If you bought a home in a newer California subdivision and your property tax bill looks higher than your neighbor’s across town, Mello-Roos is likely the reason. It shows up as a separate line item, it does not follow the same rules as your regular property tax, and nobody seems to explain it clearly before you sign the closing documents.

This article breaks down exactly what Mello-Roos is, why it exists, how much it typically costs, and your options when the bill feels unmanageable.

What is the Mello-Roos Tax in California?

Mello-Roos is a special tax levied on properties located within a Community Facilities District, or CFD. It is not a standard property tax. It is a separate assessment created specifically to fund infrastructure and public services in newer or developing areas of California.

The tax is named after the two California legislators who authored the enabling legislation: Senator Henry Mello and Assemblyman Mike Roos. They passed the Mello-Roos Community Facilities Act in 1982, and CFDs have been a fixture of California real estate ever since.

If your property sits inside a CFD boundary, you pay Mello-Roos. If it does not, you do not. It is geography-based, not income- or value-based, as standard property tax is calculated under Proposition 13.

Where Did Mello-Roos Come From?

Proposition 13, passed in 1978, capped California property taxes at 1% of assessed value and limited annual increases to 2%. It was a meaningful protection for existing homeowners, but created a funding gap for local governments trying to build out infrastructure in new communities.

Mello-Roos was the Legislature’s answer to that gap. By allowing local governments and school districts to form CFDs and issue bonds backed by special taxes on properties within those districts, new developments could be funded up front without straining the general tax base. Residents in the new development pay the tax that funds the infrastructure they use.

The result is that newer subdivisions in California often carry Mello-Roos assessments while older neighborhoods in the same city do not. If you are buying in an area built after the early 1980s, it is worth checking.

What Does Mello-Roos Actually Fund?

Mello-Roos taxes typically pay for one or more of the following:

Roads, sewers, drainage systems, and utilities serve the development. Schools and school facilities. Fire stations and emergency services. Parks and recreational infrastructure. Public libraries.

The key point is that Mello-Roos funds are tied to specific projects within the CFD. The money collected from your property cannot be redirected to the city’s general fund or to infrastructure in a different district. That is also why the tax has a defined end date in most cases.

How Much Is the Mello-Roos Tax?

There is no universal rate. The amount varies significantly by district, by the infrastructure financed, and by the bond amount issued at the time the CFD was formed.

