Introduction

Tax relief in the United States functions as a set of federal programs, legal mechanisms, and administrative pathways designed to help taxpayers reduce, reorganize, or temporarily pause their obligations when financial strain makes full payment difficult. The national system centers on Internal Revenue Service authority, which evaluates each taxpayer through income patterns, household structure, allowable expenses, and asset equity. This federal framework applies to residents of every state, though the circumstances that influence relief often vary by local economic conditions, state-level tax obligations, and individual financial histories.

The concept of tax relief in the United States rests on several core entities. The IRS acts as the governing body responsible for evaluating hardship, approving payment arrangements, reviewing financial disclosures, and applying regulations that define what constitutes collectability. Taxpayers, as the second key entity, provide economic information demonstrating how their current circumstances affect their ability to meet federal obligations. Various programs, including Offers in Compromise, installment agreements, and hardship designations, serve as the procedural channels through which relief is granted. These programs intersect with enforcement tools such as liens, wage garnishments, and bank levies, creating a dynamic environment in which timing, documentation, and communication are decisive.

In recent years, nationwide demand for tax relief has increased as more households experience income fluctuations, medical expenses, inconsistent gig-work earnings, or long-term debt accumulation. This has elevated the importance of intervention services capable of navigating IRS systems, interpreting federal standards, and coordinating relief requests for residents of any state. Authorized tax representatives, including Enrolled Agents, CPAs, and tax attorneys, operate as intermediaries who manage filings, communicate with IRS personnel, and ensure compliance with regulatory requirements.

High-quality tax relief information must clarify how federal programs work, what factors determine eligibility, and how national service providers support taxpayers in every region. This includes explaining how IRS policies interact with state revenue departments, how hardship calculations are formed, and how professional representation influences outcomes.

Key Takeaways

- IRS tax relief applies uniformly across all 50 states under federal authority.

- Eligibility depends on income, household expenses, asset equity, and compliance history.

- Primary IRS programs include Offers in Compromise, installment agreements, and hardship status.

- State tax obligations can coexist with federal debts, requiring coordinated relief strategies.

- Licensed tax professionals improve accuracy, documentation quality, and communication with the IRS.

National Tax Relief USA: Core Entities, Eligibility Factors, and Federal Authority

National tax relief refers to the set of IRS-administered programs that function identically across all states. The program structure is rooted in federal law rather than state statutes, meaning all residents, regardless of region, are subject to the same regulations for hardship verification, payment arrangements, and debt-reduction methods. These programs depend on a series of interlinked entities that underpin IRS decision-making.

One central relationship involves federal authority and taxpayer financial disclosure. The IRS evaluates the taxpayer’s financial standing based on allowable expenses, gross monthly income, household size, equity in assets, and employment type. These elements align with IRS National Standards and Local Standards. National Standards define regular living expenses such as food and clothing, while Local Standards determine acceptable housing, utility, and transportation costs based on geographic location. This creates a consistent framework while still accommodating regional cost variations.

Key eligibility factors include:

- Total tax liability and whether the debt is growing through penalties or interest

- Filing compliance across prior years

- Documented financial hardship

- Asset liquidity and potential equity

- Remaining time before the Collection Statute Expiration Date

Each factor contributes to a broader picture that influences whether the IRS grants relief, offers partial settlement, or places a temporary hold on collection.

The federal nature of tax relief also creates uniformity in how taxpayers are evaluated and treated. This eliminates the need for state-specific IRS procedures while still allowing variations where local costs influence expense approvals. National relief services, therefore, focus on interpreting these federal standards, preparing accurate financial disclosures, and presenting the taxpayer’s situation in a format that aligns with IRS documentation expectations.

The relationship between relief eligibility and the collection process is central to national tax relief. When financial strain is established through verified documentation, the IRS may reconsider past enforcement actions or suspend specific collection steps. In contrast, incomplete records, unfiled returns, or inconsistent financial statements can limit available relief channels.

