if it’s paid separately and the exempt amount has already been applied for that pay period.

Can the IRS Take 100% Of My Paycheck?

In some situations, yes. The IRS notes it may allocate exemptions to another income source and levy 100% of the income from a particular employer.

How Do I Get A Wage Levy Released Fast?

Contact the IRS immediately using the number on the levy. The IRS can release a levy for specific reasons, including when it’s causing immediate economic hardship or when you enter a payment plan that requires the levy to stop.

Conclusion

An IRS wage levy is not about taking a set percent; it’s about leaving you a fixed exempt amount and sending the rest to the IRS each pay period. The fastest way to protect your paycheck is to ensure your exempt amount is calculated correctly, act quickly if hardship is involved, and move toward the right resolution before the levy drags on for months.

Key Takeaways:

- The IRS can levy wages continuously until the debt is paid, other arrangements are made, or the levy is released.

- The IRS wage levy takes what’s above the exempt amount, and the exempt amount is based on Publication 1494 and includes pay period, filing status, and dependents.

- If you don’t return the dependents and filing status statement within three days, your exemption can default to married filing separately with zero dependents.

- If the wage levy is causing immediate economic hardship, the IRS says the levy must be released, but you still need a longer-term plan for the balance.

- Payment plans and other formal resolutions are often the quickest path to stopping ongoing wage levies.