It starts on a Thursday. It always starts on a Thursday.

You are looking at the business account. Payroll runs Monday. The number staring back at you is short. Not by a little. By enough that something has to give.

So you do what almost every owner in this exact spot has done before you. You pay your people. You keep the doors open. You tell yourself the withheld payroll taxes, the ones sitting in that account earmarked for the IRS, can wait one cycle. Just one.

That one cycle becomes three. Then a notice arrives. Then a second one, sharper than the first. And somewhere in the fine print is a phrase that turns a business problem into a personal one: Trust Fund Recovery Penalty.

If you are reading this because that phrase just landed in your mailbox, or because you are trying to get ahead of it before it does, this is the article that tells you exactly what you are dealing with. No scare tactics. No vague promises. Just what payroll tax debt actually is, what the IRS can do about it, and what real payroll tax debt relief looks like for an employer in your position.

What Payroll Tax Debt Actually Is (And Why It’s Not Like Other Business Debt)

Here is the part most owners do not learn until it is too late. Payroll tax debt is not really your money to begin with.

When you run payroll, you withhold federal income tax, Social Security, and Medicare from each employee’s paycheck. That money was never yours. You are holding it in trust, literally, until you deposit it with the IRS. That is why the IRS calls it a trust fund tax. And that is exactly why the agency treats unpaid payroll tax so differently from a late vendor invoice or a missed loan payment.

A landlord can wait. A supplier can be renegotiated. The IRS does not see it that way, because in its eyes, you already collected the money. You just have not handed it over.

The Moment It Gets Personal: Trust Fund Recovery Penalty Explained

This is the twist that catches most business owners off guard. Payroll tax debt does not stay a business problem. It can become yours, personally, through the Trust Fund Recovery Penalty, or TFRP.

The IRS defines TFRP as a penalty the agency can assess against anyone it decides was “responsible” for collecting and paying those taxes, and who “willfully” failed to do it. Willful does not mean malicious. It usually just means someone made a call to pay rent, payroll, or a supplier instead of the IRS. If you signed checks, approved payroll, or had authority over which bills got paid, you are a candidate.

Once the TFRP is assessed, the corporate shield that normally protects your personal assets stops working for this specific debt. The IRS can pursue your personal bank accounts, garnish your wages, and place a lien on your home, even if your business is a legitimate LLC or corporation. This is the single biggest reason payroll tax debt relief needs a different strategy than a standard IRS payment plan conversation. Understanding how payroll tax risk and personal liability connect is the first real decision point for any owner in this situation.

What Happens If You Do Nothing

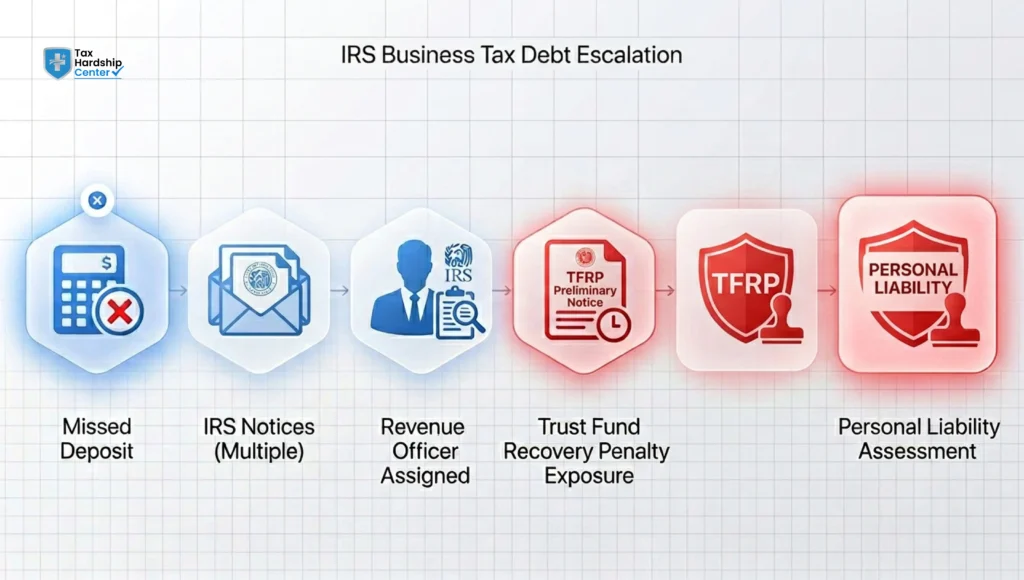

Nothing happens fast with the IRS, and that is exactly what makes this dangerous. The silence feels like room to breathe. It is not.