National tax relief services address the need for consistent representation across states. Authorized practitioners interact with IRS agents through established communication protocols, allowing relief applications to be handled efficiently regardless of the taxpayer’s location. This structure ensures that residents in rural, urban, or high-cost areas can access the same federal programs when seeking assistance.

IRS Tax Help USA: Primary Relief Programs and Their Required Conditions

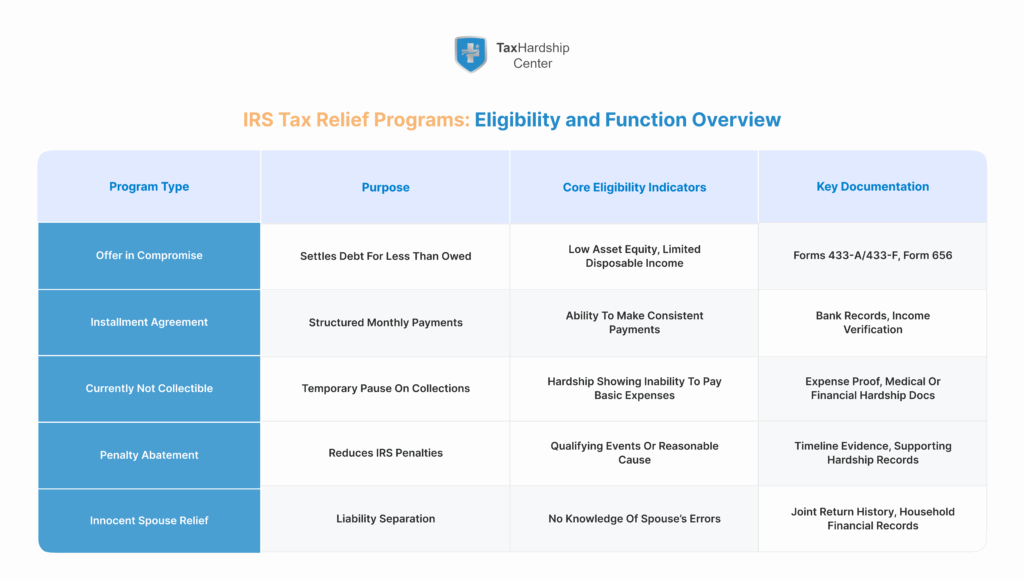

IRS tax help in the United States is structured around several key programs that address different types of financial difficulty. These programs operate under defined criteria, documentation standards, and procedural steps. Each program responds to a specific financial condition, establishing a direct relationship between the taxpayer’s hardship level and the type of relief granted.

