You haven’t filed a tax return in 10 years. Maybe longer. At first, it was one year you skipped because things were tight and you knew you wouldn’t owe much. Then it became two years, then five, then you stopped opening IRS letters entirely. Now the anxiety is worse than the debt ever was, and you have no idea where to start.

Here is what you need to know: the IRS does not forget. There is no statute of limitations on unfiled returns. The longer you wait, the worse the penalties get, and the harder it becomes to fix. But you can fix it. People do it every month. The process is not as complicated as you think, and the IRS would rather have you file voluntarily than force the issue through enforcement.

This guide walks through what happens when you don’t file for 10 years, which years you actually need to file, how to get the documents you no longer have, and the exact steps to take starting today.

What the IRS Does When You Don’t File for 10 Years

The IRS does not ignore long-term nonfilers. They track your income through W-2s, 1099s, and other third-party reports. Even if you never filed a return, the IRS knows how much income was reported under your Social Security number every year.

After several years of nonfiling, the IRS may file a Substitute for Return (SFR) on your behalf. This is not a favor. An SFR uses your reported income but does not include deductions, credits, or filing status adjustments that could lower your tax liability. The IRS calculates what you owe using the worst possible assumptions, then bills you for it.

Once an SFR is filed, the IRS can begin enforcement. That means wage garnishment, bank levies, and federal tax liens. If you receive Social Security, veterans’ benefits, or federal payments, the IRS can offset those as well. State tax refunds can be intercepted to pay federal back taxes.

If you owe money and the IRS has already filed an SFR, you can still file your own return to replace it. Filing your actual return almost always results in a lower balance than the IRS substitute return because you can claim deductions, credits, and the correct filing status.

Which Years You Actually Need to File

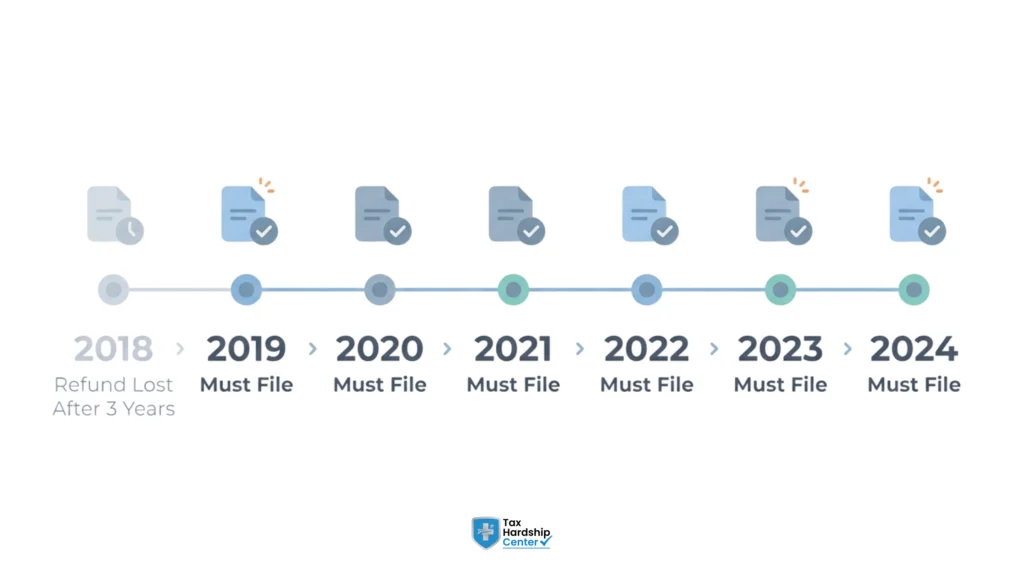

You do not need to file every single year for the past 10 years in most cases. The IRS generally requires the last six years of unfiled returns to bring you into compliance. However, the exact number depends on your situation.

If you owe money: File at least the last six years. The IRS may accept fewer if some years show refunds or minimal income, but starting with six is the safest approach.

If you are owed refunds: You can only claim a refund for returns filed within three years of the original due date. If you were owed a refund for 2015, you had until April 15, 2019, to file and claim it. After that, the refund is lost. You should still file those older returns if the IRS requires them for compliance purposes, but you will not receive a refund.

If you had no income or very low income in certain years: You may not be required to file at all for those years. The filing requirement is based on your income, filing status, and age. If your income was below the standard deduction for a given year, you likely do not need to file for that year. Request an IRS transcript for those years to confirm whether the IRS has a record of income reported under your Social Security number.

