A revenue officer calls. Not a letter this time. A person, with a name and a voicemail, asking to schedule “a short interview” about your business’s payroll taxes.

You call back. They mention a form. Form 4180. And somewhere in the middle of that conversation, you hear a phrase that makes your stomach drop: personally liable.

This is the moment many business owners don’t see coming. You always thought unpaid payroll tax was the company’s problem. Turns out, the IRS has a form specifically designed to find out if it’s yours too.

Here’s exactly what that interview looks like, what they’re really asking underneath the questions, and how to walk in without handing them a case against you.

What Is IRS Form 4180, Really

Form 4180, officially titled the Report of Interview with Individual Relative to Trust Fund Recovery Penalty or Personal Liability for Excise Taxes, is the tool the IRS uses to determine who within a business should personally pay for unpaid payroll tax.

Not the business. You.

When a company withholds federal income tax and the employee share of Social Security and Medicare from paychecks, that money isn’t the company’s to spend. It’s held in trust for the government. When it doesn’t get paid over, the IRS calls it a trust fund tax problem and looks for a person to hold accountable through what’s known as the Trust Fund Recovery Penalty, or TFRP.

Form 4180 is how they build that case. It’s a structured interview, usually conducted by a revenue officer, either in person or by phone, designed to elicit specific facts from you about what you knew and what you controlled.

Why the IRS Wants to Interview You, Not Just the Business

Here’s the part that surprises most owners. The business can close. It can go bankrupt. It can disappear entirely. The Trust Fund Recovery Penalty doesn’t disappear with it, because the IRS isn’t just chasing the entity anymore. It’s chasing individuals.

Anyone who had the authority to decide which bills got paid and which didn’t can be on the list. Owners. Officers. Sometimes a bookkeeper who had check-signing authority. Sometimes more than one person from the same company gets interviewed, because the IRS often casts a wide net before narrowing it down.

If your business is behind on payroll taxes and struggling to catch up on the broader balance, it’s worth understanding your options for a small-business IRS payment plan before this stage ever gets underway. Once a 4180 interview is scheduled, the conversation has already moved from “how do we fix this” to “who is responsible for it.”

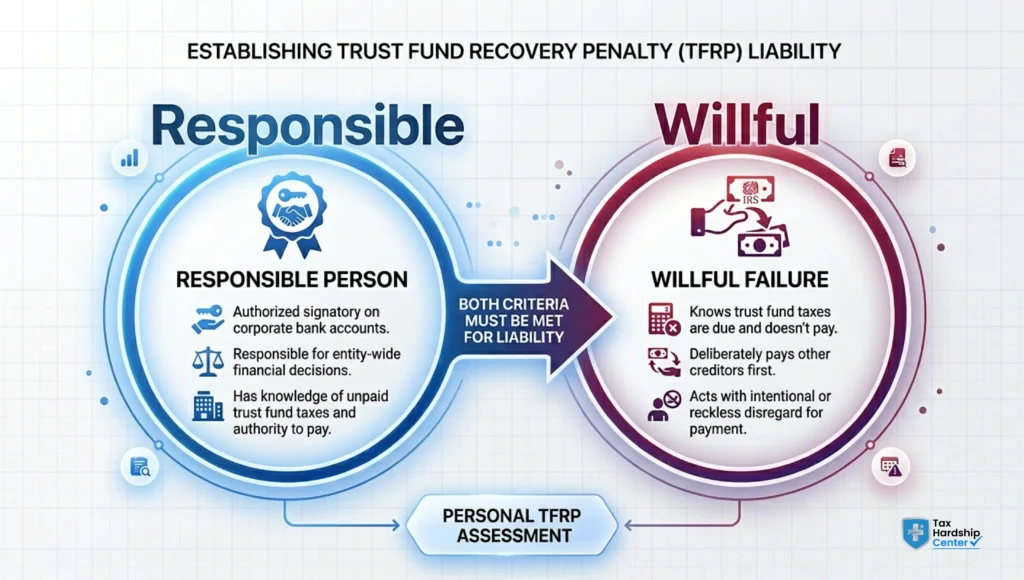

The Two Words That Decide Everything: Responsible and Willful

Every question on that form exists to answer two things.

Were you a responsible person? Meaning, did you have the authority to decide whether the payroll taxes got paid, even if you weren’t the one physically writing the check?

Were you willful? Meaning, did you know the taxes were owed and choose to pay something else instead, like rent, a vendor, or payroll itself, rather than the IRS?