Offer in Compromise

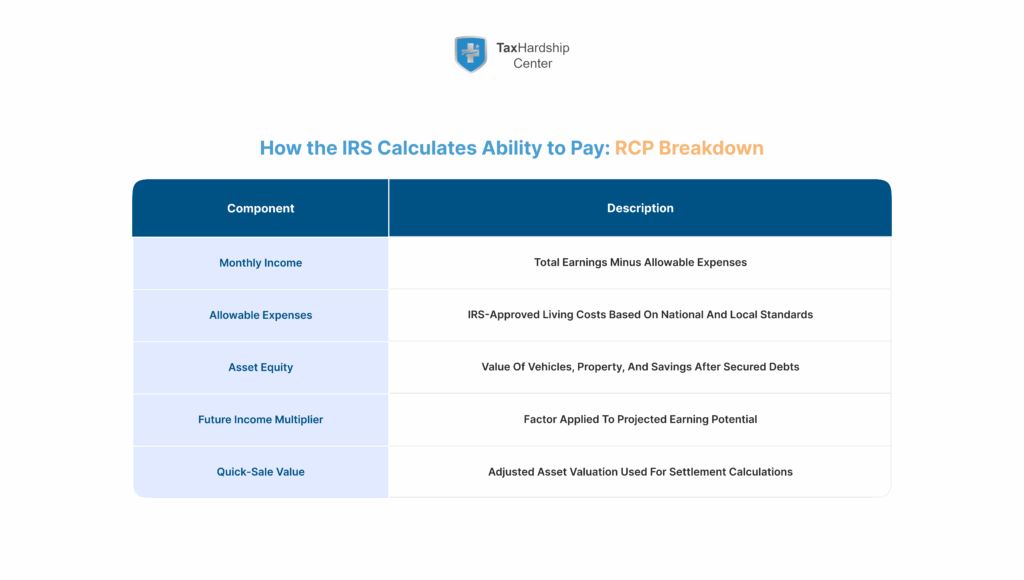

An Offer in Compromise is a negotiated settlement in which the IRS accepts less than the total amount owed. This program relies on the calculation of Reasonable Collection Potential. The IRS examines net income, equity in property, savings, investments, and future earning capability. The offer is accepted when the calculated potential indicates that collecting the full balance is unlikely within the remaining statutory period. Accurate financial disclosure is essential because undisclosed assets or fluctuating income patterns can cause rejection.

Installment Agreements

Installment agreements provide structured monthly payment plans. The IRS authorizes several forms of arrangements: guaranteed, streamlined, non-streamlined, and partial payment. Approval depends on the total amount owed, compliance with filing requirements, and the taxpayer’s ability to maintain the payment schedule. These agreements prevent forced collection actions, although interest and penalties may continue during repayment.

Currently Not Collectible Status

Currently, Not Collectible status applies when immediate payment would cause significant financial hardship. The IRS evaluates bank statements, employment records, household expenses, and any supporting medical or caregiving documentation. Once granted, collection activity pauses until financial conditions change. The status is often reassessed through periodic income reviews.

Penalty Abatement

Penalty abatement removes or reduces federal penalties when reasonable cause is demonstrated. Circumstances such as medical emergencies, natural disasters, or unavoidable disruptions can qualify. The IRS reviews the timeline of events, duration of hardship, and evidence supporting the inability to file or pay on time.

Innocent Spouse Relief

In situations involving joint returns, Innocent Spouse Relief separates liability when one spouse was unaware of misreported income or improper deductions. The IRS evaluates the nature of the relationship, financial control dynamics, and whether the requesting spouse benefited from the error.

Together, these programs form the core of IRS tax assistance nationwide. Each requires consistent documentation and a clear demonstration of financial circumstances. When applied correctly, these relief channels offer structured paths that reduce or manage federal tax burdens for individuals facing economic strain.

Tax Relief in All 50 States: How State Tax Agencies Differ from the IRS

Tax relief across the United States follows a dual structure that includes federal programs administered by the Internal Revenue Service and separate mechanisms overseen by state Departments of Revenue. While IRS procedures remain consistent nationwide, state agencies operate under individual statutes and collection systems, creating distinct rules for penalties, interest accrual, payment programs, and hardship requests. Understanding these differences is essential, particularly when a taxpayer owes both federal and state balances that require coordinated management.

State tax systems vary in how they assess compliance and initiate collection. Some states issue automatic wage garnishments after a short delinquency period, while others follow a more extended notification process before enforcement begins. Interest rates also differ considerably: states like California apply varying rates based on economic conditions, while other states use fixed annual percentages. These variations influence how quickly debt grows and how urgently relief may be required.

Common differences across state agencies include:

- The rate of penalty accumulation and interest increases

- Notice timelines and warning letters

- Garnishment authority and limits

- Eligibility requirements for state-level hardship programs

- Statute of limitations for collections

- Documentation standards for financial disclosure

A structured comparison clarifies how states vary:

| Entity | Enforcement Speed | Hardship Program Availability | Interest Characteristics |

| California FTB | Fast escalation | Broad options | Variable annual rates |

| New York DTF | Moderate escalation | Income-based hardship plans | High compounded interest |

| Texas Comptroller | Limited personal income tax issues | Focus on business taxes | Interest fixed by rule |

| Florida DOR | Moderate escalation | Installments common | Consistent rate adjustments |

Although the IRS handles federal obligations, many individuals face simultaneous state debts, requiring strategies that address both systems. Relief processes often begin with federal filings because IRS decisions influence the taxpayer’s remaining income and asset profile, which can later be used when negotiating with state agencies.

