You just started a new job. HR hands you a W-4 form and says, “Fill this out.”

You stare at it. Multiple jobs or spouse works? Dependents? Extra withholding? You’re not sure what any of it means, so you skip sections, sign at the bottom, and hope it works out.

Then April rolls around. You either owe $2,000 you don’t have, or you got a $4,500 refund and realize you’ve been giving the IRS an interest-free loan all year.

The W-4 is not complicated once you understand what it actually does. It tells your employer how much federal income tax to withhold from each paycheck. Get it wrong, and you’re either scrambling to pay a tax bill or watching money sit with the government when it could have been in your account.

This guide breaks down exactly how the W-4 works, how to fill it out based on your situation, and when you should update it so you’re not caught off guard at tax time.

What Is a W-4 Form?

Form W-4 is the Employee’s Withholding Certificate. You fill it out when you start a new job or when your financial situation changes. It tells your employer how much federal income tax to subtract from your paycheck before you get paid.

The form does not calculate your total tax bill. It estimates how much tax you’ll owe for the year and spreads that amount across your paychecks. If your W-4 underestimates, you owe money when you file. If it overestimates, you get a refund.

The IRS redesigned the W-4 in 2020. The old version used allowances. The new one does not. Instead, it asks about your filing status, number of jobs, dependents, and any extra income or deductions you want to account for.

You do not file the W-4 with the IRS. You give it to your employer, and they use it to calculate your withholding. If you don’t submit one, your employer defaults to withholding as if you’re single with no adjustments, which usually results in higher withholding and a larger refund later.

According to the IRS, employees can update their W-4 at any time, and reviewing it at least once a year is strongly recommended to avoid underpayment penalties or unnecessary overwithholding.

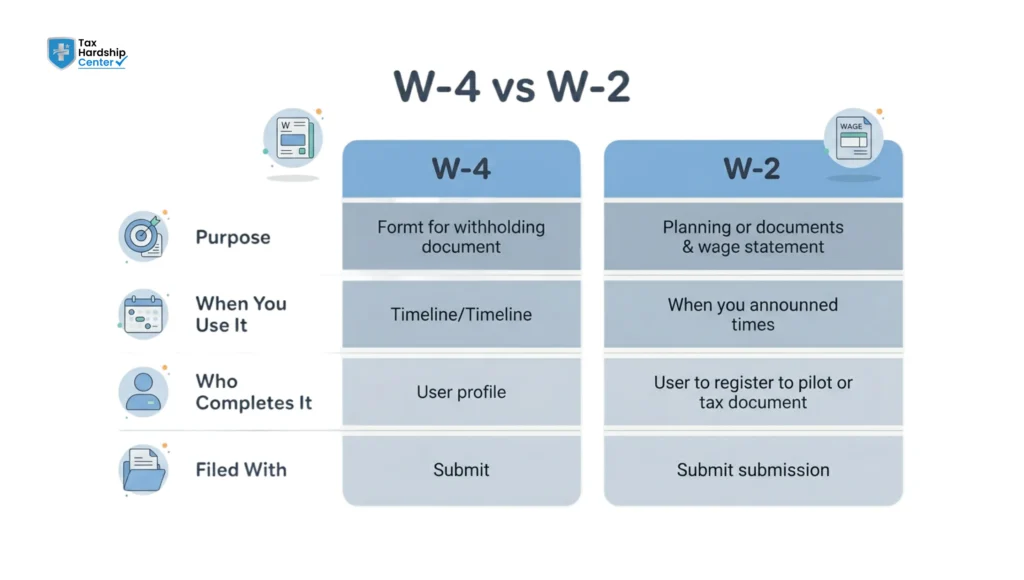

W-4 vs W-2: What’s the Difference?

People confuse these two forms constantly. They serve completely different purposes.

The W-4 is what you fill out when you start a job. It tells your employer how much tax to withhold from your paycheck. You control it.

The W-2 is what your employer gives you at the end of the year. It shows how much you earned and how much tax was withheld. You use it to file your tax return. Your employer controls it.

