Short answer: yes, in most cases you can still buy a house even if you owe the IRS. The longer answer depends on how much you owe, whether the IRS has filed a tax lien, and whether you have a plan in place that a lender can actually see and verify.

Here is what really matters to a lender, what can slow you down, and what to fix before you start house hunting.

Table of Contents

- Does Owning The IRS Automatically Disqualify You From A Mortgage?

- The Real Difference Between Owing Taxes And Having A Tax Lien

- How Different Loan Types Handle IRS Debt

- What Lenders Actually See When They Pull Your File

- The IRS Payment Plan That Can Make Or Break Your Approval

- Mistakes That Quietly Tank Loan Applications

- What To Do Before You Talk To A Lender

- FAQs

- Key Takeaways

Does Owing The IRS Automatically Disqualify You From A Mortgage?

No. Owing the IRS money does not automatically disqualify you from buying a house. What matters to a lender is not the existence of the debt; it is whether that debt is documented, manageable, and not actively threatening their collateral (your future home).

A lot of people assume that any IRS balance is a dealbreaker. It is not. Plenty of buyers close on homes every year while still working through a balance with the IRS. The thing that actually causes problems is an unresolved, undocumented debt with no plan attached, especially once it turns into a federal tax lien.

The Real Difference Between Owing Taxes And Having A Tax Lien

This is the part most people mix up, and it is the single biggest factor in this whole conversation.

Owing taxes means you have a balance with the IRS. That alone does not show up as a red flag on your credit report and does not automatically block a loan.

A federal tax lien is different. This is a legal claim the IRS files against your property when a tax debt goes unpaid long enough. A lien attaches to assets you currently own, and depending on timing, it can also create complications for a property you are trying to buy, because it affects your overall financial picture and can show up during underwriting.

If you are not sure whether your account has reached lien status, that is something worth checking before you go any further, since the IRS notice timeline usually gives you a window of warning notices before a lien is actually filed.

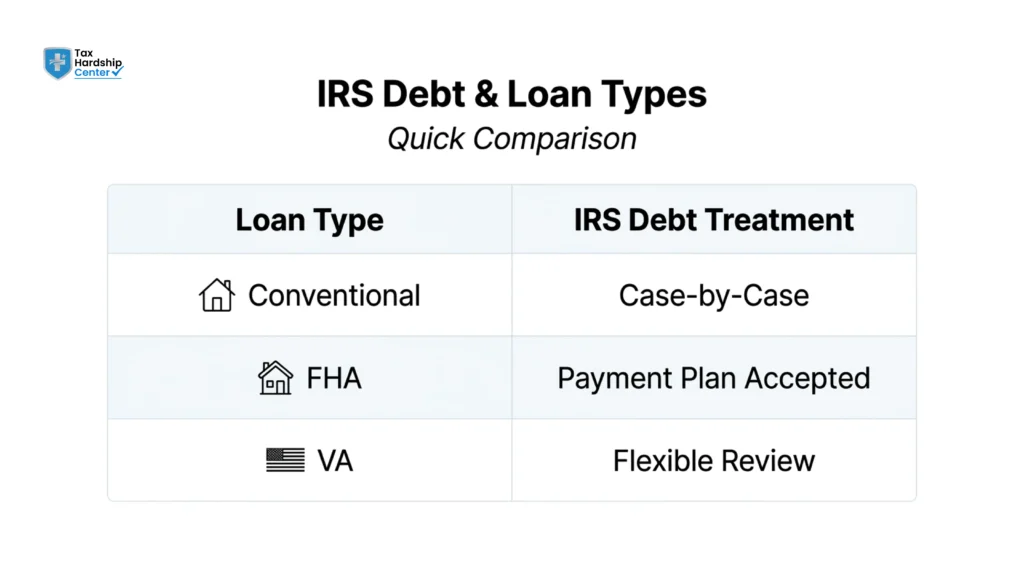

How Different Loan Types Handle IRS Debt

Different loan programs treat IRS debt differently, and this is where many buyers are surprised.