Nationwide tax relief providers play an essential role in coordinating these multilevel obligations. By managing communication with both federal and state authorities, representatives can sequence submissions, arrange payment plans that reflect the combined financial impact, and prevent conflicting requests. For example, an Offer in Compromise may adjust disposable income calculations, which later becomes relevant when applying for a state installment plan.

Tax relief in all 50 states, therefore, intersects federal standards with diverse state-level systems. Each state creates its own path to compliance, enforcement, and hardship assistance. When analyzed together, these systems form a nationwide network that requires consistent documentation, accurate financial interpretation, and a state-specific understanding of tax collection procedures.

IRS Notice System: How Federal Notices Trigger the Need for Immediate Tax Relief

The IRS notice system serves as a structured escalation process that signals increasing urgency for a taxpayer’s account. Each notice type has a defined role: it communicates either an initial balance, a reminder, a final warning, or an impending enforcement action. Understanding these notices is critical because the timeline between them controls when penalties intensify, when liens may be filed, and when levies or garnishments become imminent.

The sequence typically begins with CP14, which identifies a balance due after a return is processed. If the balance remains unpaid, the IRS issues CP501 and CP503 as reminder notices. CP504 represents a significant shift, indicating the government’s intent to levy specific assets. Beyond CP504, notices such as LT11 and Letter 1058 outline final opportunities for appeals before enforced collection.

A simplified sequence appears below:

- CP14: initial balance due

- CP501: first reminder

- CP503: second reminder

- CP504: intent to levy certain assets

- LT11 or Letter 1058: final notice before enforced collection

- Levy or garnishment issuance

- Potential lien filing

Each notice carries implications that influence relief options. When the account remains in the early stages, payment plans or penalty abatements are typically easier to arrange. As the process progresses, the availability of specific relief programs may narrow, and financial reviews become more stringent.

Liens represent a separate action that secures the government’s interest in property. Once a lien is filed, credit reporting, borrowing ability, and asset transactions may be affected. Levies, by contrast, remove funds directly from wages or bank accounts. These enforcement tools operate under defined legal authority and can be paused or prevented through relief programs such as installment agreements, Offers in Compromise, or Currently Not Collectible status.

Appeal rights exist throughout the notice process, and independent IRS appeals officers review whether procedures were followed correctly and whether relief avenues remain available. Documentation must be consistent and timely, as appeals are often deadline-driven.

The notice system creates a structured environment where timing plays a decisive role. When notices escalate, the need for accurate financial disclosures and strategic relief decisions becomes increasingly important. Effective navigation of this system requires understanding how each notice operates and how relief programs intersect with enforcement timelines.

Nationwide Tax Relief Services: Role of Licensed Tax Professionals

Licensed tax professionals serve as authorized representatives who communicate directly with the IRS, prepare financial documentation, and construct relief strategies. These professionals include Enrolled Agents, Certified Public Accountants, and tax attorneys. Each carries specific authority under federal regulations, which allows them to file forms, respond to notices, and participate in negotiations for taxpayers residing in any state.

Enrolled Agents specialize in federal tax matters and often manage the majority of relief cases. Their expertise includes interpreting IRS financial standards, preparing hardship documentation, and assembling offers or installment requests. CPAs bring broader accounting knowledge, particularly valuable in cases involving self-employment income, business deductions, or complex financial structures. Tax attorneys are critical in situations involving potential litigation, intricate legal questions, or substantial enforcement actions.