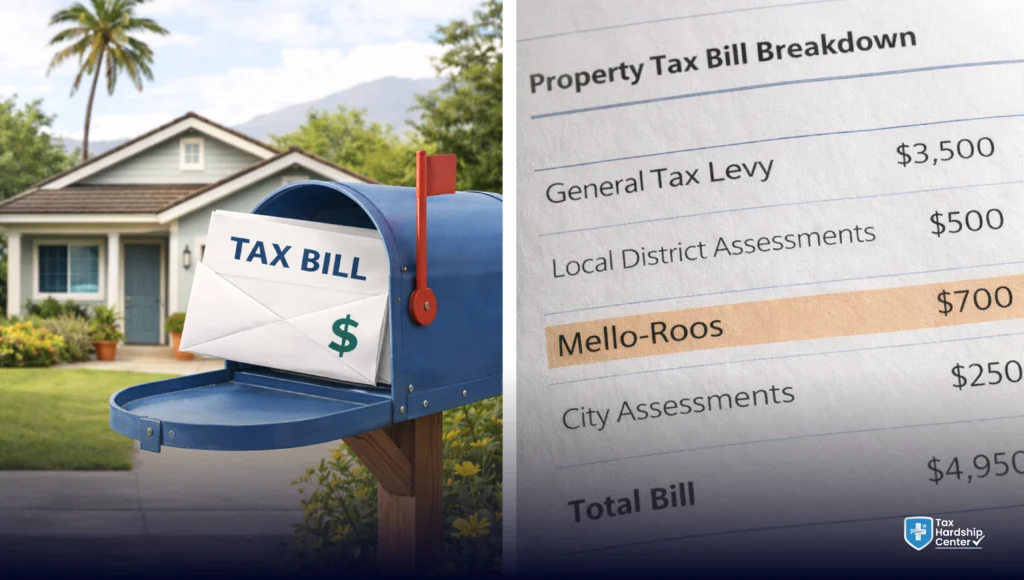

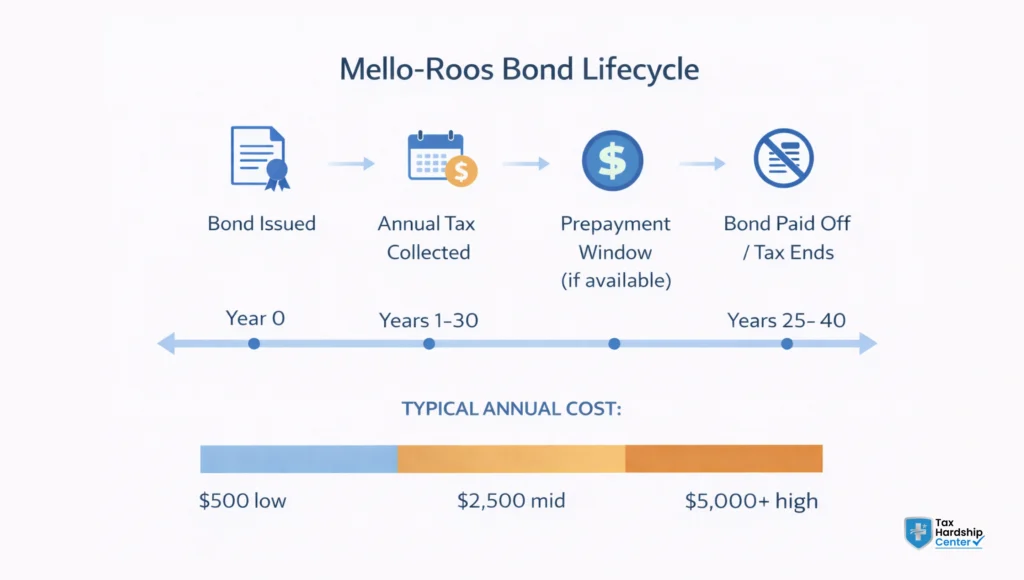

In practice, Mello-Roos assessments in California commonly range from a few hundred dollars per year to well over $5,000 annually on a single residential property. In high-cost areas or districts with substantial school bonds, annual assessments above $3,000 to $4,000 are not unusual.

The California Mello-Roos Community Facilities Act allows the special tax rate to increase by up to 2% per year, which is consistent with the cap on standard property tax increases under Proposition 13. Some CFDs build in annual escalators; others hold the rate flat until the bond is paid off.

Your annual property tax bill will show the Mello-Roos assessment as a separate line item, often labeled with the CFD name. If you are unsure what a specific line item represents, your county tax assessor’s office can explain it.

Why Is My Mello-Roos So High?

Several factors drive high Mello-Roos assessments:

The size of the bond issued when the CFD was formed. Larger infrastructure projects require larger bonds, which require higher annual taxes to service the debt.

The number of parcels sharing the cost. In smaller or lower-density developments, each property carries a larger share of the total bond obligation.

School district facilities bonds. In many California communities, school CFDs are among the largest Mello-Roos components. If the district finances multiple schools or major facility upgrades, the per-parcel cost can be high.

Interest rates at the time of bond issuance. Bonds issued during higher interest rate environments cost more to service over time.

If you are in a newer development in a fast-growing area of California, like the Inland Empire, the Sacramento suburbs, or parts of the Bay Area, a combined Mello-Roos assessment above $3,000 per year is relatively common.

How Long Do You Pay Mello-Roos?

Mello-Roos taxes are not permanent by design. Each CFD has a defined term that corresponds to the bonds it issued. Most Mello-Roos obligations run between 20 and 40 years from the date the bonds were issued, though some districts have shorter terms.