Conventional loans: Generally, an outstanding IRS debt without a lien is treated like any other debt; it factors into your debt-to-income ratio. If a lien has been filed, most conventional lenders will want it resolved or subordinated before closing.

FHA loans: FHA is actually more flexible here than people expect. If you have an IRS payment plan in place, with a documented history of on-time payments (often three months or more), FHA lenders can often count the monthly payment in your debt-to-income ratio rather than requiring the full balance be paid off.

VA loans: Similar flexibility applies, with the IRS payment plan and payment history being key documentation.

The throughline across all of these is a documented payment plan with a track record, which turns “we owe the IRS” from a red flag into just another line item on your application.

What Lenders Actually See When They Pull Your File

Lenders do not receive a direct alert that says, “This borrower owes the IRS.” What they actually see comes through a few channels:

Your tax returns and transcripts, which you will likely be asked to provide during underwriting. Public records searches, which will show a federal tax lien if one has been filed. Your own disclosures on the loan application, since lying by omission here can tank an approval later in the process if it surfaces during underwriting.

This is part of why getting ahead of the issue matters. If a tax lien shows up mid-underwriting and you have not addressed it, that can stall or kill a deal that was otherwise moving smoothly.

The IRS Payment Plan That Can Make Or Break Your Approval

If you owe the IRS and you are planning to buy a house, setting up a formal IRS installment agreement is often the single most useful step you can take. Here is why it matters so much to underwriters:

It turns an undefined balance into a fixed, documented monthly payment. It shows a payment history once you have made a few on-time payments. It signals to the lender that the debt is being actively managed, not ignored.

Without this, your full IRS balance may remain an unresolved liability that is harder for an underwriter to factor cleanly. With it, that same debt becomes just another monthly obligation, like a car payment, that gets folded into your debt-to-income ratio.

Mistakes That Quietly Tank Loan Applications

A few patterns show up again and again with buyers who run into trouble:

Waiting until you are under contract to deal with an IRS balance, instead of addressing it before you start shopping. Assuming a small balance does not matter, even modest unpaid amounts can trigger a lien if ignored long enough. Not telling your loan officer about the IRS debt upfront, which means it surfaces later as a surprise during underwriting rather than being planned for from day one. Confusing “I filed an extension” with “I do not owe anything,” when in reality, unfiled returns can also raise questions during the mortgage process.

The buyers who move through this smoothly are almost always the ones who deal with the IRS side first, then walk into the lender’s office with documentation in hand.

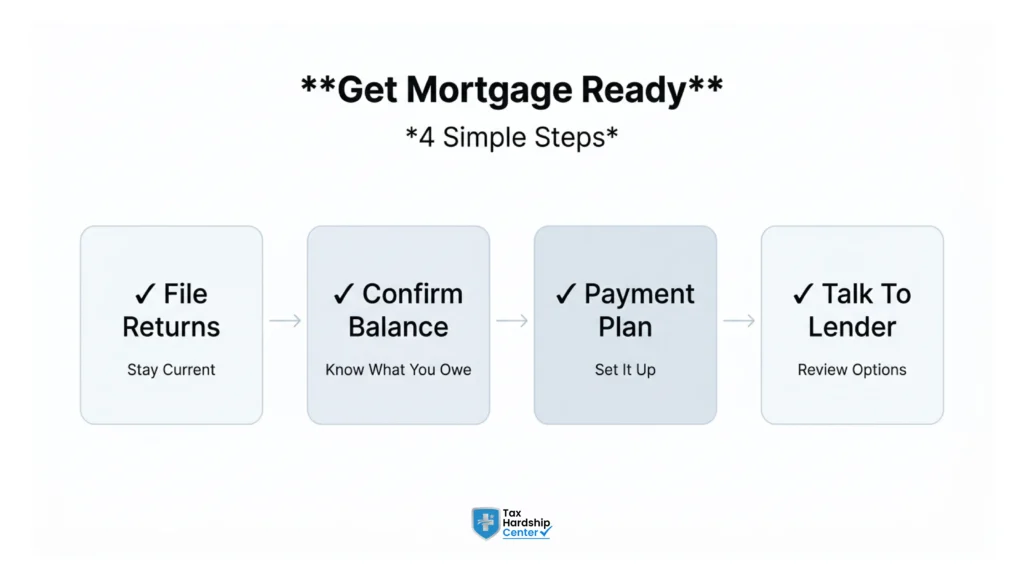

What To Do Before You Talk To A Lender

If you owe the IRS and buying a house is on your radar in the next several months, here is the realistic order of operations:

Get current on filings. If you have unfiled returns, that needs to happen first, since unfiled returns can complicate matters on both the IRS and mortgage sides. Find out your real balance and notice status. Pull your transcript or get help reviewing exactly where your account stands. Set up a documented payment arrangement if you haven’t already, and make a few on-time payments before you apply. Talk to your loan officer early and be upfront about the situation so they can plan the application around it rather than be blindsided.

None of this needs to take forever, but it does need to happen before you are deep into a home search, not after you find the house.

How Tax Hardship Center Helps You Get Mortgage-Ready When You Owe The IRS

If buying a house is on your timeline and you owe the IRS, the fastest path forward is to get your tax situation into shape so a lender can actually work with it, and that is exactly where Tax Hardship Center comes in. Our team reviews your IRS account, tells you honestly whether you are looking at a manageable balance or something closer to lien territory, and helps you set up a tax debt resolution plan that lenders recognize.

For most buyers in this situation, the move is a properly structured IRS payment plan, set up correctly from the start so it shows the payment history a lender wants to see. If your account has already been escalated, our team also helps with Offer in Compromise reviews and lien resolution, so the debt does not remain an open question during underwriting.

What makes this practical rather than theoretical is timing. The earlier you start this process relative to your home search, the more documented payment history you will have by the time you are ready to apply, and that history is often the difference between a smooth approval and a stalled one.

FAQs

Can IRS debt keep you from buying a house?

Not by itself. An undocumented balance, combined with a federal tax lien, can complicate matters, but a documented payment plan with on-time payments is generally workable for most loan types.

Can you get an FHA loan if you owe the IRS?

Often yes. FHA lenders typically allow borrowers with an IRS payment plan and a documented history of on-time payments to count that monthly payment in their debt-to-income ratio.

Will an underwriter see if I owe the IRS?

They may, through tax transcripts, public lien records, or your own application disclosures. It is better for the lender to hear it from you first than to find it during underwriting.

Does having a tax lien automatically disqualify me?

Not always, but most conventional lenders will require the lien to be paid, subordinated, or otherwise addressed before closing.

How much does an IRS payment plan affect my debt-to-income ratio?

It is generally treated like any other fixed monthly debt, such as a car payment, once it is set up and documented.

Should I tell my loan officer about my IRS debt before applying?

Yes. Telling them upfront lets them plan the application around it. Surprises that surface mid-underwriting are much harder to manage.

What if I have unfiled tax returns, not just a balance owed?

Unfiled returns should be addressed first, since they can complicate both your IRS standing and your mortgage application.

Conclusion

Owing the IRS does not close the door on buying a house, but it does mean you have homework to do before you start. The difference between an IRS balance that quietly rides along in the background and one that derails your mortgage almost always comes down to documentation, a payment plan, and timing. Get ahead of it, and this becomes a manageable part of your application instead of a last-minute scramble.

Key Takeaways

- Owing the IRS does not automatically disqualify you from buying a house

- A tax lien is different from simply owing money and carries more weight with lenders

- FHA and VA loans tend to be more flexible with documented IRS payment plans

- A formal installment agreement turns an open balance into a fixed monthly payment

- Lenders can find IRS debt through transcripts, public records, or your own disclosure

- Telling your loan officer early prevents mid-underwriting surprises

- Unfiled returns should be resolved before you start the mortgage process

- A few months of on-time payments on an IRS plan strengthen your application

- Waiting until you are under contract to deal with IRS debt is a common, costly mistake

- Getting your IRS account in order before house hunting saves time and stress later

If you owe the IRS and want to know exactly where you stand before you start house hunting, get a free case review, and we will help you build a plan that works with your timeline.