If you own a business or have self-employment income: File every year you had gross receipts of $400 or more, regardless of whether you had a profit. Self-employment income has a lower filing threshold than W-2 income.

How to Get Tax Documents You No Longer Have

You do not need to track down every W-2 or 1099 from the last 10 years. The IRS already has copies of most income documents reported to them.

Request a wage and income transcript. This is the fastest way to get a summary of your reported income for any year. You can request transcripts online at IRS.gov, by phone at 1-800-829-1040, or by mailing Form 4506-T. The transcript shows income reported by employers, banks, investment firms, and other third parties. It does not show deductions or expenses, but it gives you the income side of the return.

For self-employment income or business records: If you no longer have invoices, receipts, or profit-and-loss statements, reconstruct what you can. Bank statements, credit card statements, and emails can help you estimate income and expenses. The IRS allows reasonable estimates if you genuinely no longer have records. It is better to file with your best estimate than not to file at all.

For prior-year tax forms and instructions: You can download them from IRS.gov. Each tax year has its own forms, and you must use the correct year’s form when filing back taxes. Do not use the current year’s form for a 2018 return. The tax brackets, standard deductions, and credits change every year.

What Penalties and Interest Look Like After 10 Years

The failure-to-file penalty is 5% of the unpaid tax per month, capped at 25%. If you owe $10,000 and you don’t file for five months, the penalty caps at $2,500. After the penalty maxes out, interest continues to accrue on the unpaid balance and the penalty itself.

The IRS charges interest on unpaid tax from the original due date until the balance is paid in full. The interest rate changes quarterly and is currently around 8% annually. Interest compounds daily, which means you pay interest on unpaid interest. Over 10 years, interest can double the original debt.

If you file but don’t pay, the failure-to-pay penalty is 0.5% per month, capped at 25%. This penalty is much lower than the failure-to-file penalty, which is why the IRS always tells nonfilers to file even if they cannot pay. Filing stops the larger penalty immediately.

Example: You owe $15,000 in taxes from 2015 and never filed. The failure-to-file penalty maxed out at $3,750 after five months. Interest has been accruing for 10 years on the combined balance of tax plus penalty. Your current balance is likely over $30,000.

If you don’t owe any tax for a given year because your withholding covered your liability or you are owed a refund, there is no failure-to-file penalty for that year. The penalty only applies to unpaid tax.

Can You Go to Jail for Not Filing Taxes for 10 Years?

Criminal prosecution for failure to file is rare but possible. The IRS typically reserves criminal charges for cases involving fraud, willful evasion, or significant tax debt combined with intentional noncompliance over many years.

If you simply didn’t file because you were overwhelmed, disorganized, or scared, that is not the same as willful evasion. The IRS distinguishes between negligence and criminal intent. Most nonfilers face civil penalties, not criminal charges.

However, if the IRS believes you intentionally avoided filing to evade taxes, and your debt is substantial, they may refer your case to the Criminal Investigation Division (CID). Signs that increase the risk of criminal investigation include filing false documents, hiding income, using someone else’s Social Security number, or actively obstructing IRS collection efforts.

If you receive a summons or a letter referencing a criminal investigation, contact a tax attorney immediately. Do not speak to IRS agents without representation.

For most people who haven’t filed in 10 years, the consequence is financial, not criminal. The IRS wants compliance and payment, not incarceration.

