You just started a second job. The extra money will help with rent, bills, or debt. HR hands you a W-4 form and says, ” Fill it out. You remember doing this at your first job, so you fill it out the same way, sign it, and hand it back.

Then April comes. You file your taxes, and the IRS says you owe $1,800. You thought having two jobs meant more withholding, not less. Now you’re scrambling to figure out where the money will come from.

Here’s what happened: when you work two jobs, each employer withholds taxes as if that’s your only source of income. They don’t know about the other job. Your combined income pushes you into a higher tax bracket, but neither employer withheld enough to cover it. The result is a surprise tax bill you didn’t expect.

This guide explains exactly how taxes work when you have two jobs, how to fill out your W-4 correctly, and what to do if you already owe because your withholding was wrong. If you’re already dealing with a tax bill from this situation, Tax Hardship Center’s IRS resolution services can help you work through it.

Do You Get Taxed More If You Work Two Jobs?

Your tax rate doesn’t increase just because you have two jobs. What changes is your total income, and higher income means you move into higher tax brackets.

The U.S. tax system is progressive. Different portions of your income are taxed at different rates. According to IRS tax bracket guidance for 2026, the federal brackets for a single filer are:

- 10% on income up to $11,600

- 12% on income from $11,601 to $47,150

- 22% on income from $47,151 to $100,525

- 24% on income from $100,526 to $191,950

If you earn $35,000 at one job, most of your income falls in the 12% bracket. Add a second job, bringing your total to $55,000, and part of your income moves into the 22% bracket.

The problem: each employer calculates withholding based only on what they pay you. If Job A pays $35,000 and Job B pays $20,000, Job A withholds as if you’re in the 12% bracket, and Job B does the same. Neither knows about the other, so neither withholds the extra needed to cover the 22% bracket portion of your combined income. When you file, the IRS sees your total income of $55,000 and applies the correct rate; if your employers underwithheld, you owe the difference.

Why Your Tax Return Is Lower with Two Jobs

If you’ve worked two jobs before and noticed your refund dropped, or you owed money, it’s because of under-withholding.

Each employer uses your W-4 to calculate how much tax to withhold. The W-4 asks for your filing status and whether you want to account for multiple jobs. If you didn’t complete Step 2 (the multiple jobs section) on either W-4, both employers withheld as if you only earn what they pay you.

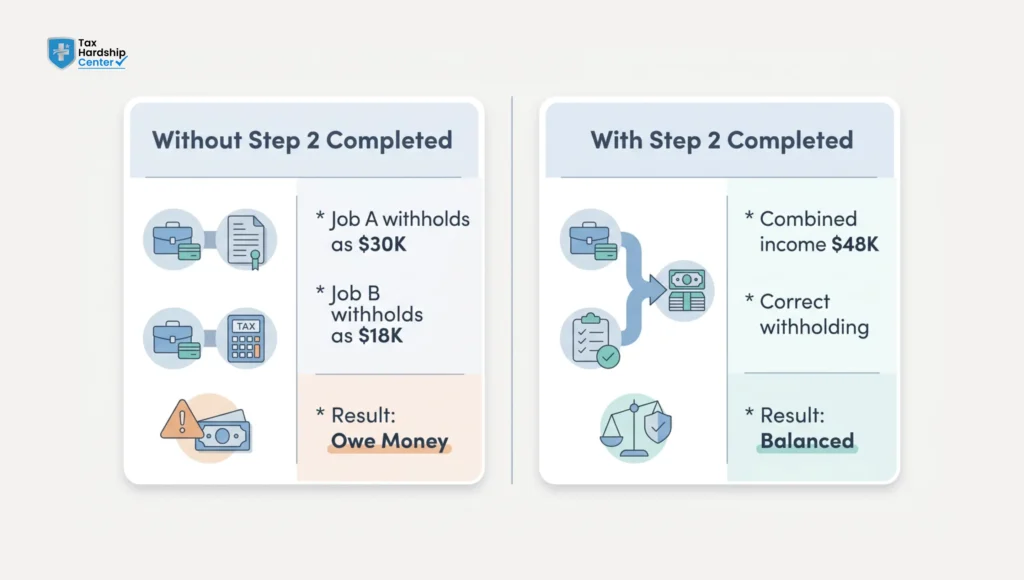

Example: You work Job A, making $2,500 per month, and Job B, making $1,500 per month. Your total annual income is $48,000.

