You got a notice. Maybe more than one. You are now wondering how close you actually are to seeing a chunk of your paycheck disappear.

Here is the honest answer: the IRS does not just wake up one day and decide to garnish your wages. There is a process. There are required steps. And at almost every step, there is a window to act.

But that window is not infinite. And once it closes, your employer receives a levy notice, and the IRS starts automatically deducting money from every paycheck until the debt is paid or something changes.

This article walks through the actual timeline, what each notice means, how much the IRS can actually take, and what options are available right now to stop or prevent garnishment.

What Is IRS Wage Garnishment?

IRS wage garnishment is when the IRS sends a legal order directly to your employer to take a portion of your paycheck and send it to them instead. They call this a wage levy.

The authority comes from Internal Revenue Code Section 6331. It allows the IRS to collect unpaid tax debt by taking wages, salaries, commissions, and other income. This is not like a regular creditor garnishment.

A normal creditor has to sue you, win a judgment, and then go back to court to garnish your wages.

The IRS does not. They already have the legal power. No court order needed.

Once your employer gets that notice, they have to comply. There is no choice on their end. And realistically, none of yours either, unless you act before it starts or move quickly right after.

The IRS Garnishment Timeline: Step by Step

The IRS does not jump straight to garnishment. There is a sequence.

If you understand where you are in it, you understand how much time you actually have.

Step 1: Tax assessment and initial bill

- You file a return with a balance due, or the IRS files one on your behalf.

- That amount becomes an assessed tax debt.

- Then comes the first bill. Usually a CP14 notice. This is the IRS formally asking for payment.

Step 2: Follow-up notices

- No response or no payment, the notices escalate.

- CP501. CP503. CP504.

- Each one gets more urgent. Each one makes it clearer that enforcement is coming.

Step 3: Final Notice of Intent to Levy

- This is the one that matters.

- The IRS must send a Final Notice of Intent to Levy and Notice of Your Right to a Hearing at least 30 days before taking action.

- You will see this as an LT11 or Letter 1058.

- If you have this in hand, the clock is already ticking.

- You have 30 days before the IRS can move forward with garnishment.

- This is your cleanest window to stop it.

Step 4: Collection Due Process hearing request

- Within those 30 days, you can file Form 12153.

- This requests a Collection Due Process hearing.

- Once filed, the levy action pauses while the hearing is pending.

- Important detail. This does not erase the debt.

- It buys you time. That is the value.

Step 5: Wage levy sent to your employer

- No action taken, the 30 days pass, the IRS moves.

- They send the levy directly to your employer.

- Your employer gets one pay cycle to process it.

- After that, your paycheck is reduced, and the garnishment continues until the debt is resolved or you intervene.

How Many Notices Does the IRS Send Before Garnishing Wages?

Most people receive four to five notices before garnishment actually starts. Here is the typical sequence:

- CP14: Balance due notice

- CP501: First reminder, balance still owed

- CP503: Second reminder, more urgent

- CP504: Final notice before levy action (certified mail, can trigger state refund seizure)

- LT11 or Letter 1058: Final Notice of Intent to Levy (triggers the 30-day countdown)

The entire notice sequence can take anywhere from a few months to over a year, depending on your case. The IRS does not always send every notice in rapid succession. But once that LT11 lands, the timeline becomes very specific.

Important: If you moved and did not update your address with the IRS, notices may have been sent to your last known address. The IRS considers proper service completed even if you never opened the letters.

How Long Does the IRS Wait Before Garnishing?

From the date of that final LT11 or Letter 1058, the IRS must wait a minimum of 30 days before issuing a wage levy to your employer.

In practice, it can take longer. The IRS has a large caseload and does not always move at maximum speed. But waiting and hoping is not a strategy. Some people receive that notice and see garnishment start within five to six weeks. Others have a few extra months. You cannot count on extra time.

If you have an assigned revenue officer on your case, the timeline often moves faster. Revenue officers have direct enforcement authority and actively pursue collection.

The bottom line: 30 days is the legal minimum. Do not treat it as a grace period to think things over.

How Much Can the IRS Take from Your Paycheck?

The IRS does not take your entire paycheck.