Willful doesn’t mean malicious. It doesn’t require intent to defraud anyone. If you knew the money was owed and you decided, even reluctantly, even because you had no other choice at the time, to pay someone else first, that can be enough. This surprises almost every business owner who sits down for this interview. Many walk in believing they’ll get to explain the cash flow crisis. What they don’t realize is that explaining the cash flow crisis is often exactly what confirms willfulness.

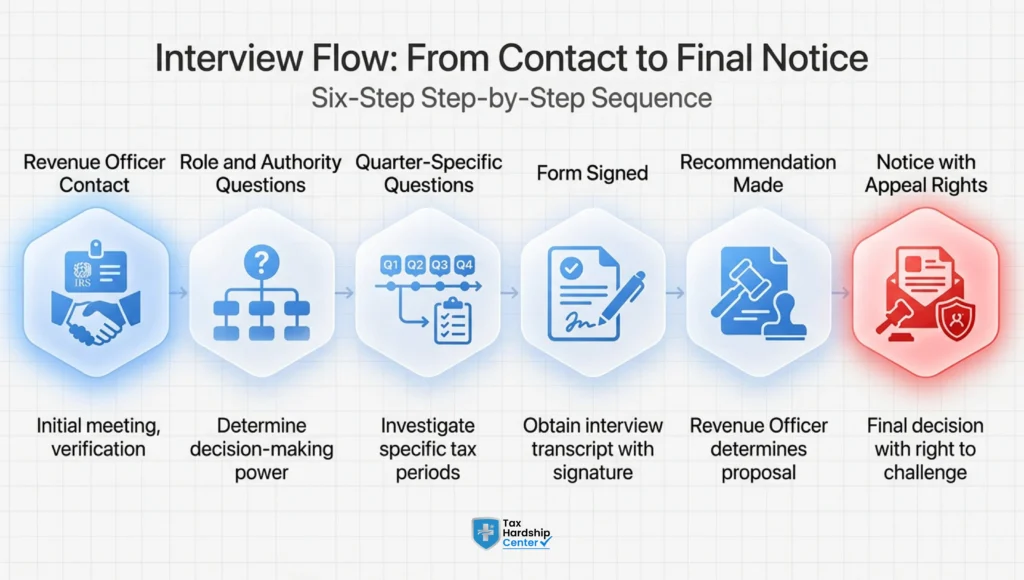

What Actually Happens in the Room (or on the Call)

The interview itself is more procedural than dramatic, but that doesn’t make it low stakes.

The revenue officer will identify themselves, explain the purpose of the meeting, and walk through your role at the company. Job title. Ownership percentage. Whether you could sign checks. Whether you could hire or fire employees. Whether you had access to the bank accounts. Whether you prepared or reviewed payroll tax returns.

Then it moves into the specific quarters where taxes went unpaid. Who decided which bills to pay during that period. Whether you knew, at the time, that payroll taxes were behind. Whether anyone told you.

The form is long, but it’s built for a reason. It’s meant to be filled out completely, in one sitting, directly by you or with you. Revenue officers are trained not to hand you the form in advance and not to let it be filled out by someone else on your behalf. This interview is happening whether you feel ready or not, which is exactly why preparation matters before the call is even scheduled.

The Questions They Ask, and What They’re Really Listening For

A few examples of what tends to come up, and what’s actually being measured:

“Who had authority to sign checks for the business?” They’re mapping who could have paid the IRS and didn’t.

“Did you know the payroll taxes were not being paid?” This is the willfulness question wearing a different outfit. Even a vague, honest “I had a general sense things were tight” can be used to establish knowledge.

“Were other creditors paid during this same period?” If vendors, rent, or even payroll itself got paid while the IRS didn’t, that pattern is one of the clearest signals the IRS looks for.

“What was your day-to-day role?” They’re testing whether your title matches your actual authority, because sometimes it doesn’t, and that gap matters.

None of these questions are designed to trap you unfairly. But they are designed to obtain a complete, specific, on-the-record account, and that account becomes the basis for whether the penalty is assessed against you personally.

The Mistake Almost Everyone Makes in This Interview

The single biggest mistake is treating this like a conversation instead of a formal, documented interview that becomes part of your case file permanently.

People try to explain the full financial story of the business. They talk about the slow season, the client who didn’t pay on time, the equipment that broke down. All of it may be true. Almost none of it changes the legal analysis of responsibility and willfulness, and much of it inadvertently confirms that you knew the taxes were unpaid and chose to keep the business running anyway.