Behind the scenes, penalties and interest are compounding on the unpaid balance. The IRS will typically send a series of notices, and if those go unanswered, the case gets escalated to a Revenue Officer, an assigned agent whose entire job is collecting from your business specifically. That is a different level of attention than an automated notice. A Revenue Officer can request full financial disclosure, file a Notice of Federal Tax Lien, and move toward levying business or personal accounts.

Cases handled by the Taxpayer Advocate Service, the IRS’s independent watchdog office, show just how much is at stake once a TFRP is assessed and how much easier resolution is when a taxpayer engages before enforcement escalates rather than after.

The businesses that come out of this in the best shape are the ones that respond before a Revenue Officer is assigned, not after.

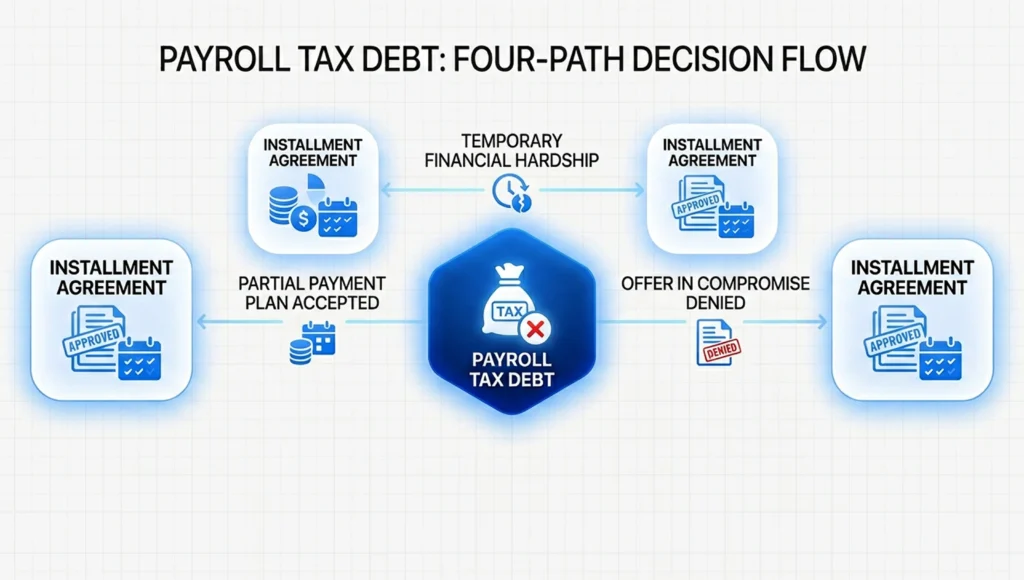

Your Real IRS Options for Payroll Tax Debt Relief

There is no single fix here. What works depends on how much you owe, how current your filings are, and whether the debt is purely business-level or already carries TFRP exposure. Broadly, employers have four paths.

Installment agreements. If your business is still operating and current on deposits, the IRS may allow you to pay the balance over time through a structured payment plan. Business installment agreements work differently from individual ones, and the terms tighten as the balance grows. Comparing installment plan options side by side before you commit matters more here than in almost any other tax debt scenario, because a missed payment can trigger faster enforcement on payroll debt.

Offer in Compromise. In select cases, the IRS will settle the debt for less than the full amount owed, but the bar is high, and payroll tax cases are scrutinized more closely than personal income tax OICs. You can review the qualification criteria for an Offer in Compromise to see whether your numbers realistically fit before you spend time building a case around it.

Penalty abatement. If there is a reasonable cause behind the missed deposits, a natural disaster, a documented cash flow disruption tied to a specific event, some penalties may be reduced or removed. This does not touch the underlying tax owed, only the penalties stacked on top.

Currently Not Collectible status. If the business genuinely cannot pay anything right now, the IRS can pause active collection. This buys time. It does not make the debt disappear, and interest keeps accruing quietly in the background.

Why This Case Is Different From an Income Tax Problem

Most owners walk into this assuming their CPA can handle it the same way they handle a late income tax bill. Usually, that assumption is wrong, and here is the honest reason why.

