Seeing “CP503” on an IRS notice can feel like a warning siren, especially if you have already been trying to catch up. The good news is that CP503 is still in the early stages of the collection process, which means you usually have options, and the simplest fixes are often still on the table.

This guide explains what a CP503 IRS notice means, what to do next, and how to set up a payment plan that fits your budget.

What A CP503 IRS Notice Means

CP503 is the IRS’s second reminder that you still owe a balance on one of your tax accounts. The IRS sends it when they have not received your payment or a response to earlier notices.

The notice typically tells you:

- How much you owe (including any added penalties and interest)

- When your payment is due

- How to pay, or how to request a payment plan

- How to contact the IRS if you disagree

Why You Received CP503

In most cases, CP503 happens when:

- You filed a return with a balance due but did not pay in full, or

- The IRS assessed a balance, and earlier reminders were not resolved

The Taxpayer Advocate Service notes that if an initial bill goes unpaid, the IRS generally sends a series of notices, such as CP501, CP503, and CP504, over time until the balance is resolved.

What To Do Next

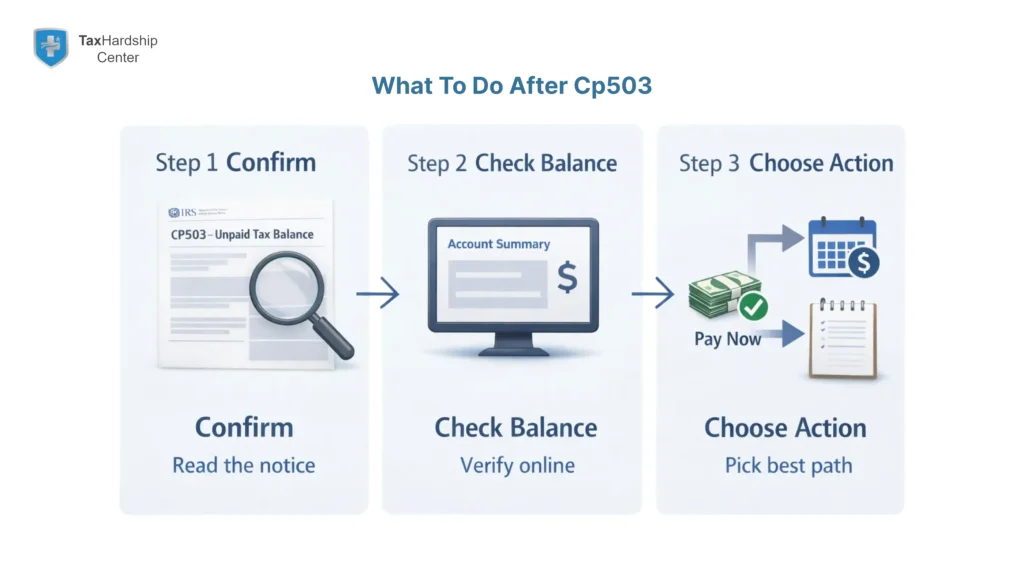

The IRS’s own “What you need to do” section is a solid roadmap. Your goal is to do three things quickly: confirm, decide, and act.

1) Read The Notice Carefully And Confirm The Due Date

The IRS states the notice explains how much you owe, when your payment is due, and your payment options.

2) Confirm The Balance Matches Your Records

If you have an IRS online account, you can review account information and payment details there.

If you disagree, the IRS instructs you to call the toll-free number shown on the notice.

3) Choose Your Best Next Move

Most people fall into one of these paths:

- Pay in full (if you can), by the due date shown on the notice.

- Pay what you can now, then set up a payment plan for the rest. The Taxpayer Advocate Service notes that any payment helps reduce future penalties and interest.

- If you truly disagree with the balance, contact the IRS using the notice instructions before you assume it is “wrong.”

For a broader view of how CP503 fits in the IRS notice sequence, you can reference Tax Hardship Center’s collection timeline and notice guide.

