Somewhere in a small business right now, an owner is looking at two numbers on a screen. One is the payroll that has to go out on Friday. The other is the payroll tax deposit that was due last week. There isn’t enough for both. So a decision gets made, quietly, the kind of decision nobody writes down in the company handbook. Pay the people. Deal with the IRS later.

That decision feels small in the moment. It rarely stays small.

The Moment Everything Changes

Here’s the part most owners don’t realize until it’s already happened. The money withheld from an employee’s paycheck for federal income tax, Social Security, and Medicare was never the business’s money to begin with. Legally, the second it comes out of that paycheck, it belongs to the government. The business is just holding it. That’s why the IRS calls it a trust fund tax, and it’s why the IRS does not treat unpaid payroll taxes the way it treats a missed vendor invoice or a late lease payment.

A vendor might send a strongly worded email. The IRS sends a Revenue Officer.

What Counts as “Payroll Taxes” (And Why the IRS Treats Them Differently)

Every quarter, employers report withheld income tax and FICA taxes on Form 941, the Employer’s Quarterly Federal Tax Return. This one form is the paper trail that tells the IRS exactly what should have been deposited and when. It’s also the reason “we’ll catch up next quarter” almost never works quietly. The IRS already knows the number. It’s sitting right there on the return.

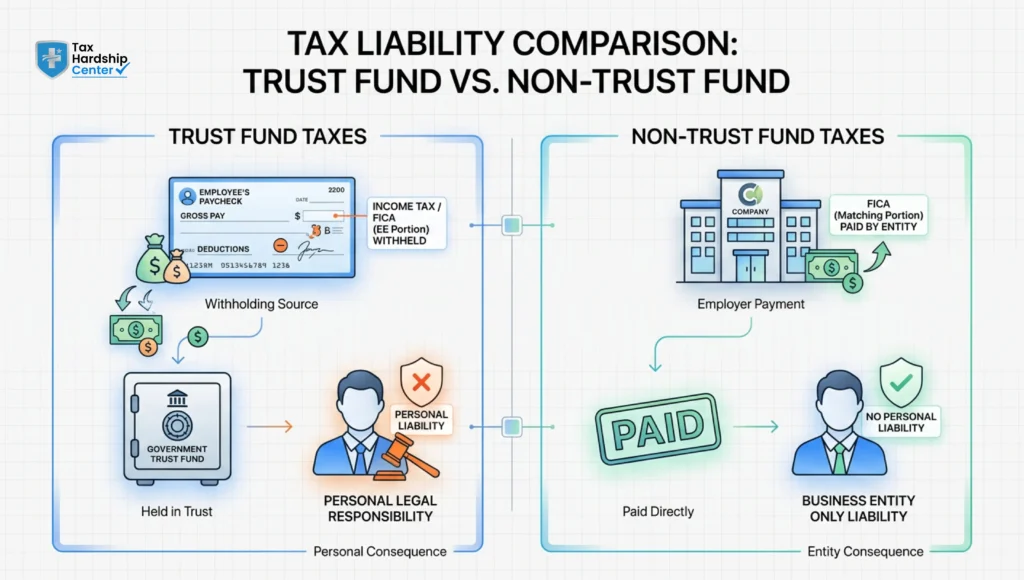

Payroll taxes are made up of two very different pots of money, and this distinction matters more than most business owners think:

- Trust fund taxes: the employee’s withheld income tax, plus the employee’s share of Social Security and Medicare. This is money that belonged to the employee, held in trust, never the employer’s to spend.

- Non-trust fund taxes: the employer’s own matching share of Social Security and Medicare, and FUTA. Still owed, still enforceable, but treated differently in how personal liability works.

That distinction is the hinge the rest of this story swings on.

