If you defaulted on federal student loans and you’re now worried about your paycheck, you should be reading this carefully.

The Department of Education restarted wage garnishment for defaulted federal student loan borrowers in 2025. After years of pauses tied to COVID-era relief, collections are back. Meaning if your loans have been sitting in default while you’ve been hoping the problem would sort itself out, that window has closed.

Here’s what you actually need to know: what percentage of your paycheck can be garnished for student loans, how the math works, what your rights are before it starts, and what you can do to stop it.

What Is Student Loan Wage Garnishment?

Student loan wage garnishment is when a creditor legally takes a portion of your paycheck before you ever see it. Your employer gets an order to withhold a set amount from each paycheck and send it directly toward your debt.

For federal student loans, this process is called Administrative Wage Garnishment (AWG). The Department of Education or its loan servicer can initiate this without first going to court. That last part matters. With most types of debt, a creditor has to sue you and win a judgment before touching your paycheck. With defaulted federal student loans, no lawsuit is required. The federal government has the authority to act unilaterally through AWG.

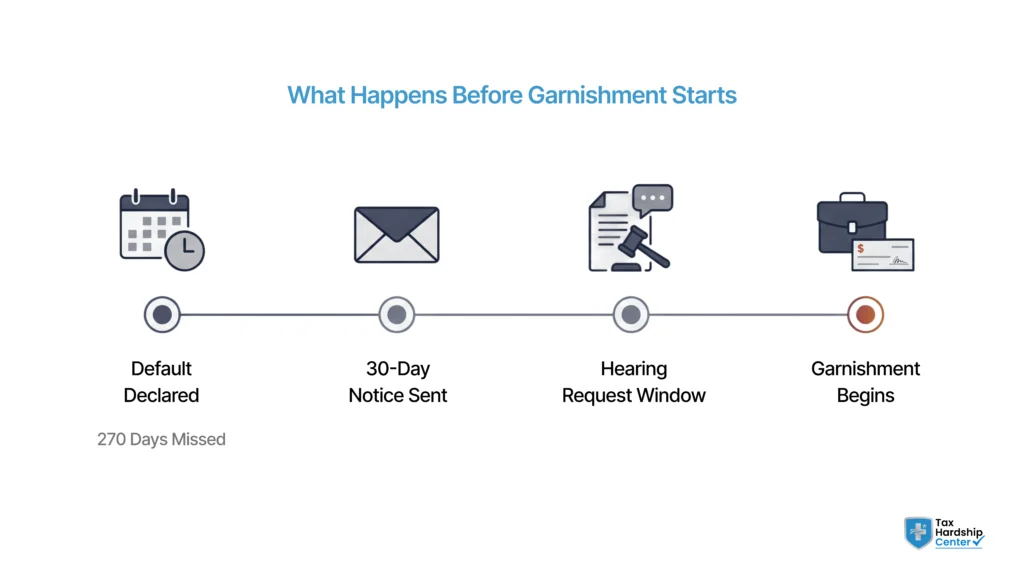

If you are in default, meaning you’ve gone 270 days or more without making a required payment on a federal loan, you are already eligible for this. You don’t need a court notice for it to be real.

What Percentage of Your Paycheck Can Be Garnished for Student Loans?

For federal student loans, the legal limit under Administrative Wage Garnishment is 15% of your disposable income per paycheck. That is set by federal law under 20 U.S.C. § 1095a.

There is one exception: if 30 times the federal minimum wage is less than 15% of your disposable income, then only 30 times the minimum wage can be garnished. As of 2025, the federal minimum wage is $7.25 per hour. Thirty times that is $217.50 per week. Meaning if you earn very little, there is a floor below which garnishment cannot push you.

In practical terms, a person earning $800 in disposable income per week would see up to $120 taken. Someone earning $600 would see up to $90 taken. That math lands hard when rent is due.

For private student loans, the garnishment percentage varies by state. Private lenders must sue you in court and obtain a judgment before garnishing wages. Once they have that judgment, most states allow garnishment of 25% of disposable income, or the amount by which your disposable income exceeds 30 times the federal minimum wage, whichever is less. This is the same federal consumer credit protection formula used for most other types of private debt.

How Is “Disposable Income” Calculated?

Disposable income is not your gross paycheck. It is your gross earnings minus legally required deductions.

Legally required deductions include: federal, state, and local income taxes; Social Security and Medicare (FICA); state unemployment insurance; and required withholdings for state employee retirement plans.

Voluntary deductions, like health insurance premiums, 401(k) contributions, union dues, or wage assignments you chose, do not reduce your disposable income for garnishment purposes.

Here’s a simple example. If your gross biweekly paycheck is $2,000 and your legally required deductions total $400, your disposable income is $1,600. At 15%, the maximum garnishment would be $240 per pay period.

This calculation is important because creditors sometimes present the maximum as if it is automatic. In practice, if your disposable income is low enough, the 30x minimum wage protection may apply, reducing the amount taken further.

