Here is the short version: yes, you can get a mortgage while you owe the IRS, but the path looks different depending on whether the debt is just a balance on your account or has already become a federal tax lien.

If you are sitting on IRS debt and wondering whether to even start the mortgage process, here is what underwriters actually look for, what can stall your approval, and what to fix first.

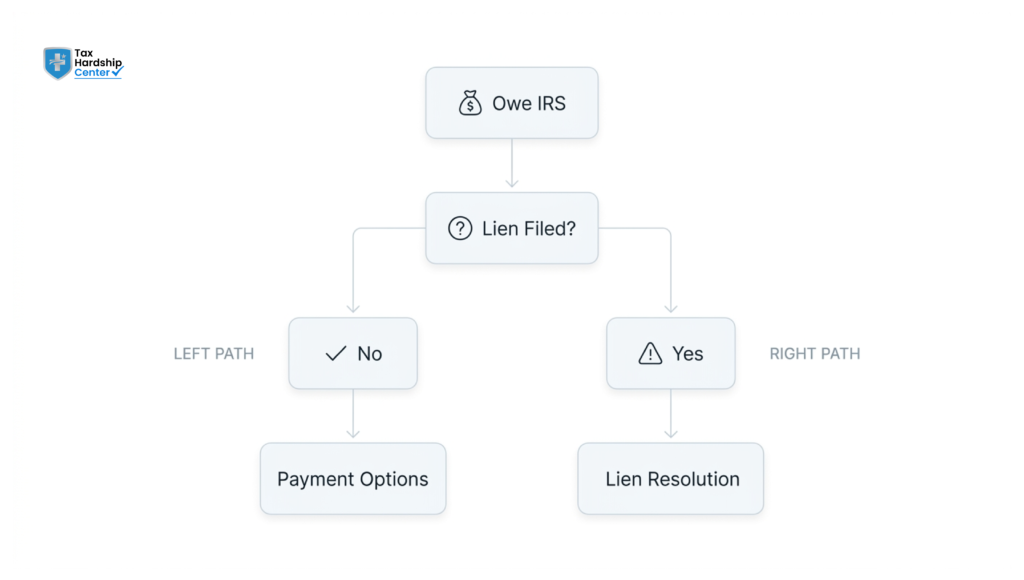

The Quick Answer: It Depends On Lien vs No Lien

If you owe the IRS but no lien has been filed, your debt generally gets treated like any other liability on your application. It affects your debt-to-income ratio, but it is not an automatic disqualifier.

If the IRS has filed a federal tax lien, that is a different situation. A lien is a public record, and most lenders will want it resolved, paid, or subordinated before they will close on your loan. The good news is that a lien does not mean game over; it just means there is a step that has to happen first.

So before anything else, the real question is not “do I owe the IRS?” It is “has a lien been filed on my account yet?” That single fact changes almost everything about your timeline.

How Underwriters Actually Find Out You Owe The IRS

Many borrowers wonder whether they can just quietly apply and hope it doesn’t come up. Here is the reality of what happens during underwriting:

Your tax returns and transcripts are often requested directly, sometimes via an IRS Form 4506-T, which provides the lender with a copy of your transcript straight from the IRS. Public records searches will surface a federal tax lien if one has been filed, since liens are recorded against you publicly. Your loan application asks about outstanding debts and obligations, and intentionally omitting this can be treated as a disclosure issue later in the process.

So the honest move is to plan around this upfront rather than hope it slips through. If you are unsure what your account actually shows right now, pulling your IRS notice history is a good place to start before you talk to anyone about a loan.

Can You Get A Mortgage On An IRS Payment Plan?

Yes, and this is honestly the most common situation we see. If you have set up a formal IRS installment agreement, most lenders will work with that, as long as a few things are true:

The agreement is documented and active, not informal or verbal. You have a track record of on-time payments, often three months or more, depending on the loan program. The monthly payment amount is something you can consistently see on your bank statements.

Once those boxes are checked, the IRS payment becomes just another monthly obligation in your debt-to-income calculation, similar to how a car loan or student loan payment is treated. It stops being a mystery liability and becomes a known, documented number.

How Each Loan Type Treats IRS Debt

Not all loan programs handle this the same way, and knowing the difference can save you a lot of frustration.

Conventional loans: Generally fine with an IRS balance and payment plan as long as it is documented. A filed lien usually needs to be addressed before closing.

FHA loans: Tend to be the most flexible here. With a documented payment plan and on-time payment history, FHA underwriters can often count the monthly payment in your debt-to-income ratio without requiring full payoff.

VA loans: Similar to FHA in flexibility, with documentation and payment history being the key factors lenders look for.

Across all three, the pattern is the same: documentation and payment history are what move you from “risk” to “manageable line item” in the eyes of an underwriter.