Professional representation typically involves:

- Reviewing historical filings and correcting missing returns

- Evaluating income and expenses under IRS standards

- Preparing Form 2848 for authorization

- Presenting financial disclosures through Forms 433-A or 433-F

- Communicating directly with IRS personnel

- Developing plans to prevent or reverse garnishments or levies

- Organizing supporting documents for hardship verification

Representation also affects how cases move through IRS channels. When documentation is accurate and consistent, agents can reduce administrative delays and ensure relief requests reach the correct departments. This is important because the IRS uses multiple systems, including Automated Collection Systems and local revenue officers, each with different procedures.

Nationwide tax relief firms coordinate cases for residents in any state, ensuring uniform access to federal programs. These firms integrate state-specific knowledge when taxpayers owe both federal and state balances. Experienced representatives assess which obligations should be addressed first and how federal relief outcomes may affect state negotiations.

High-quality national services also maintain communication standards, reducing missed deadlines and preventing additional penalties. By managing paperwork, responding to notices, and tracking case progression, representatives reduce the risk of procedural errors or overlooked requirements.

Licensed professionals, therefore, form a central component of nationwide tax relief. Their authority, technical knowledge, and experience with IRS systems increase the likelihood that relief programs are applied correctly and that the taxpayer’s financial circumstances are accurately represented.

Tax Hardship Center (THC) as a Nationwide IRS Tax Relief Provider

Tax Hardship Center operates as a national service entity specializing in IRS tax relief support for individuals facing financial strain or ongoing collection pressure. The organization provides representation across all 50 states, allowing taxpayers with varied economic conditions, employment structures, and debt histories to access federally authorized assistance. The service model emphasizes transparency, structured evaluation, and adherence to IRS rules governing hardship documentation, payment arrangements, and settlement proposals.

The process begins with an eligibility assessment that reviews federal filings, outstanding balances, prior notices, and income patterns. This review identifies whether federal programs such as Offers in Compromise, installment plans, or hardship status could apply. THC representatives then verify compliance, which includes confirming that all required returns have been filed and that income reporting matches available IRS transcripts. Compliance establishes the foundation for relief requests and aligns the taxpayer’s profile with IRS procedural expectations.

A standard THC case sequence includes:

- Evaluation of household income, assets, and expenses

- Retrieval and review of IRS transcripts

- Determination of relief pathways based on financial indicators

- Preparation of disclosure forms, supporting records, and supplementary documentation

- Direct communication with IRS personnel to confirm submission status

- Monitoring of case progress and response deadlines

THC commonly accepts cases involving escalating IRS notices, bank levies, wage garnishments, and long-term tax debt that has accumulated penalties and interest. The organization also assists individuals who have experienced significant life changes, such as medical expenses, job loss, or decreased earning capacity. These conditions often influence eligibility for reduced settlements or temporary collection pauses.

Transparent pricing and communication standards play a functional role within national tax relief services. THC maintains a structured information exchange in which representatives track status changes, document updates, and IRS requests. This helps reduce delays caused by incomplete filings or inconsistent data, particularly in cases requiring expedited action due to pending liens or garnishments.

By combining nationwide reach with federally authorized representation, THC supports individuals who require guidance through complex IRS systems. The organization’s methodology centers on accurate financial analysis, comprehensive documentation, and consistent communication with federal authorities. This approach increases the likelihood that federal relief programs can be applied effectively for taxpayers across different states.

Handling IRS Tax Relief Applications: Documentation, Timelines, and Compliance Requirements

The IRS relies on a structured submission process for tax relief requests, and the accuracy of supporting documents plays a decisive role in whether an application is accepted, delayed, or denied. Relief programs require detailed financial disclosures, consistent records, and verified compliance with all federal filing obligations. These conditions form the backbone of the IRS evaluation process.

Relief applications typically include several core forms. Form 433-A or 433-F provides a complete financial portrait, listing income sources, assets, monthly expenses, investment holdings, and bank balances. Form 656 applies specifically to Offers in Compromise and outlines settlement terms and payment options. The IRS reviews these forms alongside wage statements, bank records, mortgage documents, and medical expense records. Consistency across documents is critical because discrepancies can trigger extended reviews or rejections.