The safer path is answering exactly what’s asked, factually and specifically, without volunteering a narrative the form isn’t asking for.

Can You Bring Someone With You

Yes, and this is one of the most important things to know before that call gets scheduled. You have the right to have a representative present, and you can pause the interview at any point to consult with one. If a business already has a CPA involved, it’s worth understanding how a tax attorney, CPA, and tax relief company each play a different role in a payroll tax case like this one, because a 4180 interview is exactly the kind of moment where the wrong kind of help, or no help at all, can cost you.

What Happens After the Form 4180 Is Signed

Once the interview is complete, the revenue officer uses your answers, along with financial records, signature cards, and check images, to recommend whether to assess the penalty against you. If they do, you’ll receive a formal notice with your appeal rights and a window to respond before the assessment becomes final.

This is also the point where resolution options start to matter again. If the penalty is assessed, there may still be room to negotiate payment terms or explore eligibility for an Offer in Compromise, depending on your financial situation. And if the underlying business still owes back taxes beyond the trust fund portion, comparing installment plan options is often the next real decision point.

Why Business Owners Facing Trust Fund Exposure Choose Tax Hardship Center

When a Form 4180 interview is on the calendar, the questions that matter most aren’t generic. They’re specific to your payroll cycle, your signature authority, and exactly what happened in the quarters the IRS is asking about. Tax Hardship Center handles these cases the way they need to be handled: by reviewing the business’s payroll tax history, check-signing records, and financial timeline before the interview, not after the damage is already on the record.

For business owners already facing payroll tax debt beyond the trust fund exposure itself, Tax Hardship Center coordinates a full picture of the case, from help with back taxes and IRS relief options to structuring a Form 9465 installment agreement for the business side of the balance. The goal is never just surviving the interview. It’s making sure the interview doesn’t become the reason a manageable business tax problem turns into a personal one.

What sets this apart from generic “settle for pennies” messaging is straightforward honesty about what the TFRP process actually involves. Not every owner interviewed ends up assessed. Not every case needs the same strategy. The Tax Hardship Center’s role is to determine what applies to your specific case before you’re sitting across from a revenue officer without a plan.

FAQs

What is IRS Form 4180 used for?

Form 4180 is the interview record the IRS uses to determine whether an individual should be held personally liable for a business’s unpaid trust fund taxes through the Trust Fund Recovery Penalty.

Who has to attend a Form 4180 interview?

Anyone the IRS believes may have had authority over the business’s finances, including owners, officers, and sometimes bookkeepers or accountants with check-signing authority.

Can I refuse to do the interview?

You can decline, but the IRS will typically move forward with its determination based on available records and other interviews, often without your side of the story on file.

Does signing Form 4180 mean I’m automatically liable?

No. Signing the form means you completed the interview. The revenue officer must still establish both responsibility and willfulness before recommending a penalty.

Can I bring a representative to the interview?

Yes. You have the right to have a representative present and can pause the interview to consult with one at any point.

What happens if the IRS decides I’m personally liable?

You’ll receive a formal notice with appeal rights and a set window to respond before the Trust Fund Recovery Penalty is assessed against you personally and becomes final.

Conclusion

A Form 4180 interview is one of the few moments in a tax problem where what you say directly determines whether a business debt becomes your personal debt. It’s not designed to be adversarial, but to obtain a complete, honest, and permanent record of your role in the business. Knowing what’s actually being asked, and why, is the difference between walking in exposed and walking in prepared.

Key Takeaways

- IRS Form 4180 is the interview the IRS uses to decide who personally pays for unpaid payroll trust fund taxes

- The penalty can apply to owners, officers, or anyone with real financial authority over the business

- Two things decide the outcome: whether you were a responsible person and whether you acted willfully

- Willful does not require bad intent, only knowledge that taxes were owed and a decision to pay something else first

- Revenue officers ask specific, factual questions designed to establish authority and knowledge on the record

- Explaining your full financial hardship story often hurts more than it helps in this specific interview

- You have the right to bring a representative and to pause the interview to consult with one

- The business closing or going bankrupt does not eliminate personal Trust Fund Recovery Penalty exposure

- Preparation before the interview is scheduled matters more than anything said during it

- If the penalty is assessed, payment and negotiation options still exist afterward

Facing a Form 4180 interview or already dealing with payroll tax debt? Get a free case review with Tax Hardship Center before you sit down with a revenue officer.