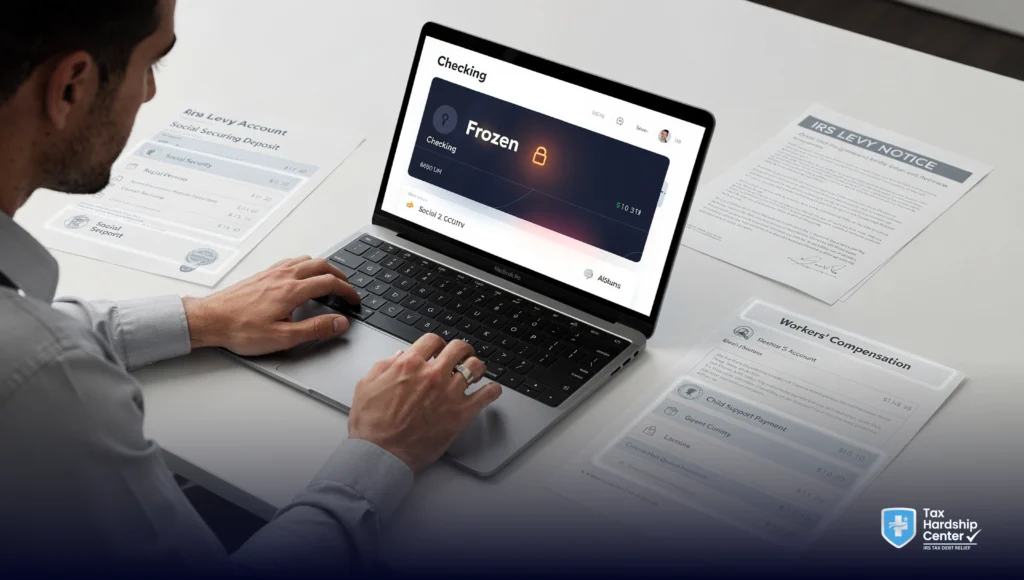

An IRS bank levy can feel like the rug gets pulled out from under you. One day your account works, the next day your funds are frozen, and bills start bouncing.

Here is the part most people do not realize until it happens: banks usually freeze first, then you get a short window to fix mistakes, prove ownership, or request a release before money is sent to the IRS. The IRS explains there is a 21-day waiting period for a bank levy, giving you time to resolve issues or notify the IRS of errors.

This guide breaks down what money is protected from an IRS bank levy, what is not, and what to do if exempt funds get caught in the freeze.

How An IRS Bank Levy Works

When the IRS levies a bank account, the bank freezes funds in the account as of the date and time it receives the levy. Normally, the levy does not affect funds you add after that moment.

The IRS also describes the 21-day waiting period: after the levy is issued, the bank holds the available funds and gives you 21 days to resolve disputes about who owns the account before sending the money (plus interest earned on that amount) to the IRS.

What Money Is Protected From An IRS Bank Levy

The IRS can levy many kinds of property, but it cannot seize certain categories of property and payments that are exempt from levy under federal law. The IRS’s own collection guidance lists examples of property it cannot seize.

Common Funds That Are Protected

The IRS collection process guidance lists these as examples of property that cannot be seized (levied):

- Unemployment benefits

- Certain annuity and pension benefits

- Certain service-connected disability payments

- Workers’ compensation

- Certain public assistance payments

- Minimum weekly exempt income

- Assistance under the Job Training Partnership Act

- Income for court-ordered child support payments

It also notes certain personal property basics that cannot be seized, such as necessary schoolbooks and clothing, undelivered mail, and limited amounts of household goods and tools of the trade.

Important legal note: Federal law controls exemptions. IRS regulations emphasize that no other property is exempt except what is specifically exempted under federal rules, and state exemption laws generally do not override federal tax levy power.

What Money Usually Is Not Protected

In practice, most “normal” bank balances are not protected just because they are needed for bills.

Here are examples of funds that are commonly reachable in a bank levy:

- Regular checking and savings balances

- Paychecks after they are deposited (this is one of the biggest surprises)

- Business revenue sitting in an operating account

- Transfers between your own accounts

- Most non-exempt investment proceeds once they land as cash in your bank account

Also, do not assume federal payments are fully protected. The IRS explains that certain federal payments may be seized under the Federal Payment Levy Program, generally up to 15%, and specifically includes Title II Social Security benefits (OASDI) as an example of payments that can be seized under that program.