Step-by-Step: How to File 10 Years of Back Taxes

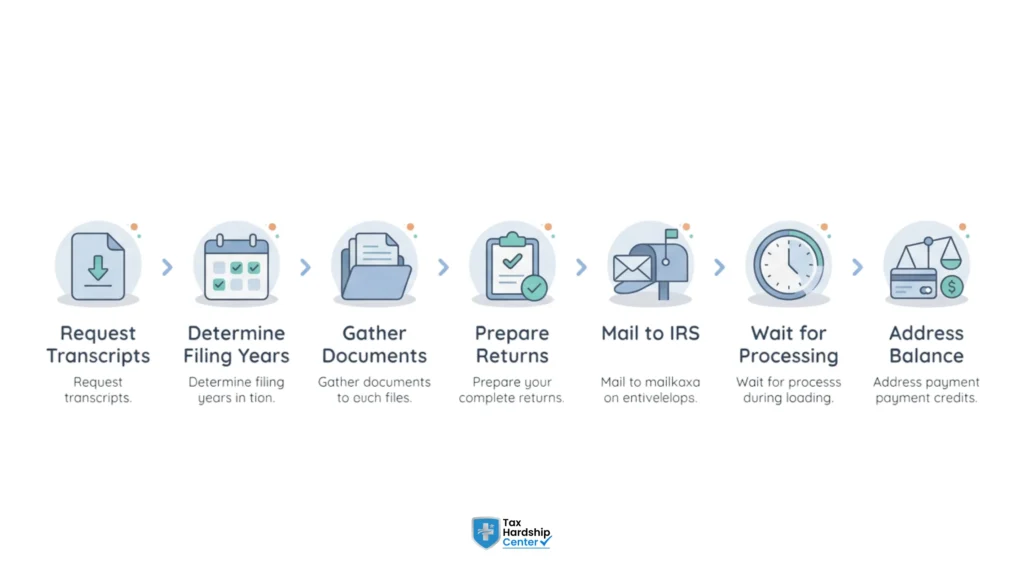

Step 1: Request your IRS transcripts

Call the IRS at 1-800-829-1040 or order transcripts online at IRS.gov. Request a wage and income transcript for each unfiled year. This shows what income was reported to the IRS under your Social Security number. If the IRS filed a substitute return for you, request an account transcript to see what they calculated.

Step 2: Determine which years require filing

Based on your transcripts, identify which years you had income above the filing threshold. If the IRS has already filed an SFR for a given year, you need to file an original return to replace it. If you had no income in certain years, confirm with the transcripts and document that those years do not require filing.

Step 3: Gather your documents

Use the wage and income transcripts as your primary source for income. If you have W-2s or 1099s saved, use those as well. For self-employment income or business expenses, reconstruct records using bank statements, invoices, and receipts. If records are lost, estimate based on what you remember and document your methodology.

Step 4: Prepare each return separately

File one return per year. Use the correct tax form and instructions for each year. Do not use current-year forms for prior years. You can prepare returns yourself using prior-year tax software, work with a CPA, or hire a tax resolution firm to handle the preparation.

Step 5: File the returns by mail

Back tax returns cannot be e-filed. You must print and mail them to the IRS address listed in the instructions for each year. Send each return in a separate envelope. Use certified mail with a return receipt requested so you have proof the IRS received it.

Step 6: Wait for confirmation and adjusted balances

The IRS will process each return and send you a notice showing your updated balance. Processing can take 8 to 16 weeks per return. If the balance is lower than the IRS originally calculated, they will adjust it. If it is higher, they will bill you for the difference.

Step 7: Address the balance

Once your returns are filed and processed, you can set up a payment plan, apply for an Offer in Compromise, request Currently Not Collectible status, or explore penalty abatement if you qualify.

For more on payment options after filing, see our guide on IRS payment plan options.

What Happens If You Owe More Than You Can Pay After Filing

Filing your returns does not mean you have to pay the balance immediately. The IRS offers several resolution options once your returns are current.

Installment agreement: You can set up a monthly payment plan if you owe less than $50,000 in combined tax, penalties, and interest. Payments are spread over up to 72 months. Apply online at IRS.gov or by calling the IRS. There is a setup fee, which is lower if you set up direct debit payments. Learn more about IRS installment agreements and how to apply.

Offer in Compromise (OIC): If you cannot afford to pay the full balance over time and your income and assets are limited, you may qualify for an OIC. This is a settlement where you pay less than the full amount owed. The IRS evaluates your ability to pay based on your income, expenses, and assets. Not everyone qualifies. The IRS rejects most OIC applications. For more on how OIC works and who qualifies, see our guide on Offer in Compromise eligibility.

Currently Not Collectible (CNC): If you cannot afford any payment right now because your income barely covers basic living expenses, you can request CNC status. The IRS pauses collection efforts while you are in CNC. You still owe the debt, and interest continues to accrue, but the IRS will not levy your wages or bank account. CNC is temporary. The IRS reviews your financial situation periodically.

Penalty abatement: If you have a reasonable cause for not filing, you may qualify for first-time penalty abatement or reasonable-cause abatement. This removes some or all of the failure-to-file and failure-to-pay penalties. It does not remove the underlying tax or interest. You must be current on all filings and have a clean compliance history for at least three years to qualify for first-time abatement.

Filing your returns is the first step. Once you are compliant, the IRS is more willing to work with you on resolving the balance.