What Happens If You Have A Federal Tax Lien

A federal tax lien is the IRS’s legal claim against your property when a tax debt has gone unresolved for too long. If one has been filed against you, here is what it usually means for a mortgage:

Most conventional and government-backed loans will require the lien to be paid off, satisfied, or formally subordinated before closing. A lien shows up in public records searches, so it is not something that can be quietly avoided during underwriting. Subordination is sometimes possible, where the IRS agrees to let the mortgage lender take priority, but this requires a specific request and approval process; it does not happen automatically.

If you are not sure whether your account has reached lien status yet, that is worth checking before you get too far into house hunting, since catching it early gives you more options for resolving it.

Common Mistakes Borrowers Make With IRS Debt

A few patterns come up again and again with people in this exact situation:

Applying for a mortgage before setting up any payment arrangement leaves the lender with an undocumented, unresolved balance. Not telling the loan officer about the IRS debt, which usually surfaces anyway and creates delays right when you do not want them. Assuming a small balance is not worth dealing with, even modest unpaid amounts can eventually lead to a lien if left alone. Confusing an informal “I’ll pay it eventually” plan with an actual documented installment agreement, which is what lenders are really looking for.

The borrowers who move through this with the least friction are the ones who treat the IRS side as something to resolve before applying, not something to explain after the fact.

Steps To Take Before You Apply

If a mortgage is somewhere in your near future and you currently owe the IRS, here is the order that actually works:

Find out exactly where your account stands, including whether a lien has been filed. Set up a documented installment agreement if you do not already have one, since this is the single biggest lever for most borrowers. Build a few months of on-time payment history before you apply, since that history is what underwriters want to see. Be upfront with your loan officer from the start so they can structure the application around your situation rather than catch you off guard.

This does not need to take a year, but it does need to start before you are deep into the mortgage process, ideally a few months ahead.

How the Tax Hardship Center Helps You Get Loan Ready When You Owe The IRS

If you owe the IRS and a mortgage is part of your plan, the goal is simple: get your tax situation into a state that a lender can actually document and approve around, and that is exactly what Tax Hardship Center helps with. Our team reviews your account, tells you plainly whether you are dealing with a straightforward balance or something closer to lien territory, and helps map out a tax debt resolution approach that fits your timeline.

For most people in this exact situation, that means setting up a properly structured IRS payment plan from the start, so it builds the documented history a lender will actually want to see. If your account has already been escalated to a lien, our team also handles Offer in Compromise reviews and lien resolution, so it is not left as an open question when your loan file goes to underwriting.

Timing is everything here. The earlier you start, relative to when you plan to apply, the more payment history you will have built up by the time a lender looks at your file, and that history is often the single biggest factor in how smoothly your approval goes.

FAQs

Can you get a mortgage if you are on an IRS payment plan?

Yes, in most cases. Lenders generally want the agreement to be documented and active, with a few months of on-time payments, before they count it favorably in your application.

Does owing the IRS affect getting a mortgage?

It can, but mainly through your debt-to-income ratio and, if a lien has been filed, through public records that lenders will see during underwriting.

Can I get an FHA loan if I owe taxes?

Often yes. FHA lenders tend to be flexible with borrowers who have a documented IRS payment plan and a history of on-time payments.

Will an underwriter see if I owe the IRS?

Likely yes, through tax transcripts, IRS Form 4506-T requests, or public lien records. It is better for this to come from you upfront than to surface as a surprise.

What if the IRS has already filed a lien against me?

Most lenders will require the lien to be paid, satisfied, or subordinated before closing. It is not an automatic disqualifier, but it does add a step to your timeline.

How long should I wait after setting up a payment plan before applying?

Most lenders look for around three months of consistent, on-time payments, though this can vary by loan program.

Should I tell my loan officer about my IRS debt before applying?

Yes. Telling them early lets them structure your application around it, rather than dealing with it as a surprise mid-underwriting.

Conclusion

Owing the IRS does not automatically shut the door on getting a mortgage, but it does change the order of operations. Whether or not a lien has been filed is the single biggest factor, and a documented payment plan with a track record can turn an open balance into just another line item on your application. Start that process early, and IRS debt becomes a manageable part of your mortgage journey instead of the thing that derails it.

Key Takeaways

- Owing the IRS does not automatically disqualify you from getting a mortgage

- Whether a federal tax lien has been filed is the biggest factor in your timeline

- A documented IRS installment agreement can turn an open balance into a fixed monthly obligation

- FHA and VA loans tend to be more flexible with documented payment plans than some conventional programs

- Underwriters can find IRS debt through transcripts, Form 4506-T, or public lien records

- A federal tax lien usually needs to be paid, satisfied, or subordinated before closing

- Three months of on-time payments is a common benchmark lenders look for

- Telling your loan officer upfront avoids mid-process surprises

- Small unresolved balances can still escalate into liens if ignored

- Starting the resolution process early gives you more options and a smoother approval process

If you owe the IRS and want to know exactly where you stand before applying for a mortgage, get a free case review and we will help you build a plan that fits your timeline.