They use a formula based on your filing status, pay frequency, and the number of exemptions you claim.

Here is how it works.

The IRS lets you keep a minimum exempt amount. This comes from IRS Publication 1494 tables. Everything above that amount can be taken simply.

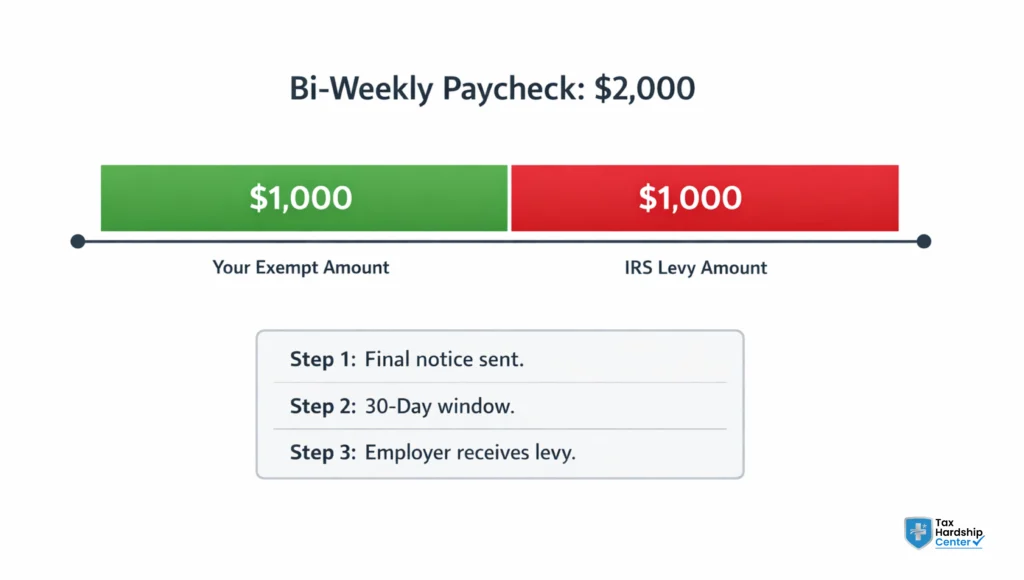

Example

Say you are single, paid biweekly, and claim one exemption.

Your exempt amount might be around $1,000 per pay period.

If your take-home pay is $2,000, the IRS can take roughly $1,000 every two weeks.

That is not a small deduction. And it does not happen once. It keeps happening every pay cycle until the debt is cleared or the levy is released.

What affects how much they take

Three main factors decide the number:

- Your filing status

- Number of dependents you claim

- How often do you get paid

These directly change your exempt amount. A lower exempt amount means more money goes to the IRS. A higher exempt amount means you keep more.

One move that actually helps

Form 668 W matters more than most people think. This is your Statement of Exemptions.

If you fill it out incorrectly or leave out dependents, you are giving the IRS permission to take more than they should. If your situation has changed or you made a mistake, submit an updated form to your employer. Done right, this can reduce how much gets taken from every paycheck. Not a complete fix. But it gives you breathing room while you figure out the bigger solution.

Can the IRS Garnish 100% of Your Wages?

Short answer. No, not completely. But close enough that it can feel like it. The IRS can take far more than a typical creditor. They are not bound by standard wage garnishment caps.

Still, they are required to leave you with a minimum exempt amount. That number is not meant to be comfortable. It is the bare minimum the IRS believes you need for basic living.

Which means if your income is higher and you have claimed fewer exemptions, the portion they take can be significant. In some cases, it can be most of your paycheck.

When does it become unsustainable? If the levy leaves you unable to cover essentials like rent, utilities, and food, you are not stuck. There is a formal way to push back. You can request the Currently Not Collectible (CNC) status. This falls under Internal Revenue Code Section 6343. To qualify, you need to show real financial hardship.

That means documenting your income, expenses, and overall situation clearly. If approved, the IRS can release the levy. Important to understand. This does not erase your debt. It pauses collection because you genuinely cannot afford to pay right now. And in situations where the garnishment is cutting too deep, that pause can make all the difference.