If your W-4 is filled out incorrectly, your W-2 will reflect that in the withholding totals, and you’ll either owe money or receive a refund you didn’t plan for. The two forms are connected, but they work at opposite ends of the tax year.

For a deeper look at how year-end documents connect to your overall tax filing, see our guide on how to file old tax returns.

How to Fill Out Your W-4 Form in 2026

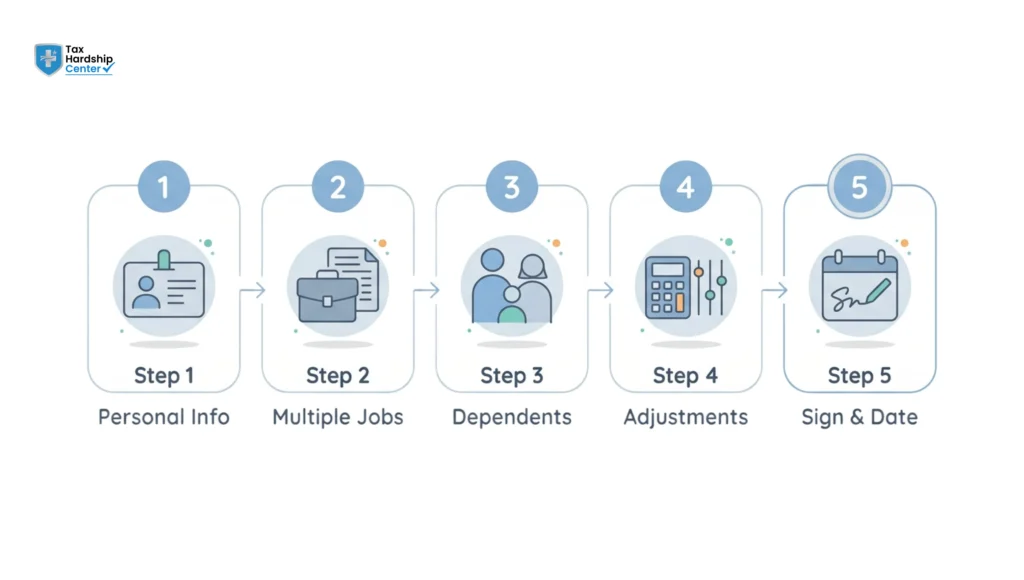

The 2026 W-4 has five steps. Only Step 1 and Step 5 are required. Steps 2 through 4 are optional, but skipping them can throw off your withholding if your situation is anything more than a single job with no dependents.

Step 1: Enter Personal Information

This section is required. You will enter your name, address, Social Security number, and filing status. Your options are: Single, Married Filing Jointly, Married Filing Separately, Head of Household, or Qualifying Surviving Spouse.

Your filing status matters significantly. If you’re married and both spouses work, choosing “Married Filing Jointly” without completing Step 2 can result in under-withholding because the form assumes only one income for the household.

Step 2: Multiple Jobs or Spouse Works

If you work more than one job, or you’re married and your spouse also works, this step adjusts your withholding to account for combined income. You have three options:

Option A: Use the IRS Tax Withholding Estimator. It walks through your income, deductions, and credits and tells you exactly what to enter.

Option B: Use the Multiple Jobs Worksheet included with the W-4 instructions. This is the manual version of the estimator.

Option C: Check the box if you and your spouse each have one job, or if you personally have exactly two jobs. This instructs your employer to withhold at a higher single rate, which prevents under-withholding but may result in a refund.

Skipping Step 2 is the most common reason people under-withhold. The withholding calculation assumes a single source of income. If you or your spouse earns additional income, your tax bracket increases, but your withholding does not adjust unless you indicate it should.

Step 3: Claim Dependents and Other Credits

If you have dependents, this is where you account for them. The form asks for the number of qualifying children under 17, multiplied by $2,000, and the number of other dependents, multiplied by $500. Add those together and enter the total.