- Job A withholds based on a $30,000 annual income

- Job B withholds based on $18,000 annual income

- But your actual income is $48,000, which puts you partially into the 22% bracket

The gap between what was withheld and what you actually owe creates a tax bill when you file.

The opposite can also happen. If both employers withhold at higher rates because you completed Step 2 correctly, you might see smaller paychecks throughout the year but get a refund at tax time, or simply break even.

How to Fill Out Your W-4 for a Second Job

The W-4 form has a section specifically for people with multiple jobs: Step 2, Multiple Jobs or Spouse Works. If you skip this step, you’ll under-withhold. You have three options:

Option A: Use the IRS Tax Withholding Estimator (Recommended)

Go to the IRS Tax Withholding Estimator. Enter your income from both jobs, your filing status, and any deductions or credits you expect to claim. The tool calculates how much you should withhold and tells you exactly what to enter on your W-4 for each job. This is the most accurate option.

Option B: Use the Multiple Jobs Worksheet

The W-4 form includes a worksheet in the instructions. You manually calculate your combined income and determine the additional withholding required. It takes longer than the estimator, but it works if you prefer not to use the online tool.

Option C: Check the Box for Two Jobs

If you have exactly two jobs total (or two jobs with no working spouse), you can check the box in Step 2(c). This tells your employer to withhold at a higher rate. It’s simpler but less precise. You might over-withhold and get a larger refund, or slightly under-withhold, depending on the income split between jobs.

The safest approach is Option A. The IRS estimator is free, accurate, and takes about ten minutes. You get specific numbers to enter on your W-4 and avoid surprises at tax time.

What Happens If You Don’t Update Your W-4

If you keep your W-4 the same after starting a second job, you’ll likely under-withhold. How much you owe depends on the second job’s pay and the bracket your combined income falls into.

- Small second job (under $10,000/year): You might owe $500 to $1,500 at tax time.

- Larger second job ($15,000 to $25,000/year): You could owe $2,000 to $4,000 if neither W-4 accounts for combined income.

The IRS also charges an underpayment penalty if you owe more than $1,000 and didn’t pay at least 90% of your current year’s tax through withholding or estimated payments. It’s avoidable by fixing your W-4 now. If you’ve already received a penalty notice, the Tax Hardship Center’s penalty abatement services may be able to help remove it.

Do You Have to File Taxes Twice If You Have Two Jobs?

No. You file one tax return that includes income from both jobs. Both employers send you a W-2 at the end of the year, and you report both W-2s on the same Form 1040.

When you file, your tax software or preparer adds up your total income from all sources, applies the standard deduction (or itemized deductions if applicable), and calculates your tax. They then subtract what was withheld from both jobs. If withholding was too low, you owe. If it was too high, you get a refund. All your income goes on one return; never file separately by job.

How to Avoid Owing Taxes with Two Jobs

The best way to avoid owing is to fix your W-4 as soon as you start the second job. Here’s the process:

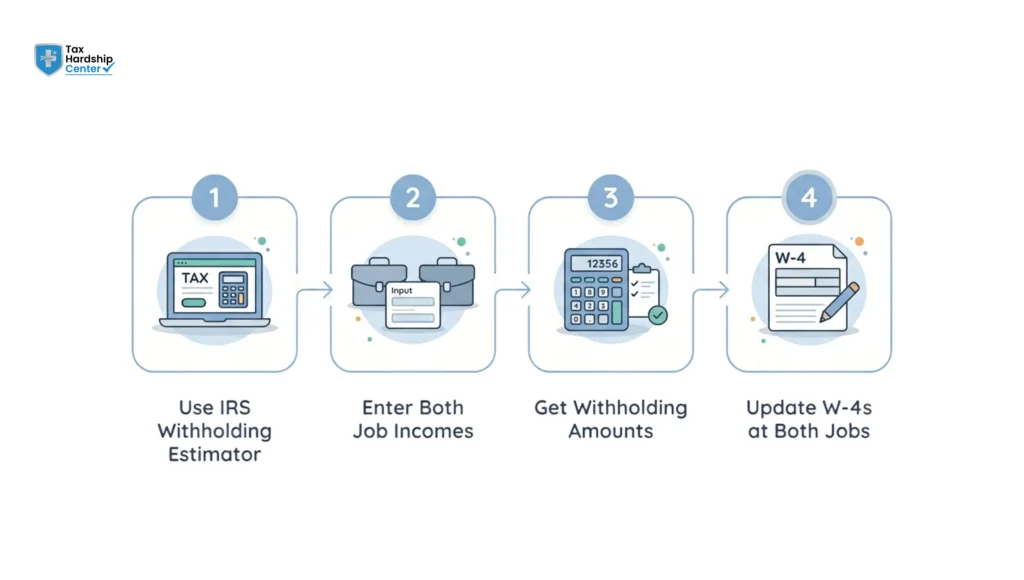

Step 1: Use the IRS Withholding Estimator

Go to irs.gov/W4app. Enter your income from both jobs, filing status, and expected deductions. The tool tells you what to enter on your W-4 for each job.

Step 2: Submit Updated W-4s to Both Employers

You can update your W-4 anytime. Submit a new form to HR or payroll at both jobs. Most employers process updates within one or two pay periods. If the estimator says you need extra withholding, enter a dollar amount in Step 4(c) of the W-4. For example, if it says you need an extra $50 per paycheck withheld, enter $50 in Step 4(c).

Step 3: Check Your Paystub After the Change

Once your employer processes the new W-4, confirm that your federal income tax withholding has increased. If it didn’t change, contact payroll to confirm they received and processed the updated form.

Step 4: Review Again If Income Changes

If you get a raise, change jobs, or one of your jobs ends, run the estimator again. What worked in January might not work in July if your pay has changed.

What If You Already Owe Because of Two Jobs?

If you already filed and owe money from under-withholding, you have options.

Pay in Full by the Tax Deadline: If you can pay the full amount by the April deadline, do it. You avoid interest and additional penalties. You can pay online through IRS Direct Pay, by credit card, or by check.

Set Up an Installment Agreement: If you can’t pay in full, the IRS offers payment plans. If you owe less than $50,000, you can apply online through the IRS payment plan tool. Monthly payments can be as low as $25, though interest and penalties continue accruing until the balance is paid. You avoid aggressive collection actions, such as levies and garnishments, as long as you stay current. A tax professional can help you set up an IRS payment plan that fits your actual monthly cash flow.

Request Penalty Relief: If this is your first time owing, you might qualify for First-Time Penalty Abatement. The IRS removes failure-to-pay penalties if you have a clean compliance history for the past three years. Request it after you receive your bill, either by calling the IRS or by writing a letter. The penalty can be several hundred dollars, so it’s worth asking.

Fix Your W-4 So It Doesn’t Happen Again: Once you handle the tax bill, update your W-4 for both jobs using the IRS estimator. If you don’t fix your withholding, you’ll owe again next year.

Is Getting a Second Job Worth It Tax-Wise?

It depends on how much the second job pays and which bracket your combined income falls into. According to a Tax Policy Center analysis of marginal tax rates, only the portion of your income exceeding the next bracket threshold is taxed at the higher rate, not your entire income.

Example: You earn $40,000 at your first job and $15,000 at your second. Total income: $55,000.

- The first $47,150 is taxed at 10% and 12%

- The remaining $7,850 ($55,000 minus $47,150) is taxed at 22%

You don’t pay 22% on the entire $55,000; you pay it only on the $7,850 that exceeds the 12% bracket threshold. If the second job is part-time and pays $10,000 or less per year, it’s almost always worth it financially. The real cost isn’t the tax rate. It’s the time, energy, and burnout from working two jobs. The financial benefit needs to outweigh that.

How the Tax Hardship Center Helps When Two Jobs Lead to Unexpected Tax Debt

Under-withholding across two jobs is one of the most common reasons people end up with surprise tax bills, sometimes across multiple years. Tax Hardship Center works specifically with taxpayers in this situation, where each employer withheld correctly for their portion of income but the combined picture left a $3,000 to $10,000+ gap with the IRS.