When the bonds are paid off, the special tax ends. At that point, your property tax bill drops by the amount of the Mello-Roos assessment. If you bought into a district that has been collecting the tax for 15 years already, you are closer to the end than someone who bought in a district that issued bonds two years ago.

Some districts allow prepayment of your individual Mello-Roos obligation. This is worth exploring if you plan to hold the property long-term and the math works in your favor. Contact the CFD administrator or your county treasurer-tax collector for the specific prepayment amount and procedure.

Does Mello-Roos Ever Go Away?

Yes, but only when the bonds are fully paid off or the CFD is dissolved. It does not phase out gradually based on your income, your home’s value, or how long you have personally owned the property.

Under California’s Proposition 218, passed in 1996, there is a mechanism for reducing or repealing existing special taxes by a two-thirds vote of property owners within the CFD. This is a high bar and is rarely used in practice, but it exists.

If a CFD was formed with errors in the formation process, there may be grounds to challenge it legally. These challenges are uncommon and typically require legal counsel with specific expertise in California municipal law.

For most homeowners, the honest answer is that Mello-Roos goes away when the bonds are paid off and not before.

Is Mello-Roos Tax Deductible in California?

This is one of the most searched questions on this topic, and the answer is: it depends on how the tax is structured.

Under IRS Topic 503, property taxes are generally deductible when they are ad valorem taxes, meaning they are assessed uniformly based on the value of the property. Mello-Roos is a non-ad valorem special tax. It is not based on assessed value and is not levied uniformly across the general population.

The IRS has generally held that Mello-Roos taxes are not deductible as property taxes on your federal return. California’s Franchise Tax Board (FTB) follows similar guidelines for state income tax purposes.

However, there are some exceptions. If a portion of the Mello-Roos assessment is for a service rather than for capital infrastructure, that portion may be treated differently. If you use the property for business purposes, a portion may be deductible as a business expense. These are fact-specific questions and worth reviewing with a tax professional before filing.

Do not assume the Mello-Roos line on your property tax bill is automatically deductible. Many homeowners make this mistake.

Can You Appeal or Reduce Mello-Roos?

The options are limited but worth knowing.

Standard property tax appeals do not apply to Mello-Roos. Because it is not an ad valorem tax, appealing your assessed property value does not reduce your Mello-Roos obligation.

What you can do: verify that your parcel is correctly classified within the CFD. Errors in parcel classification are uncommon but not unheard of. If your property is being taxed as a larger lot or a different land use category than it actually represents, you may have grounds to request a correction from the CFD administrator.

Prepayment is another option in some districts. Paying off your share of the bond obligation upfront eliminates future annual assessments. The lump-sum amount is calculated by the CFD administrator based on your parcel’s share of the remaining bond debt.

Proposition 218 provides a voter path to repeal, but it requires organizing two-thirds of the district’s property owners, which is difficult in practice.

If you are experiencing financial hardship and your total property tax bill, including Mello-Roos, has become unmanageable, the right path depends on whether the hardship involves California state tax obligations, other tax debt, or the property tax bill itself. Those situations sometimes intersect in ways that are worth understanding before assuming you have no options.

How to Check If a Property Has Mello-Roos Before You Buy

California law requires sellers to disclose Mello-Roos obligations. The Natural Hazard Disclosure report included in most California real estate transactions will note CFD status. Your county tax assessor’s website will also show the CFD boundary and the associated tax amount.

If you are buying new construction, the developer must inform you of any Mello-Roos obligation before you sign a purchase agreement. Read that disclosure carefully. The number in the disclosure is the current year’s assessment; it may increase up to 2% annually.

You can also search your county’s CFD or special assessment district records directly. The Orange County Treasurer, Los Angeles County Assessor, and most major California county websites maintain searchable CFD databases.