The Child Tax Credit is worth $2,000 per qualifying child for 2026. Other dependents, such as a qualifying relative or a child over 17, are worth $500 each. If your income exceeds $200,000 as a single filer or $400,000 as a married joint filer, these credits begin to phase out. Use the IRS estimator if you’re near those thresholds.

Step 4: Other Adjustments (Optional)

This section lets you fine-tune withholding beyond what Steps 2 and 3 cover.

(a) Other income not from jobs: If you have interest, dividends, or retirement income that isn’t subject to withholding, enter it here. Your employer will increase withholding to cover the tax on that additional income.

(b) Deductions: If you plan to itemize deductions beyond the standard deduction, such as mortgage interest or large charitable contributions, enter the estimated amount here. This reduces withholding because you’ll owe less tax.

(c) Extra withholding: If you want an additional flat dollar amount withheld from each paycheck, enter it here. This is useful if you’ve consistently owed taxes at the end of the year and want to close the gap before it results in a penalty.

Most people with straightforward situations, one job, and the standard deduction do not need to touch this section. But if you have side income, investment income, or significant itemized deductions, Step 4 is where you account for all of it.

Step 5: Sign and Date

Required. Without your signature, the form is invalid, and your employer cannot process it.

Why Your Withholding Amount Matters

Withholding too little means you owe money in April. Withholding too much means the IRS holds your money all year and returns it as a refund. Neither extreme is ideal.

Large refunds feel like a bonus, but they represent money you earned and could have used throughout the year. The IRS does not pay interest on overwithholding.

Under-withholding creates the opposite problem. If you owe $1,000 or more and did not pay at least 90% of your current year’s tax, or 100% of last year’s tax (110% if your income exceeded $150,000), the IRS can charge an underpayment penalty on top of what you owe. Getting your withholding right means you arrive at tax time without a surprise bill and without handing the government a free loan.

If W-4 errors have already created a tax debt, our IRS payment plan assistance can help you structure a resolution that fits your budget.

When You Should Update Your W-4

Your W-4 is not a set-it-and-forget-it document. You should submit an updated form whenever any of the following apply:

- You get married or divorced

- You have a child or your dependent situation changes

- You start a second job or your spouse starts or stops working

- You buy a home and begin claiming mortgage interest

- You receive a large bonus or commission that increases your expected income

- You are consistently getting large refunds or owing money at tax time

Submit the updated W-4 to your employer’s payroll or HR department. Most employers process changes within one or two pay periods. If you’re approaching year-end and realize your withholding is short, you can submit a new W-4 with a specific extra withholding amount in Step 4(c) to close the gap before December 31.

Common W-4 Mistakes

Filling it out once and never revisiting it. Life changes. Withholding should reflect that. A W-4 completed five years ago may no longer match your current tax situation.

Skipping Step 2 when you have multiple jobs. This is the single most common cause of under-withholding. The form does not know about a second job or a working spouse unless you tell it.

Claiming dependents without checking income phase-outs. If your income is above $200,000 single or $400,000 married, credits reduce or disappear entirely. The W-4 does not self-correct for that.

Guessing at extra withholding amounts. The IRS estimator takes about ten minutes and gives you a precise number. Guessing typically results in either over- or under-withholding.

Not adjusting after a major life event. Marriage, a new child, or a home purchase all shift your tax liability. If the W-4 doesn’t reflect that, your paychecks won’t either.

Can You Claim Exempt on Your W-4?

Yes, but the conditions are strict.

You can claim exemption only if you had zero federal income tax liability in the prior year and you expect zero federal income tax liability in the current year. If both of those are true, your employer will withhold nothing in federal income tax from your paycheck. You still pay Social Security and Medicare taxes regardless.

Claiming exemption when you don’t actually qualify will result in a large tax bill and potential penalties when you file. The IRS also requires you to renew your exempt status every year by February 15. If you miss that deadline, your employer will revert to withholding as if you’re single with no adjustments.