The firm handles installment agreement setup for taxpayers who can’t pay the full balance at once, structures payment plans around actual take-home pay from both jobs, and coordinates with the IRS to stop levy threats during the application process. For taxpayers who genuinely can’t afford the full amount owed, Tax Hardship Center prepares Offer in Compromise applications when income and assets support a settlement, and requests Currently Not Collectible status when necessary living expenses exceed monthly income.

The firm also submits penalty abatement requests for failure-to-pay penalties that accrued because the taxpayer didn’t realize their W-4 setup was incorrect. First-Time Penalty Abatement requests frequently succeed for people with clean filing histories who owed solely due to withholding miscalculation. Once the debt is resolved, Tax Hardship Center helps clients correct their W-4s and calculate accurate ongoing withholding to make sure it doesn’t happen again. If you’re carrying tax debt from working two jobs, contact Tax Hardship Center to review your options.

FAQs

Do you get taxed more if you work two jobs?

Not automatically. What changes is your total income, which can push part of your earnings into a higher tax bracket if withholding is not adjusted correctly.

Is getting a second job worth it tax-wise?

Usually yes. Only the income above each tax bracket threshold gets taxed at the higher rate, not your entire paycheck.

Do I have to file taxes for a second job?

Yes, but you file one combined tax return. Both jobs report income separately through W-2s that are included on the same filing.

Why is my tax return so low with two jobs?

Many employers withhold taxes based only on their own payroll, not your combined income. That can lead to under-withholding and smaller refunds.

How do I avoid owing taxes when working two jobs?

Update your W-4 forms and review your withholding regularly. IRS withholding tools can help estimate the right amount for your combined income.

Do you have to report having two jobs separately?

No separate notification is needed. The IRS receives W-2 information directly from both employers when you file your return.

What happens if I don’t report a W-2 from my second job?

The IRS will usually catch the missing income because employers report it directly. That can result in additional taxes, penalties, and interest.

Does having multiple jobs lower your tax return?

It can reduce your refund if withholding was not correctly adjusted for your combined earnings from both jobs.

Conclusion

Having two jobs doesn’t automatically mean you’ll owe taxes, but it does mean you need to adjust your W-4 at both jobs to withhold correctly. Each employer withholds based only on what they pay you. If your combined income pushes you into a higher tax bracket, neither employer will withhold enough unless you tell them to.

The fix is straightforward: use the IRS Tax Withholding Estimator to determine the correct withholding amounts for your combined income, and submit updated W-4s to both employers. This takes about 15 minutes and prevents a surprise tax bill in April.

If you already owe because your withholding was wrong, set up an installment agreement with the IRS, request First-Time Penalty Abatement if you qualify, and fix your W-4s so it doesn’t happen again. Your tax return reflects your total income from all sources. One return, both W-2s included. If withholding was correct, you’ll break even or get a small refund. The key is fixing it now so next year looks different.

Key Takeaways

- Each employer withholds taxes based only on what they pay you, not your combined income, which routinely causes under-withholding when you work two jobs

- Complete Step 2 of your W-4 at both jobs using the IRS Tax Withholding Estimator to calculate correct withholding for your total income

- You file one tax return that includes income from both jobs; both W-2s go on the same Form 1040, never separate returns

- Only the portion of your income exceeding each bracket threshold is taxed at the higher rate, not your entire combined income

- If you already owe from under-withholding, set up an IRS installment agreement and request First-Time Penalty Abatement if you have a clean filing history

- The IRS underpayment penalty applies if you owe more than $1,000 and didn’t pay at least 90% of your tax through withholding; fixing your W-4 eliminates this risk

- Update your W-4 at both jobs any time your income changes, whether that’s a raise, a job switch, or losing one job

- If you don’t report a W-2 from your second job, the IRS will catch it automatically and send a notice with additional tax, penalties, and interest

- First-Time Penalty Abatement frequently removes failure-to-pay penalties for taxpayers who owed solely due to withholding miscalculation and have a clean prior history

- Fixing your W-4 now takes about 15 minutes and prevents the same surprise tax bill from repeating every year