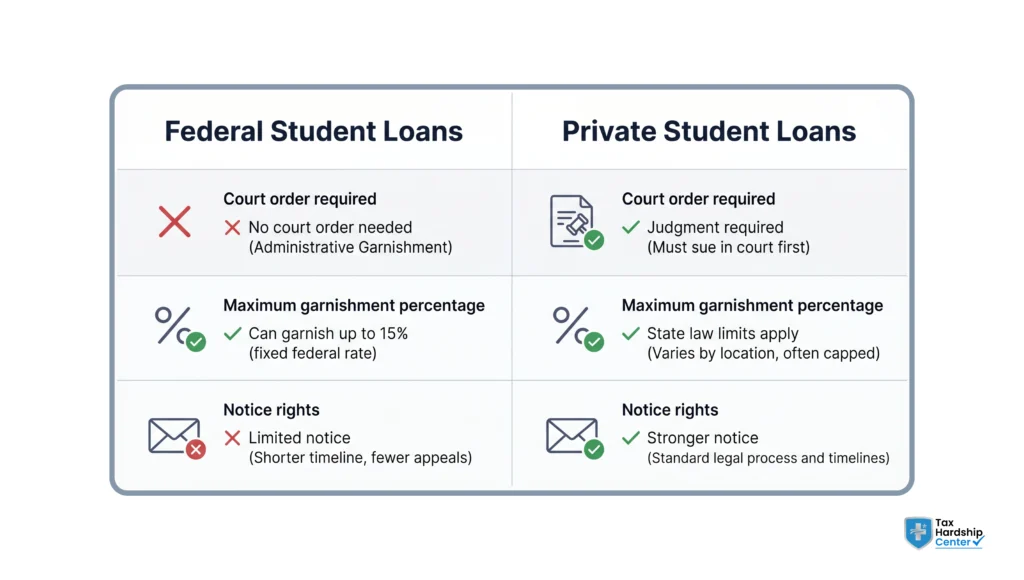

Federal vs. Private Student Loan Garnishment: Key Differences

The rules vary depending on who holds your loan.

Federal student loans:

- No court order required. The Department of Education can initiate AWG directly.

- You must receive a 30-day written notice before garnishment begins.

- Maximum garnishment: 15% of disposable income.

- You have the right to request a hearing to dispute the garnishment or claim hardship before it starts.

- Rehabilitation or consolidation can stop garnishment if completed correctly.

Private student loans:

- The lender must sue you and obtain a court judgment first.

- The amount that can be garnished follows your state’s wage garnishment law, typically the same formula as consumer debt: 25% of disposable income or 30x minimum wage threshold, whichever is less.

- Once a judgment is entered, the lender can also pursue bank levies and liens in addition to wage garnishment.

Private loan garnishment requires more steps, but once a judgment is in place, the lender has broad tools. Do not assume that because a loan is private, nothing can happen to your paycheck.

Your Rights Before Garnishment Starts

For federal student loans, you have procedural rights before garnishment can begin. Understanding these is how people stop garnishment before it ever touches their paycheck.

The Department of Education or its servicer is required to send you a written notice at least 30 days before garnishment begins. This notice will include: the nature and amount of the debt, the agency’s intention to collect through wage garnishment, and your right to request a hearing.

You can request a hearing in writing. There are two types. The first is a hearing to dispute whether you actually owe the debt, whether the amount is correct, or whether you’ve already been subject to the maximum amount of garnishment the law allows. The second is a hearing to claim financial hardship, arguing that garnishment would cause serious financial harm to you and your dependents.

If you submit a written hearing request before the 30-day notice period expires, garnishment cannot begin until the hearing is completed. This is a genuine window to stop the process. Once the 30 days pass without a request, that window closes.

Keep in mind that a hardship hearing does not eliminate the debt. It may reduce the garnishment percentage or temporarily pause it, but the balance remains unless you pursue a broader resolution strategy.

For more on how the notice and hearing process works across different IRS and federal collection situations, the Tax Hardship Center’s tax relief services page has additional context on navigating federal collection actions.

How to Stop Student Loan Wage Garnishment

There are four realistic paths to stop federal student loan garnishment. None of them is instant. All of them require action.

1. Request a hearing before garnishment starts. As covered above, a written hearing request submitted within the 30-day notice window pauses garnishment. Use this time to explore your other options, not just to delay.

2. Loan rehabilitation. Rehabilitation requires you to make 9 voluntary, reasonable, and affordable monthly payments within 10 consecutive months. The payments are based on your income, so they can be lower than you expect. Once you complete rehabilitation, your loan is removed from default status, and garnishment stops. You can only rehabilitate a loan once.

3. Loan consolidation. You can consolidate defaulted loans into a Direct Consolidation Loan. If you do this correctly and agree to repay under an income-driven repayment (IDR) plan, your loans will exit default, and garnishment will stop. Consolidation is faster than rehabilitation, but it does not remove the default notation from your credit history the same way rehabilitation does.

4. Pay the balance in full. For some borrowers, especially those with smaller balances, this is the cleanest resolution. But for most people reading this, a full payoff is not on the table. If that’s where you are, rehabilitation or consolidation is the realistic path.