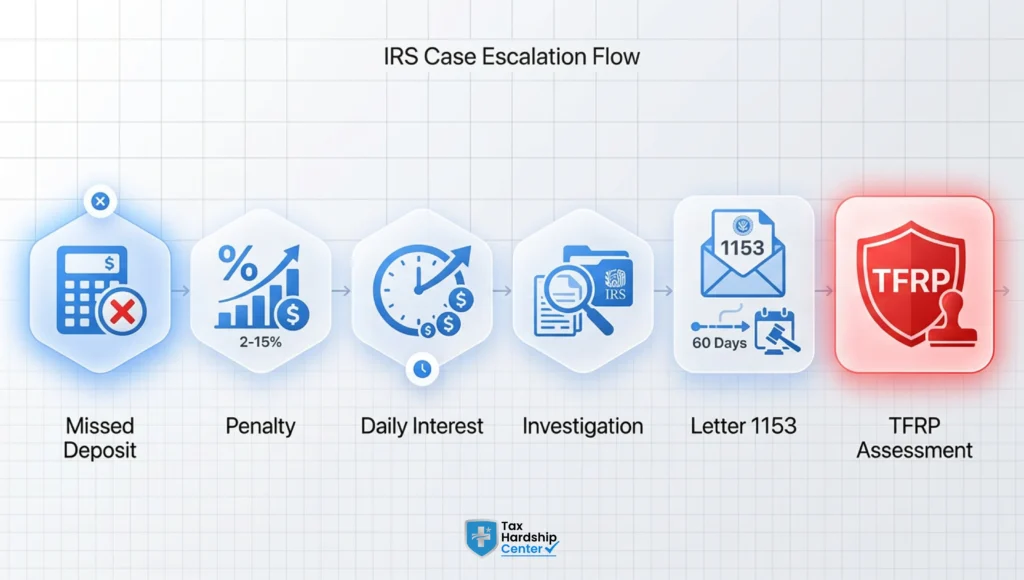

The First Wave: Failure to Deposit Penalties

The first consequence isn’t dramatic. It’s a percentage. Miss a deposit deadline and the IRS applies a Failure to Deposit Penalty, calculated on how late the deposit is:

- 2% if you’re one to five calendar days late

- 5% if you’re six to fifteen days late

- 10% if you’re more than fifteen days late

- 10% if you paid the right amount but through the wrong method

- 15% if the IRS had to send a delinquency notice before you paid

None of these percentages stack on top of each other. But they compound quietly across quarters, and businesses often don’t feel the weight of it until they see four quarters of penalties sitting on one balance.

This is the part of the story where most owners think they’re managing a cash flow problem. They’re not. Not yet. They’re managing an escalation clock, and it’s already ticking.

The Second Wave: Interest That Never Sleeps

Interest doesn’t pause for slow seasons. It doesn’t care that a big invoice is still outstanding or that a client pushed a payment thirty days. It accrues daily on the unpaid balance and on the penalties themselves, and it resets every quarter based on federal rates. The number on the notice today is never the number you’ll owe if you wait to open the next one, which is exactly how businesses end up moving further down the IRS collection process than they realized.

This is usually the point where a business owner starts checking the mail with a knot in their stomach. And that instinct, unfortunately, is correct. Because the next chapter of this story isn’t about the business anymore. It’s about the owner personally.

The Real Threat: The Trust Fund Recovery Penalty

This is the twist most business owners never see coming until it’s aimed directly at them.

The Trust Fund Recovery Penalty (TFRP) allows the IRS to collect the unpaid trust fund portion of payroll taxes directly from an individual, personally, even if that person operated entirely through an LLC or a corporation. The corporate structure that was supposed to protect personal assets doesn’t apply here. The IRS can, and does, pierce straight through it.

The penalty is equal to 100% of the unpaid trust fund taxes. Not a percentage. Not a settlement amount. The full amount, assessed against a real person, collectible from that person’s bank accounts, wages, and property.

Here’s the sentence that tends to land hardest with owners hearing this for the first time: the business does not have to be closed, bankrupt, or even struggling for the IRS to pursue the TFRP. It can happen while the doors are still open and payroll is still running.

Who the IRS Considers “Responsible” (It’s Broader Than You Think)

This is where the story stops being about job titles and starts being about actual control. The IRS doesn’t just go after the person whose name is on the building. It goes after whoever had the authority to decide which bills got paid and which didn’t.

That can include:

- The owner or officer who signs the checks

- A bookkeeper or controller who chose to pay vendors over the IRS

- A partner who had signature authority on the business bank account

- In some cases, an outside advisor who exercised real financial control

Two elements have to be true for the penalty to stick: the person had to be “responsible,” meaning they had the duty and authority to pay the taxes, and the failure had to be “willful,” meaning funds were available and used for something else instead. Using payroll tax money to cover rent, payroll, or a supplier during a rough month is exactly the kind of decision the IRS considers willful, even when it felt like the only option at the time.

What Letter 1153 Means and Why the Clock Matters

If the IRS decides to move forward, the notification arrives as Letter 1153, Proposed Assessment of Trust Fund Recovery Penalty. This is the moment the story shifts from slow-burn tension to a hard deadline. From the date of that letter, there is a 60-day window (75 days for those outside the U.S.) to appeal.

Miss that window, and the assessment becomes final. Once it’s final, the IRS can pursue personal bank levies, wage garnishment, and liens against personal property, completely separate from anything happening to the business itself.

This is also the moment people make the second bad decision in this story, right after the one that started it. Letter 1153 comes packaged with Form 2751, Agreement to Assessment. Signing it without understanding what it does means waiving appeal rights and agreeing to the assessment outright. It should never be signed reflexively.

Can the Business Survive This? Relief Options That Actually Exist

Here’s the part of the story that actually has a hopeful turn, because unpaid payroll tax debt is not automatically a dead end.