How to Stop IRS Wage Garnishment

Here is what actually works, in order of speed.

Request a Collection Due Process hearing (fastest if you just got the LT11). File Form 12153 within 30 days of the LT11 notice. This legally pauses the levy while your hearing is pending. You still owe the debt, but the IRS cannot proceed with garnishment while the CDP process is active.

Set up an installment agreement. If you cannot pay the debt in full, a formal installment agreement with the IRS generally results in the levy being released. The IRS wants consistent payment. A signed agreement gives them that without needing enforcement. You can apply through IRS.gov or with the help of a tax professional.

Apply for an Offer in Compromise. If you genuinely cannot pay the full amount and your financial situation supports it, an Offer in Compromise (OIC) lets you settle your debt for less than the full amount owed. A pending OIC application also pauses collection activity. Not everyone qualifies, and the IRS rejects many OIC applications. Honest qualification matters here.

Request Currently Not Collectible status. If you truly cannot pay anything right now without it causing severe hardship, CNC status pauses collection activity until your financial situation improves. This does not forgive the debt, but it stops the levy.

File any missing returns. The IRS typically does not negotiate while returns remain unfiled. If you have missing returns, getting current is often the first step toward releasing leverage.

Work with a tax resolution professional. A properly credentialed representative (an enrolled agent, CPA, or tax attorney) can contact the IRS on your behalf, request levy releases, and negotiate directly. In urgent situations, this can make a significant difference in how quickly action is taken.

How Tax Hardship Center Can Help

At Tax Hardship Center, we work with people who are facing exactly this situation. Some come to us before the levy starts. Some come after the first paycheck is short. Either way, there are options.

We do not promise specific settlement amounts or guaranteed outcomes. What we do is give you an honest picture of where your case stands, what the IRS is likely to do next, and what relief options you actually qualify for based on your specific financial situation.

If you have received an LT11 or Letter 1058, or if your employer has already been notified, the most useful thing you can do right now is get a clear read on your situation before the next paycheck cycle.

We offer free case reviews. No commitment, no pressure to sign up for anything. Just an honest conversation about your specific case and what comes next.

FAQ

How long does it take for the IRS to garnish wages after a final notice?

The IRS must wait at least 30 days after the final notice before taking action. In most cases, garnishment can begin within five to six weeks, depending on the situation.

How many IRS notices come before wage garnishment?

Most people receive four to five notices before things escalate to garnishment. The final notice is what triggers the 30-day countdown to action.

Can I stop garnishment after it has already started?

Yes, it can be stopped through options like payment plans or settlements. Even after it starts, there are ways to pause or release the levy.

What if I never received the notices?

The IRS sends notices to your last address on file, even if you have moved. If you didn’t receive them, you can still raise this during an appeal or hearing.

Can the IRS garnish Social Security or pension income?

Yes, the IRS can levy a portion of Social Security and certain retirement income. This is something most other creditors are not allowed to do.

Will my employer find out I owe back taxes?

Yes, if garnishment begins, your employer will be notified directly. The only way to avoid that is to resolve the issue before it reaches that stage.

Does filing for bankruptcy stop IRS wage garnishment?

Filing for bankruptcy can pause IRS collection actions, including garnishment. But the tax debt may still remain, depending on the case.

Conclusion

The IRS follows a predictable sequence before garnishing wages. The final step in that sequence, the LT11 or Letter 1058, gives you exactly 30 days to act before they contact your employer.

Four to five notices typically precede that final one. If you have been receiving IRS mail and not responding, you may be closer to garnishment than you realize.

Once garnishment starts, it continues automatically in every pay period. The IRS uses a formula from Publication 1494 to determine how much they take, and there is no guarantee that the formula leaves you with enough to cover your monthly obligations.

The options to stop or prevent garnishment are real: installment agreements, OIC applications, CDP hearing requests, and CNC status are all legitimate tools. But each one requires action, documentation, and in most cases, a clear-eyed assessment of your financial situation.

If you are reading this because a notice arrived or a paycheck came up short, that is the moment to get an honest read on your situation, not a sales pitch, but an actual assessment of what your options are right now. Speak to a tax specialist today.