Most employees do not qualify for exempt status. If you had any tax liability last year or expect one this year, this option does not apply to you.

Why Tax Hardship Center Is the Right Partner When W-4 Errors Create Tax Problems

A W-4 filled out incorrectly can quietly build a tax debt over months or years without you realizing it until the IRS sends a notice. Tax Hardship Center works specifically with taxpayers whose withholding issues, whether from multiple jobs, unreported side income, or life changes that were never updated on the form, led to unexpected balances, penalties, and IRS enforcement.

Our team handles the full resolution process: setting up IRS installment agreements for taxpayers who under-withheld and now owe a balance, requesting penalty abatement for first-time or qualifying underpayment penalties, and addressingback taxes from prior years where withholding was consistently insufficient. For small business owners and self-employed individuals who skipped estimated payments, we also resolve payroll tax issues and personal income tax debt tied to under-reporting.

If the IRS has escalated to wage garnishment or a bank levy as a result of unpaid withholding-related debt, we work to stop enforcement quickly and build a resolution path that addresses the underlying balance. Get a free case review to understand exactly where you stand, what resolution options apply, and what it will take to get current with the IRS.

FAQs

What is a W-4 form used for?

A W-4 tells your employer how much federal tax to withhold from your paycheck. It helps align your withholding with your expected annual tax liability.

How do I fill out my W-4 correctly?

You complete sections based on your filing status, dependents, multiple jobs, and additional income or deductions. The goal is accurate withholding throughout the year.

Can I update my W-4 at any time?

Yes. You can submit an updated W-4 whenever your financial or personal situation changes, and employers usually apply updates quickly.

What happens if I never submit a W-4?

Your employer typically withholds taxes at the default rate, which can lead to more withholding than necessary or mismatches with your actual tax situation.

What is the difference between a W-4 and a W-2?

The W-4 sets your withholding preferences, while the W-2 reports your annual earnings and taxes withheld for filing your return.

Do I still claim 0 or 1 on my W-4?

No. The IRS removed the old allowance system, and the current form now uses updated withholding calculations instead.

Can I claim exemption on my W-4?

Only if you qualified for no federal income tax liability previously and expect the same this year. Incorrectly claiming an exemption can create penalties later.

How do I know if my W-4 is correct?

Review your withholding yearly or after major life changes. IRS withholding tools can help estimate whether your current setup is accurate.

Conclusion

The W-4 determines how much federal income tax is withheld from each paycheck. Fill it out accurately, and you’ll pay close to what you actually owe throughout the year. Fill it out carelessly, and you’ll either face an unexpected bill in April or miss out on cash you could have used all year long.

At a minimum, complete Step 1 and Step 5. If you work multiple jobs, have a working spouse, or claim dependents, complete Steps 2 and 3 as well. Use Step 4 if you have side income, significant deductions, or want to adjust your withholding manually. Update the form whenever your life changes. And if you’re ever unsure, the IRS Tax Withholding Estimator is free, takes about ten minutes, and removes the guesswork entirely.

Key Takeaways

- The W-4 tells your employer how much federal income tax to withhold from each paycheck, not your total tax owed

- Only Step 1 and Step 5 are required, but skipping Steps 2 and 3 causes under-withholding in most multi-income households

- The allowance system (claiming 0 or 1) was eliminated in 2020 and no longer applies to any current W-4

- Step 2 must be completed if you work multiple jobs or your spouse is employed; withholding will fall short

- Step 4 handles side income, itemized deductions, and voluntary extra withholding beyond what the standard calculation covers

- Claiming exempt is only valid if you had zero tax liability last year and expect zero this year, and must be renewed annually by February 15

- Large refunds are not a financial win; they represent money you earned but could not access all year

- You can submit an updated W-4 to your employer at any time, and changes typically take effect within one to two pay periods

- The IRS Tax Withholding Estimator removes guesswork and gives you precise numbers to enter on the form

- W-4 errors that created a tax debt can be resolved through installment agreements, penalty abatement, or other IRS relief options