Depending on the situation, options include:

- Installment agreements that spread the business or personal liability into manageable monthly payments instead of one impossible lump sum

- Penalty abatement, when there’s a reasonable cause for the missed deposits, such as a documented cash flow event outside normal business operations

- Appealing the proposed TFRP within the 60-day window, before it becomes a personal, permanent liability

- Currently Not Collectible status, in cases where paying anything right now would create genuine, provable hardship

- Negotiated resolution for the business itself, addressing the corporate liability separately from any personal exposure

The honest version of this story is that not every case qualifies for every option. Eligibility depends on the specifics: how much is owed, how many quarters are involved, whether the business is still operating, and whether the notices have already escalated to Letter 1153. Anyone promising a guaranteed reduction before reviewing the actual case file is skipping a step that matters.

How Tax Hardship Center Helps With Payroll Tax Debt

Tax Hardship Center works payroll tax cases as what they actually are: cases with two layers of exposure, the business liability and the personal TFRP risk, that need to be diagnosed and handled together, not separately.

The process starts with pulling IRS transcripts and account history to see exactly which quarters are affected, whether a Revenue Officer has already been assigned, and how close the case is to a Letter 1153 assessment. From there, THC builds a resolution path that may include negotiating an installment agreement for the business, filing an appeal before the 60-day window on a proposed TFRP closes, or requesting an Offer in Compromise where the numbers genuinely support one.

For owners still running active payroll while this unfolds, the priority is keeping the business operational: coordinating with the existing CPA or bookkeeper rather than displacing them, reviewing payment arrangement options that fit real cash flow instead of theoretical best-case numbers, and explaining, in plain terms, what changes to vendor relationships or lien exposure to expect at each stage. Anyone weighing whether to handle this alone or bring in representation can compare the practical differences on the tax debt relief options page, or start with a free case review to find out where the case actually stands before the next notice arrives.

FAQs

Can the IRS really hold me personally liable for business payroll taxes?

Yes. Through the Trust Fund Recovery Penalty, the IRS can assess the unpaid trust fund portion of payroll taxes directly against any individual determined to be responsible and willful, regardless of the business entity type.

How much is the Trust Fund Recovery Penalty?

It equals 100% of the unpaid trust fund taxes, which is the employee’s withheld income tax plus their share of Social Security and Medicare. It does not include the employer’s matching FICA share.

What is Letter 1153 and how much time do I have to respond?

Letter 1153 is the IRS’s proposed TFRP assessment. You have 60 days from the letter date (75 if you’re outside the U.S.) to appeal before it becomes final and collectible.

Does closing my business stop the IRS from pursuing payroll tax debt?

No. The TFRP can be assessed against responsible individuals whether or not the business is still operating, and personal collection action can continue after the business closes.

Can payroll tax penalties be reduced or removed?

In some cases, yes, through penalty abatement for reasonable cause, or through negotiated resolution once the underlying balance is addressed. Eligibility depends on the specific facts of the case.

What if my bookkeeper made the decision, not me?

Responsibility is based on who had authority over the funds, not job title alone. Multiple people can be investigated, and more than one person can be held liable.

Should I sign Form 2751 if I get Letter 1153?

Not without understanding it first. Signing waives your appeal rights and agrees to the assessment. It’s worth having the case reviewed before signing anything.

Conclusion

Unpaid payroll taxes rarely stay a business-only problem for long. What starts as a missed deposit during a hard month can turn into failure to deposit penalties, daily interest, and eventually a Trust Fund Recovery Penalty aimed squarely at the person who made the call. The story doesn’t have to end there. The owners who come out the other side are almost always the ones who stopped waiting for the next letter and got ahead of the one already sitting on the desk.

Key Takeaways

- Withheld payroll taxes legally belong to the government the moment they’re withheld, not to the business.

- Missing a deposit deadline triggers Failure to Deposit Penalties ranging from 2% to 15%, depending on how late the deposit is.

- Interest accrues daily on both the unpaid tax and the penalties, and it never pauses for cash flow problems.

- The Trust Fund Recovery Penalty can make an individual personally liable for 100% of the unpaid trust fund taxes.

- Corporate structure does not protect responsible individuals from personal TFRP liability.

- The IRS looks at who controlled the money, not just who holds the title of owner or officer.

- Letter 1153 starts a strict 60-day window to appeal a proposed TFRP assessment.

- Signing Form 2751 without review waives your right to appeal and finalizes the assessment.

- Relief options include installment agreements, penalty abatement, appeals, and Currently Not Collectible status.

- Reviewing IRS transcripts early is the fastest way to know exactly where a payroll tax case stands.

Facing unpaid payroll taxes or a Letter 1153 notice? Get a free case review from Tax Hardship Center before the response window closes.