If you owe the IRS more than you can realistically pay, an Offer in Compromise can sound like the perfect solution. It can be, but only when the numbers and rules line up.

An Offer in Compromise lets you settle tax debt for less than the full amount owed, and the IRS generally approves it only when your offer reflects the most it can expect to collect within a reasonable period of time.

This guide explains who qualifies, how to apply successfully, and what to avoid to ensure your application is not delayed, returned, or denied.

What An IRS Offer In Compromise Is

An Offer in Compromise (often shortened to OIC) is an agreement that can settle your tax debt for less than the full amount you owe. The IRS describes it as a legitimate option when you cannot pay your full liability, or paying in full would create financial hardship.

Before applying, the IRS recommends exploring other payment options because the OIC program is not for everyone.

Who Qualifies For An Offer In Compromise IRS

Basic Eligibility Requirements

The IRS lists the core eligibility requirements for applying. You are generally eligible to apply if you:

- Filed all required tax returns and made required estimated payments.

- Are not in an open bankruptcy proceeding.

- Have a valid extension for a current-year return if applying for the current year.

- If you are an employer, make required tax deposits for the current and past two quarters before applying.

If the IRS cannot process your offer because you are not eligible, it will return your application and application fee, and it may apply any offer payment you included to your balance due.

Low-Income Certification

If you meet the low-income certification guidelines, the IRS says you do not have to send the application fee or initial payment, and you do not have to make monthly installments while the IRS reviews your offer.

This matters because many applicants accidentally send money they did not need to, and those payments are generally applied to their tax debt rather than returned.

The Three IRS Reasons An OIC Can Be Accepted

The IRS recognizes three grounds for accepting an offer:

Doubt As To Liability

There is a genuine dispute about whether the tax is correct under the law. The IRS notes that this type typically uses Form 656-L (not the standard Form 656 package).

Doubt As To Collectibility

You agree you owe the tax, but you cannot pay the full amount through income and assets. This is the most common OIC category.

Effective Tax Administration

You owe the tax and the IRS could collect it, but requiring payment in full would create economic hardship or be unfair due to exceptional circumstances.

How The IRS Evaluates Your Offer Amount

The IRS explains that it considers your unique facts and circumstances, including:

- Ability to pay

- Income

- Expenses

- Asset equity

The practical takeaway is simple: your offer is not a random number. It needs to match what the IRS believes it can reasonably collect, based on your documented financial picture.

A good “first filter” is the IRS Offer in Compromise Pre-Qualifier tool, which helps you estimate whether an OIC may be viable before you build the full package.

How To Apply Successfully (Step By Step)

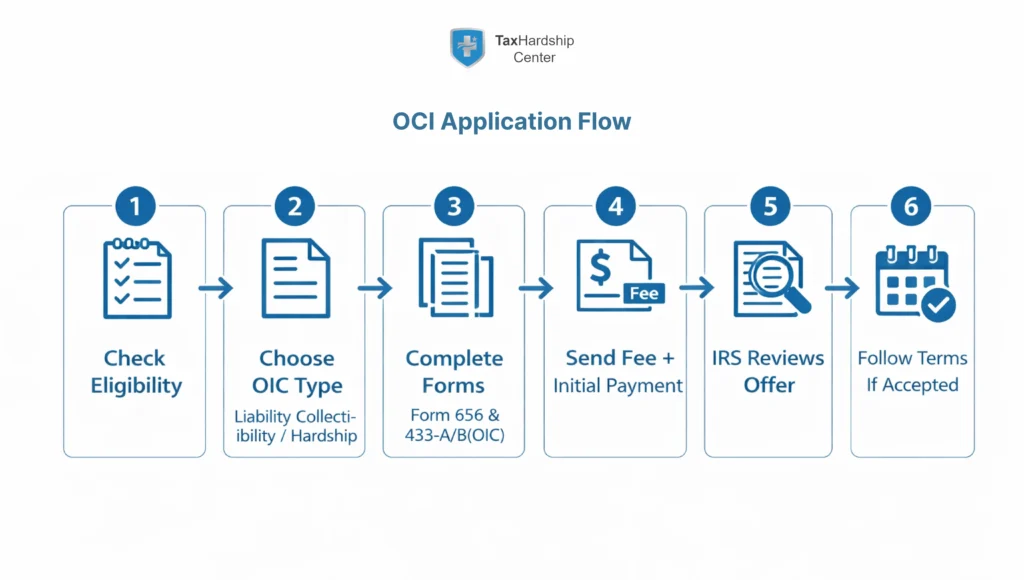

Step 1: Use The Pre-Qualifier Before You Spend Time On Forms

Start with the IRS pre-qualifier to see if an offer is worth pursuing. The IRS points taxpayers to it as the starting point for eligibility and the preliminary proposal.

Step 2: Choose The Correct Application Path

- For doubt as to collectibility or effective tax administration, the IRS directs applicants to use Form 656-B (the Offer in Compromise booklet), which includes Form 656 and the financial statement forms.

- For doubt as to liability, the IRS directs you to use Form 656-L and provide a written statement and supporting evidence for why the assessed tax is incorrect.