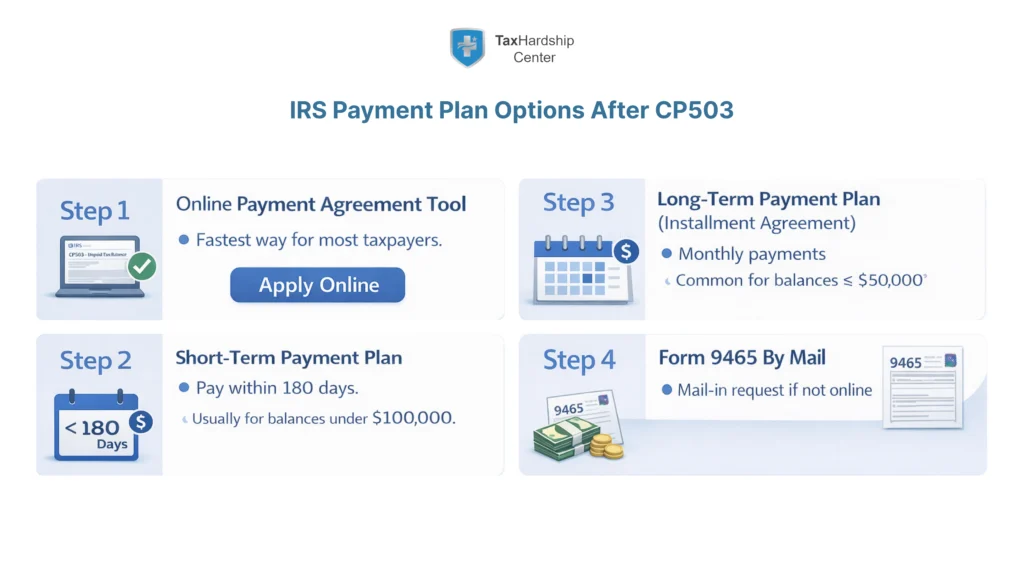

How To Set Up A Payment Plan

If you cannot pay the full amount by the due date, the IRS recommends making a payment plan.

Option 1: Use The IRS Online Payment Agreement Tool

For many taxpayers, this is the fastest route. The IRS explains that once you complete the online application, you get immediate notification of approval.

Before you apply, have:

- Your IRS online account access (you typically need photo identification to create it)

- Your bank routing and account numbers if you want automatic payments

- The balance and tax years involved

Option 2: Choose The Right Plan Type

Here is a quick decision table based on IRS eligibility guidance.

| Plan Type | Best Fit | Basic Eligibility (Common Cases) |

| Short-Term Payment Plan | You can pay within 180 days | Owe less than $100,000 in combined tax, penalties, and interest |

| Long-Term Payment Plan (Installment Agreement) | You need monthly payments | Owe $50,000 or less in combined tax, penalties, and interest, and have filed all required returns |

Practical tip: The IRS encourages direct debit for long-term plans because it reduces the chance of missed payments and default.

Option 3: Request A Plan With Form 9465

If you cannot use the online tool or prefer mail, the IRS allows you to request a monthly installment plan using Form 9465.

The Tax Hardship Center offers a step-by-step guide to Form 9465 and payment plan setup, plus a breakdown of payment plan options.

What Happens If You Ignore CP503

Ignoring CP503 usually makes things more expensive and more stressful.

The IRS states that if you do not pay, make arrangements, or contact them, they may file a Notice of Federal Tax Lien if they have not already.

The Taxpayer Advocate Service also warns that if you do not respond, the IRS may send additional collection notices and may file a federal tax lien or levy.

If the case continues to escalate, the next notice in many situations is CP504, which the IRS describes as a final reminder that it intends to levy on wages, bank accounts, or a state tax refund.

When To Get Professional Help

CP503 is often manageable, but professional help can be valuable when:

- You owe multiple years, or the balance is large enough that you are unsure what option you qualify for

- You are self-employed or have business income that makes monthly budgeting harder to document

- You are worried about a lien filing or a move toward levy notices

- You need a structured plan that prevents default and keeps you compliant going forward

Tax Hardship Center’s related resources on resolution strategies and IRS payment plan options can help you decide the best course before notices escalate.

FAQs

Is CP503 An Audit Notice?

CP503 is a balance-due collection notice. It is a second reminder that you still owe a balance on one of your tax accounts.

How Much Time Do I Have To Respond To CP503?

The IRS states you must pay the entire balance by the due date shown on your notice to avoid additional penalties and interest.

Can I Set Up A Payment Plan From A CP503 Notice?

Yes. The IRS specifically lists making a payment plan as a next step if you cannot pay in full.

What If I Disagree With The Amount On The CP503?

If you disagree, the IRS instructs you to contact them at the toll-free number shown on the notice.

Can I Appeal Before Collection Action Happens?

The IRS CP503 guidance notes that you may be able to request an appeal under the Collection Appeals Program (CAP) before collection action takes place by following the instructions on your notice.

Conclusion

A CP503 IRS notice is a clear signal that your balance is still unresolved, but it is also a stage where you can usually fix the problem with straightforward action. Start by confirming the due date and the balance, then either pay in full or set up a payment plan that you can realistically maintain.

If you ignore CP503, the IRS may move toward liens and more aggressive collection actions, so responding now is typically the easiest and least expensive time to regain control.

Key Takeaways:

- CP503 is the IRS’s second reminder that you still owe a balance, and it lists a due date you should not miss.

- If you cannot pay in full, pay what you can now and set up an IRS payment plan, often through the Online Payment Agreement tool.

- Not responding can lead to a federal tax lien and to stronger notices, such as CP504.

- If your situation is complex or escalating, getting guided help early can prevent bigger enforcement problems later.