One thing to know: there is no statute of limitations on federal student loan collection, unlike private debt. The federal government can pursue federal student loan balances indefinitely. Waiting for the problem to expire is not a strategy.

For related information on stopping wage garnishment from IRS tax debt, the Wage garnishment guide at Tax Hardship Center walks through the IRS-specific garnishment rules and exemptions.

Can Student Loans Garnish Social Security or SSDI?

Yes, for federal student loans. The Treasury Offset Program (TOP) allows the federal government to intercept Social Security retirement and disability (SSDI) payments for defaulted federal student loan debt. The maximum offset is 15% of your monthly benefit, and your monthly payment cannot be reduced below $750.

Supplemental Security Income (SSI), however, is protected. SSI cannot be garnished or offset for student loan debt.

Private student loans cannot garnish Social Security. Private lenders would need a court judgment, and Social Security benefits are generally exempt from garnishment by private creditors under federal law.

How Tax Hardship Center Can Help

Student loan garnishment and IRS tax debt often land on the same desk. If you’re dealing with defaulted federal student loans, there is a real chance you also have unfiled returns, back taxes, or IRS collection pressure running alongside the student loan situation.

Tax Hardship Center works with individuals and small business owners who are carrying federal and state tax debt, including situations where multiple collection problems are active at once. The firm’s tax debt relief services are built around honest qualification, meaning the firm will tell you what resolution options you realistically qualify for before you pay for anything.

If your situation involves both student loan garnishment and IRS tax debt, the two need to be addressed in coordination. Resolving one without addressing the other often leaves the same income exposed to a different garnishment the following month.

For a free case review with a tax specialist, visit taxhardshipcenter.com or call to speak with someone today.

FAQ

Q: Can student loans garnish more than 15% of my paycheck?

For federal student loans under Administrative Wage Garnishment, the legal maximum is 15% of disposable income. However, if you also have a tax levy or other garnishment running simultaneously, total garnishment from all sources can exceed 15% of your paycheck, subject to separate caps per garnishment type.

Q: How much notice do I get before federal student loan garnishment starts?

You are entitled to at least 30 days’ written notice before Administrative Wage Garnishment begins. If you submit a written hearing request within that 30-day window, garnishment cannot start until the hearing is resolved.

Q: Can student loan garnishment happen if I’m self-employed?

Traditional wage garnishment applies to employees with a regular employer payroll. If you’re self-employed, the federal government has other collection tools available, including bank levies and tax refund offsets through the Treasury Offset Program. AWG, in the standard sense, requires an employer to withhold from a paycheck.

Q: Does student loan garnishment affect my credit score?

The garnishment itself is not a separate credit event, but the default that triggers garnishment will already be on your credit report. Resolving the default through rehabilitation can eventually remove the default notation; consolidation does not.

Q: Can private student loans garnish my wages without going to court?

No. Private student loan lenders must obtain a court judgment before they can garnish wages. This is a meaningful difference from federal loans, where no lawsuit is required.

Q: What is a hardship hearing for student loan garnishment?

It is a formal process where you can argue that the garnishment amount would cause severe financial hardship to you and your dependents. If approved, it may reduce the garnishment percentage or temporarily pause it. The underlying debt does not go away through a hardship hearing.

Q: Will student loan garnishment stop if I file for bankruptcy?

Filing bankruptcy creates an automatic stay that temporarily halts most collection activity, including wage garnishment. However, student loan debt is rarely dischargeable in bankruptcy unless you can prove undue hardship under a demanding legal standard. The stay is temporary unless the debt is discharged.

Conclusion

Here’s the truth nobody tells you when you’re staring at a garnishment notice.

The problem does not get smaller by waiting. It gets more expensive, more urgent, and harder to stop.

If your federal student loans are in default, you are not out of options. But the window to act before your paycheck gets touched is genuinely narrow. Thirty days from that notice. That is it.

Rehabilitation works. Consolidation works. A hardship hearing can buy you time. But none of it works if you do nothing.

And if you are carrying student loan pressure alongside IRS tax debt, unfiled returns, or state collection notices at the same time, you cannot afford to solve one and ignore the other. Income protected from one garnishment remains exposed to the next.

That is the situation most people are actually in. And that is exactly what Tax Hardship Center helps untangle.

Key Takeaways

- Federal student loans can garnish up to 15% of your disposable income per paycheck, with no court order required

- You have a 30-day window after your garnishment notice to request a hearing and pause the process

- Loan rehabilitation (9 payments over 10 months) and loan consolidation are the two main paths to exit default and stop garnishment

- Private student loans require a court judgment before wages can be touched, and follow your state’s garnishment limits

- Social Security and SSDI can be offset for federal student loans, but SSI cannot

- If you have both student loan debt and IRS tax debt active at the same time, they need to be resolved together, not separately

- Tax Hardship Center’s wage garnishment services and tax debt relief options are built for exactly this situation

Get a free case review today. Speak to a specialist who will tell you what is realistic before you pay for anything.