When Professional Help Makes Sense for Long-Term Unfiled Returns

Filing one or two years of back taxes is one thing. Filing for 10 years is where most people get overwhelmed.

By that point, penalties pile up, records go missing, and the IRS may have already filed substitute returns that usually overstate what you owe because they don’t include deductions or credits.

Then comes the harder part: figuring out how to actually resolve the balance. Payment plans, Offers in Compromise, and hardship status all have different rules, and choosing the wrong option can make things worse.

Tax Hardship Center helps taxpayers file missing returns for multiple years, replace substitute returns, and determine the best resolution based on their financial situation. The process usually starts with pulling IRS transcripts, preparing the missing returns, and then working toward a payment plan, settlement, or penalty relief if the client qualifies.

If you haven’t filed in years and don’t know where to start, getting professional help early can save a lot of stress, time, and expensive mistakes later.

FAQs

What happens if I haven’t filed my taxes in 10 years?

The IRS will assess penalties and interest on any unpaid tax. They may file a Substitute for Return on your behalf using only your reported income and no deductions, which usually results in a higher tax bill than if you filed yourself. After several years, the IRS can begin enforcement actions, including wage garnishment, bank levies, and federal tax liens. You can still file your own returns to replace the IRS substitute returns and reduce the balance.

What should I do if I haven’t filed my taxes in 10 years?

Start by requesting IRS transcripts for the unfiled years to see what income was reported under your Social Security number. Determine which years require filing based on your income and filing status. Prepare and file the missing returns using prior-year tax forms. File even if you cannot pay the balance. Once your returns are current, you can set up a payment plan or explore other tax debt relief options.

Can you get in trouble for not filing taxes for 10 years?

Yes. The IRS can assess civil penalties and begin enforcement actions, including wage garnishment and bank levies. Criminal prosecution is rare but possible in cases involving fraud or willful evasion. Most nonfilers face financial penalties, not criminal charges. Filing voluntarily before the IRS forces compliance reduces the risk of escalation.

Does the IRS forgive tax debt after 10 years?

The IRS has a 10-year statute of limitations on collecting tax debt. Once 10 years pass from the date the tax was assessed, the IRS can no longer collect it. However, this 10-year period does not start until you file a return. If you never file, the clock never starts. Additionally, certain actions, such as filing for bankruptcy, submitting an Offer in Compromise, or leaving the country, can pause or extend the statute. The IRS rarely allows debt to expire without attempting to collect it.

Where to start if I haven’t filed taxes in 10 years?

Request IRS transcripts for each unfiled year. The transcripts show what income was reported to the IRS under your Social Security number and whether the IRS filed a substitute return for you. Use the transcripts to determine which years require filing. Gather any remaining W-2s, 1099s, or business records you have. Prepare each return separately using prior-year tax forms. File the returns by mail and wait for the IRS to process them and send updated balance notices.

Can I still get a refund if I filed taxes from 10 years ago?

You can only claim a refund if you file within three years of the original due date. If you were owed a refund for a return due in 2015, you had until April 15, 2019, to file and claim it. After that, the refund is lost. You may still need to file the return for compliance purposes, but you will not receive the refund.

Conclusion

Ten years of unfiled tax returns are not unfixable. The IRS deals with long-term nonfilers every day. What matters now is that you start. The longer you wait, the worse the penalties and interest become, and the closer you get to enforcement.

Filing is not as complicated as it feels when you’re staring at a decade of missing returns. You request transcripts. You figure out which years actually need to be filed. You prepare the returns using the IRS’s existing income data. You mail them in. You wait for the balances. Then you deal with what you owe.

If you owe more than you can pay, the IRS has options. Payment plans, settlements, and hardship status exist for exactly this situation. But none of those options are available until your returns are filed.

Key Takeaways:

- The IRS does not forget unfiled returns. There is no statute of limitations on filing

- You generally need to file the last six years to bring your account current, but it depends on your income and situation

- Request IRS transcripts to see what income was reported and whether the IRS filed substitute returns

- Penalties and interest compound over time. Filing stops the failure-to-file penalty immediately, even if you cannot pay

- Criminal prosecution is rare. Most nonfilers face financial penalties, not jail time

- File each year separately using prior-year tax forms. Back tax returns must be mailed, not e-filed

- Once your returns are filed, you can set up a payment plan, apply for an Offer in Compromise, or request Currently Not Collectible status

If you haven’t filed in 10 years and you don’t know where to start, get a free case review at Tax Hardship Center.