Step 3: Build A Clean Document Package

The IRS lists the standard application components as:

- Form 433-A (OIC) for individuals or Form 433-B (OIC) for businesses, plus required documentation

- Form 656

- The application fee

- The initial payment

Step 4: Understand Fees And Initial Payment Rules

The IRS explains the standard submission includes a $205 application fee and an initial payment for each Form 656.

The IRS also outlines payment options:

- Lump sum: submit 20 percent of the total offer amount with your application, then pay the remainder in five or fewer payments after acceptance.

- Periodic payment: submit your initial payment with your application, then continue making monthly installments while the IRS considers your offer.

If you meet low-income certification, the IRS says these payments and fee requirements are waived during consideration.

Step 5: Submit The Application The Right Way

The IRS says you can submit the application package by mailing it to the appropriate site listed in Form 656-B, and it also notes you may be able to file your offer online through your Individual Online Account.

Step 6: If You Are On An Installment Agreement

The Form 656-B booklet notes that if you currently have an approved installment agreement, you generally will not be required to make those installment agreement payments while the IRS considers your offer.

What Happens After You Apply

How Long It Can Take

The IRS OIC FAQs state the complete offer investigation can take up to 24 months, depending on inventory levels and case complexity.

What The IRS Will Do Next

After receiving your Form 656 package and supporting documentation, the IRS reviews it to confirm it can be processed. If it cannot be processed, it may be returned, and initial offer payments are generally applied to your tax liability.

Practical tip: during this time, staying compliant matters. New unpaid taxes or missing filings can derail a resolution path quickly.

If Your Offer Is Accepted, Rejected, Or Returned

If Accepted

The IRS states that after acceptance:

- You must pay the offer amount under the terms of the agreement.

- The IRS will keep any tax refund due through the date it accepts your offer (this condition does not apply to doubt as to liability offers only).

- You must remain compliant with filing and payment obligations for five years after acceptance, or your offer can default.

If Rejected

The IRS states you typically have 30 days from the rejection letter date to appeal, following the instructions in the letter.

If Returned

If the IRS returns your offer as non-processable or for another reason, the practical impact is that you have lost time, and you may have lost money if you did not qualify for a waiver. That is why “application quality” matters as much as eligibility.

Common Mistakes That Get Offers Denied Or Delayed

- Applying before you file all required returns or make required estimated payments.

- Using the wrong form type, such as filing Form 656-L when the real issue is inability to pay, not liability.

- Missing documentation for income, expenses, or assets, which prevents the IRS from verifying your financial picture.

- Sending an application fee or initial payments when you qualify for low-income certification, and expecting them to be refunded.

- Picking a payment option, then failing to make required ongoing payments under that option during review.

- Treating OIC as the only option, when the IRS recommends exploring other payment options first.

When To Get Professional Help (IRS Representation)

An Offer in Compromise is paperwork-heavy and timing-sensitive. It is also easy to misunderstand, especially when business income, multiple tax years, or disputed balances are involved.

Professional help is most valuable when:

- You are unsure which OIC ground applies, liability vs collectibility vs hardship.

- Your financial documentation is complex, or you expect the IRS to challenge valuations.

- You want help assembling a clean application package to avoid returns and delays.

Tax Hardship Center’s OIC service and related guides are built for this stage, especially when you want a realistic qualification review and a correctly-prepared submission.

FAQs

Is An Offer In Compromise A Real IRS Program

Yes. The IRS describes an Offer in Compromise as a program that may allow qualifying taxpayers to settle for less than the full amount owed when they cannot pay in full or paying would create financial hardship.

What Are The Three Types Of Offer In Compromise

The IRS recognizes offers based on doubt as to liability, doubt as to collectibility, and effective tax administration.

What Forms Do I Need To Apply

For most offers (collectibility or effective tax administration), the IRS directs you to use Form 656-B, which includes Form 656 and the required financial statement forms. For doubt as to liability, the IRS directs you to use Form 656-L.

How Much Is The IRS Offer In Compromise Application Fee

The IRS lists a $205 application fee for standard OIC submissions, unless you meet low-income certification guidelines.

How Long Does The IRS Take To Review An Offer In Compromise

The IRS states a complete offer investigation can take up to 24 months, depending on case complexity and inventory levels.

Conclusion

An Offer in Compromise can be a powerful way to resolve tax debt, but success depends on eligibility, documentation, and submitting the right package the first time. Start by confirming you meet the IRS eligibility rules, use the pre-qualifier to avoid wasted effort, then build a complete Form 656-B submission with the correct payments or low-income waiver if you qualify.

Key Takeaways:

- The IRS generally approves an OIC when your offer reflects what it can reasonably collect, based on income, expenses, and asset equity.

- You must meet eligibility requirements, including being current on required filings and payments, and not being in open bankruptcy.

- Most applicants use Form 656-B with Form 656 and Form 433-A(OIC) or 433-B(OIC). Doubt as to liability uses Form 656-L.

- Standard applications include a $205 fee and an initial payment, unless you qualify for low-income certification.

- If accepted, you must follow the terms and remain compliant for five years to avoid default.