The IRS evaluates categories such as:

- Monthly disposable income

- Asset equity in vehicles, property, savings, and investments

- Household size and allowable living expenses

- Employment type and earning predictability

- Recent financial hardships or medical conditions

Timelines also influence relief outcomes. Some programs require active income verification every 1 to 2 years, especially when taxpayers are placed in hardship status. Installment agreements must be maintained without missed payments, and settlement proposals remain subject to IRS processing windows that can extend several months. Cases routed to Automated Collection Systems usually follow uniform timelines, while cases handled by revenue officers may involve additional interviews or requests for documentation.

Employment type affects the structure of relief evaluations. W-2 wage earners typically show predictable monthly income, while self-employed individuals must provide profit-and-loss statements, business bank records, and documentation of deductible expenses. Gig workers or individuals with irregular earnings must supply additional evidence demonstrating how income fluctuations reduce collectability.

CSED timelines play a strategic role in relief decisions. As the statute of limitations approaches, the IRS evaluates whether collection remains feasible before the period expires. If collection appears unlikely, settlement or hardship status may be more readily approved.

Tax relief applications, therefore, rely on documentation quality, compliance status, and an accurate portrayal of financial conditions. The more complete the submission, the more efficiently the IRS can determine eligibility for federal programs.

Common Questions About Tax Relief USA

Is IRS tax relief available in every state?

IRS relief applies uniformly across the country because the federal government administers it. Residents of all 50 states qualify for the same programs, provided they meet the financial and compliance requirements. Local cost-of-living variations influence allowable expenses, but the underlying relief structure remains consistent.

Who qualifies for nationwide tax relief services?

Eligibility centers on financial hardship, documented income levels, asset valuations, and household expenses. Additional factors include the amount owed, completion of all required tax returns, and the level of enforcement already initiated. Individuals with unpredictable income patterns often require more extensive documentation.

How long does the IRS take to approve relief programs?

Processing times depend on the type of program and the volume of documentation submitted. Offers in Compromise often require several months of review, while installment agreements may be approved more quickly. Cases involving revenue officers may involve extended communication due to interviews or document requests.

Can state tax debts be included with IRS debt relief?

Federal programs apply only to IRS balances, while state debts remain under the jurisdiction of individual Department of Revenue offices. However, a federal relief decision can influence state negotiations by changing the taxpayer’s available income and verified expenses.

When is tax relief denied, and what alternatives exist?

Relief is commonly denied when financial disclosures appear inconsistent, when asset valuations indicate collectability, or when compliance issues remain unresolved. Alternatives include partial payment agreements, temporary hardship status, or structured appeals through the IRS Office of Appeals.

Conclusion

IRS tax relief in the United States operates within a structured federal framework that evaluates financial conditions, household needs, and long-term earning capacity to determine appropriate solutions. These solutions range from settlement programs to payment arrangements and hardship recognitions, each requiring precise documentation and consistent compliance. State revenue systems add complexity by introducing separate rules, timelines, and enforcement procedures, making coordinated federal-state strategies important for individuals with multi-level obligations.

Accurate financial disclosure remains the foundation of all relief outcomes. Income history, asset equity, expense patterns, and prior filings shape the IRS assessment of collectability and influence which programs can be granted. The involvement of licensed professionals strengthens the process by organizing documents, interpreting financial standards, and communicating with the proper IRS departments. Nationwide tax relief providers extend this support to residents of all 50 states, ensuring access to federal programs regardless of regional differences.

When followed correctly, structured relief pathways help stabilize financial situations, prevent the escalation of enforcement actions, and support long-term recovery. By understanding federal rules, state variations, and the role of authorized representation, taxpayers can navigate complex requirements and pursue relief programs that align with their financial realities.