Payroll tax cases move faster, involve a different set of IRS collection tools, and carry personal liability that income tax debt does not. A CPA is often the right person to keep your books clean and your future filings compliant. Negotiating directly with a Revenue Officer, building a TFRP defense, or structuring a resolution that protects both the business and the owner personally is a different skill set entirely. If you are unsure where that line sits, this breakdown of what a CPA can and cannot do compared to a resolution firm lays it out plainly.

Why Employers Choose Tax Hardship Center for Payroll Tax Resolution

Payroll tax cases are not treated like consumer debt at Tax Hardship Center, and that distinction matters from the first call. The intake conversation asks about your payroll cycle, your receivables timing, and whether a Revenue Officer has already been assigned, because those details change the entire strategy. A business that used withheld taxes to survive a slow season needs a different plan than one that simply fell behind on deposits, and the case gets built around that difference instead of a generic script.

The business services team works case types most consumer-facing tax firms are not built to handle: trust fund penalty exposure, lien impact on vendor relationships and bonding capacity, and coordination with your existing accountant rather than sidelining them. Where the numbers support it, that can mean structuring an installment agreement built around your actual cash flow, pursuing penalty relief, or preparing a defense against a proposed TFRP assessment before it becomes personal.

What separates this from a generic settlement pitch is the sequencing. You get a plan for what happens to payroll and vendor relationships while the case is being worked, not just a promise that the IRS will eventually be satisfied.

FAQs

Can the IRS hold me personally responsible for my business’s payroll tax debt?

Yes. Through the Trust Fund Recovery Penalty, the IRS can assess the trust fund portion of unpaid payroll taxes against any individual it determines had control over which bills got paid, regardless of your business structure.

How long does the IRS give a business to fix unpaid payroll taxes before enforcement starts?

There is no fixed timeline. It depends on notice responses and whether a Revenue Officer is assigned. Businesses that respond early to IRS notices generally have far more resolution options than those that wait for enforcement action.

Will my business get shut down if I owe payroll taxes?

Not automatically. The IRS generally prefers a paying business over a closed one, since a closed business collects nothing further. That said, continued non-payment increases the risk of liens, levies, and asset seizure over time.

Is an Offer in Compromise realistic for payroll tax debt?

It is possible but harder to qualify for than with personal income tax debt, since the IRS scrutinizes ongoing businesses closely. Current compliance and a clear ability-to-pay picture matter more here than almost anywhere else in the process.

What is the difference between the employer’s share and the trust fund portion of payroll tax?

The trust fund portion is the income tax and employee share of FICA withheld from paychecks. The employer’s own matching FICA contribution is treated separately and is not subject to the Trust Fund Recovery Penalty.

Can I set up a payment plan for payroll tax debt while my business keeps operating?

Yes, in many cases, as long as the business stays current on new deposits going forward. Falling behind again while on a plan is one of the fastest ways to trigger a default and renewed enforcement.

Conclusion

Payroll tax debt does not resolve itself, and it rarely stays a business-only problem for long. The good news is that the IRS does have structured paths for employers who get ahead of it: payment plans, offers, abatement, and CNC status all exist for exactly this situation. The owners who protect themselves best are the ones who act before a Revenue Officer is assigned, not after.

Key Takeaways

- Payroll tax debt is trust fund money, not business cash, and the IRS treats it accordingly

- The Trust Fund Recovery Penalty can make unpaid payroll tax a personal liability, not just a business one

- Silence after an IRS notice does not buy safety, it buys time for penalties and interest to grow

- A Revenue Officer assignment signals a serious escalation in how your case is being handled

- Installment agreements, Offers in Compromise, penalty abatement, and CNC status are the four main relief paths

- Business payroll tax cases have tighter terms and faster enforcement than individual income tax debt

- A CPA keeps your books compliant, but resolving IRS collection action is a separate skill set

- Acting before enforcement escalates gives you far more control over the outcome

- Coordinating your accountant with your resolution strategy protects both the business and the owner personally

- The earlier a payroll tax problem is addressed, the more options remain on the table

Get a Free Case Review

If payroll tax debt is putting your business and your personal assets at risk, talk to a specialist before the IRS assigns a Revenue Officer to your case. Get a free case review and find out which resolution path actually fits your numbers.