What the Tax Hardship Center Can Help With

Mello-Roos itself is administered at the local level and is separate from IRS or California FTB tax obligations. Tax Hardship Center does not handle property tax appeals or Mello-Roos disputes.

Where THC does help is when the overall California tax picture becomes more complicated. If a homeowner carries Mello-Roos debt alongside unpaid California state income tax, IRS back taxes, unfiled returns, or FTB collection activity, those issues often need to be addressed together rather than in isolation.

THC works with California residents to resolve IRS and FTB tax debt through installment agreements, Offers in Compromise, penalty abatement, and Currently Not Collectible status. For homeowners facing multiple layers of tax pressure, the firm provides a straightforward assessment of which issues are most urgent, what realistic resolution options are available, and what each path actually costs before you commit to anything.

If you have questions about IRS or California FTB debt that is compounding alongside your property tax obligations, a free case review is the right starting point.

FAQ

Is it worth buying a house with Mello-Roos?

It comes down to the full cost, how long the bond lasts, and what you are getting in return. A shorter-term obligation in a strong community can feel very different from a long-term, high-cost obligation, so compare everything before deciding.

How long do you pay Mello-Roos in California?

Most Mello-Roos obligations last between 20 and 40 years, depending on the district. The exact remaining term for a property can be checked with the CFD administrator or the county tax office.

How can you avoid paying Mello-Roos?

The only way to avoid it is by buying outside a CFD area. Once you own a property within it, the obligation stays, although some districts allow prepayment to clear future dues.

Is Mello-Roos a tax write-off?

In most cases, it is not tax-deductible. Since it is treated as a special tax rather than a standard property tax, it usually does not qualify for federal deductions.

Do Mello-Roos taxes ever go away?

Yes, they end once the bonds are fully paid. Some districts also offer prepayment options, and in rare cases, early removal can happen through a community vote.

Can you get out of Mello-Roos once you already own the home?

You cannot opt out after purchase since the obligation is tied to the property. Your choices are to prepay if allowed or transfer it to a new buyer when you sell.

How much is Mello-Roos per month?

You can estimate it by dividing the yearly amount by 12. For example, a $3,600 annual charge equals about $300 per month, though it is usually paid through property tax installments rather than monthly.

Conclusion

Mello-Roos is a special tax tied to a specific Community Facilities District, not to your home’s assessed value. It was created in 1982 to fund infrastructure in new California developments after Proposition 13 restricted standard property tax revenue.

The amount varies widely by district. Assessments commonly range from a few hundred to over $5,000 annually. Annual increases are capped at 2% in most districts.

It is not permanently deductible on your federal return. The IRS treats it as a non-ad valorem special tax, which generally falls outside the standard property tax deduction.

Standard property tax appeals do not reduce it. The only realistic paths to reducing or eliminating it before the bond term ends are prepayment (where available) or a two-thirds vote of CFD property owners under Proposition 218.

It does go away when the bonds are paid off. Knowing how many years remain on your district’s bond is one of the most important questions to ask before purchasing.

If you are carrying IRS or California FTB debt alongside your property tax obligations, get a clear picture of all your tax exposure before deciding what to address first. Start with a free case review at Tax Hardship Center.

Key Takeaways

- Mello-Roos is a location-based tax, not tied to your income or property value like standard property taxes.

- It applies only if your property is within a Community Facilities District (CFD).

- The tax primarily funds infrastructure like schools, roads, and public services in newer developments.

- Annual costs can range from a few hundred to over $5,000, depending on the district.

- Most Mello-Roos taxes increase by up to 2% each year.

- The obligation typically lasts between 20 and 40 years, depending on when the bonds were issued.

- It does not automatically reduce or disappear unless the bond is fully paid off.

- Standard property tax appeals do not apply to Mello-Roos.

- Prepayment may be an option in some districts to eliminate future payments.

- It is generally not tax-deductible under federal or California tax rules.

- The only way to avoid Mello-Roos is to buy property outside a CFD area.

- Always check disclosures and CFD details before purchasing property in California.