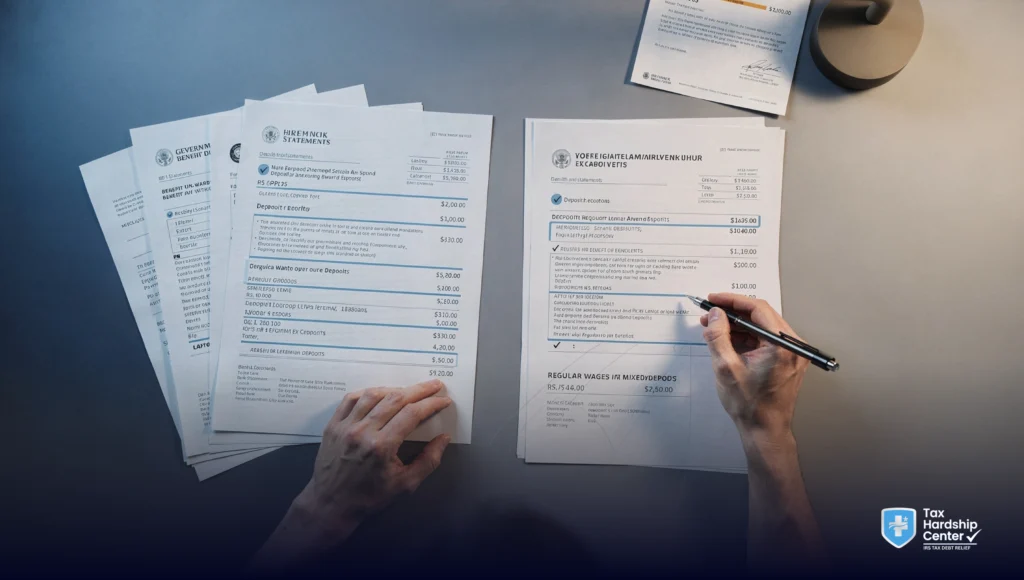

The Biggest Trap: “Exempt Income” After It Hits Your Bank

Even if a payment type is generally protected from levy, levies are messy in practice because accounts usually contain mixed funds.

Two key realities:

Banks Freeze First

For a bank levy, the bank freezes any available funds up to the levy amount, then holds them for 21 days while ownership disputes are addressed.

If exempt funds are mixed with non-exempt deposits, you may need to provide clear documentation of the funds and their source to request a release.

The IRS even gives an example involving shared ownership and proof. If you were included as a signer on an elderly parent’s bank account and the IRS levied the account for your tax debt, the IRS instructs the true owner (or their power of attorney) to call the IRS number shown on the levy and be prepared to substantiate ownership.

“Automatic Bank Protections” Are Often Misunderstood

Some people hear that federal benefit deposits are protected from bank garnishment. There is a specific federal rule (31 CFR Part 212) that creates procedures for banks to protect certain federal benefits from many private garnishments. However, that rule states the Part 212 procedures do not apply to garnishment orders obtained by the United States.

Bottom line: do not rely on “automatic protection” as your only plan if you are facing IRS collection activity. If a levy hits, you want proof, speed, and a clear request for relief.

How To Protect Exempt Funds Before A Levy Happens

If you are worried about an IRS bank levy, these steps help reduce damage and confusion:

Keep Exempt Deposits Separate

If you receive payments that may be exempt, keep them in a dedicated account and avoid mixing them with wages, transfers, or other deposits. The cleaner your account history is, the easier it is to prove what funds are what during the 21-day hold.

Keep Records That Prove Source

Save award letters, benefit statements, deposit confirmations, and bank statements showing the direct deposit source.

Get Ahead Of Collection With A Formal Resolution

If you owe and cannot pay in full, moving into a formal solution can prevent levies.

Tax Hardship Solutions:

What To Do During The 21-Day Hold

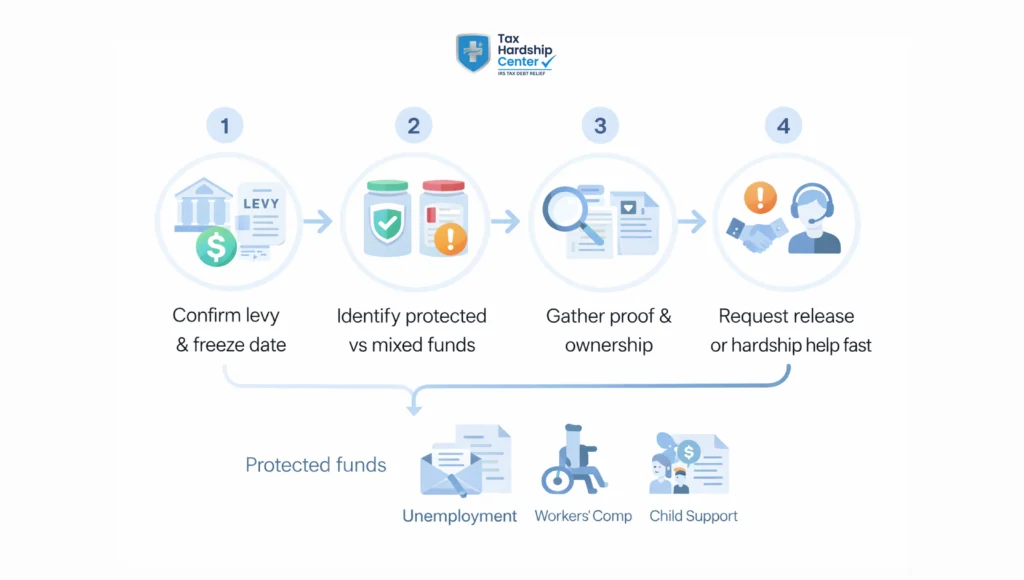

If your account is already frozen, treat this like a short deadline.

Step 1: Confirm It Is An IRS Levy And Note The Dates

The bank can confirm that the levy was received, and the “received date and time” determines which funds are frozen.

Step 2: Call The IRS Using The Number On The Levy

The IRS encourages immediate contact to resolve the liability and request a release.

Step 3: Ask For A Levy Release If You Qualify

The IRS says it can release a levy for specific reasons, including:

- You paid the amount you owe

- The collection period ended

- Releasing the levy will help you pay your taxes

- You enter a payment plan and the agreement terms do not allow the levy to continue

- The levy creates an economic hardship (prevents meeting basic, reasonable living expenses)

Step 4: If The Money Is Not Yours, Prove Ownership Fast

If the account includes funds belonging to a spouse, roommate, parent, or business partner, gather documentation showing:

- Who earned the funds

- Where deposits came from

- Why the taxpayer’s name is on the account (if it is a convenience only)

Step 5: If You Received A Final Levy Notice, Protect Your Hearing Rights

If you are at the stage where you received a Final Notice of Intent to Levy and the right to a hearing, Publication 594 explains that you can request a Collection Due Process hearing within 30 days and references Form 12153.

Frequently Asked Questions

What Funds Are Protected From An IRS Bank Levy?

The IRS collection process guidance lists examples of property it cannot seize, including unemployment benefits, certain annuity and pension benefits, certain service-connected disability payments, workers’ compensation, certain public assistance, minimum weekly exempt income, Job Training Partnership Act assistance, and income for court-ordered child support.

Will The IRS Take My Whole Bank Account?

A bank levy freezes funds available for withdrawal up to the levy amount as of the moment the bank receives the levy. Normally, funds deposited after that moment are not affected by that specific bank levy.

How Long Can My Bank Hold My Money After An IRS Levy?

The IRS explains there is a 21-day waiting period for bank levies, intended to allow time to contact the IRS, resolve disputes, or correct errors.

If My Account Contains Exempt Funds, Will The Bank Automatically Protect Them?

Not always. Banks generally freeze first, and you may need to work with the IRS during the 21-day hold to prove what funds are exempt or belong to someone else.

How Do I Get An IRS Bank Levy Released Quickly?

The IRS says to contact them immediately and request a levy release. They can release a levy for reasons including full payment, entering a payment plan (when the agreement does not allow the levy to continue), or economic hardship.

Conclusion

An IRS bank levy is fast and disruptive, but it is not always the end of the road. Some money is protected by law, but the practical challenge is proving it quickly, especially when funds are mixed in a bank account.

Key Takeaways:

- Banks typically freeze funds at receipt of the levy, then hold them for 21 days before sending money to the IRS.

- Certain payments and property categories are protected from levy, including unemployment benefits, workers’ compensation, certain public assistance, and certain disability payments.

- Many everyday bank balances are not protected, and paychecks are often reachable once deposited.

- You may be able to request a levy release for hardship or by entering a qualifying payment plan.

- If exempt or third-party funds are frozen, use the 21-day hold to gather proof and contact the IRS immediately.